The five giants look forward to the week: What is the market looking at

what really depends is not just a single company beat, but whether the technology main line will continue to be underpinned by fundamentals。

Foreword: This is not a regular financial week, it's a centralized validation of the main technology line

This week, the U.S. Unit will usher in a truly “core asset test week”. Microsoft, Google, Amazon, Meta will beAfter 29th of AprilWe'll publish the financials and the apples will be30th of AprilPUBLICATION OF UPDATES ON PERFORMANCE. SINCE THESE FIVE COMPANIES COVER ALMOST ALL OF THE MOST IMPORTANT CURRENT TECHNOLOGIES, SUCH AS CLOUD COMPUTING, ADVERTISING, CONSUMER ELECTRONICS, ELECTRICIANS, ENTERPRISE SOFTWARE AND AI INFRASTRUCTURE, THEIR FINANCIAL IMPACT IS NOT JUST THE STOCK ITSELF, BUT WHAT THE WHOLE NANO-FINGER AND TECHNOLOGY BOARD IS WILLING TO TRADE NEXT。

If the main market lines of the past few months are condensed into one sentence, it is:LARGE PLANTS ARE CONTINUOUSLY ADDED TO AI, AND THE MARKET CONTINUES TO BUILD ON TECHNOLOGY MASTER VALUATIONS。& nbsp; but the problem is that, after valuation has risen to this position, the market is not satisfied with the fact that the company is investing in AI itself, but is beginning to ask more practical questions:Have these investments continued to bring about growth in cloud operations? Did it bring about an increase in advertising efficiency? Did you hold on to the terminal needs? And, most critically, has the beginning been made clearer in terms of income, profits and future guidance。

Microsoft gave the middle of the quarterly revenue guide last season$81.2 billionAzure Speed Guide37% - 38%; Alphabet has identified capital expenditure plans for 2026175 billion - 185 billion United States dollars; Amazon projected capital expenditure for 2026 Approximately$200 billion;Meta lifts the 2026 capital expenditure target to$115 billion - $135.0 billionI don't know. These figures themselves show that the real theme of this financial roundIt is still “high investment and will continue to be paid for by the market”。

I. What does the market really want to know about this round of financial returns

1.DO YOU WANT TO CONTINUE SPENDING MONEY ON AI

Because many AI infrastructure chains are now valued on an essentially premise: Microsoft, Google, Amazon, Meta, these super-buyers will continue to write down, continuously expand data centres, continuously purchase computing, network and power infrastructure. If management releases any cautious signals of capital expenditure at the financial conference, they will not be affected only by themselves, but by the AI industry chain as a whole。

2.Can the two cash machines, Cloud and Advertising, hold on

Microsoft Azure, Google Cloud, AWS are the most direct windows for observing enterprise IT expenditures and AI needs, while Google and Meta ' s advertising business represents the core cash flow resilience of Internet platforms. If the clouds were stable and advertising stable, the market would continue to believe:Even with high capital costs, the technology giant is still capable of supporting future investments with mature businessI don't know。

3.AI, IS IT STILL A STORY OR IS IT STARTING TO BE A PROFIT

These five companies are all talking about AI, but the way they validate AI is not the same: Microsoft watching companies pay, Google watching clouds and searching, Amazon watching AWS and self-study chips, Meta watching advertising efficiency, Apple looking at terminal entrances and ecological locations. It's also because it's a different cut。

What are the questions to be answered by the five giants

1.MICROSOFT: THE FIRST ANSWER IS NOT GROWTH, BUT HOW FAR IS AI COMMERCIALIZATION GOING

Of the five giants, Microsoft is the best model room in the AI cycle. The market has been willing to continue giving Microsoft premiums over the past year, not only because it is the cloudhead, but also because it is seen as the company that is most likely to be the first to actually do business with AI. Copilot is embedded in Office, developing tools, business flows, and superseding Azure as a bottom cloud platform. Microsoft has the advantage not only of providing modelling capacity, but also of reaching out to the most expensive corporate clients。

