$79,000 bitcoin blocked, $65-70 million or critical support

The demand for spot warms up, but the futures market has a clear mood and the pattern of inter-temporal shocks continues. 。

Photo by Glassnode

Original: AididiaoJP, Foresight News

Bitcoin is still being suppressed below the real market average, with a support position between $65,000 and $70,000. The pressure on spot sales is easing and financial flows are stabilizing, but demand remains weak. The empty silo left room for run-off in the market for inter-temporal shocks。

Summary

- Price breakthroughs were hampered by real market averages (approximately $79,000) and short-term holder costs, and reinforced the medium-term downward bias。

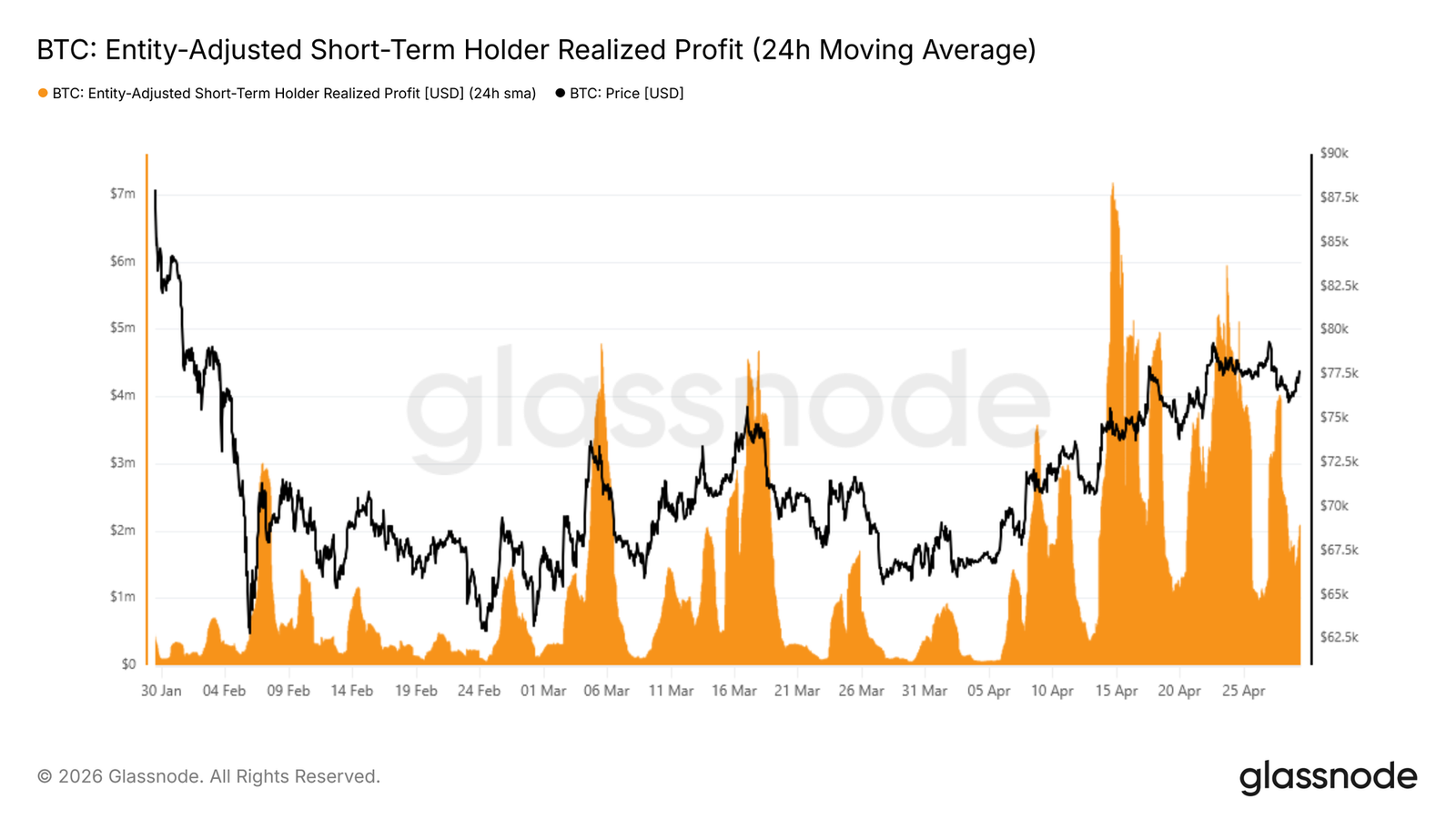

- Short-term holders have achieved a sharp increase in profits to $4 billion per hour, reflecting a substantial gain that has reduced the sustainability of the rebound。

- The dense accumulation of clusters between $65,000 and $70,000 constituted short-term support, but a collapse would weaken short-term structures。

- the spot-sale pressure is being eased, the amount of bartered delta is going back to the neutral vicinity and early signals of buyer re-involved。

