Gate Agency Weekly Report: BTC fund rate revised and CEX TradFi transactions surged (23 March-29 March 2026)

The market has been driven mainly by the escalation of the US-Iraq conflict over the past week, with the WTI crude oil rising by nearly 17 per cent, going back to $100, boosting the rate of return on US debt (10Y to 4.4 per cent), a stronger dollar, and an overall decline in the encryption market of over 6 per cent and VIX to 31. At the financial level, BTC and ETH ETF net outflows of about $500 million in weeks, followed by small returns. On the chain, Perp DEX TradFi transactions rose to about $17 billion, CEX TradFi was at a high start in the permanent trading phase; DEX was down as a whole。

1.Market Focus Interpretation

THE CENTRAL DRIVER OF LAST WEEK’S MARKET WAS THE SHARP ESCALATION OF THE US-IRAQ CONFLICT, WHICH, AS THE STRAIT OF HORMUZ WAS UNDER SUBSTANTIAL THREAT, BROUGHT WTI CRUDE OIL PRICES TO NEARLY 17 PER CENT WITHIN WEEKS, RETURNING TO THE $100 MARK. THIS, AT THE SAME TIME, TRIGGERED STRONG INFLATION EXPECTATIONS, LED TO HIGH RATES OF RETURN ON UNITED STATES DEBT AND SEVERELY HIT HIGH-VALUED TECHNOLOGY UNITS. THE DOLLAR INDEX WENT THROUGH THE 100-POINT MARK TO CONTAIN THE INCREASE IN GOLD. ENCRYPTED CURRENCY WAS SIGNIFICANTLY SOLD AS A HIGH-RISK ASSET, WITH A SINGLE WEEK DOWN BY MORE THAN 6 PER CENT. AS THE AMERICAN-IRANIAN CONFLICT ENTERS ITS FIFTH WEEK AND SHOWS NO SIGN OF RESOLUTION, THE TIDE CONTINUES. THE VOLATILITY AND UNCERTAINTY INDICATORS OF LAST WEEK REFLECT THE CURRENT MACROECONOMIC TONE. THE VIX INDEX STANDS AT 31.05, THE HIGHEST LEVEL SINCE THE OUTBREAK OF THE WAR, WHILE THE CNN INDEX OF FEAR AND GREED HAS FALLEN TO “EXTREME FEAR”, THE LOWEST LEVEL SINCE LAST NOVEMBER. THE BOND MARKET HAS FURTHER ADJUSTED ITS PRICING TO REACH 4.44 PER CENT OF ANNUAL US DEBT RETURNS, 30 PER CENT OF ANNUAL US DEBT RETURNS, AND THEN SLIGHTLY BELOW THAT LEVEL. THIS TREND REFLECTS THE MARKET'S DEEP-ROOTED EXPECTATION THAT “HIGH INTEREST RATES WILL LAST LONGER” AND THAT THERE IS NOW A GENERAL PERCEPTION IN THE MARKET THAT THE FED'S INTEREST RATE WILL BE REDUCED BY AUTUMN, WHILE THE RATE OF 25 BASIS POINTS THIS YEAR IS LIKELY TO INCREASE BY ABOUT 25 PER CENT。

2.Liquidity analysis

2.1ENCRYPT ETF NET FINANCIAL FLOWS

IN THE PAST WEEK, THE ENCRYPTED ETF FUNDS FLOW HAS SHOWN A CLEAR STRUCTURE OF “FIRST-OUT, THEN-REHABILITATION”: IN THE MID-WEEK PERIOD, THE FINANCIAL MOOD IS RAPIDLY WEAKENING, AND THE TOTAL NET OUTFLOW OF SPOT ETFS IS ABOUT $500 MILLION, OF WHICH BTC OUTFLOWS ABOUT $296 MILLION, ETH OUTFLOWS ABOUT $207 MILLION, AND DEPRESSIONS ARE CONCENTRATED ON TWO TRADING DAYS, 26-27 MARCH, SHOWING A CLEAR RISK OF INSTITUTIONAL PHASE DEPARTURE. THERE IS A MARGINAL RETURN ON THE WEEKEND, ENDING THE TREND OF MULTIPLE CONSECUTIVE DAYS. OVERALL, INSTITUTIONAL FUNDING REMAINS FOCUSED ON PRUDENT ALLOCATION IN THE CONTEXT OF MACRO-UNCERTAINTY。

