Why is Intel supposed to take advantage of the heat when stock prices get stronger

Intel's real missing is not a story, but capital.

Original title: Intel Should Raise Capital

This post is part of our special coverage Syria

Original by Peggy, Block Beats

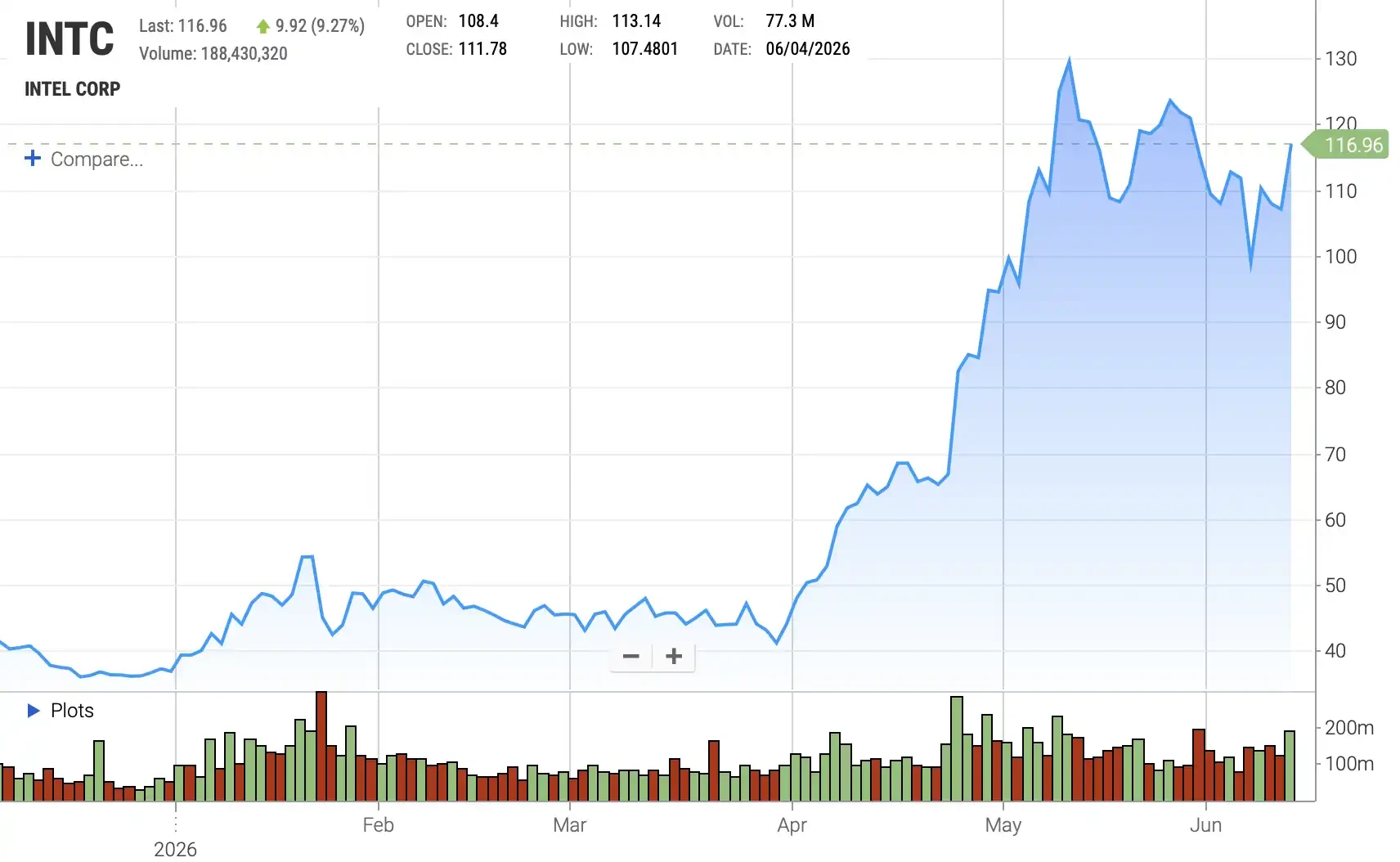

The editor presses that, since the breakout in early April, the Intel stock price has continued to be repaired and two key catalysts have taken place in June: first, the market has passed out Google's order for an AI chip to Intel, pushing its stock price to increase sharply; and second, the rare US dollar has moved the Intel rating directly from "run and lose" to "buy" and the target price has risen from $96 to $135. Behind this rebound, market re-pricing is not just the short-term performance of Intel, but rather its strategic position in AI CPU, advanced processors and the United States local chip supply chain。

INTC STOCK PRICE TRENDS

TODAY, INTEL’S NARRATIVE OF TRANSITION IS MOVING FROM “SELF-HELP” TO “RE-EXTENSION”. WITH CHEN LIWU'S SUCCESSION TO CEO, THE NEW BOARD OF DIRECTORS' BLOOD EXCHANGE, AND THE ENTRY OF STRATEGIC CAPITAL FROM THE UNITED STATES GOVERNMENT, SOFT SILVER, AND WEIDAR, THE MARKET'S EXPECTATIONS FOR INTEL HAVE BEEN SIGNIFICANTLY REPAIRED. BUT THIS ARTICLE REMINDS US THAT WHAT REALLY DETERMINES WHETHER INTEL CAN GO BACK TO THE CORE OF THE ADVANCED PROCESS IS NOT JUST THE CUSTOMER’S COMMITMENT AND STOCK PRICE REBOUND, BUT WHETHER IT HAS ENOUGH CAPITAL TO ACTUALLY BUILD UP THE SURROGACY。

Intel's problems over the past decade, according to the authors, have come to a large extent from financial engineering: selling assets, introducing joint venture partners, easing cash flow pressures through Smart Capital (reducing capital expenditure pressures through joint ventures and asset disposal), but also allowing long-term gains from core assets such as the Crystal Circle。

