Why is it the biggest time for money in the encryption industry

The age of the chain lovers has come to an end, and we are just the best users of the books. 。

Original by Joel John, Siddharth, Sarabh Deshpande

This post is part of our special coverage Syria Protests 2011

The fear of greed index in the encrypted market has fallen to its lowest point in history. At the same time, however, the profitability of the industry has reached unprecedented levels。

Since 2018, DeFiLlama statistics show that the encoded original protocol has accumulated $74.8 billion in fees. Nearly half of that - $31.4 billion - was created in the 18 months between January 2024 and June 2025。

Why is it that everyone is still afraid of the best seasons that an industry has seen in eight years

Over the past two months, 12 projects have been closed directly: Entropy Protocol, Milkyway Protocol, Nitty Gateway, Rodeo, Forgoten Runivse, Slingshot, Polynomial, Zerolend, Grix Finance, Parsec Finance, Angle Protocol, Step Finance. These are all products that we respect, that are made by enthusiastic entrepreneurs and that we have sustained for many years。

KOKX, Mantra, Polygon Labs, Gemini, and Minan have also been retrenched. The audience was less popular, the wind turned to AI, and the developers went to AI. The pessimism in the industry is real. "Doing encryption, turning al" has become the mainstream voice。

But should you really turn? We have been thinking about this for the past few weeks。

WHEN A NEW TECHNOLOGY EMERGES, THE MARKET WILL INITIALLY GIVE IT AN EXTREMELY HIGH PREMIUM BECAUSE OF ITS NOVELTY AND AMBITIOUS VISION. IN THE 19TH CENTURY, NEARLY 6% OF BRITISH GDP WAS INVESTED IN RAILWAY STOCKS. IN 2026, THE CAPITAL EXPENDITURE OF SUPER-LARGE CLOUD PRODUCERS WILL ACCOUNT FOR 2 PER CENT OF US GDP。

But when reality is on the ground, technical valuations return to rationality。

What really matters is whether the industry can prove useful in returning to normal。

In this paper, I will break down:

- How revenues from the encryption industry have evolved

- (a) How sticky the funds are generated

- What exactly is the moat in this industry。

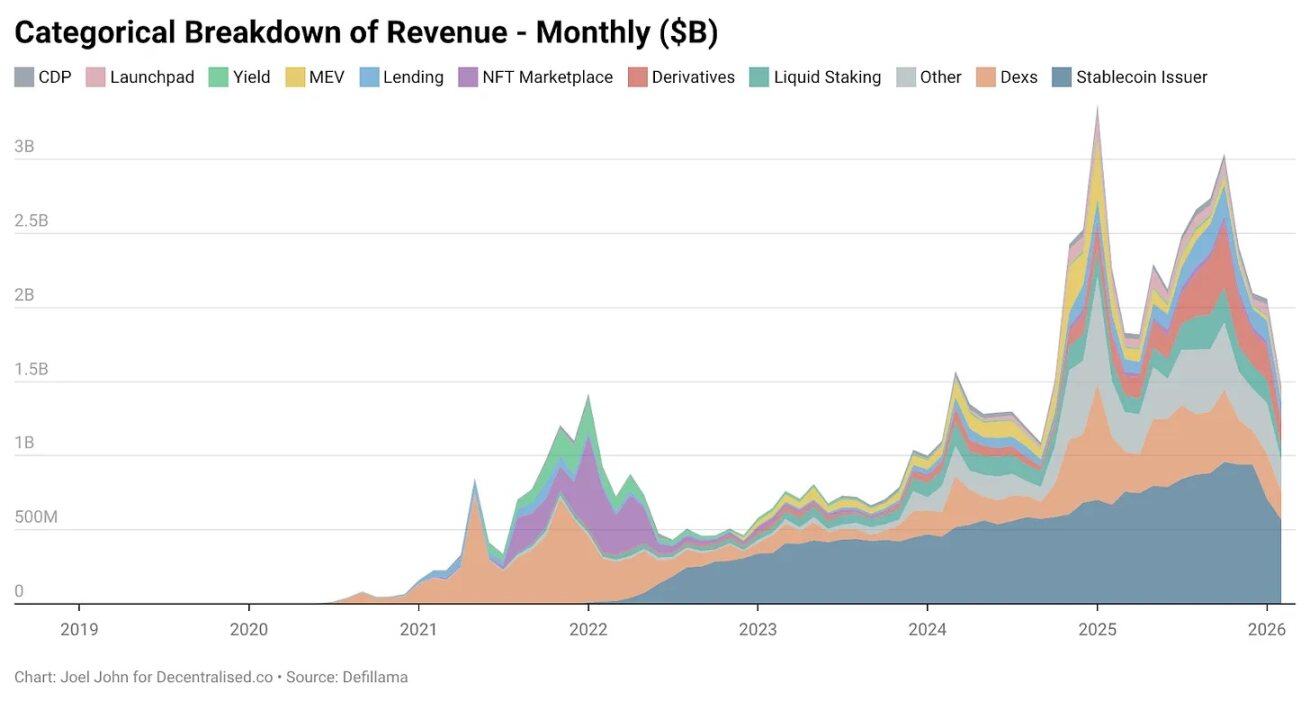

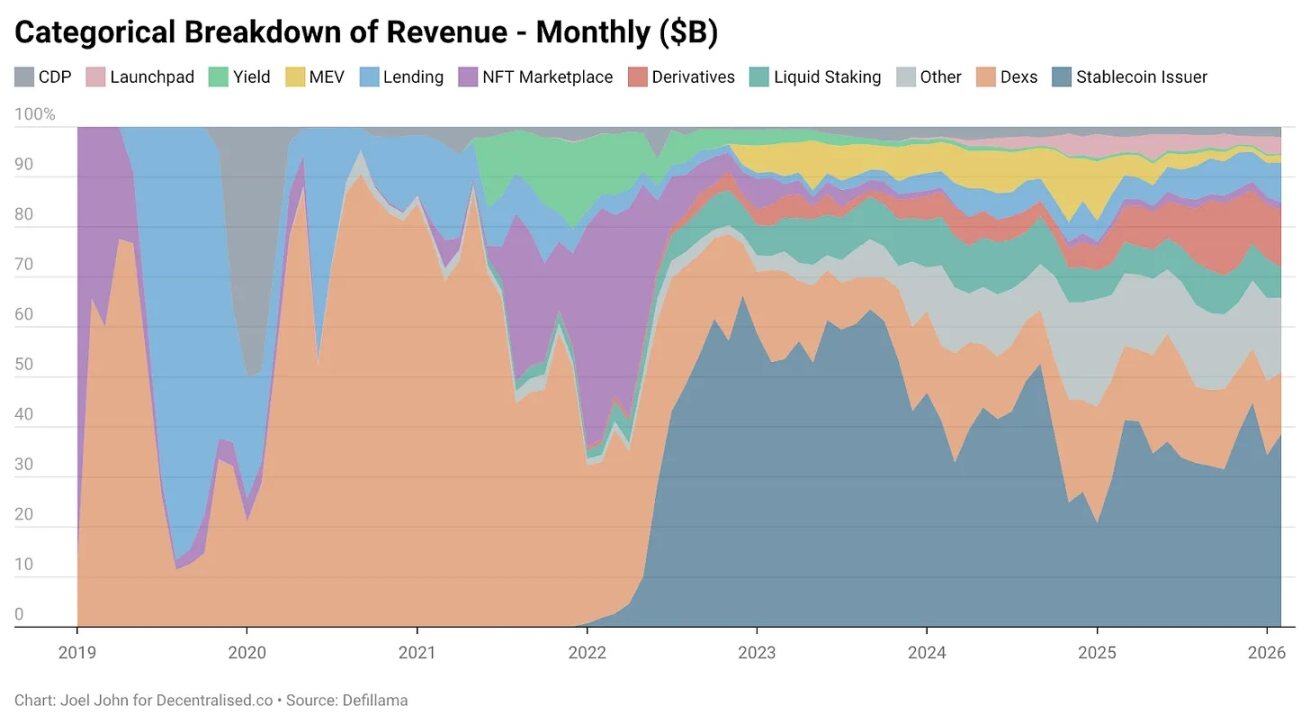

Accounts study: major changes in income patterns

Since the beginning of the industry, the encryption business has been making money。

Bitmex, François, Coinbase, these exchanges have earned a lot of money. They are, however, central, held by a few and their income is not disclosed。

Uniswap, Aave, this kind of DeFi original agreement changed everything. You can check how much money the agreement makes every day. The valuation of the tokens should have reflected the economic activities supported by these basic components。

Until 2022, the decentralised exchange accounted for 28.4 per cent of total industry revenue, generating $2.77 billion in that year. Lending tracks are also highly concentrated: Aave and Comp sound took 82% of the charges. At that time, it was believed that there was a head on the track, but that there was a chance for the long-tail agreement to grow up. Technology itself is innovative enough to support high valuations。

This is followed by the stage of encryption expansion to the public。

NFT has represented a promising vision: cultural values are priced in chains. The stars changed their Twitter image, and ordinary people thought it would lead to a massive spread. OpenSea generated $5.55 billion in revenue that year, accounting for 71.7 per cent of the NFT market。

Looking back, its $13 billion valuation doesn't seem to be out of line -- it could have been a long-term monopoly。

But fate and the market are different。

BY 2025, NFT INCOME WAS LESS THAN 1%. WE WENT THROUGH A BUBBLE LIKE THE SOYBEANS, AND WE DIDN'T EVEN LEAVE A PHYSICAL SOUVENIR。

(Note: Beanie Babies, a series of velvet toys launched in 1993 by Ty Warner, United States of America, and a well-known global collection of hot and speculative bubbles in the mid-1990s)

BY CONTRAST, REVENUES FROM DECENTRIZED EXCHANGES ARE GROWING, BUT VALUATIONS ARE FALLING SHARPLY. LAST YEAR, DEX GENERATED $5.03 BILLION IN HANDLING FEES AND $1.65 BILLION IN BORROWING PLATFORMS. TOGETHER, THEY ACCOUNT FOR 22.9 PER CENT OF TOTAL FEES, WELL BELOW THE 33.1 PER CENT IN 2022. THEIR ECONOMIC ACTIVITY HAS BECOME SMALLER IN LARGER PLATES, AND VALUATIONS HAVE BEEN REDUCED SIGNIFICANTLY。

So what's growing

Since 2022, how has the coded business model evolved? The answer is hidden in the data:

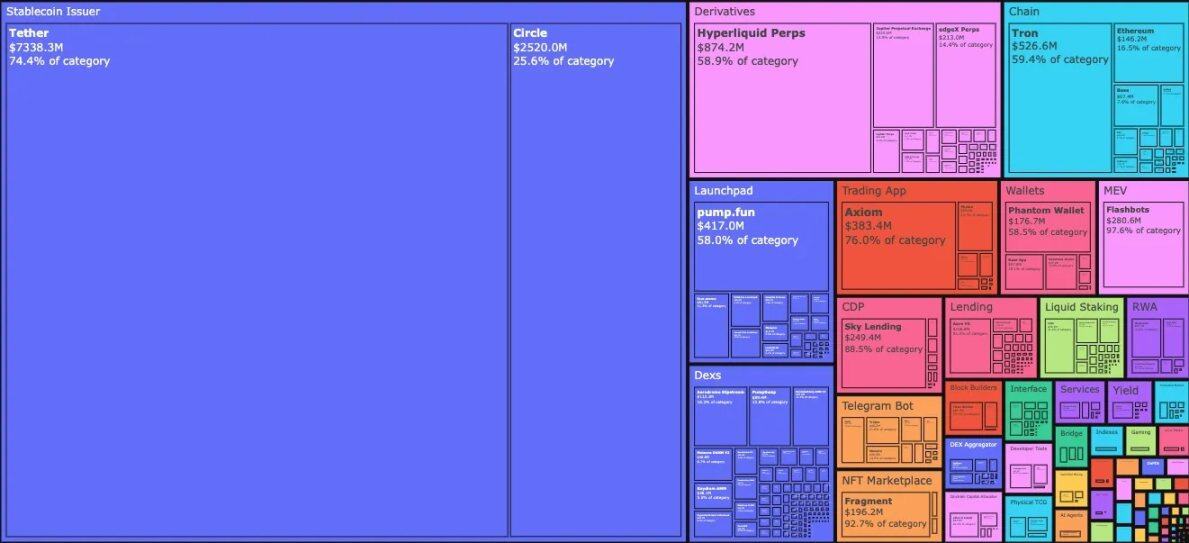

In January 2026, stabilizers Tether and Circle took 34.3% of the industry fees. In other words, for every dollar in the industry, 34 cents go into the pockets of these two companies. Their income doubled from $4.95 billion at the beginning of 2023 to $9.89 billion in 2025, almost entirely from United States debt earnings。

It is a financial product at the bank level, but it runs out of the growth of start-ups. Tether's income is almost three times that of Circle。

Their rise stems from two forces:

- Requirements

The global South has always needed tools that allow it to hedge against local inflation and freely transfer funds. The dollar, even the dollar, filled the gap -- the local currency couldn't do it. Capital flight is just needed, not additional functions。

- Cost structure

The block chains assume the operational part of the stable currency operation. In contrast to traditional banks, financial technology companies, Tether and Circle do not need to be recruited on the same scale as distribution increases. Another $1 billion was released on the chain, $100 billion moved between addresses, and the marginal cost was almost zero。

Demand pulls and costs are very low. The combination of the two makes stable currency issuance one of the most efficient businesses in financial history。

The moat of the stable currency is: liquidity, compliance, time dividend. Few distributors can live too many cycles。

Tether and Circe took almost 99% of the stable currency issuance revenue. Why? Because they start early. The network effect of multiple exchanges is the legitimacy of technology alone. Tether was initially wired on the Omni side chain, slow and clumsy, but it was within reach of OTC counters and exchange contacts。

This is a distribution barrier, not a technical one. It's a moat that encrypts native entrepreneurs can't replicate only with codes。