So the most important thing for Microsoft is not just the rate of growth, but..DOES AI CONTINUE TO ENHANCE THE “PENETRATION” OF INCOME STRUCTURESI DON'T KNOW. THE MARKET IS NOW EXPECTED TO BE ABOUT FY2026, THIRD QUARTER COLLECTION$81.4 billion or soEPS ADJUSTEDUSD 4.07; and the income guidance area given by Microsoft last season is806.5 billion-81.75 billion dollarsThis is largely close to market expectations。

What is really worth looking at is whether Azure's growth can continue at a higher speed, and whether Copilot's IA products have given any clearer commercial progress. Last season Microsoft revealed the growth of Azure and other cloud services39%And give this season37% - 38%The growth guidelines of & nbsp; mean that the market's core expectations for this financial statement are not “growth or no” but “are AI still driving growth acceleration”。

If Microsoft continues to prove that the budget for the AI tool has not shrunk for business clients, that the Azure AI contribution is increasing, then the market will see it as the “AI commercial first delivers”, and that the associated enterprise software, cloud and data centre chains will continue to benefit. Conversely, if Azure is not further reinforced and capital expenditure pressures remain high, the market will refocus its attention on input output。

In other words, Microsoft's most critical financial performanceNOT TO PROVE THAT AI IS IMPORTANT, BUT TO PROVE THAT BUSINESSES ARE REALLY PAYING FOR AI。

2.Google: Claude Next

Google's situation is more like a “development of cloths before taking a quiz” than Microsoft. In the immediate aftermath of Claude Next 2026, Google focused at the Congress on a number of signals about AI inputs, Gemini Enterprise, Vertex AI, TPU and infrastructure inputs, which did lead to renewed expectations of Google Cloud. But the Assembly spoke of a vision, and the financial report looked at delivering, and Alphabet's most important pressure on the press this time came from the fact that it had to turn “story” into “numbers” as soon as possible。

The unique thing about Google is that it is not a pure cloud company, nor is it a pure advertising company, but that it is simultaneously stepping on two main lines: Google Cloud and AI Foundation, and Search and Advertise the mature cash flow machine. The market is currently expected to be roughly Q1$10.6 billion-10.7 billionEPSAround 2.73 United States dollarsI DON'T KNOW. BUT WHAT MATTERS MORE THAN SIMPLY LOOKING AT THE COLLECTION AND THE EPS IS WHETHER THREE THINGS CAN BE ESTABLISHED AT THE SAME TIME:Google Cloud continues to grow, capital spending continues to rise, and search advertising remains robustI don't know. In February of this year, Alphabet was clearly given175 billion - 185 billion United States dollars& nbsp; Capital Expenditure Planning 2026; Last season Google Cloud Income Growth48 per cent to$17.7 billion, the annual running scale has exceeded$70 billionThe backlog of orders is also rising rapidly. In other words, the market has partially factored in the price of "Claud is strong and AI is heavily invested."。

So the real question of Google's examination is not whether Cloud can grow, but whether it can keep the profit base of search and advertising while continuing to invest heavily. If all three lines are stable, Alphabet is likely to be redefined by the market as the Al platform tap that currently has the most “balancing” feature; but if there is any relaxation between Claude, Capex and the ads, the market’s demands on it will immediately rise。

Google is the representative of the newspaperIt is not whether a single business is ahead of expectations, but whether the financial report can catch up with expectations after Claude Next。

3.AMAZON: IT'S NOT AWS, IT'S "BLOWING MONEY AND MAKING MONEY."

IT'S NOT LIKE MICROSOFT OR GOOGLE. THE MARKET CERTAINLY LOOKS AT AWS, BUT IT'S NOT ENOUGH TO LOOK AT AWS, BECAUSE AMAZON IS NOT A SINGLE CLOUD PLATFORM COMPANY, WITH THE LINES OF RETAIL, ELECTRIC, LOGISTICS, ADVERTISING, AND CASH FLOW. IN OTHER WORDS, THE MARKET LOOKS AT MICROSOFT AND GOOGLE, MORE AT AI AND BUSINESS DEMAND, AND AT AMAZON, AT WHETHER A COMPANY CAN CONTINUE TO BET ON THE FUTURE WITHOUT SACRIFICING THE QUALITY OF CURRENT PROFITS。