Today, what Intel should do most is not buy back stocks, but take advantage of strong equity prices. The reasons for this are straightforward: on the one hand, the current valuation is already high, with a dilution of shares of between 4 and 5 per cent likely to raise about $25 billion, which will significantly enhance Intel’s ability to build advanced production capacity; on the other hand, the United States government, soft silver, and Britain, among others, have previously entered the market at prices lower than current equity prices, at a time when the increase does not necessarily “punish” new shareholders, but may increase the book value per equity and allow strategic investors to receive book returns。

More importantly, the alternative financing that Intel has tried in the past has proven not to be cheap. Neither the sale of NAND, the reduction of Mobilee, the granting of Altera ownership, nor the introduction of Apollo, Brookfield and others through the SCIP (semiconductor co-investment project, i.e., long-term earnings from the Crystal Circle in exchange for external capital) are essentially cash-for-assets and future earnings. Now Intel spends $14.2 billion on repurchases of Fab 34 shares held by Apollo, precisely to show that it wasn't cheap to give the Crystal Mill a profit. Continued debt build-up would increase balance sheet pressure, with limited space for the continued sale of assets, and equity would be the cheapest and cleanest source of funding at present。

Thus, the central judgement of this article is that Intel is now in a state of "restoration" and that what is really missing is the capital needed to deliver on it. Agenic CPU (a new CPU for the AI smart age) needs, potentially large clients such as SpaceX and Tesla, and orders such as Inverda and Google, all give Intel the basis for demand that can be demonstrated to capital markets. For Intel, increased equity is not simply diluted, but, when market windows are opened, cheap capital is used in exchange for advanced production capacity, surrogate business and the enforcement of the Silicon sovereign narrative. Missing this window may be more expensive than financing itself

The following is the original text (for ease of reading and understanding, the original text has been consolidated):