2.2TradFi Liquidity

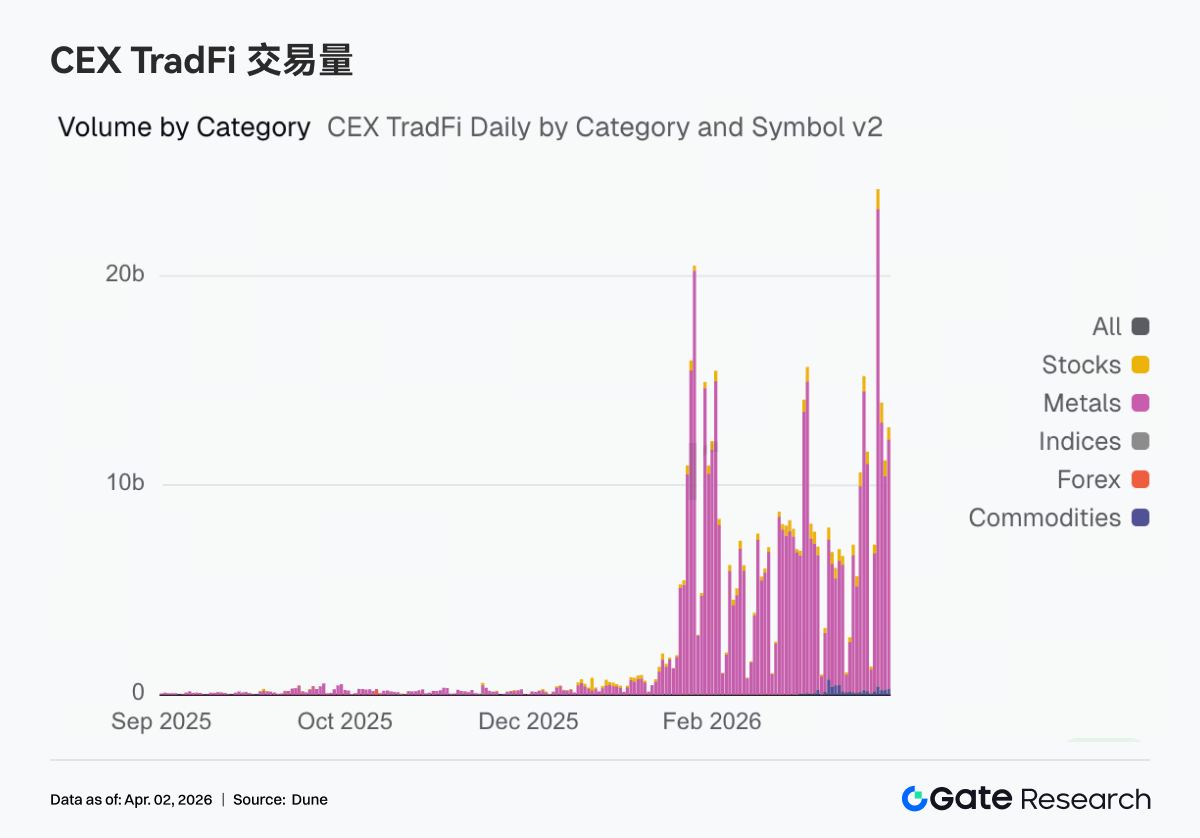

In recent weeks, the core of chain transactions has continued to revolve around macro-asset volatility. Perp DEX TradFi trading volume rose to $17 billion, with crude oil trading still having the highest weight but declining ring ratio and gold share rising again. The number of tradfi transactions on the CEX has soared that on March 23, there was an all-time high. There has been a significant increase in the various sub-groups, with the highest increase in the ring-to-metal ratio。

In the last week, PAXG's market depth changed with the structural features of “weak, strong, tail discharge”. At the beginning of the week, Delta, which is mostly negative, has fallen from the top to the top, showing that the market is dominated by net sales and that liquidity is being withdrawn; then, around 23 March, there was a round of concentrated push-downs, which corresponded to rapid price downsliding, creating a staged liquidity vacuum. There was a marked improvement in the depth structure over the weekend, with Delta turning to a constant positive and a significantly larger scale, indicating that the funds were beginning to take over and drive up prices。

The number of TradFi asset classes has expanded further in the past week, with three mainstream CEX in the TradFi asset classes (statistically only the TradFi and CFD boards, excluding durability contracts) increasing from 598 to 619 with an increase of 3.5 per cent. The most significant increase was in metals, from 22 to 31, with an increase of 40 per cent in ring; overall, only Gate had an increase in the number of TradFi asset classes last week。