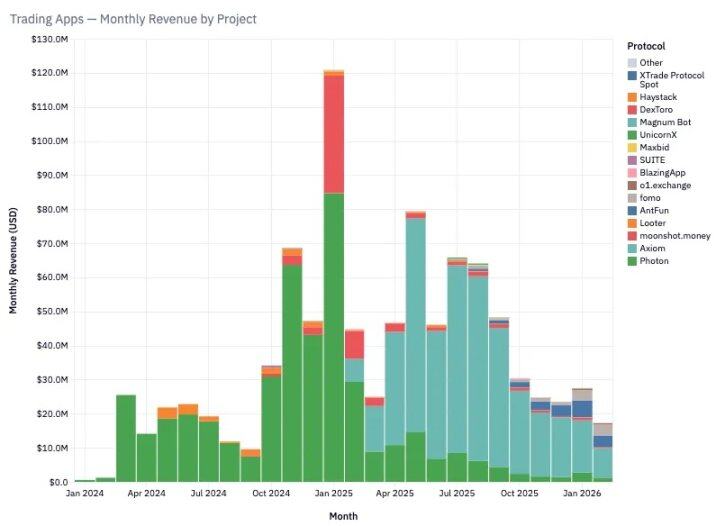

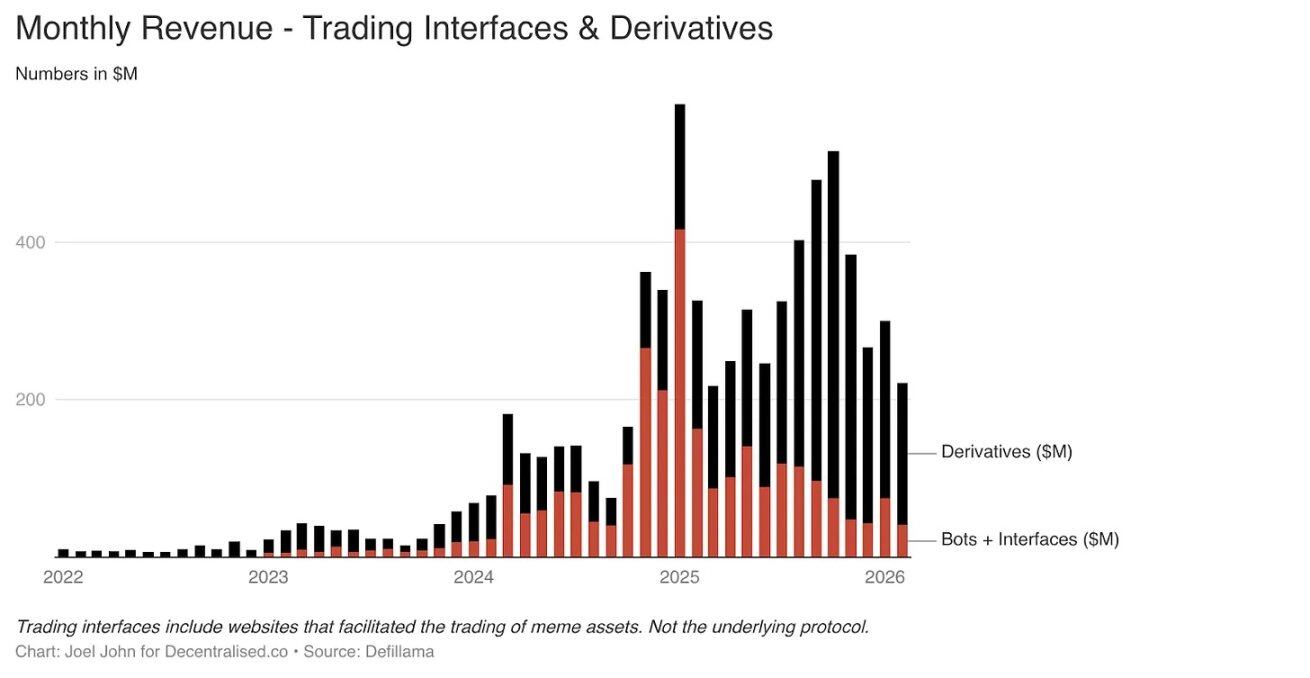

New growth engine: trade-type application outbreak

Our previous article mentioned that encryption is essentially a trading economy. But we didn't expect that the products based on Telegram trading robots and trading interfaces would grow so fast。

In January 2025, the single-month charges in these two areas amounted to $575 million. The reason is simple: this is what users really want。

Meme currency trading, and a permanent contract exchange that allows users to profit quickly. In pursuit of high returns, they are willing to pay high fees。

Between 2022 and 2025, this track rose from 1% of total income to over 15%。

TryFomo, Moonshot, a product that focuses on end users, earns millions of dollars. It is not technically complex, but the key is to make a better user experience by packing together encrypted primary components. When such tools matured, developers no longer needed to motivate mobility and worry about wallet management. The basic components that we were excited about in 2022 are now mature. This type of application is built on BullX, Phototon。

Between January 2024 and February 2026, this track created a $933 million commission. But there is a fatal flaw in Meme assets: they are light quantitative applications, and they are extremely seasonal。

Does it look like you've known each other

NFT, Web3 games have experienced similar outbreaks and collapse. This cyclicality is both a bug and a characteristic of the industry。

The sustainable contract exchange (and later the forecast market) is a new and more permanent direction。

PumpFun democratizes asset distribution through Meme, but the game is not fair. Finally the market woke up: Meme will die。

Buying a funny token for a dream that's so rich, it's broken. People don't want to manage a bunch of random coins, they want risk exposure。

The contract of renewal offers this。

You can trade lots of bitcoins, Solana, Ether. There is a need for marketers and traders who need to replace centralized channels. At the heart of this class is mobility。

Hyperliquid became the lead because its order book was much deeper than the Centralized Exchange. Without such a reciprocal experience, users have no reason to migrate. Over the past three years, Hyperliquid and Jupiter have taken most of the fees from this track。

The permanent contract exchange and trading platform have torn the veil of the encryption industry: the real way to make money is to draw small fees from high-frequency transactions. Meme's trading platform, the permanent exchange, is the "dopamine machine" that packs and sells risks. Some of them will mature into core financial infrastructure components — which can also be used to trade goods, stocks, digital assets around the world over weekends。

The original block chain application reproduces what Robinwood, François, has long provided: a risk path。