- INSTITUTIONAL FLOWS HAVE STABILIZED, ETF ASSET MANAGEMENT HAS REBOUNDED ON A SCALE, AND CME CONTRACTS HAVE BEGUN TO BOTTOM UP AFTER CONTINUOUS OUTFLOWS。

- The continuing contractual silo has been transformed into a record net empty bias, highlighting the intensification of hedge activity and the potential for squeezing。

- The continued compression of volatility, rising protection demand but weak faith, has reinforced the pattern of cautious and inter-temporal shocks。

- The achievement of a high degree of consistency between the volatility rates and the implied volatility rates confirmed a more calm market background and limited orientation conviction。

Insight on the chain

Breaking through resistance, looking towards the support line

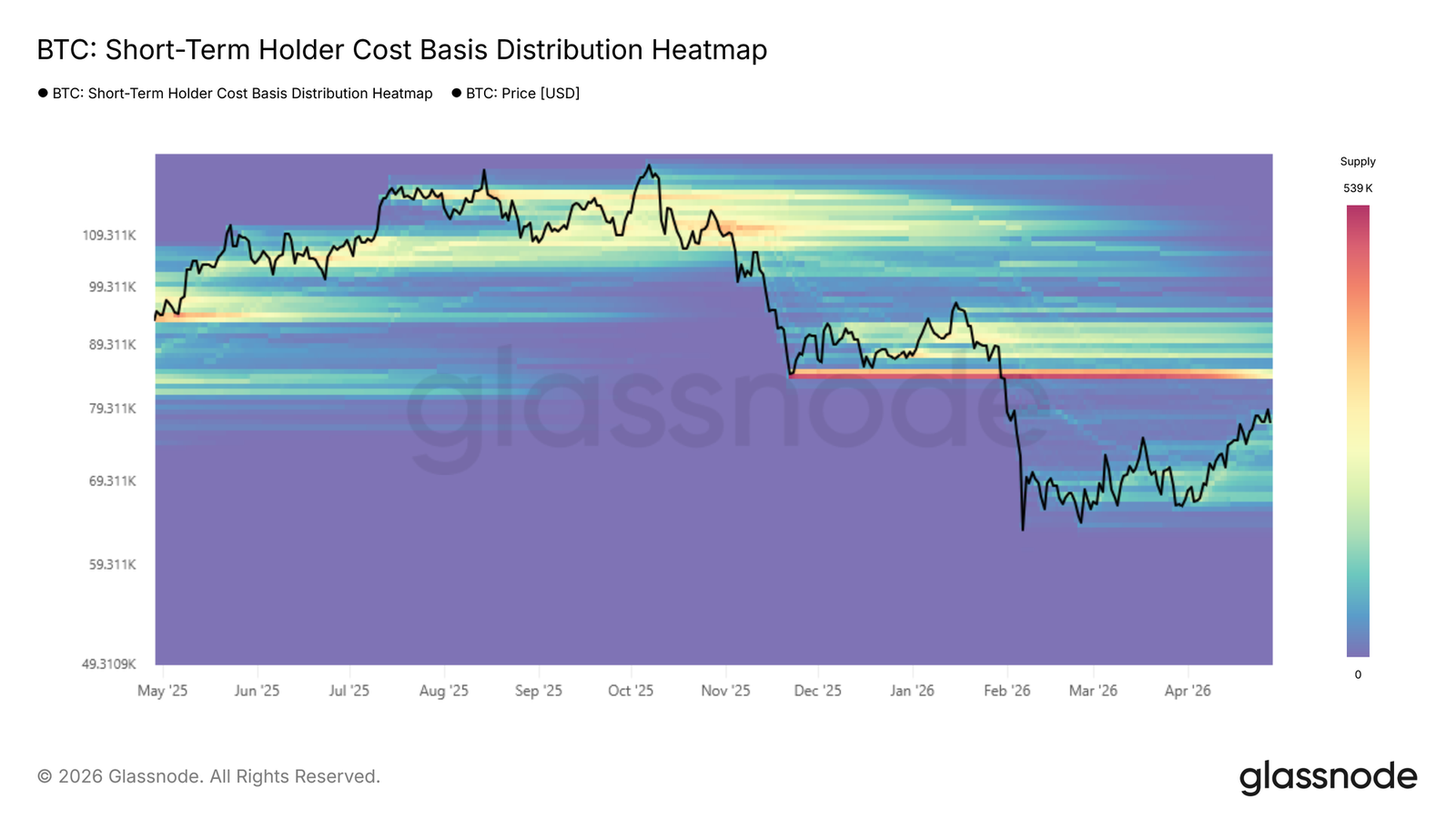

Last week, the report identified the short-term holder ' s cost base and real market average as the most likely area of resistance to the bear market ' s rebound, with the recent build-up of buyers to levels historically consistent with the local top. It was in this region that prices were then rejected and could not be maintained above the real market average of $78,000 and the short-term holder cost base of $79,000. This behaviour is a textbook model in Bear City: prices are close to the balance of gains and losses for the most price-sensitive groups, and exit incentives overwhelm demand for growth and thus exhaust mobility。