3.Data Insight on Chain

3.1DEX trade cooling, Meteora maintaining height

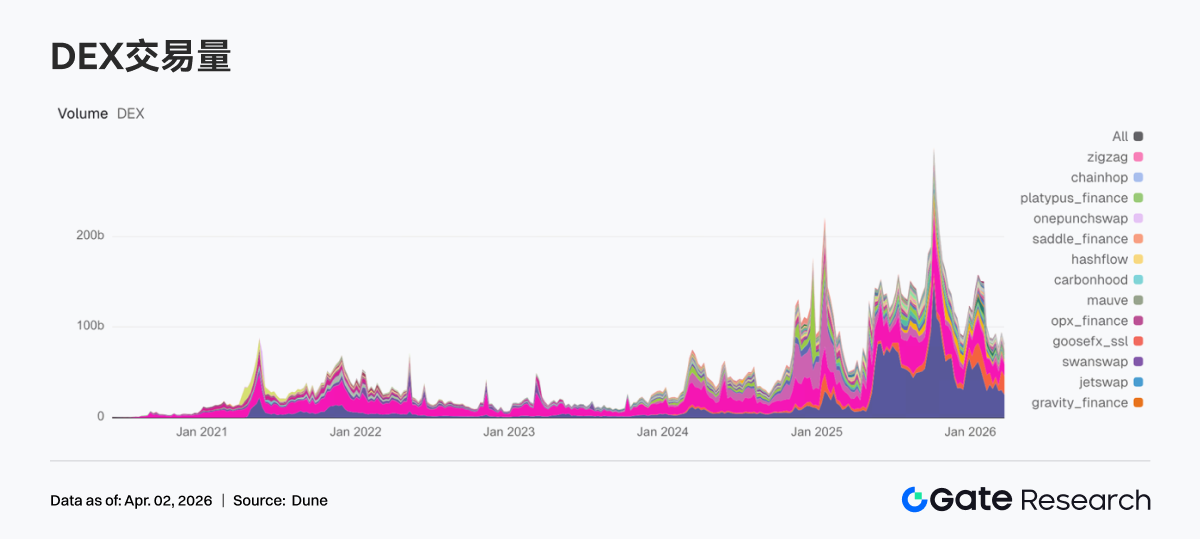

The trade heat returned from last week ' s rush to cooling and the head agreement generally fell. PancakeSwap and Uniswap week trades were down from last week, and demand for spot transactions in the mainstream chain was down overall. Solana is divided, Meteora remains slightly above $20 billion in trade volume, but marginal increase has slowed; Raydium weekly trade volume has declined by 50 per cent, leading to the largest decline in head DEX. Aerodrome, Humidifi, and Bisonfi all have different degrees of regression. In combination with the protocol, the PancakeSwap Infinity Architecture and the DLMM in Meteora remain the strongest efficiency labels, but the market is more focused on certainty of liquidity this week。

