a16z: 7 maps that understand how monetization changes the nature of assets

It is much more than moving traditional assets into chains。

From:a16z crypto

Compiled Odaily Daily Planet (@OdailyChina); translated by Moni

Tokenize assets, known by many as “real world assets” (RWA), are changing the shape of assets, the way they flow, and the way financial systems are constructed。

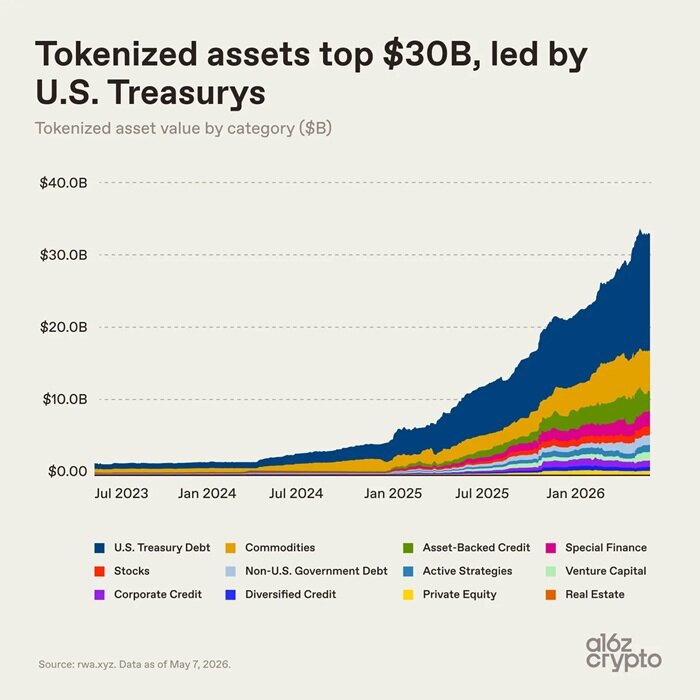

Just last month, the size of the monetized asset market was over $30 billion, which is now stable near about $34 billion (excluding the Stabilized Currency), a size roughly equivalent to a regional bank or the top university endowment fund, although still small compared to the global financial system, but sufficient for real impact。

YOU KNOW, TWO YEARS AGO, THE MARKET FOR MONETIZED ASSETS WAS LESS THAN $3 BILLION, BUT THEN THE MARKET CHANGED DRAMATICALLY: THE US GENIUS ACT BROUGHT A CLEARER FRAMEWORK FOR STABLE CURRENCY REGULATION, INSTITUTIONAL CHAIN INFRASTRUCTURE MATURED, AND A LARGE NUMBER OF FINANCIAL INSTITUTIONS BEGAN TO DEPLOY BLOCK-LINK TECHNOLOGY ALMOST IN THE SAME PERIOD – A FACTOR THAT LED TO A 10-FOLD INCREASE IN THE MONETIZED ASSET MARKET IN LESS THAN TWO YEARS. (NOTE: ALTHOUGH THE STABILIZATION CURRENCY IS NOT INCLUDED IN THE ABOVE STATISTICS, IT CONTRIBUTES SUBSTANTIALLY TO OVERALL MARKET GROWTH BY SIGNIFICANTLY SIMPLIFYING PAYMENTS AND SETTLEMENTS ALONG THE CHAIN

Seven maps will be used to analyse the reasons for the rise of monetized assets and the way forward。

Currencyized asset take-off: US debt became the biggest engine of growth

United States Treasury debt is the main driver of recent growth in the market for monetized assets。

The advantages of dollarization are clear: investors can hold robust interest-bearing assets in digital form, and the flow of transactions is more efficient and flexible; financial institutions can achieve settlements, mortgage asset transfers and smooth access to digital financial markets。

Encrypted investors can also generate hundreds of billion-scale markets through the active and idle use of national debt stocks to generate traditional currency market revenues and the dynamic deployment of a host of regulatory agencies, such as Belet and Franklin Templeton。