With this refusal confirming resistance above and a medium-term shift towards further downward pressure, attention now turns to -1 near the standard range of $68,000 as the most direct structural support that requires focused monitoring。

Decline analysis

The decline in the short-term holder ' s cost base is more than price observation; the data spent on the chain accurately captures how it unfolds. A 24-hour simple moving average of short-term holders ' realized profits is a real-time measure of the extent to which recent buyers have converted unrealized gains into withdrawal。

With prices approaching $80,000, the indicator skyrocketed to about $4 million per hour, about four times the base level established since mid-April, confirming that short-term holders seized the rebound as a distribution opportunity. The buyer simply lacked sufficient liquidity to absorb the profit stream, thereby limiting momentum and triggering subsequent refusals。

The indicator is most useful when analysing two dimensions at the same time: the baseline (as agent for the wider trajectory of buyer mobility) and the peak (as a reliable local top indicator throughout the current bear market cycle)。

Two scenarios, one cluster

The resistance in the real market averages and the cost base of short-term holders reinforces the broader structural weaknesses that characterize this bear city. But the picture is not completely empty。

The intensive accumulation of clusters over the past two months, built between $65,000 and $7,000, reflects the remarkable degree of conviction of buyers at these levels and provides the basis for a short-term rebound to the vicinity of $84,000 below the upper supply cluster。

On the contrary, if markets fail to absorb continued sales pressures from real market average regions, the same $65,000-$77 million cumulative cluster, more specifically the short-term holder cost base -1 near the standard deviation of $68,000, will serve as the main supporting reference in the short to medium term. The way forward therefore depends on the ability of buyers in the zone to maintain sufficient conviction to overcome the pressure of distribution above。

