Dismantling Hyperliquid from five layers of financial stacking

Author:Baheet

Other Organiser

Institutional financial infrastructure is often well established. You can't start with the most productive products and then push backwards。

You have to start at the liquidation level and prove that it works under pressure and then unlock all the functions that depend on it。

The New York Stock Exchange did not add derivatives before having a well-functioning stock market. The Chicago Commodity Exchange also did not introduce options before launching futures。

This order is by no means arbitrary. The order of the grass-roots level determines the possibility of top-level buildings。

Hyperliquid knows this well。

The popular view of Hyperliquid as an ongoing DEX product. A permanent contract exchange that adds spot, tokenized assets and then predicts markets. A quick team。

That is correct, but it is completely off the point。

Hyperliquid is not creating a DEX and then adding products. They built a clearing engine and unlocked it layer by layer。

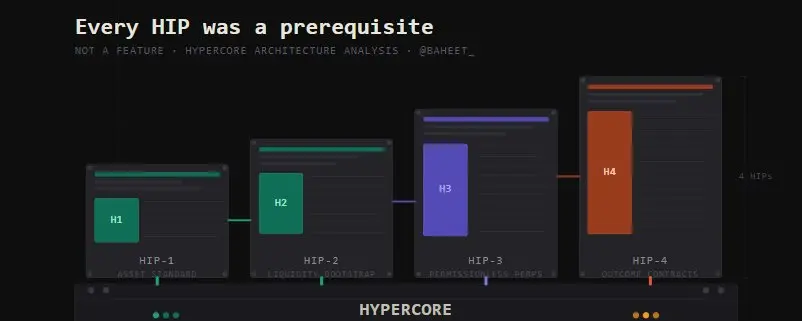

EVERY HIP IS A PREREQUISITE, NOT A SIMPLE FUNCTION。

And the HIP-4, the proposal that everyone calls the Polymarket Killer, is the ultimate proof that its goal was clear from the beginning。

Basis

BEFORE ANY HIP APPEARED, THERE WAS A DESIGN DECISION THAT DETERMINED EVERYTHING。

Hyperliquid constructs HyperCore as a specific application for perfecting market microstructures. Do not pursue universal programmability. Do not pursue the execution of any smart contract。

Focus only on market microstructures. Subsecond recognition, predictable implementation, clear state management, and a blended engine capable of addressing the demand for throughput for trade in specialized derivatives。

This is a deliberate constraint. By refusing to build a universal chain, Hyperliquid gave up the breadth of the developers competing with Solana。

In return, they have received a clearing engine that can reliably support institutional markets from day one。

THIS PERFORMANCE GUARANTEE IS BASED ON THE AMM-BASED DEX AND UNIVERSAL L1 THAT HAVE SPENT YEARS TRYING TO ADAPT BUT NOT FULLY REALIZED。

And every HIP that comes up is because HyperCore was first built in this way。

The constraints themselves are strategies。

HIP-1: ASSET STANDARDS

The first level is the most basic and least talked about。

The HIP-1 introduction of the Hiperliquid original currency criterion, which is the response of the agreement to ERC-20, is a key structural difference。

The currency under HIP-1 is not the smart contract balance that exists on the universal virtual machine. They are primary units of the HyperCore engine itself, and from that moment on, they can be traded directly within the high-performance interface infrastructure。

This distinction is far more important than it sounds。

At the Ether Workshop, the exchange of assets and transactions in such assets is an independent system and must communicate across contractual boundaries。

On Hyperliquid, assets and exchanges are the same system. There are no bridges between them, no delays in the introduction of cross-contract calls, and no implementation risk space of the kind that bothers the DeFi agreement, which is built on the common chain。

HIP-1 ADDRESSES THE AVAILABILITY OF ASSETS。

But its deeper function is to establish the environment in which HyperCore can be used as an original home in the financial language, rather than simply as an enforcement code。

Without this proof, everything that follows will not be credible。

HIP-2: GUIDED MOBILITY

Assets without liquidity are meaningless. That is the cold-starting problem, which stifles potentially more agreements than any technical failure。

You need to be mobile before a dealer, you need a dealer before a liquid provider shows up。

Most projects alleviate this contradiction through incentive schemes, token release schedules and municipal subsidies. These are not solutions. These are delays。

HIP-2 introduced Hyperlibure, a primary algorithm that is directly embedded in the protocol layer as a market mechanism。

Unlike AMM, which waits passively for the volume of transactions and exposes the provider of liquidity to an inevitable loss in the market settlement, Hyperliquidity automates the availability of spot assets in a way that makes economic models sustainable from the first block。

Any asset launched on Hyperliquid immediately has a well-functioning market. Not "finally." Be right there。

The significance of HIP-2 is not only at the operational level. It demonstrated that the problem of cold start-up could be solved by the HyperCore natives without the need to channel liquidity for outsourcing to market or incentive schemes。

THIS PROVED TO BE THE FOUNDATION FOR SUBSEQUENT DEVELOPMENTS. UNLICENSED AND SUSTAINABLE CONTRACTS WILL FACE SIMILAR COLD START PROBLEMS ON A LARGER SCALE. THE HIP-2 INDICATES THAT THE ENGINE IS FULLY CAPABLE OF RESPONDING。

HIP-3: PRESSURE TESTING

It is from here that this argument becomes indisputable。

HIP-3 broke the currency monopoly. Prior to this, each market on @HyperliquidX was deployed and managed by a core team, a centralized model that guaranteed quality but limited diversity。

THE HIP-3 INTRODUCED A PERMANENT CONTRACT FOR THE DEPLOYMENT OF THE BUILDER, ALLOWING EXTERNAL TEAMS TO DEPLOY A PERMANENT MARKET FOR ANY ASSETS WITHOUT THE NEED FOR PERMISSION。