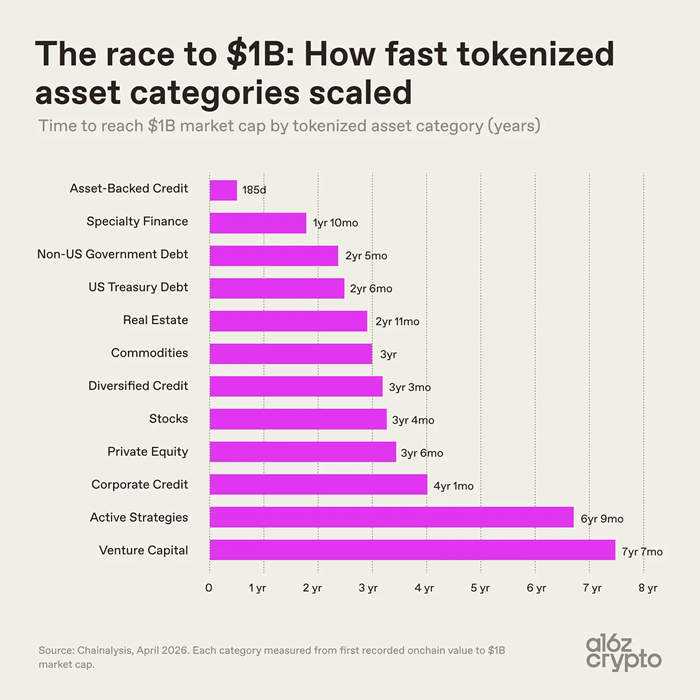

It is important to note that the disparity in the rate of increase between the various types of monetized assets stems from the technical and compliance difficulties of the chaining of different assets and depends on the market acceptance of the product after it has landed。

- Assets in the asset-support credit class are growing at a much faster pace, and such monetized assets include, inter alia, home net-value credit lines, loan bank notes, reinsurance contracts and special financial assets such as bitcoin mining instruments, with a market value of $1 billion within two years。

- Risk-investment-type assets take more than seven years to break the market value of billions of dollars, and the active-strategy-type asset cycle is similar, with complex structures, long investment cycles and higher operational and regulatory thresholds。

- The country's debt is at the right pace with large commodities, with a market value of between 2 and 3 years, which is now the dominant market category。

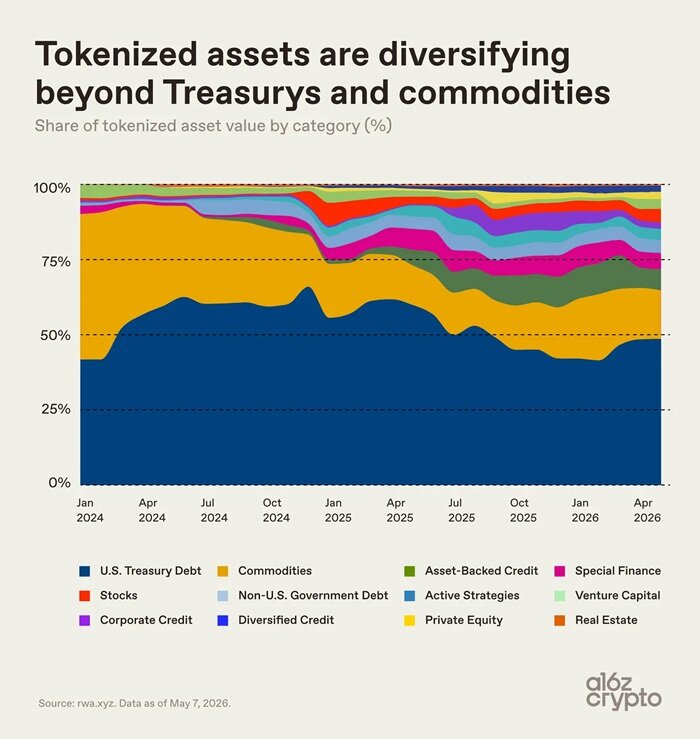

At the beginning of 2024, national debt and bulk commodities covered almost the entire market share of monetized assets. After 2024, the shares of credit, specialty finance, equities, etc. have increased steadily, but market concentration remains high. Currently, United States dollar-based national debt combined with large commodities accounts for about two thirds of the market share。