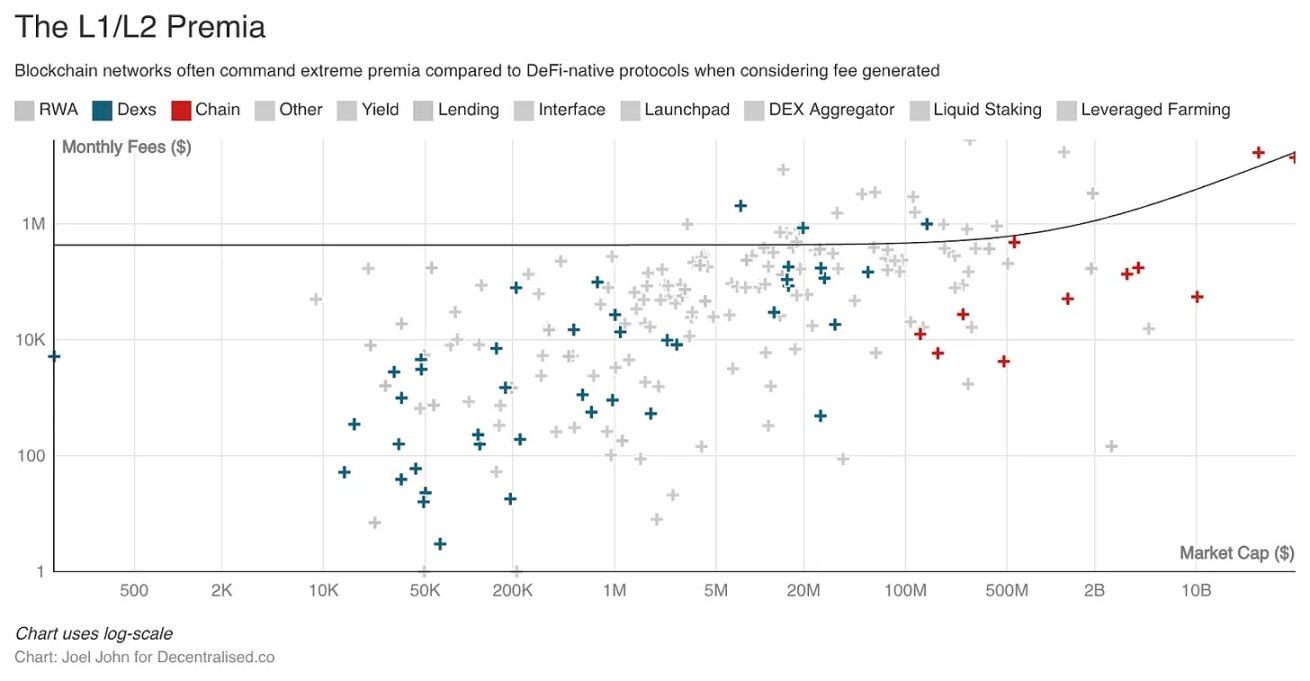

Fat compacts for hunger: the public chain and DeFi valuation fell sharply

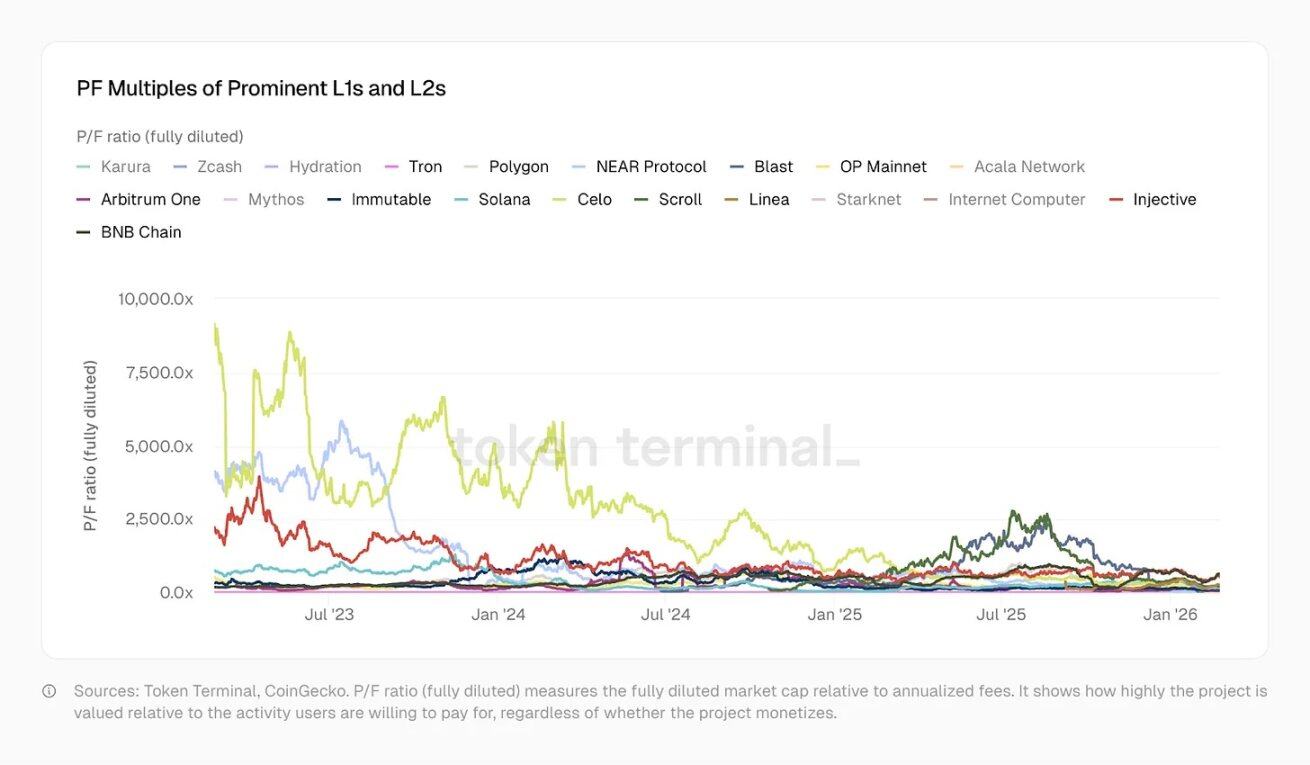

So far I haven't mentioned the bottom chain. Because their stories are completely different: they are the victims of novel premiums, and they are now moving towards discounts。

January 2023:

- Optimism 465 times (PF)

- Solana 706 times

- Arbitrum, BNB about 206 times

Today:

- Solana 138 times

- Arbitrum 62 times

- OP 37 TIMES

- Polygon is only 20 times the size of traditional financial technology

- Tron supports stable currency ecology, and it's only 10.2 times

These chains have supported more complex products over the years, with more users, better mobility and more financial applications. However, their fee-for-price ratio has declined significantly, reflecting a shift in market attitudes。

Historically, Layer1 and Layer2 have been extremely high compared to independent infrastructure valuation premiums. If used well, the premium could have created a new economy and financed a truly useful application by developers. However, open source + tokenization is too easy, leading to 50 homogenization projects in 30 public chains and poor interoperability。