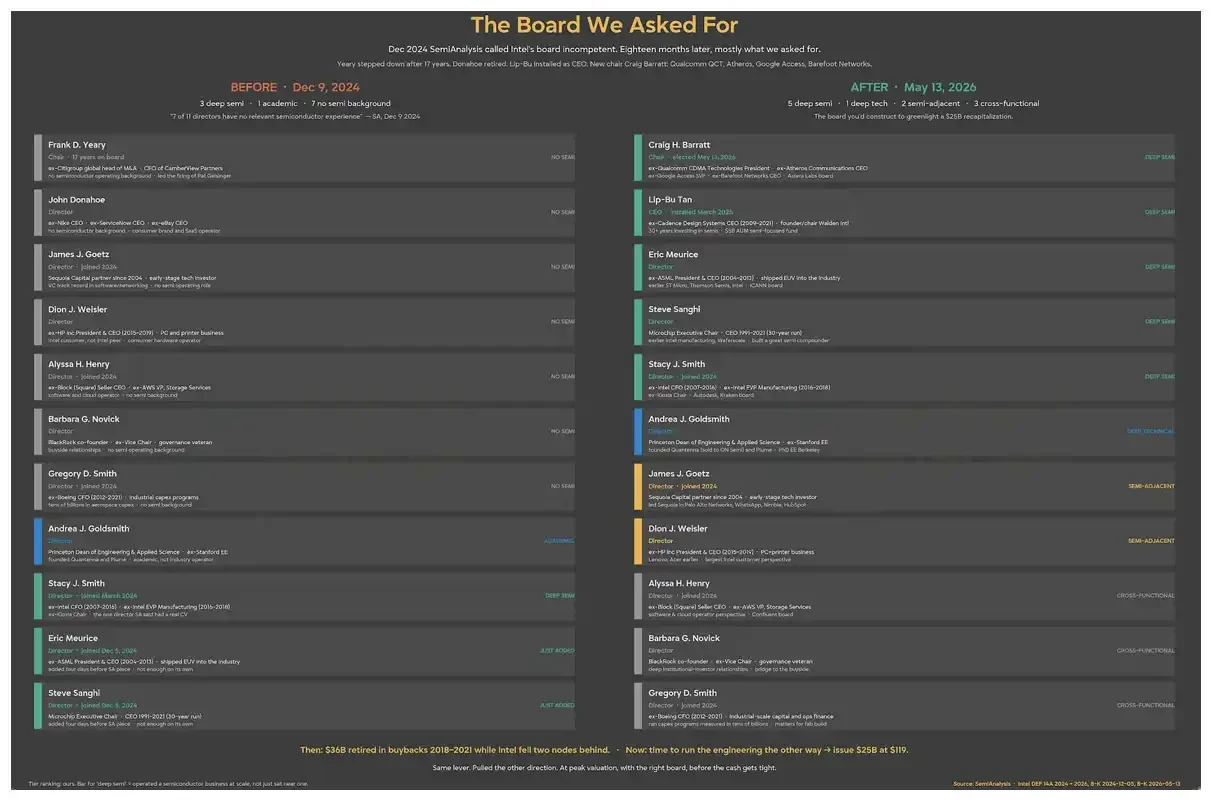

We've written a lot about Intel. For us, this company has special significance; it is also almost a starting point for the semiconductor industry. It is still not enough to say that we love Intel and recognize its role in the world. In the past, when the products of the early Intel failed, we pointed out the problem very bluntly; and we have always supported and expected its transformation. One of our strongest judgements is that the Intel Board of Directors is one of the most responsible parties for the decline of Intel, and recently we have finally seen the changes that we have always wanted to see。

Franky Yeary just left the board 17 years later, and now the new board is made up of people who really understand the industry, not just people who know financial engineering. The new chairman of the board, Lip-Bu Tan, was also on the board of directors of CEO, Steve Sanghi of Microchip, Stacey Smith and Eric Meurice of ASML. In other words, the Board finally really understood technology。