3.2STABLE TOTALS HIGH-SPEED, DAI SHOWS RESILIENCE

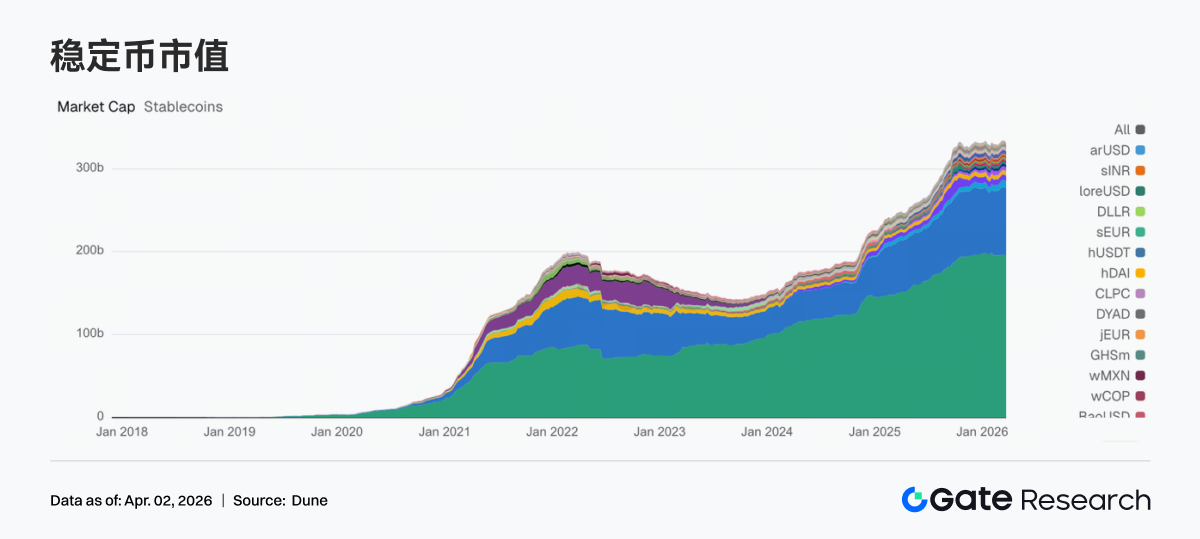

This week, there was no new external increment to the stabilization plate, and the entire high-platform. USDT is almost the same as the previous week. USDC has returned about $1.4 billion, and PYUSD has also fallen by almost $200 million, a slight fall this week in the demand for fixed currency for payment and settlement orientation. And what's more stable is the conventional stable currency, the DAI small growth, the USDS high. USD1, USDE, GHO have small fluctuations and a structural reconfiguration bias. Circe is still advancing the multi-chain expansion of USDC + CCTP in the recent past, but this week's data reflect a shift in the stability currency from payment settlement to deFi scenario resilience。

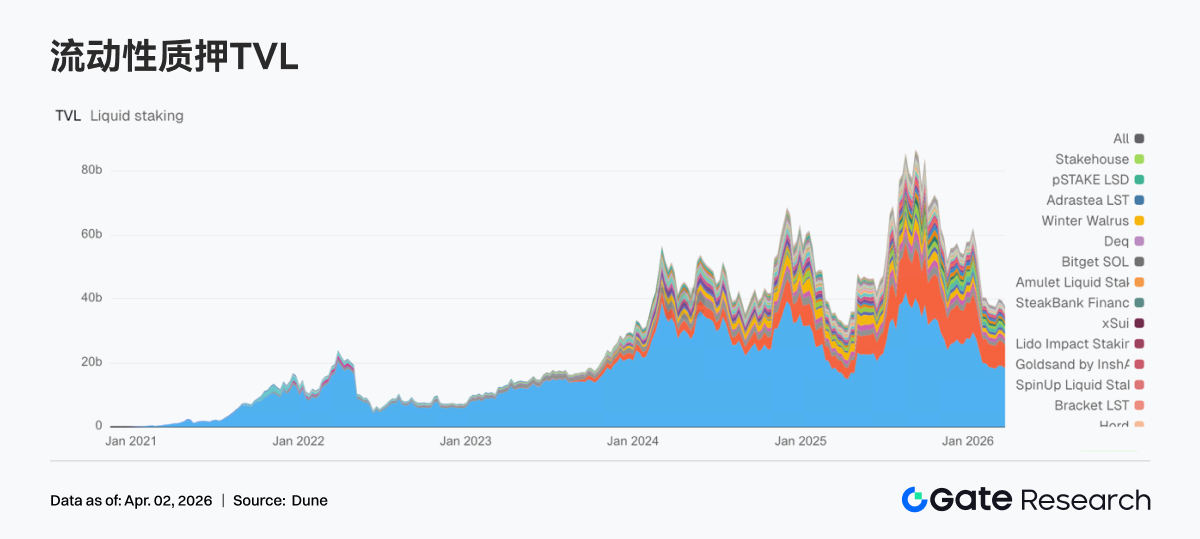

3.3LST PROTOCOL SYNCHRONIZED RETREAT, ETH AND SOL BOTH STARTING TO SLOW DOWN

ETH in the mobile plate this week synchronizes the speed reduction with the two main lines of SOL. As a result of the poor performance of ETH, ETH LST funds began to be phased down and Lido and Rocket Pool TVL were down. The expansion of the V3 and EarnETH/EarnUD vaults in Lido has already widened the product boundary, but in the short term TVL is more affected by market risk preferences and price fluctuations in pledged assets. Sol direction is the same, and Jito and Sanctum Validator LSTs are coming back. Overall, the week was a downward trend in the overall risk profile of the plate。