Mobs, indices, front coins, small transactions. Anyone who can pledge a million hypes can build a market and operate within the infrastructure of HyperCore。

The results are immediate. The volume of open contracts has increased from less than $200 million to over $1.26 billion. The volume of daily transactions reached $5.9 billion。

EARLY PARTICIPANTS ACCOUNTED FOR UP TO 85 PER CENT OF THE MARKET SHARE IN THEIR RESPECTIVE CATEGORIES. BY ANY STANDARD, THE HIP-3 IS AN OUTBREAK。

BUT THE MOST IMPORTANT THING THAT HIP-3 DOES IS NOT CREATE TRADE VOLUMES。

It demonstrates that the creation of unlicensed markets on HyperCore can operate on a large scale under real conditions and can withstand real financial risks。

Stuck up the engine. Status management is holding up. Cost mechanisms have survived。

HyperCore has now passed pressure tests to cross dozens of assets while trading unlicensed derivatives。

HIP-3 IS THE EXAMINATION. THE HIP-4 IS THE POINT OF THE EXAM。

HIP-4: END GOAL

As a result, contracts appear to predict market products. It's really a close ring to the whole structure。

HIP-4 INTRODUCED CONTRACTS FOR FULL COLLATERAL, BINARY SETTLEMENTS, WHICH ARE TRADED BETWEEN 0 AND 1 AND ARE SETTLED AS ONE OF THE VALUES BASED ON VERIFIABLE EVENT RESULTS。

WITHOUT LIQUIDATION, ENTRY IS A FIXED RISK EXPOSURE WITH USDH AS THE CASH SETTLEMENT。

On the surface, this directly competes with Polymark and Kalshi. This framework is not wrong, but it underestimates the substantial changes that are taking place。

The deeper function of the HIP-4 is to extend the pricing capacity of HyperCore from assets and leverage to probability itself。

Before HIP-4, HyperCore can price the value of an asset and how much leverage the market can support. After HIP-4, it can price for whether something will happen。

This step complements the last link in the financial operating system。

Price orientation, leverage and probability are the three fundamental dimensions of financial risk. HyperCore can now express these three dimensions in the same clearing engine in a unified bond environment。

THAT'S WHY THE WHOLE-PORT GUARANTEE CAPACITY IS THE MOST IMPORTANT FUNCTION OF THE HIP-4, NOT JUST THE SURFACE FORECAST MARKET。

Dealers may use the same collateral while holding a leverage to continue the contract position and purchasing a result contract。

Unencumbered financing at the market level is projected to become active capital at the sustainable contractual level。

The two systems are not adjacent to shared balance sheets. They are the same system and represent the risk of different dimensions for the same liquidation infrastructure。

This could not be provided by any of the available forecast markets, as no existing forecast markets are based on certified derivative clearing engines。

Polymarket and Kalshi are binary bets of the settlement. And HyperCore is a financial operating system that now supports binary bets as one of its many original languages。

Comparison

When you look at how broader ecosystems deal with the same issues, Hyperliquid's sequence choices become clearer。

Most block chain infrastructure is designed around a core conviction: first, to give developers the largest programmable space, and then to keep up。

This is not a mistake. This is a rational bet, given the needs of the industry in its early years。

The programmability of the Taifeng has unlocked an entire class of financial experiments that could not have been achieved. Solana's throughput is proof that the chain system is close to the speed demand for real financial applications。

Both chains have made real breakthroughs and continue to carry some of the most important applications in the field of encryption。

However, the priority of programmable space over performance creates a specific technical debt。

When applications built on a universal chain develop sufficiently complex to require implementation at the institutional level, the chain must transform performance guarantees that it does not prioritize when laying the foundation。

It is difficult, expensive and never completely clean。

The implementation environment is not designed around market microstructures, and many Layer 2 amplifications or certifiers optimization do not fully compensate for the original design options。

Hyperliquid played the contrary. The design space is completely confined to market microstructures at the base level and is then unlocked on a liquidation engine that has been validated under real conditions。

The cost is the narrower exposure of early developers. The return is for every product based on HyperCore, which inherits the reliability of the lower level of liquidation。

This is not a criticism of the universal chain. This is an observation: what is the possibility when the financial infrastructure is designed around the market rather than programmability, based on the principle of primaryity。

Two different starting points, two different endpoints。

Final view

This team was never built for better money. That pattern is always too small。

Hyperliquid actually constructs a minimum viable technology warehouse for a financial operating system and is assembled in the only structured sequence。

First liquidation. Second asset. Liquidity third. Leverage number four. Probability five。

EACH LAYER IS A CONCEPTUAL VALIDATION OF THE NEXT LAYER. EVERY HIP IS A PREREQUISITE, NOT A FUNCTION。

The evidence itself is in that order。

The HIP-3 is not connected to the HIP-2 because the team has a good idea for a contract without permission. It follows because HIP-2 has proven that HyperCore can solve the cold-start problem。

THE HIP-4 IS NOT CONNECTED TO THE HIP-3 BECAUSE THE MARKET IS PROJECTED TO BE POPULAR. IT FOLLOWS CLOSELY BECAUSE HIP-3 HAS ALLOWED THE CLEARING ENGINE TO CONDUCT LARGE-SCALE STRESS TESTS ACROSS DOZENS OF ASSETS WITH REAL MONEY。

This sequence is in itself the best argument。

HyperCore can now price assets, maintain liquidity, express leverage and settle probability。

This is not a list of functions that fast-acting teams have put together over time. It is a structure with clear objectives。

THE FINISH LINE HAS ALWAYS BEEN HIP-4. IT TAKES ONLY FOUR PRECONDITIONS TO ARRIVE。

That's it