Underlink Insight

Selling pressure eased. Buyers re-emerged

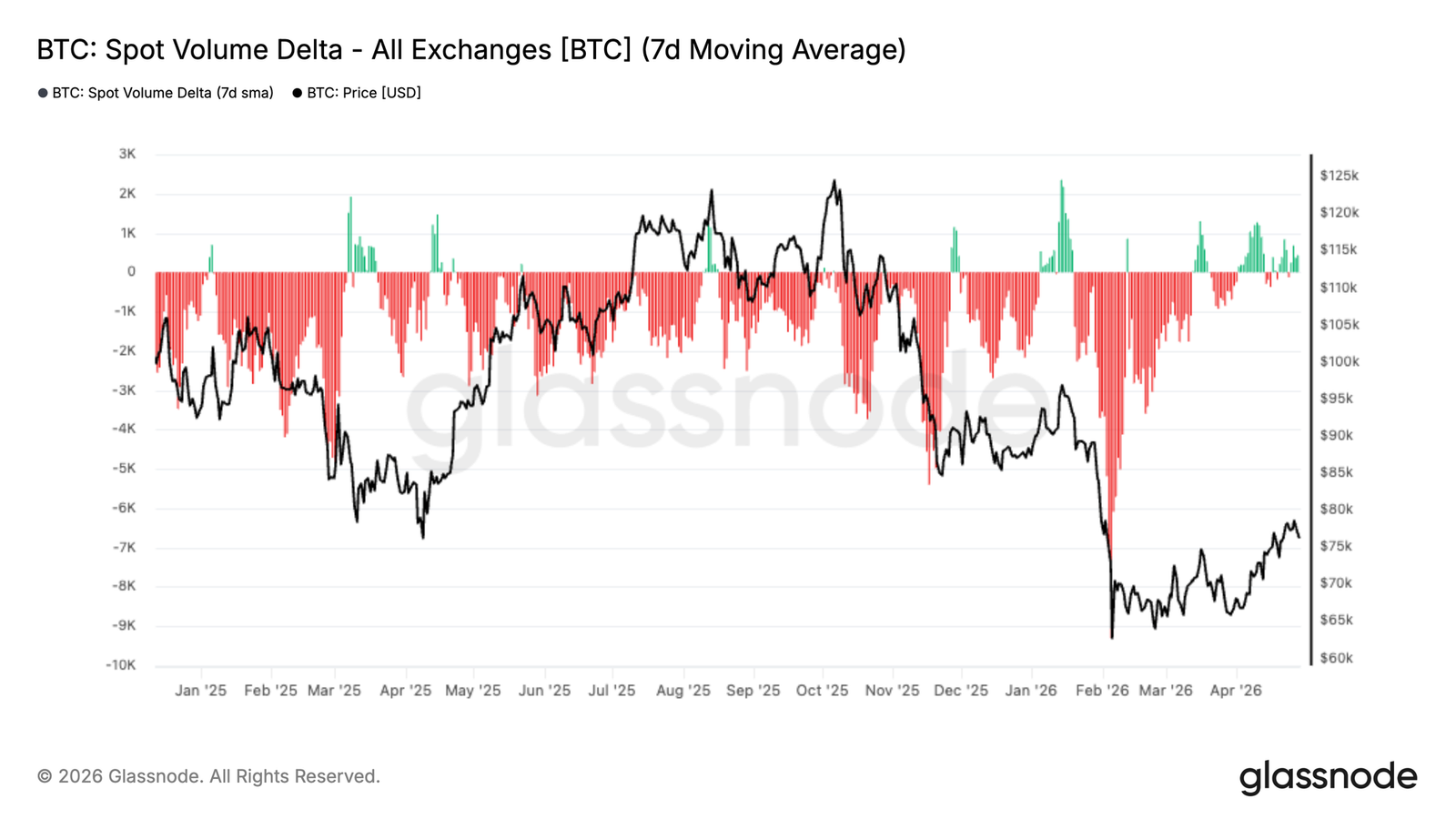

the spot trade volume delta has been in the depth negative range for most of the past months, reflecting continued net sales pressure on the exchange. this continued seller-led approach is consistent with the broader recall, especially during periods of significant return to areas of approximately $60,000-$70,000。

however, there has been a marked shift in recent data. 7 the average daily line now rises back to the neutral vicinity and begins to experience intermittent positive delta outbreaks. this indicates that sales pressure is being eased and buyers are beginning to re-engage at the current level。

This shift is important from a market structure perspective. While the strong accumulation has not yet been demonstrated, the movement to balance shows an improvement in spot demand and a decrease in seller urgency. A more sustainable recovery will require sustained expansion to the positive zone to confirm that buyers are regaining ownership。