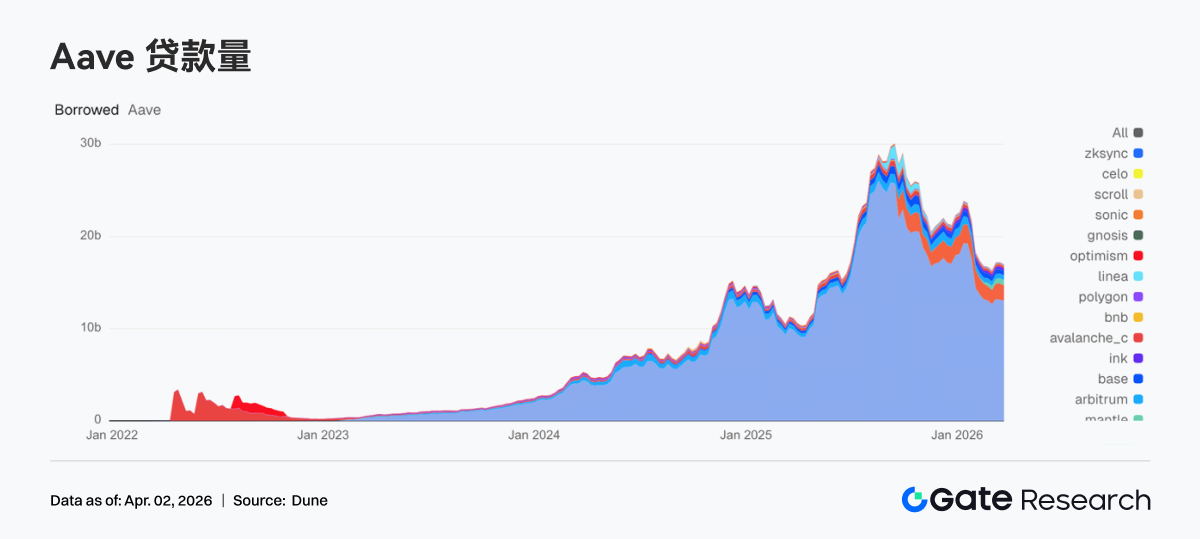

3.4Aave, loan rolls back, Mantle, into a few markets absorbing incremental amounts

This week, Aave's total loan balance is down slightly from the previous week. The main market of Etheum and Plasma both showed a decline of about $100 million, and the mainstream market showed signs of deleveraging. Multi-chain expansion has also slowed this week, and Base is backsliding with Arbitrum. Mantle is a small market of negative growth, with loans increasing from $555 million to $574 million, becoming the structural highlight of the week. Ink also slightly increased from $289 million to $292 million, albeit with a limited increase. Aave has recently advanced around V4 Hub-and-Spoke, where markets are pricing future cross-market liquidity efficiency, but the current funding has given priority to the total leverage for contraction, with a small incremental allocation to new sub-markets。

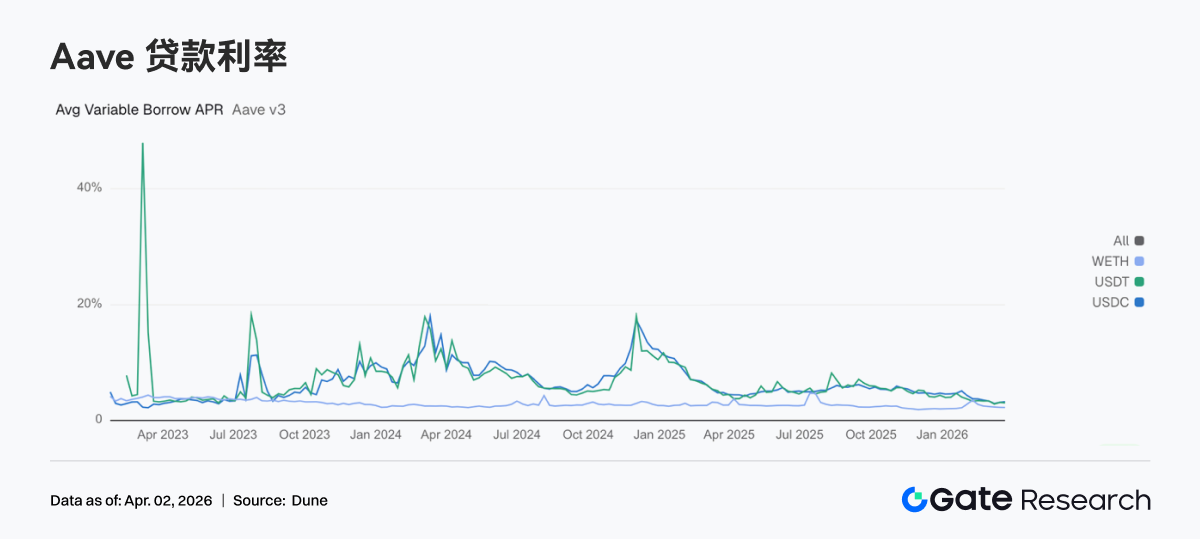

3.5Aave, interest rates on three core asset loans continue to split

On average, the USDC floating borrowing APR rose from 3.10 per cent to 3.23 per cent, and the demand for the dollar to stabilize the currency this week did not weaken as the total loan balance recedes. By contrast, USDT returned from 3.10% to 3.02%, and WETH from 2.25% to 2.23%. The current week’s finance is being kept more centrally on USDC while constricting broad risk exposures. From a strategic point of view, this is usually more of a USDC approach to mobility, collateral management and neutral strategy turnover. Together with the latest developments in Aave ' s governance, the V4 risk segregation and liquidity route framework is becoming clearer, and in the future interest rate splits between different assets will be more frequent and reflect real financial preferences。