ACCORDING TO THE DISCLOSED INFORMATION, AMAZON INPUT TO AI IS VERY RADICAL. THE COMPANY CLEARLY STATED IN ITS QUARTERLY FINANCIAL STATEMENTS IN FEBRUARY THAT CAPITAL EXPENDITURE PROJECTIONS FOR 2026 APPROXIMATELY$200 billion, mainly for AI infrastructure; CEO Andy Jassy then added in the shareholders ' letter that the AI service annualized revenue performance rate for AWS has exceeded$15 billion, AND AWS TOTAL ANNUAL INCOME OPERATING RATES AROUND$142.0 billionI don't know. At the same time, the annual revenue performance rate of self-study chip-related operations such as Trainium, Graviton and Nitro has exceeded that of the annual production rate$20 billionI DON'T KNOW. THIS MEANS THAT THE AMAZON IS NOT JUST TALKING ABOUT "WE'RE DOING AI," BUT "WE WANT AI TO BE THE CORE ENGINE OF THE NEXT AWS GROWTH."。

BUT THE PROBLEM IS THAT THE AMAZON CANNOT SPEAK ONLY OF THE FUTURE. AWS IS ITS ENGINE OF GROWTH AND PROFIT, BUT THE RETAIL AND COMPLIANCE SYSTEMS DETERMINE WHETHER OVERALL PROFIT MARGINS ARE MAINTAINED. LAST SEASON AWS INCOME GROWTH24% to$35.6 billionALL YEAR ROUND, AWS CAMP$12.8 billion;-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------$16.5 billion-21.5 billionTHE MEDIAN IS NOT RADICAL. THIS MEANS THAT THE MARKET LOOKS AT THE AMAZON THIS TIME, NOT JUST AT THE AWS GROWTH ITSELF, BUT AT A MORE REALISTIC QUESTION:HIGH-INTENSITY AI INPUT, WILL IT AGAIN REDUCE THE PROFIT MARGIN if the answer is no, the amazon can be seen as an example of “high-input versus high-quality profits”; if the answer starts to blur, then the market's patience for it will decline。

Amazon is really hardIT'S NOT PROOF THAT AWS IS GROWING, IT'S PROOF THAT IT CAN CONTINUE TO INVEST IN THE FUTURE AND MAKE MONEY NOW。

I'm sorry.Meta: The market is willing to continue to pay, not because it spends much, but because it spends efficiently

Of the five giants, Meta's logic is most likely to be miscalculated. On the face of it, Meta, like several others, is making a crazy increase in capital spending; but the market is willing to give it a high valuation, not because it has a bunch of AI presses, but because it has proven many times that AI can actually improve its core business directlyAdvertisingI don't know. For Meta, AI is not a new story that hangs on far away, but more like an ongoing "efficiency revolution."。

According to last season's financial report, Meta's advertising business remains the foundation for all of its AI inputs. In the fourth quarter of 2025, Meta's advertising exposure increased over and over again18%Increase in average advertising prices6%Capital expenditure reached throughout the year$72.2 billionI don't know. Meanwhile, the company has further increased its 2026 capital expenditure$115 billion - $135.0 billionAnd the total cost is up162 billion - 16.9 billion dollarsI don't know. This means that what investors really want to see now is not how much Meta spends, but whether it continues to be replaced by greater recommendatory capacity, longer user stays, better advertising orientation and more efficient advertising。

The pre-fiscal market is expected to be roughly Meta's quarter camp. Take it$5.546 billionIncome from advertising$53,930 millionEPSUS$ 6.73I don't know. These figures are of course important, but what really determines market sentiment is the bottom of the logic chain:AI recommends optimisation, more user stay, more advertising, more advertising, more advertising, more advertising, more marketing, more markets, more marketsI don't know. If this chain continues, Meta will continue to be seen as one of the best examples of “AI to improve the efficiency of mature operations”; in turn, if advertising increases at a slower pace, while capital expenditure is under increasing pressure, the market will begin to look more critically at its input tempo。

In other wordsMeta is not answering “AI is not worth voting”, but is it saying that AI continues to make the ad machine more profitable。