Institutional liquidity reconstruction

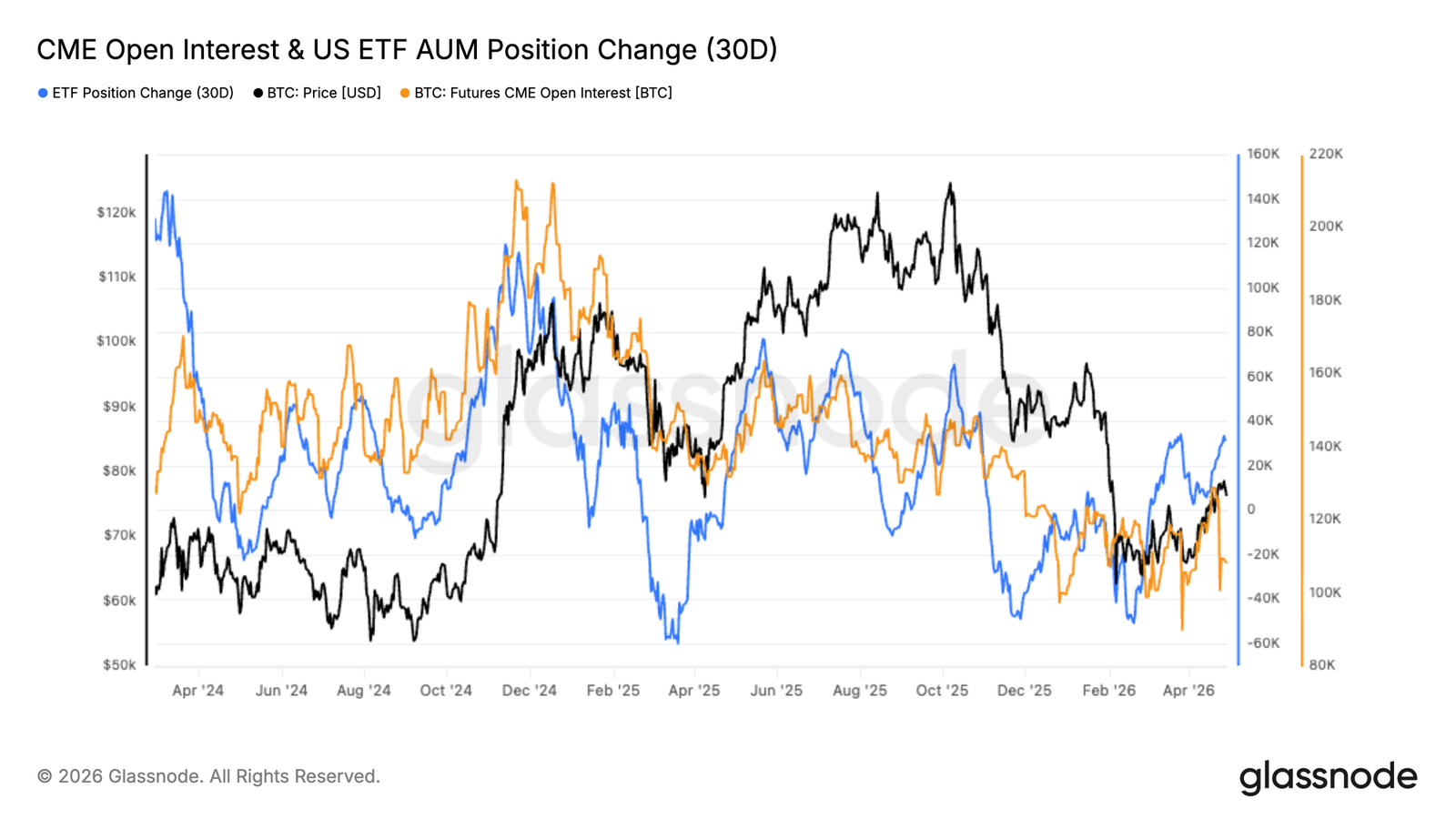

INSTITUTIONAL WAREHOUSE POSITIONS ARE BEGINNING TO STABILIZE, AND THE SIZE OF CME CONTRACTS AND UNITED STATES SPOT ETF ASSET MANAGEMENT SHOWS EARLY SIGNS OF RECOVERY AFTER THE OUTFLOW PERIOD. ETF POSITION CHANGES HAVE BEEN REBOUNDED FROM NEGATIVE DEPTHS, WHILE THE CME OPEN CONTRACT APPEARS TO BE LAYING DOWN, INDICATING EARLY RE-ENGAGEMENT。

THE EARLY DECLINE REFLECTED A WIDE RANGE OF RISK AVERSION POSITIONS AND THE SIMULTANEOUS WITHDRAWAL OF CAPITAL FROM FUTURES AND ETF CHANNELS DURING THE RECALL PERIOD. RECENT TOP-LINE MOVES HAVE BEEN DIRECTED TOWARDS PRUDENT REACCUMULATION RATHER THAN RADICALIZATION。

Sustained inflows will need to support stronger trends. Currently, the data indicate the early re-entry of the institution, but the full conviction has not yet been demonstrated。

A record empty bias

The market-oriented premium for a lasting contract has fallen to its lowest level ever recorded, marking the deepest and continuing empty bias in this data concentration. Unlike the negative values associated with the shorter of the previous cycle, the move reflects a more sustained defensive stance。

EXTREME DISCOUNTS ARE DRIVEN BY MULTIPLE FACTORS. THE RECENT WEAKENING OF PRICES HAS LED TO AN INCREASE IN INSULATION AND DIRECT EMPTYING OF THE MARKET, WHICH WAS ACCELERATED BY THE PRE-CROWDED SILO THROUGH THE CRATER. AT THE SAME TIME, LOW SPOT DEMAND AND SOFT ETF FLOWS HAVE REDUCED NATURAL PURCHASES AND ALLOWED DERIVATIVES TO DOMINATE SHORT-TERM PRICE ACTIONS。

Historically, such extremes have occurred in periods of high uncertainty, often ahead of turning points. While short-term uncertainty remains, markets are increasingly preparing for squeezing if mood or spot demand improves。