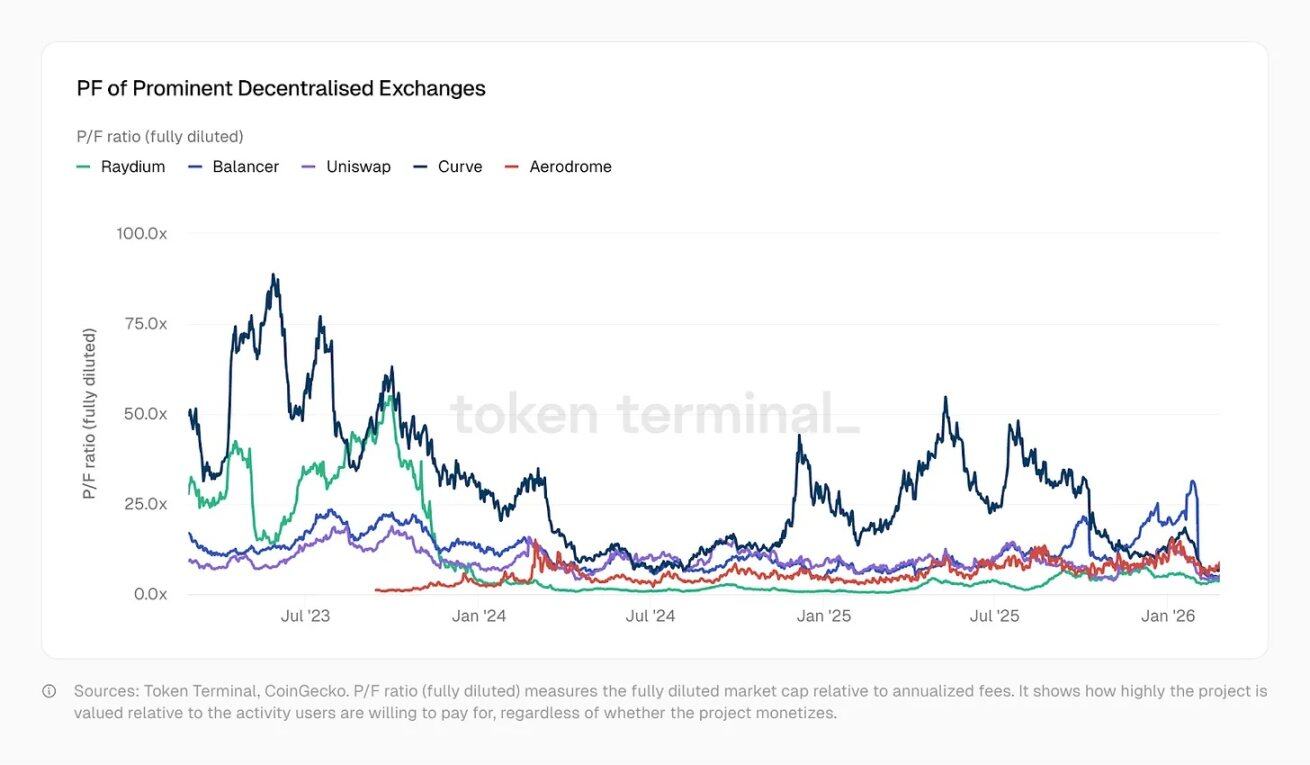

The fate of DeFi's basic components is even worse。

Investors have chosen too much to be novel, even if economic activity increases and valuations are cut off。

Kamino, Euler, Fluid, Meteora and PumpSwap have been on the air for far less than 2022. Some DEX prices are even down by one。

In other words, the market gives them a lower valuation than would be the case in the coming year。

A strange paradox has emerged: the valuation of bottom agreements (DeFi components, public chains) has fallen, but applications built on them have made more money in a shorter period of time。

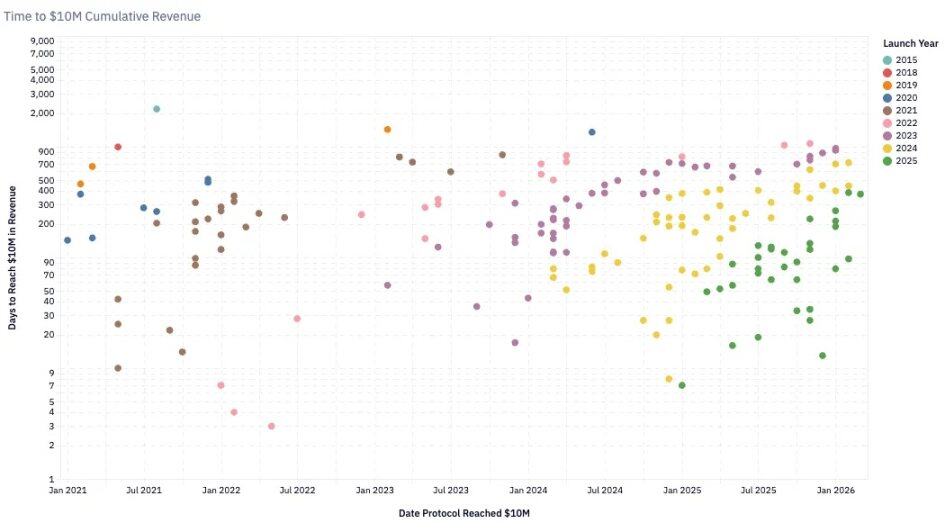

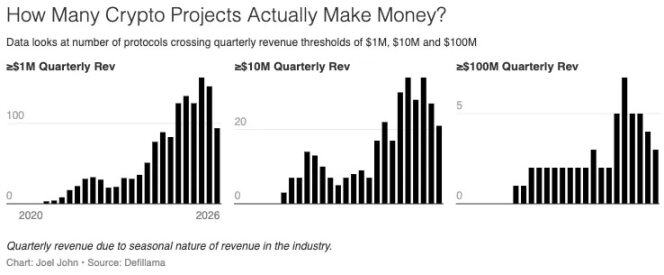

The number of teams earning more than $1 million per quarter has steadily increased and now exceeds 100。

