Encryption arbitrage has died: how traditional finance (TradFi) achieves a 361.6 per cent return on a lasting contract

The old arbitrage deal did not disappear; it simply left the most crowded lanes of the market。

CORE SUMMARY (TL; DR)

- During the current cycle, the financial arbitrage space for mainstream encrypted assets has been completely squeezed by the agency ' s current arbitrage funds。

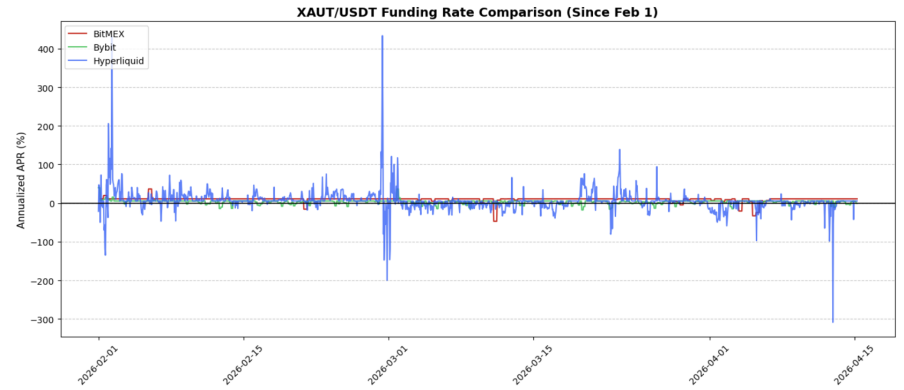

- In the XAUTUSDT transaction pair, in the past 73 days, the simple “ spot-for-renewal contract” arbitrage on BitMEX achieved an annualized rate of return of about 9.67 per cent, compared with 5.99 per cent for Hyperliquid and 3.22 per cent for Bybit。

- Brent Oil has a more profitable margin: more BRENTUSDT in BitMEX / emptied in Hyperliquid, with an implicit 7-day annualized return of approximately 361.6 per cent, 22.7 per cent in 14 days and 103.0 per cent in 30 days。

- Now there is a better opportunity to hide in BitMEX's TradFi contract for sustainability — where assets are renewed, financial flows are not yet ripe, and the misalignment of financial rates remains as large as absolutely profitable。

Mainstream encryption arbitrage is no longer attractive

For most of the time in the history of encrypted currency, the arbitrage of capital rates on mainstream sustainable contracts is one of the purest trading opportunities in the market. The script is simple: buy a spot, make a permanent contract, keep Delta neutral and charge interest. This strategy has worked because of the long-term lopsided demand for leverage, the structural bias of the financial rate mechanism itself and the fact that the market remains inefficient enough to keep these price differentials attractive for a long time。

but things have changed now. since 2025, the decline in the rate of capital in the mainstream currency has been extremely severe, most notably the sharper the impact on the market value of the currency. this suggests that the old logic of trade is not institutionally broken, but simply that it is “rolled” by arbitrage. the space for easy profit has been swallowed up by hedge funds, current arbitrage counters and large structured players, who now view the arbitrage of encrypted assets as a large-money balance sheet business. once the funding rate rises to a level worthy of harvesting, large sums of money will quickly flow in and be eliminated. the result is that today the return on the financial rates is no longer worth putting so much effort into it by traders。

The advantage has been transferred to the TradFi contract

The change is not the arbitrage of the financial rate itself, but where it exists. More interesting opportunities have moved to the TradFi contract, where market structures are still young and capital flows are far from rigid. These products are in an unusual middle ground: they are macro-financial, but on the infrastructure of encrypted money, 24/7 are traded all day, and the user groups facing them are still at the stage of learning how to properly price them。

This is crucial, because TradFi's permanent contract performance is very different from that of a mature encrypted currency contract. They will respond to the headlines of macro-news, remain traded when the market at the bottom is closed, and are scattered on platforms with very different images of participants. This creates a more chaotic financial rate environment, where traders are able to obtain excess returns. In particular, on BitMEX, this opens up a range of opportunities for arbitrage of financial rates that are far more attractive than mainstream encryption in the remaining space。

Trading opportunities: XAUt (Tada gold) and BRENT (oil)

Trading policy one: XAUTUSDT - a more pure and robust arbitrage

First chance is more direct: buy XAUt cash in BitMEX, and make an empty XAUTUSDT in BitMEX and charge a fee in Delta neutral structure. It's a classic arbitrage deal, but it's applied on token gold, not on mainstream encrypted assets. Its attraction lies not only in the apparent rate of return, but also in the “quality” of the proceeds。