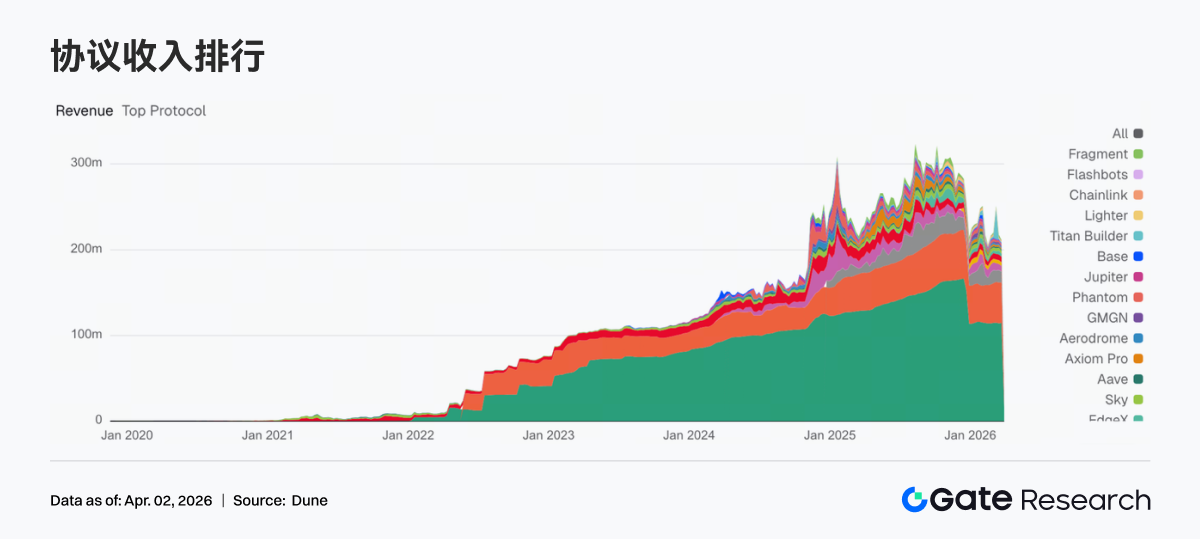

3.6Agreement revenue from transaction-driven regression stock

Revenues from trade-type agreements have generally cooled, and stable currency issuers remain the most stable profit centres. Tether and Circle's income remained high and stable that week. By contrast, Hyperliquid fell from $14.3.25 million to $12.627 million, Pump from $7.1452 million to $6.6905 million, and EdgeX from $45.534 million to $3.7969 million, and the cooling of trade activity has been channelled to revenue. Overall, the main line of revenue for this week ' s agreement is less dependent on short-term fluctuations。