In 2020, a deal takes 24 months to earn $10 million a year, which is fast. By 2024, only about six months. Pump.Fun, who was on line at the beginning of 2024, had a record revenue of $10 million in just about two months。

This acceleration reflects the maturity (facility and cheaper) of the underlying infrastructure, as well as the expansion of the financing for profit and recreation in the chain。

For developers and entrepreneurs, the facts are clear:

- Today there are nearly 900 agreements making money

- People compete for median income and share less, but there are more teams that make money as a whole

- The median monthly income has fallen to $13 million。

Three moats in the encryption industry

There are three types of moats in the chain business:

- First advantage

Tether, Circle’s early web effects are extremely difficult to replicate. They cross multiple cycles and form a double oligarchy. De-monetaryized and highly financialized operations. Tether is a central entity whose income comes mainly from United States debt。

- Mobile moat

In sectors where capital has always been profitable, Aave maintains deep liquidity across cycles. Hyperliquid is copying this, but it will take time to verify. These agreements return funds to liquidity providers and optimize token governance。

- Distribution of moats

Seasonal applications such as the Meme Currency Trading Platform rely on liquidity and user requirements. Web3 games and NFTs also belong to this category. After increasing productivity, small and fine teams can move faster towards C-end products. Core competitiveness becomes: the ability to regenerate and retain users in times of passion。

Products based on distribution barriers may be of great value, but they are different and not normal. The value of traditional start-ups lies in the replicability of experience, such as Y Combinator. But encryption is too fast, and it's hard to sink。

AND THAT'S WHY IT'S HARD FOR ENTREPRENEURS TO REPLICATE THE C END PRODUCT。

The cyclical nature of the project that helped to break out was not necessarily repeated. It's not that entrepreneurs shouldn't do it. Data service providers in markets and smart economies may have excellent cash flows in the short term。

But let's be clear: this is a high turnover, short-term game, not necessarily for long. The trap is blind financing, or holding a long-defunct token after the hot spots have disappeared。

Challenged governance: soul torture of token value

In 1999, many technology shares were marketed 10-20 times. Akamai once reached 7434 times. In 2004, it fell eightfold. A large number of companies fell from 30 to 50 times to less than 10 times。

Internet bubbles had collapsed and trillions of dollars in speculative value had evaporated. But many companies survived because the business was real。

Amazon fell 94 per cent and later became one of the most valuable companies in the world. Encryption is going through the same valuation compression, only faster。

In 2020, DeFi was still in the pilot phase, with a total annual income of only $21 million and a market-wide market share (P/S) of 40,400 times。

The market is full of fantasies about the future。

In 2021, DeFi summer turned income into real figures and P/S fell 338 times. Today, annualized income is $18 billion, P/S about 170 times. Five years, from 40400 times to 170 times。

But here's the key:

Visa has a marketing rate of about 18 times, with shareholders having a share, buyback and legally guaranteed rights of return and governance. Aave has a marketing rate of about four times, but the holders of coins have only the right to govern, and only recently have the right to direct economic gain. Hyperliquid repurchases with a rescue fund to bring HYPE holders closest to traditional equity holders. Aave passed an annual buy-back plan of $50 million in 2025。

These are meaningful actions, but only exceptions。

Throughout the market, most agreements do not have a mechanism to return value to token holders. Valuation appears cheap, but rights attached are much weaker than traditional markets. These valuations are valid because of the size and efficiency of the industry, which is not comparable to traditional commerce。

The agreement to compress encrypt market sales is not a large organization for thousands of people. They are small teams that operate a global financial infrastructure with almost zero marginal costs and no physical footprint。

The split of the track will be clearer:

- Aave: P/ S ~4 times

- Hyperliquid: P/ S ~7 times

- This is no longer a foam valuation, even less than traditional target companies:

- Coinbase: ~9 times

- CME: ~16 TIMES

- Visa: ~15 times

Will Clemente, in our podcast, said that encryption is pure capitalism. There is no industry in which successful firms have a per capita profit close to Tether's -- Tether has about 125 employees, with an annual income of about $12.5 billion and $100 million per capita。

Comparison:

- Young Weida: $5.2 million per capita

- Apple: $2.4 million

- Google: $2 million

Tether's efficiency is probably the highest in business history. Although the whole 170 times the P/S seems crazy, the market is not irrational about making real money -- pricing is even lower than traditional financial infrastructure。

This raises the next question: What is the use of tokens

In many categories, tokens are a powerful tool for coordinating the movement of capital towards a shared vision. Encryption is now at the stage of dual oligarchy solidification。

Traditionally, the founders had to borrow debt or equity to finance financial products. Hyperliquid, Uniswap, Jupiter, and Blur demonstrate that individuals are willing to provide capital for new products with token incentives。

If tokens are accompanied by powers of governance, they can also be deeply involved in governance。

In the future, the token may evolve into two main functions:

- Harmonizing capital and resources for appropriate populations

- Give them power over the governance agreement

Simple tokens are no longer valuable. Even stocks can be monetized. These instruments must have the right to the return of economic activity + the right to lead governance. Many Layer1 and Layer2 tokens can't do either。

Teams and wind investments hold most of the coins and ordinary holders are scattered. There is no reason for ordinary people to care about newly acquired assets. Now the industry is split. MetaDAO allows investors to refund the full amount when the team makes false statements. No major agreements have yet been adopted。

The core reflection of encryption is that traditionally, tokens give too few rights to holders. Now the agreements are answering an old question: how can people hold these things

Crossroads: The Next Era of Encryption

Over the past two decades, capital markets have become increasingly intertwined, largely as a result of technological advances。