For the past 1,759 hours (about 73 days), the average annual funding rate for the XAUTUSDT on BitMEX was reached9.67 per cent5.99% of Hyperliquid and 3.22% of Bybit. More importantly, BitMEX's rate performance seems more stable. This is crucial, because only arbitrage that can be held is really useful. Traders tend to focus only on peak data, but the real value of the financial rate strategy lies in whether its manifestations allow traders to actually cash without continuing anxiety. It is difficult to zoom in and hold it。

That's why XAUTUSDT emerged. It is not the most dramatic transaction on the market, but it is more practical. It provides a relatively clean, less maintenance-cost arbitrage version at a time when most of the traditional encryption-period current arbitrage has been compressed to nothing. This is a much more “civilized” layout for traders who wish to find a sound return strategy rather than engaging in tactical speculation。

Trading strategy two: Brent -- higher flash across platforms

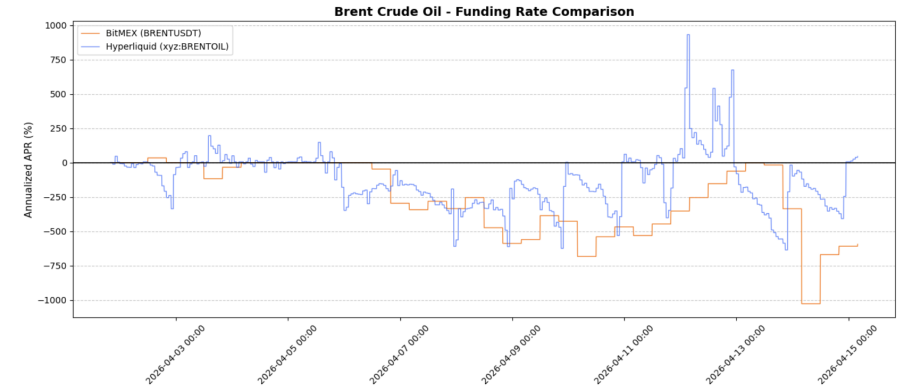

The second is much more radical and highly explosive. The difference in the financial rates between BitMEX and Hyperliquid has become one of the most attractive cross-platform differentials in the current market. The structure is simple:In BitMEX do more BrentusDT, and in Hyperliquid do empty Brent。

The rationale is equally simple. The BRENTUSDT fund rate on BitMEX is often extremely negative, while Brent on Hyperliquid usually remains positive. This creates a rare structure: traders can often charge money at both ends of the gap. This is exactly what traders used to dream of in the encryption market, the “two-way capture of money,” but this good day has largely disappeared in mature BTC and ETH ecology。

The data performance was exceptionally strong. In the latest snapshot, BitMEX's Brent fund rate is annualized-594.585%, and Hyperliquid is age40.792 per centI don't know. Over the past seven days, the price differential has implied an annualized rate of return361.607%80.5 per cent. In the 14-day cycle, the implicit annualized rate of return remained high220.740%30 days103.012%I don't know. In the 14-day and 30-day time window, BitMEX has 65.4% of the time of holding a low-cost platform. These are by no means normal data for mature markets, and this is the key. The price differential at this level is due to the fact that the crude oil trade, which operates on the encryption base, is still at an early stage, is highly dispersed and has not been fully offset by the arbitrage forces。

Why do these trading opportunities still exist

The deeper story is that TradFi is still in the early stages of price discovery. They attract different groups of traders than mainstream encrypted assets, respond more directly to macro- and geopolitical news, and they do so on a continuous basis even when markets are closed for bottom reference. Such a combination triggers distortions in pricing, which are not sustainable in a crowded mainstream currency arbitrage pool。

BitMEX is particularly interesting here, because its TradFi contract matrix is young enough, and these price differentials have not been completely wiped out by the whale's financial liability statement. This creates an excellent hunting ground for traders. Indeed, the market continues to reward those who are willing to leapfrog the obvious BTC/ETH transaction of funds and find opportunities elsewhere。

Final conclusions

Traders seeking the main position of real advantage are no longer trading in old-day money rates for mainstream encrypted assets. That has become an extremely crowded institutional strategy, with internal volumes compressing their returns to a level that is no longer cost-effective vis-à-vis the risks and investments they are taking. Alpha (excess gains) did not disappear, but simply moved to a corner of the market where structural inefficiencies still existed。

Right now, one of the clearest places to find these Alphas is the TradFi contract of BitMEX. XAUTUSDT offers a more pure and stable arbitrage, with an annualized rate of return of about 9.67 per cent over the past 73 days; and by comparing BitMEX to the Brent contract of Hyperliquid, BRENTUSDT offers an opportunity to offer a better and more tactical price differential, with recent window data showing annualized returns of up to three digits. The old arbitrage deal did not disappear; it simply left the most crowded lanes of the market。