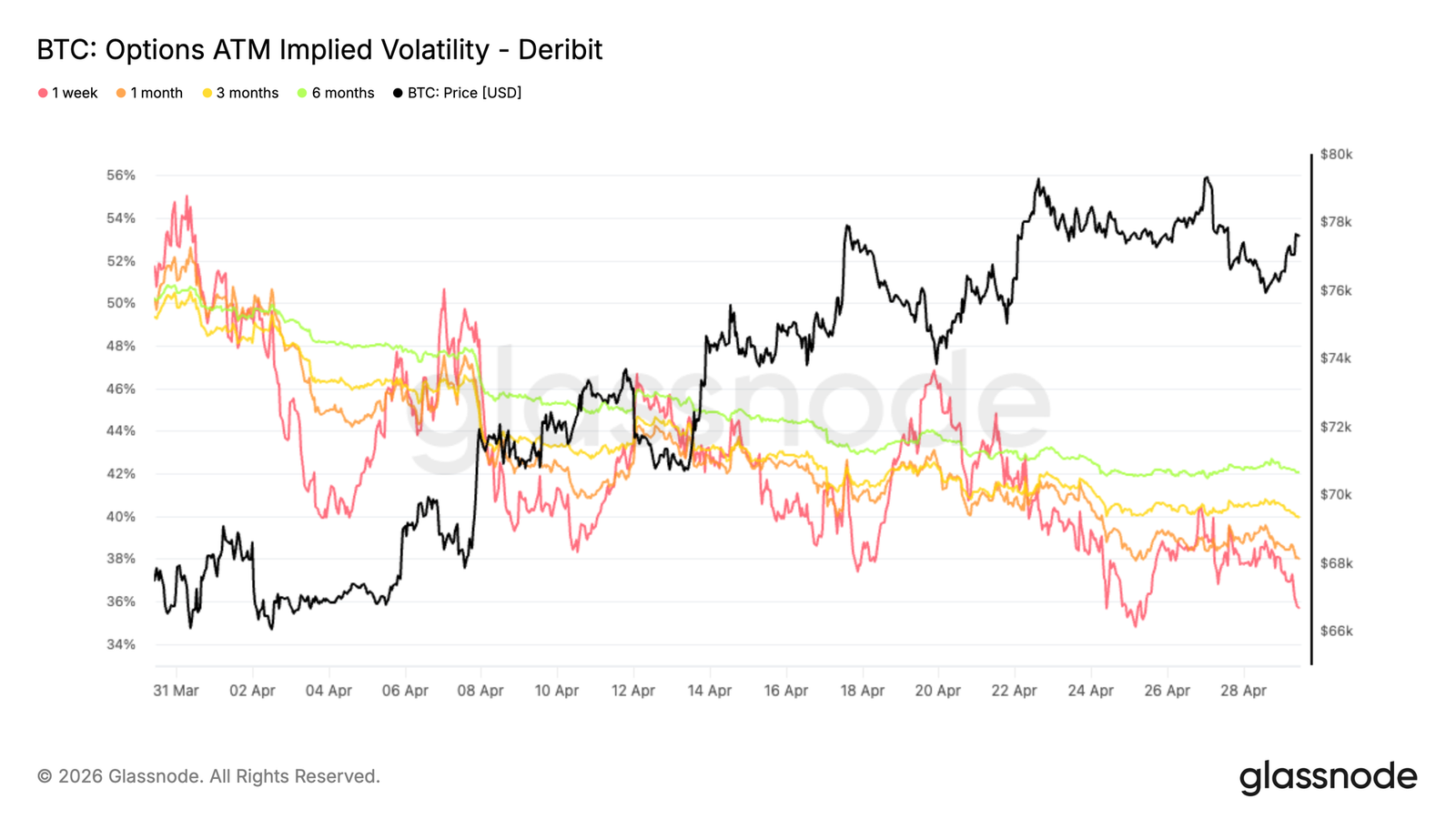

Implied volatility below curve durations Okay

It is recalled that in April, starting with implied fluctuations, the trend was dominated by a broad compression of durations。

1 The weekly flat-rate fluctuations decreased by about 16 percentage points and the six-month period by about 8 percentage points. The other duration is within that range, with an average reduction of about 10 volatility points。

The curve remains positive, i.e. longer-term options are still traded in premium on short-term options but at a lower level. This reflects the pricing of a more stable environment for the future。

Lower implied volatility reduces the cost of options, especially the right to move forward. At the same time, the need for protection appears to have been alleviated. Dealers are no longer willing to pay high premiums for volatility, which is consistent with the recent price recovery and points to expected normalization rather than accumulation of conviction。