WE CAN TRADE IN GOODS, OVERSEAS INDICES, DIGITAL ASSETS, AND EVEN FUTURE TRADING VALUES. THE BLOCK CHAINS ALLOW THESE MARKETS TO BE TRADED AROUND THE GLOBE ALL DAY. NASDAQ, NCIS, AND 24/7 TRADING ARE EXAMPLES OF TECHNOLOGICAL CHANGE。

We live in a highly financial world。

For the founders, this means rethinking: what to build, how to build. The data are clear: all block chain products end up making money in two modes:

- Draw down petty handling fees from high frequency transactions

- Draw high fees from transactions requiring authentication and trust

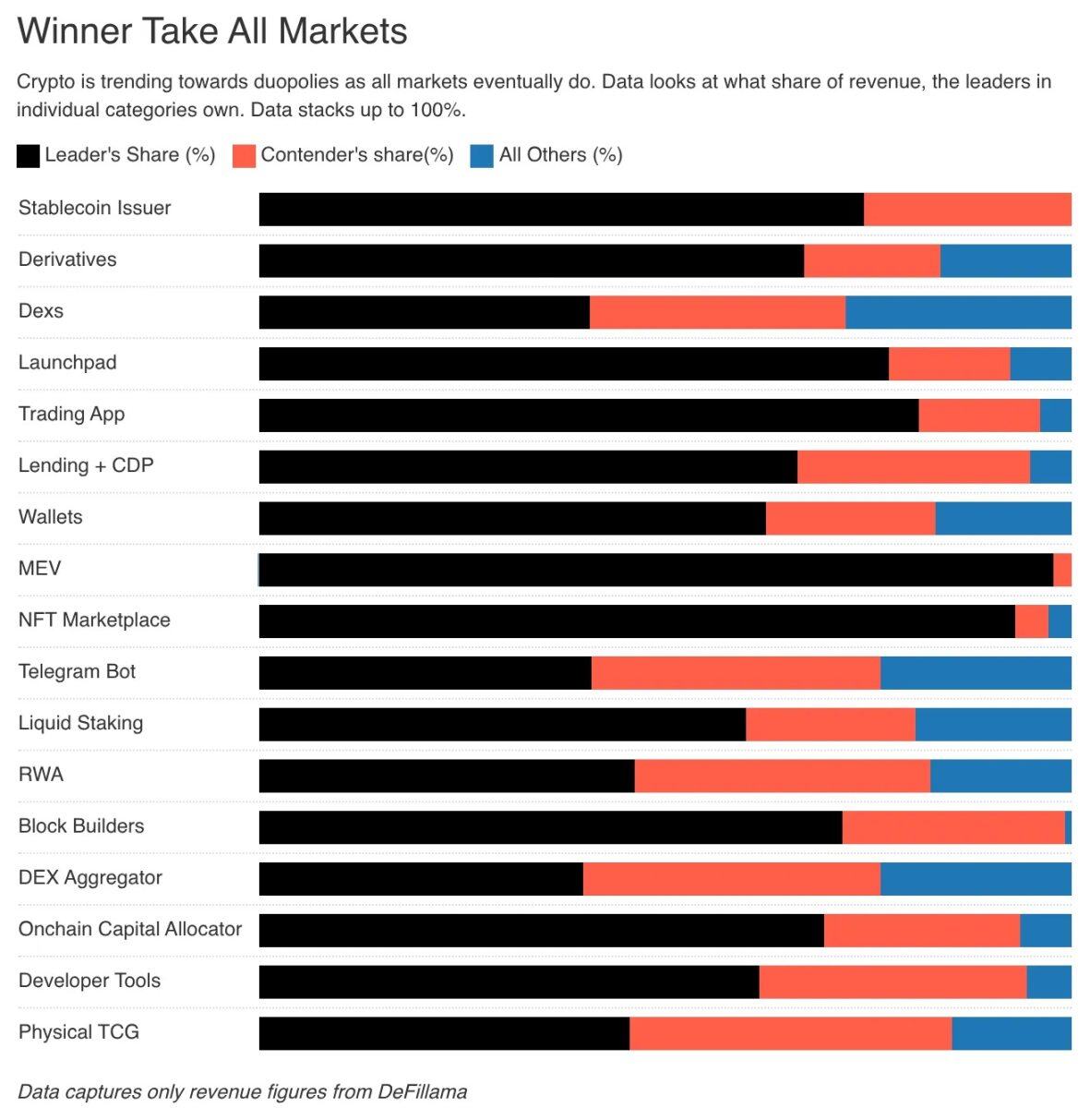

Core competitiveness is either trade speed or verifiable transparency. Leverage is the purest motivation of capital market participants. Markets eventually move towards extreme efficiency. We've seen more than 70 percent of the tracks taken by the heads of both families, as proof。

For the founders, the capital that was invested in your currency will now turn to assets with higher volatility and higher return on capital. Long-term capital is still available and even willing to pay a premium, but only for business value。

Investors in Google and Amazon need not panic because the business itself is valuable. In an era when the value of the software itself is being questioned, it is important that the block chain primary applications find new forms of value。

We can reconstruct the tokens, or even let the equity of start-ups flow through the chain. But this is not just a question of tokens, but of business models。

The vast majority of long-tailed block applications, such as Web3 socialization, identity, games, have failed to achieve scale and effective differentiation between traditional products. It's not that these experiments are worthless, but we're not actually commercializing them。

The age of encrypted infrastructure has passed. In the future, it will be deeply integrated with the Internet。

No more "online business," you just exist on the Internet. Nobody calls "Moving Applications Developer." You're just a developer。

The age of the chain lovers has come to an end. We're just the maximizers, thinking about the best use of these books。