Market breakdown of monetized assets

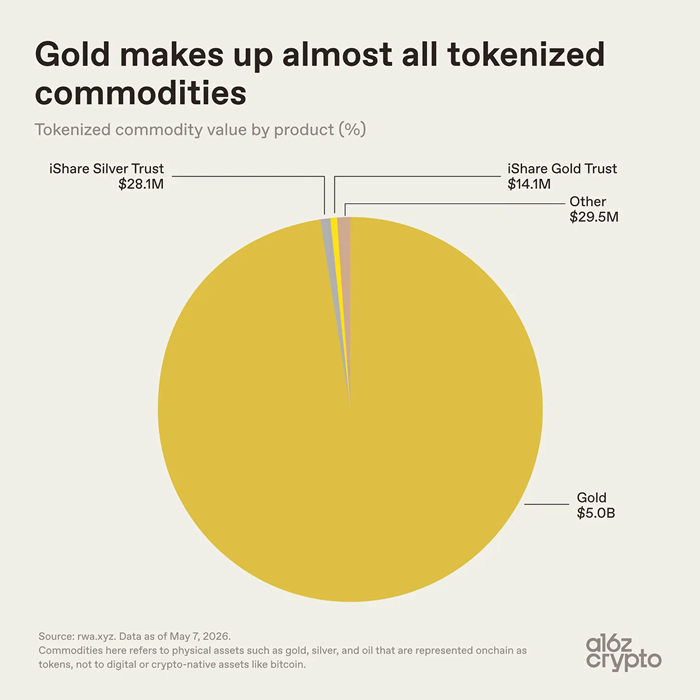

There is a high concentration of large commodity monetized asset tracks, with gold coins accounting for the vast majority of the total of $5.1 billion, of which $5 billion is in volume. For silver and other goods, the equivalent was only $57.6 million, or less than 0.01 per cent。

Gold is a natural monetized asset modelAt this stage, the market for bulk commodity coins is largely dominated by gold, because gold has globally uniform standards, is easily stored, is not easily depleted, and is itself traded on a long-term basis based on equity documents。

Moreover, investors in the encrypted market have traditionally favoured gold assets and Bitcoin was hailed as digital gold in the early years。Tether gold tokens XAUT, Paxos gold tokens PAXG, etc., map the ownership of gold in the vaults to the block chain, converting the physical gold interest into digital tokens that can be held in a wallet on the chain。

The market for monetized assets of crude oil, agricultural products and emerging goods such as energy, computing, etc. is extremely low and the industry is still in its infancy。

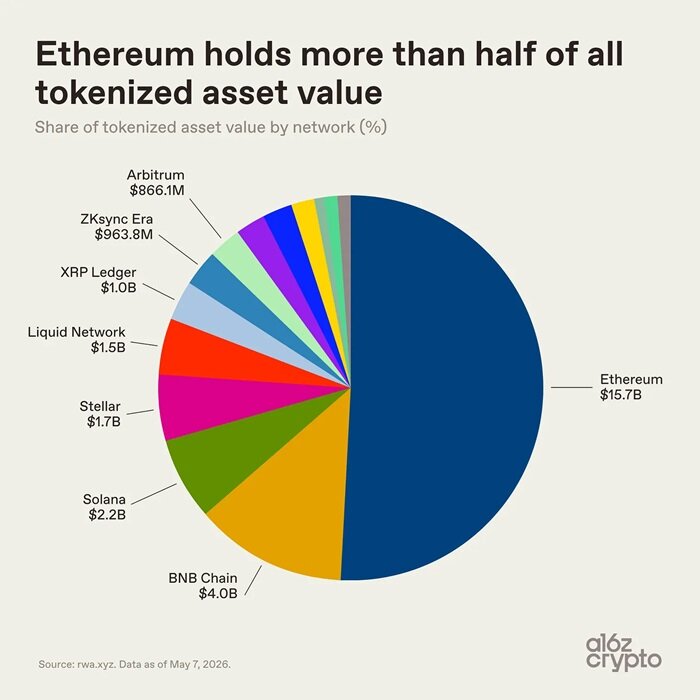

The ecological distribution of monetized assets is more diverse from the bottom of the public chain。With its decentralised financial pre-emptive advantages and institutional basis, the ETA continues to be at the forefront, carrying assets of $15.7 billion, and the market over half。