However, despite the partial initiation of Intel's transformation, there is still a long way to go before companies can be fully revitalized. We believe today that Intel should take the next major strategic bet under the new Board: not buy back stocks, but add enough stock to completely repair Intel's financial position once and for all。

Chen Liwu has pulled Intel back from the cliff and raised some $20 billion through strategic investments by the United States Government, soft silver, Altera and Weida. Intel should not stop in half, but should continue to take advantage of current stock prices. In the past bad years, the company had been a large net buyer of shares; now it was time to take advantage of strong equity prices. If properly operated, this will make Intel's transition more successful。

NOTE: CHEN LIWU IS INTEL CEO, APPOINTED IN MARCH 2025, ALSO ON THE INTEL BOARD

At this point, the equity is diluted and rewards investors who have already been betted

Look at the price at which these funds came in. The United States Government has subscribed to a maximum of 433 million shares at a price of US$ 20.47 per share, corresponding to 9.9 per cent of the share held at the time of the signing; as at the end of the quarter, 144 million shares were still held in trust. The equity price for soft silver is US$ 23.00, and the equity price for Inverda is US$ 23.28. Today, all of these holders are already floating。

Thus, the hunch that financing would punish investors who had just entered the room was in the wrong direction. The issuance of shares at prices far above these entry rates today would increase the book value of each share and would allow the United States Government, soft silver and British to receive book returns. That near-ten percent of sovereign capital anchor is also an important reason why Intel is able to complete large-scale distribution at lower cost. Intel is one of the few companies in the world that can sell stocks on a large scale while the United States government is at the bottom of the market. As long as such leverage exists, it is worth using。

Intel needs capital to make the transition

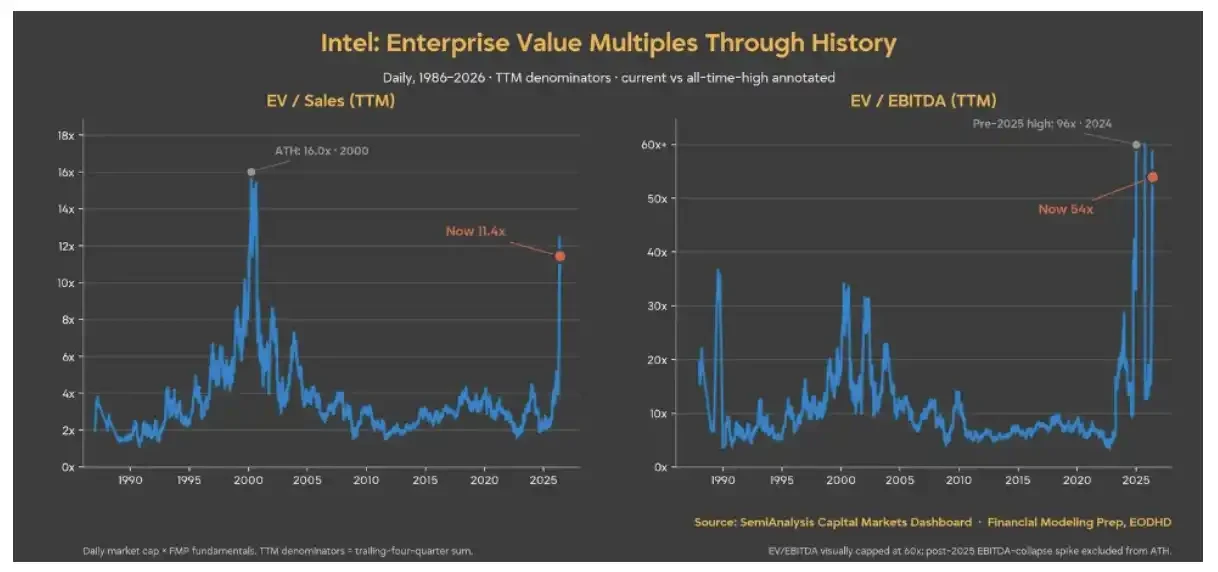

Intel has almost never been as expensive since the bubble in the last 12 months. We believe that the company has a bright future, but one of the most critical elements for achieving this is capital; current equity prices do not adequately reflect real implementation risks。