I'm sorry.Derivative tracking

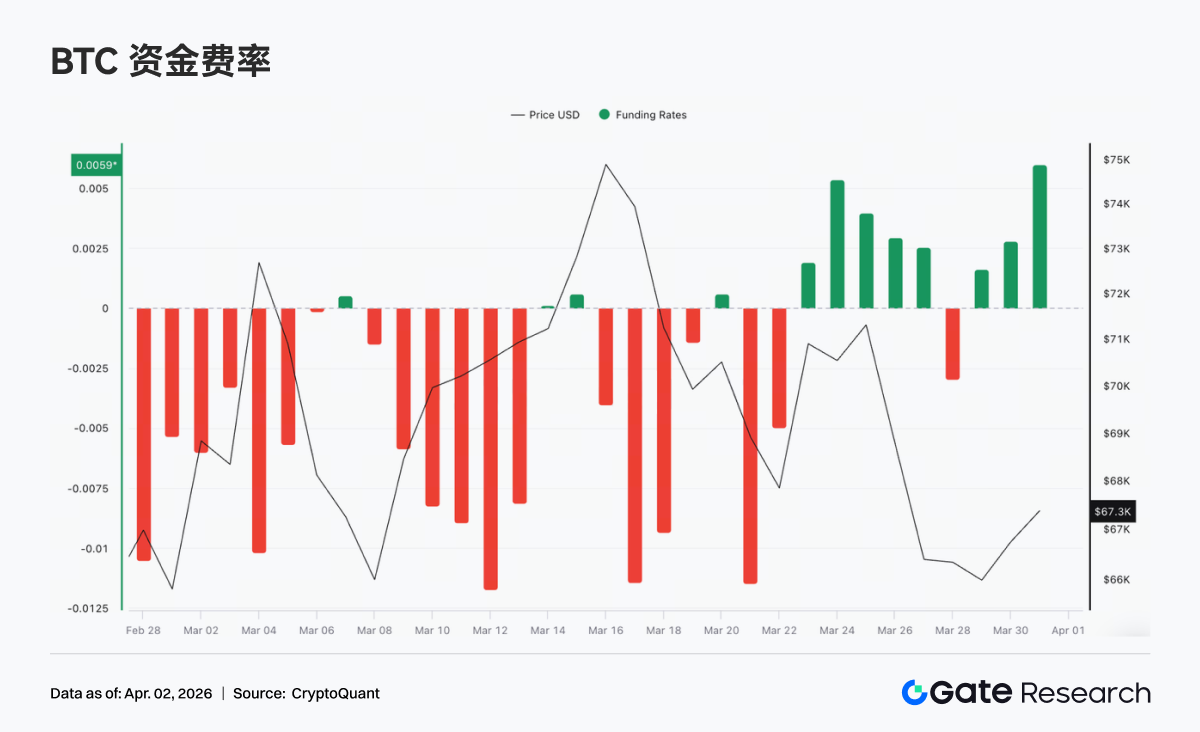

4.1The funding rate is shifting to a short-term overload, and the mood is changing to a test

THE BTC FINANCIAL RATE AS A WHOLE REFLECTS A SHIFT FROM REHABILITATION TO A SHORT-TERM POSITIVE AND THEN VOLATILE STRUCTURE. THE PRE-EXISTING EMPTY-HEADING PATTERN, WHICH HAD BEEN AT A CHRONIC NEGATIVE DEPTH, HAD BEEN SIGNIFICANTLY EASED, WITH FUNDING RATES BEING REVISED AND MAINTAINED FOR SEVERAL DAYS DURING THE WEEK (UP TO +0.005), MARKETS TURNING TO ACTIVE MULTI-HEAD TESTING, SHORT-TERM RISK PREFERENCES HAVING BEEN REPAIRED AND RESONATED WITH PRICE-STAGE REBOUNDS. HOWEVER, THIS POSITIVE RATE PHASE IS SHORT-LIVED AND LIMITED IN INTENSITY AND DOES NOT HAVE A TREND POSITIVE PREMIUM STRUCTURE。

4.2We'll have to wait and see

OVER THE PAST WEEK, THE BTC HOLD STOCK HAS EXPANDED TO THE TOP OF THE PRICE LEVEL FOR A WHILE, BUT HAS SINCE FALLEN RAPIDLY, TO AROUND $21B, FOLLOWED BY A MARKED DELEVERAGING IN THE MARKET; SINCE THEN, THE HOLD STOCK HAS NOT RETURNED TO ITS PREVIOUS HIGHS, BUT HAS MOVED DOWNWARDS IN THE INNER SHOCK RESTORATION AND OVERALL HUB OF THE 21B–$22.5B ZONE, WITH INSUFFICIENT ENTRY MOMENTUM AND LEVERAGE SHIFTING FROM EXPANSION TO CONTRACTION. OVERALL, THE CURRENT HOLD-UP STRUCTURE IS DOMINATED BY STOCK GAMES, WITH A LACK OF SUSTAINED RELEASE COOPERATION, AND MARKETS ARE STILL IN THE POST-LEVERAGING SHOCK RECONSTRUCTION PHASE。

4.3Long-term and high implementation prices, with multiple structures prevailing

BTC options are concentrated in mid-month contracts in April and June, with the market dominated by medium-term layouts; the structure of Call is significantly higher than Put, and the overall picture is still mixed. In terms of implementation prices, Call is concentrated in the $80,000 – $120,000 zone, while the Put is distributed in the $60,000 – $80,000 zone, forming a typical structure of up-to-up and down-to-up. It should be noted that the fact that the $60K-$70K area of Put is not too low indicates that the short-term defensive sentiment is growing while the market sustains expectations of medium-term increases。

4.4Skew is in a negative zone, and short-term defensive sentiment still dominates

Over the past week, BTC 25D Skew as a whole has remained in negative range (approximately -6 to -10), Put still has a premium vis-à-vis Call and the market continues to be overpriced for downside risk. Short-term (7D, 30D) fluctuations are more pronounced, with short-term lows and short-term repairs, reflecting repeated changes in short-term emotions, while the medium-term and long-term (60D and above) are relatively stable and the overall range is between -5 and -7, indicating little change in medium-term risk expectations. Overall, the fact that Skew did not continue to recover to near-neutral or positive values meant that the market was dominated by defensive configurations despite attempts at repair。