5.Apple: The market doesn't ask it to be the most aggressive, just to make sure it doesn't fall

IF THE FIRST FOUR OPERATE IN SOME WAY AROUND "AI INPUT AND COMMERCIALIZATION", THE APPLE LOGIC IS COMPLETELY DIFFERENT. THE MARKET DOESN'T EXPECT APPLE TO TELL THE MOST RADICAL AI STORY IN THIS NEWSPAPER, NOR WILL IT MEASURE IT WITH "HOW MUCH CAPITAL YOU SPEND." THE KEY QUESTION FOR APPLES IS ONE: IS IT STILL HOLDING THE MOST IMPORTANT TERMINAL ENTRANCE IN THIS ROUND OF AI CYCLES。

And that's why apples fall into a more subtle combination:HARDWARE REQUIREMENTS, SERVICE OPERATIONS, AI STRATEGIC CLARITY。 apple's guidance in the last quarter of january's financial statements is that the current season's income is growing over and over13-16%; according to this guidance, the revenue is roughly earned$10.78 billion-1110.7 billion interval. markets are now expected to be more or less the same$10.89 billionEPSUSD 1.94-1.95;S& P Global preview shows that market expectations for iPhone revenue for this season are about$56.5 billionI don't know. At the same time, apples grew globally in the first quarter of 20265%And take the world in a quarter21%Share of iPhone exports in the Chinese market also increased at the same time20%I don't know. This means that, at least before the financial statements, the market did not see a signal of a marked shortfall in the demand for apple terminals。

SO THE REAL FOCUS OF APPLE'S OBSERVATION THIS TIME IS NOT WHETHER IT WILL EMPHASIZE AI INPUTS AS LOUDLY AS MICROSOFT OR GOOGLE, BUT WHETHER IT WILL CONTINUE TO PROVE THAT EVEN THOUGH THE PACE IS NOT THE MOST RADICAL IN THE AI CYCLE, IT STILL HAS THE MOST IMPORTANT TERMINAL ECOLOGY, THE STRONGEST USER BASE AND THE MOST STABLE AND HIGH-QUALITY SOURCE OF PROFITS. AS LONG AS HARDWARE DEMAND IS STABLE, SERVICE OPERATIONS ARE STABLE, AND AI IS CLEARER THAN IN THE PAST, THE MARKET WILL NOT EASILY EXCLUDE APPLES FROM THIS CYCLE OF TECHNOLOGY。

Apples representNOT THE FIRST AI COMMERCIALIZATION TO BE REALIZED, BUT: THE VALUE OF THE FINAL ENTRY IN THE AI CYCLE IS STILL IN ITS HANDS。

To put five companies together, the market is actually doing a "cross-check"

If one looks at a single company, this week is, of course, five separate financial statements; but if they are put together, the market is actually performing a larger cross-check. Microsoft looks at AI as if it has become a closed business fee; Google as to whether the General Assembly narrative can be implemented quickly to the double payout of Cloud and advertising; Amazon as to whether high inputs can coexist with high-quality profits; Meta as to whether AI continues to improve the efficiency of mature operations; and Apple as to whether the terminal entrance and ecological positions remain secure。

Five different lines seem to point to the same problem:Whether the current high valuation of the leading technology is based on real realization or still more on expectations。& nbsp; If most of the answers given by the five companies are positive, the market would be more willing to continue to push the AI, cloud, advertising platform and terminal eco-related directions; but if there is a clear division, the market will move from a “general upscaling” to a “reward only the strongest deliverers”。