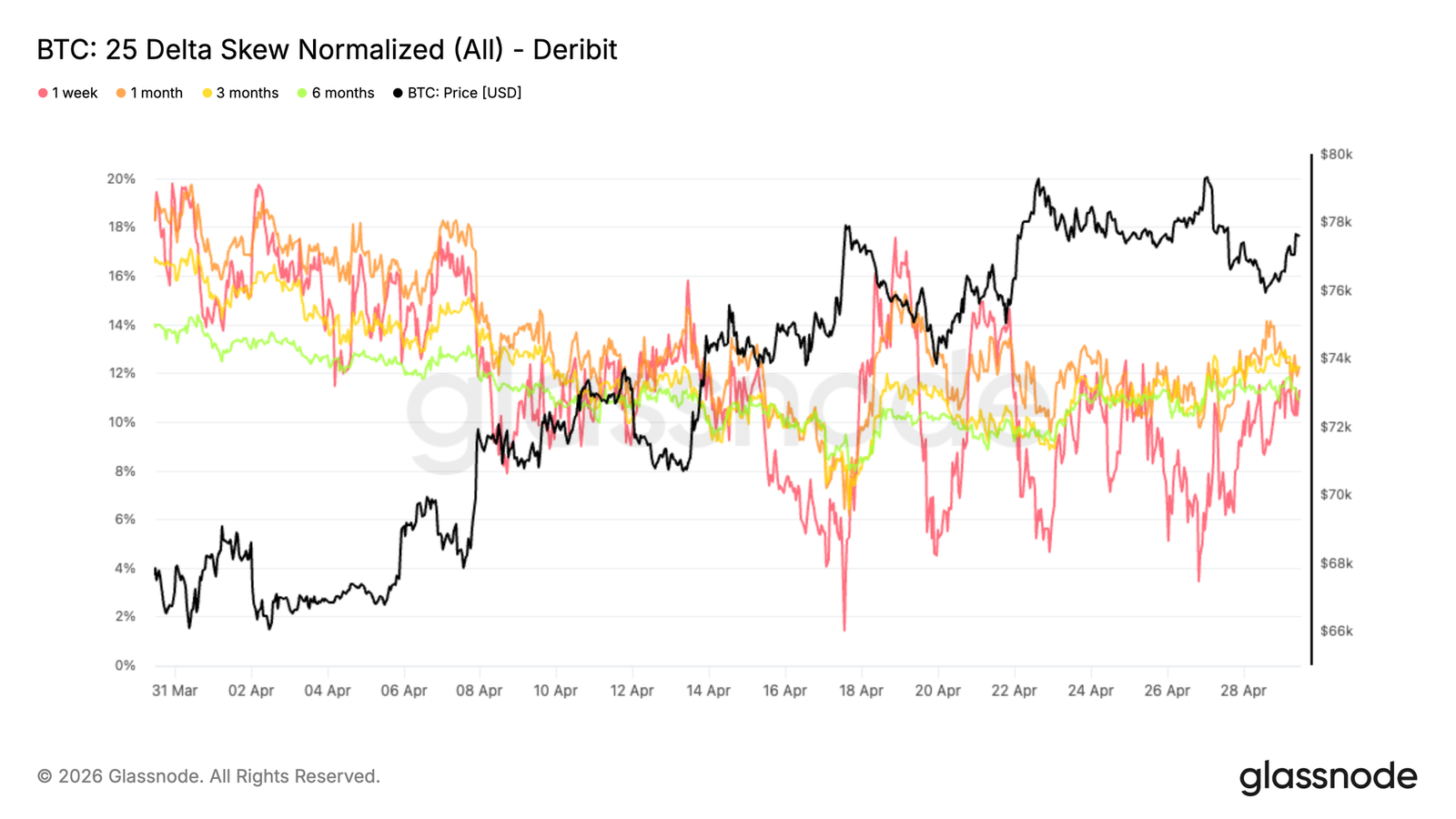

25 Delta tends downward, but protection still exists

With the compression of implied fluctuations, the deviation shows how protection needs evolve in April. The broader trend is a steady decline in the margin premium from about 18 per cent to 12 per cent per month. This reflects a marked reduction in the demand for lower-level protection as conditions stabilize。

At the short-term end, 1 week-wide bias is more intense, with several spikes to neutral (2-4%) at multiple points in April. These movements are mainly tactical in nature, as they are used to buy increased options and sell down, temporarily flattening the bias。

Recently, as prices approached $80 million in resistance, the need to fall options rebounded, pushing deadlines back to 11 per cent to 12 per cent. Protection still exists, and the market adjusts tactically in the short term while maintaining a cautious stance further away。

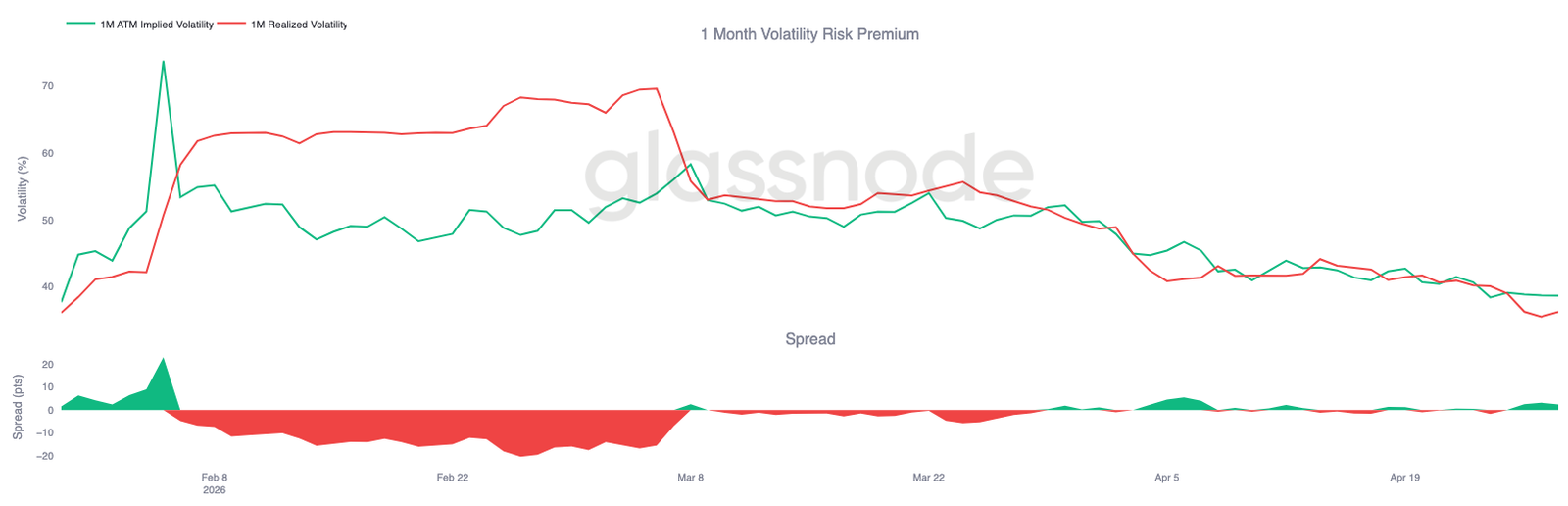

A downward shift in the rate of fluctuations achieved

As implied fluctuations continue to shrink, the realized volatility also moves in the same direction and reinforces the trend. Bitcoin has achieved a steady decline in volatility. This is important because the rate of volatility has been achieved to anchor the pricing of options. When the rate of volatility has been reduced, it naturally lowers the implied rate, as the need for large price fluctuations has diminished。