The rest of the monetized asset markets are spread across multiple public chains: the BNB Chain monetized asset market is about $4 billion, Solana is about $2.2 billion, Stellar is about $1.7 billion, Liquid Network is about $1.5 billion, and the XRP Ledger, ZKsync Era and Arbitrum are close to $1 billion。

The monetized asset industry has not been consolidated into a single public chain, with assets distributed across large regions in the chain ecology, based on transaction costs, liquidity, compliance requirements and business partnerships. However, the most illustrative data point is not the size of the monetized asset market ... but the way these assets are used。

Let's keep analyzing--

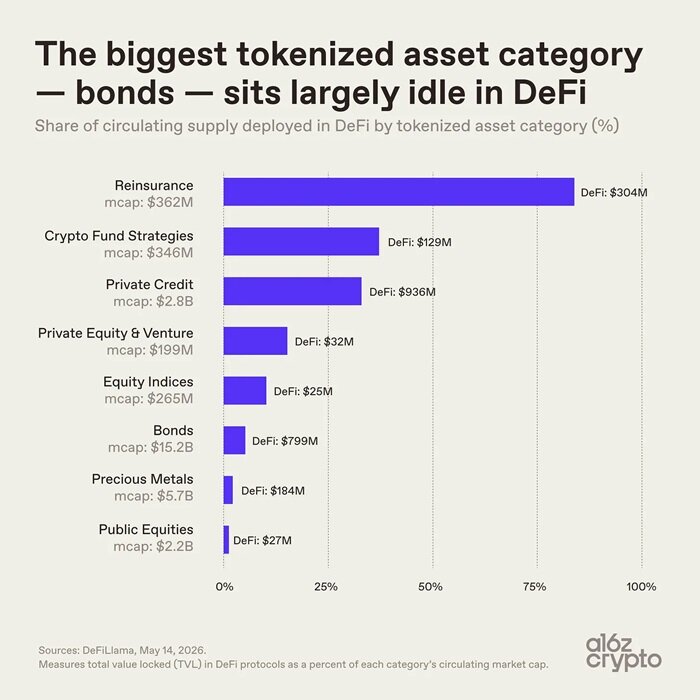

Most monetized assets do not currently have a “portfolio”

Market size is not the only core indicator, and the practical application value of assets is more relevant。

Bonds are the largest group of tokenized assets, with a market value of $15.2 billion, but only 5 per cent of the circulation is applied to the DeFi agreement, and only about $800 million. Precious metal monetization assets are similarly under-utilized, with most monetized assets being stored on the chain only and not yet a basic financial module that can be freely assembled and re-used。

Small-currency asset classes show the opposite: market value of $362 million in reinsurance tokens with a high rate of 84 per cent use of chain agreements; 33 per cent use of private credit tokens; and a combination of application scenarios for two types of asset from the beginning of the design. The fact that the core location of assets, such as sovereign debt and gold, is simply to simplify the holding and transfer of assets along the asset chain, without altering the original logic of the asset operation, also highlights the core differences in the proxy asset industry: the degree of originality in the chain of the various types of assets is uneven。

Some of the assets are free-flowing across the chain, while some use the block chain only as a bookkeeping tool and the transfer and portfolio function is limited。Most of the current monetized assets are by their very nature digitized assets, moving the accounts only to the chain without unleashing the portfolio potential。Portfolio is the core value of chain finance and the key to upgrading the financial system。

According to the Pantera Capital Ingenuity Index, over 70 per cent of the monetized asset chain is at its lowest level. A large number of tokens are only digital vouchers of the assets of the sub-linee entities, and the physical control of the assets remains on the basis of sub-linee books and intermediaries。