IV. What can markets repricing after financial reporting

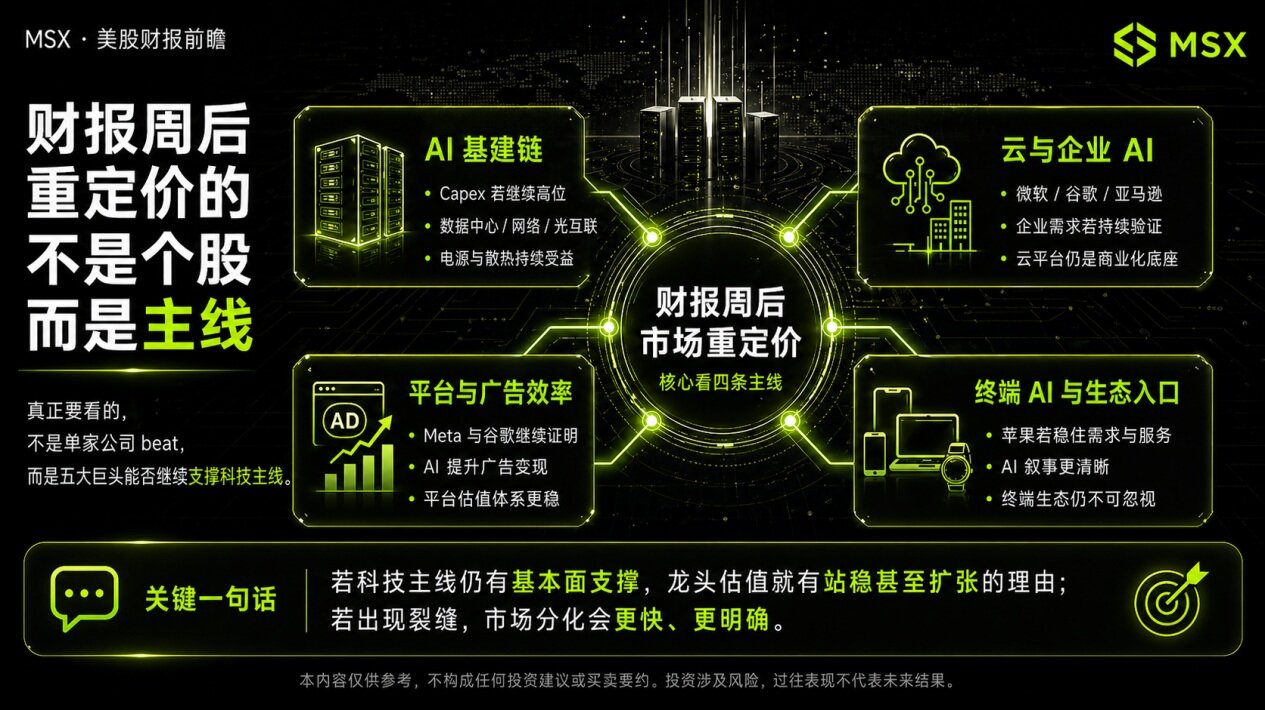

After the financial week, the market is most likely to re-pricing not a single company, but a few major lines。

First of courseAI CAPITAL CHAIN: Data centres, networks, light interconnections, power supply and heat dispersion will continue to be supported by basics if the capital expenditure calibre of large plants continues to be high。

Number two:CLOUD AND ENTERPRISE AI: MICROSOFT, GOOGLE, AMAZON WILL CONTINUE TO VIEW CLOUD PLATFORMS AS CORE INFRASTRUCTURE FOR THE COMMERCIALIZATION OF AI AS LONG AS BUSINESS NEEDS CONTINUE TO BE PROVEN。

Number three:Internet platforms and advertising efficiency: Meta and Google will also be more stable if they continue to demonstrate that AI is making advertising more efficient。

And finallyTERMINAL AI AND ECOLOGICAL PORTAL: HOW APPLES CAN STABILIZE DEMAND AND SERVICE OPERATIONS, WITH CLEARER AI NARRATIVES, AND END-OF-PIPE ECOLOGY WILL REMAIN A PART OF THE MARKET THAT CANNOT BE IGNORED。

so, what's really worth looking at this week is not what's ahead of us alone, but whether the five companies together can continue to prove one thing:There is still enough solid foundation behind this technology line。 if the answer is yes, there is a reason for the technology tap to remain stable and even expand; if the answer cracks, then the market will begin to divide faster and more clearly。

Risk tips: This paper is for information sharing and investor education only and does not constitute any investment proposal. VIX and related products are highly volatile and complex, and historical performance does not represent the future and does not mean that markets simply repeat the same path. Investment requires careful decision-making that combines its own risk tolerance。