This creates a feedback cycle: cheaper options reduce the urgency of hedging, leading to less hedge-driven price movements。

One month has achieved a volatility rate of approximately 36, while the implicit volatility rate is close to 38, leaving only a small premium to the seller at risk。

The current environment reflects a shift from pressure to a more balanced one. Volatile rates are no longer being aggressively bought, and markets seem comfortable with a narrower range of expected price fluctuations。

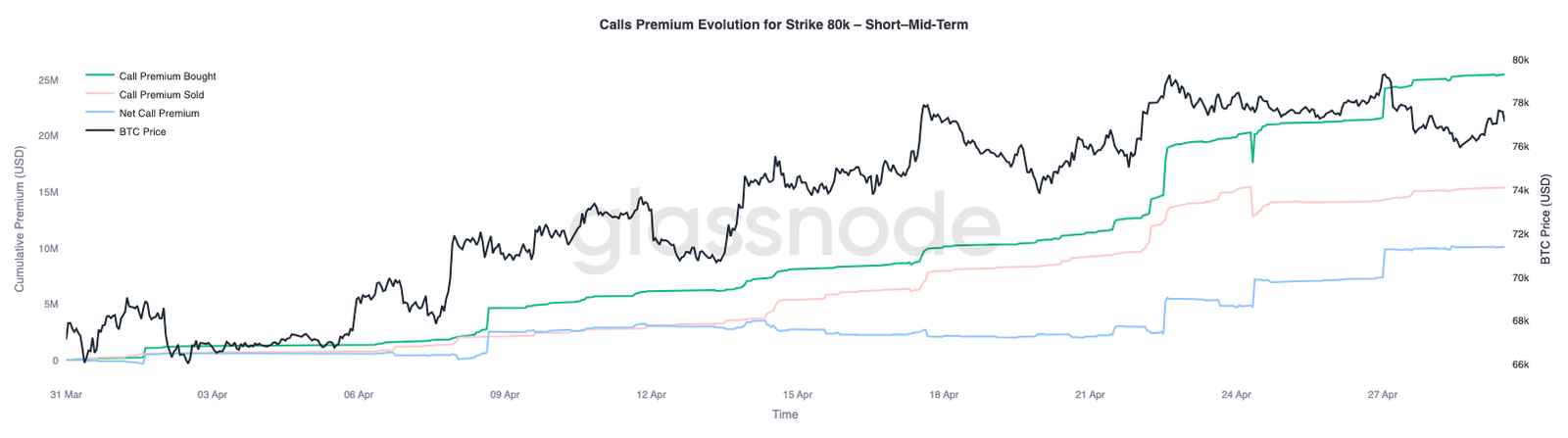

Eighty-one million United States dollars (US$) in right premium build-up to key points

As volatility and bias are reduced, the position becomes the next level to be monitored, and the level of $80,000 is becoming the next key focus。

The continued buy-in over a short- and medium-term period of $80,000 reflects growing interest in openings above this level. This indicates that traders are locating for test resistance rather than empty。

At the same time, there are two key negatives in the Gamma region, down $76,000 and up $82,000. These levels could be a region for hedge flows to scale up price actions, particularly in low-liquidating environments。

The breakthrough of $80,000 will bring the spot closer to the $82,000 area, where negative Gamma may force the market to buy strong and boost the movement. The position remains cautious, but if resistance is removed, it is becoming more and more vulnerable to more intense upward reactions。

Conclusions

In short, markets remain trapped below critical resistance, real market averages continue to limit upward attempts, while supporting clusters around $65,000 to $7,000 provide support at the bottom. The pressure on spot sales began to ease and early signs of institutional re-engagement emerged, but demand has yet to demonstrate the strength needed to sustain the breakthrough。

At the same time, derivative silos have been decisively turned to empty, and the record net open and high protection needs reflect a defensive mentality. This puts the market in a delicately balanced state. While the weight of the warehouse position is cautious, it also leaves room for sharp ups and downs if the flow of funds turns。

Until there is a clear expansion of spot demand or institutional inflow, the most likely outcome will remain a concussion, an inter-zonal shock environment. It is likely that the next directional movement will not be driven solely by warehousing positions, but will depend on whether real capital is involved in absorbing supplies and recovering higher levels。