The monetized asset industry is still at an early stage of development: a purely formal chain-up digital record-keeping asset and an asset-based chain-based asset that fits deep-seated block-chain characteristics。

The technological infrastructure of the chain is well developed and the asset class is gradually rich, but the application of deep integration is only just beginning。

Future trends in monetized assets

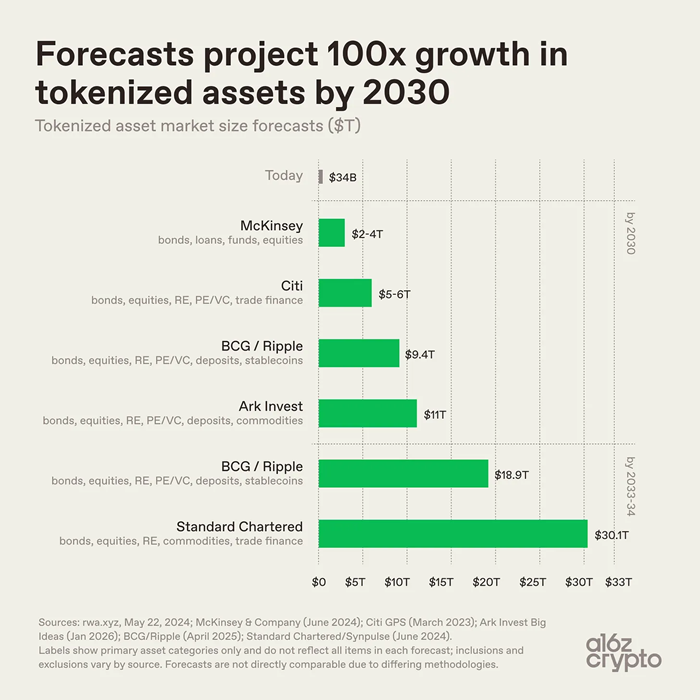

In-industry projections of the long-term size of the monetized asset sector vary, but overall the market is judged to be expanding。

- McKinsey projected a monetized asset market of US$ 2 to 4 trillion in 2030

- Ark Invest estimated the size of the monetized asset market at $11 trillion

- The Boston Consulting Consortium Ripple measures that the market size of monetized assets will reach $9.4 trillion in 2030, climbing to $18.9 trillion in 2033

- The Slag Charter Bank predicts that the monetized asset market will break $30 trillion in 2034。

On the basis of the above, it is estimated that the monetized asset market sector can grow hundreds of times faster than the current $34 billion market volume. Of course, the value gap does not stem from differences in the prognosis of the rate of spread of the industry, but from differences in statistical definitions. There are differences in the range of agencies ' statistics, covering asset classes, the inclusion of stable currencies and deposits, and the definition of tokenization, such as McKinsey Statistics Focused Bonds, Credits, Funds, Equitys; Scum-Bank Bank Pockets and Added Merchandise and Trade Finance; Boston Consulting and Rippo Additional Inclusion of Deposits and Stability Currency. However, although there are differences in statistical calibres, industry consensus on the size of monetized assets will usher in a leapfrogging。

In view of the global financial landscape, the volume of monetized assets remains minimal。

- The total size of global bonds was more than $14 trillion, with tokenized bonds only $15.2 billion, or 0.01 per cent

- The global market value of in-kind gold reached trillions of dollars, with $5 billion, or less than 0.02 per cent, in dollar gold

- Global equities have a market value of over $100 billion and monetized equities of $1.5 billion, or 0.001 per cent。

Today, the new track has grown steadily, with United States Treasury bonds, gold, private credit, etc. being clearly priced, demand stable, and simple assets owned, leading the way to the bottom of the chain. At this stage of the monetization process, the asset base properties have not been subverted, with only optimization of the asset settlement flow, and the deep interface between assets and the digital financial system is still being explored。

When more monetized assets remain at the digital level, it is difficult for assets to achieve programmable portfolio applications. The next stage in the industry is a hard-core challenge: to chain the more complex parts of the financial system and to more closely integrate monetized assets into a combination of original Internet-based financial infrastructure。