4.5Implied volatility stabilized and the market expected limited short-term volatility

Over the past week, the BTC DVol index as a whole has remained stable at 52 per cent - 55 per cent, with a small backsliding rebound, without an upward trend, and the market as a whole remains more restrained in its pricing of future fluctuations. While there was a marked fall in price during the period, the implied volatility went up only mildly, with no panic magnification, and the market did not regard the current adjustment as a high-risk event. Overall, IV and prices are somewhat dissensitized, reflecting a trader ' s preference for inter-temporal fluctuations over unilateral trends。

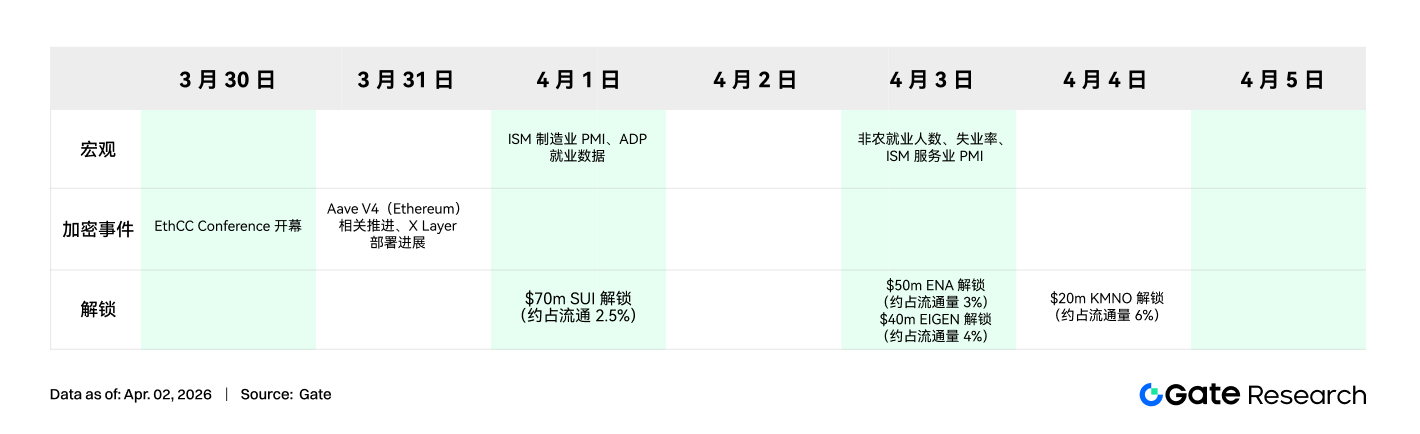

5.This week ahead

6.Gate Institutional Dynamic Update

Fine operation

1. advancement of data drive and precision management, precision targeting of customer needs and enrichment of customized solutions

2. sleeping user awakening significant

Financial operations

1. mortgage lending continues to grow at near cattle market level

2. & nbsp; BTC interest rate adjustment to drive new demand growth

Products and technologies

1. Websocket Contract BBO Real-time Delivery Full Open in April

2. AI step-by-step landing, institutional services entering AI ancillary operating phase

Activities and markets

1. & nbsp; CrossEx Progress Trading Incentive Scheme launched with maximum reimbursable contract return bill rate - 0.01% effective 9 April

2. & nbsp; April Hong Kong Web3 Federal Side Event

Data source:

• & nbsp; Investing, https://investing.com/currences/xau-usd-historic-data

• & nbsp; Gate, https://www.gate.com/trade/BTC USDT

• & nbsp; CMC, https://coinmarkcap.com/real-world-assets/? type=all-tokens

• & nbsp; Coinglass, https://www.coinglass.com/pro/depth-delta

• & nbsp; Dune, https://dune.com/gatesearch/gate-interactive-weekly-report

• & nbsp; CriptoQuant, https://cryptoquant.com/asset/btc/chart/derivatives

• & nbsp; Amberdata, https://pro.amberdata.io/options/deribit/btc/current/

Gate InstituteIt is a comprehensive block chain and encrypted monetary research platform that provides readers with in-depth content, including technical analysis, hot spot insight, market review, industry research, trend forecasting and macroeconomic policy analysis。

Disclaimer

The investments in encrypted money markets involve high risks, and users are advised to conduct independent research before making any investment decisions and to fully understand the nature of the assets and products purchased。Kate& nbsp; is not liable for any loss or damage caused by such investment decisions。