More importantly, even when the demand for Agenic CPU (a new CPU for the AI age of intelligent bodies) has re-emerged, and the situation is most optimistic, Intel cannot alone afford the inputs needed for all up-to-date scenarios. We believe that it is time for Intel to do a "reverse buyback": issue equity financing while the current market still needs to issue shares。

Equity is now the cheapest money Intel can get

Opponents may say that Intel has other ways of financing the round mill. But it tried these ways and just told the market that they were not working。

Apollo had invested $11.2 billion in 49 per cent of the equity of the Fab 34 joint venture; Brookfield had designed a financing structure for the Arizona Crystal Circle project; Silver Lake had taken Altera 51 per cent of its equity at the value of $8.75 billion, bringing about $4.3 billion in net cash to Intel. Intel also sold NAND operations to KK Hercules in stages and continued to sell Mobileye shares. “Smart Capital” (capital strategy to reduce capital expenditure pressure through joint ventures, asset sales, etc.) was at the heart of Intel’s narrative。

Then, on 31 March 2026, Intel agreed to repurchase Fab 3449 per cent of the shares held by Apollo and completed the transaction on 8 April at a total value of $14.2 billion, of which approximately $7.7 billion was in cash and $6.5 billion in cross-bridge loans. Management was right, and that was the key, to say that the buyback would increase the returns. If the return of the value of the value of the profit is increased, the sale of the value of the profit of the benefit to the partner has been by nature an expensive financing. The SCIP (Semiconductor Co-Investment Project) effectively ceded a portion of the company ' s best assets to external donors in exchange for a fund that appeared to be lower in nominal terms and higher in real terms. Intel has now demonstrated in its cheque book that it is more willing to own the mill itself and to assume the corresponding debt than to continue to give revenue to the mill。

So cut the other options. Continue to do more SCIP, the kind of option that management has just reversed at $14.2 billion. Continued debt build-up will be added to the $45 billion debt available on the balance sheet; if this bridge loan is included in Apollo, the debt will reach approximately $51.5 billion. The sale of large assets has also largely been completed, and Mobileye and Altera have either been sold or have been in possession. The rest is equity financing. At current valuation levels, equity is the cheapest capital in Intel's hands。

With the announcement of the large Terrafab project and the spillover requirements associated with the severe N3 shortfall, Intel's work has only just begun. To truly capture this particular window, Intel must be an important supplier for the entire industry at a time when there is a shortage of cutting-edge round supplies. And this huge wager requires much more money than Intel can afford to operate on cash flows。

Just 4 to 5 per cent of the shares are diluted, raising about $25 billion, and making the most optimistic narrative of supply capacity a reality at this critical time。

Agenic CPU needs, not enough to pay Terrafab's bills

SpaceX, Tesla and Terrafab represent large client commitments that are key to solving 14A capacity problems. The initial target was to reach 100,000 crystal-turned monthly energy (WSPM) and further expand it to 1 million tablets — which would be very difficult and would entail extremely heavy capital pressures. But this must happen because Chen Li Wu has publicly told the market that he will close his substitute business if there is no customer. Now that the client's here, it's time for construction。

Apart from Terrafab partners, Intel's order book is being filled. The DGX Rubin NVL8 configuration of Inverda listed the bi-Intel Xeon 6 host CPU; Google signed a multi-year agreement covering Xeon and custom IPU; and Sambanova also joined in the reasoning business. The volume of crystals behind these orders is not fully disclosed, but capital markets finance a visible order book at a much lower cost than a transition story. And Intel finally had orders to show to the market. Equity financing around contracted needs is quite different from equity financing around a commitment, with pricing logic。

As CPU demand fell short of expectations, Intel had been making every effort in the past to postpone capital expenditure. But now it's time to bet all the chips again, like the Gelsinger era. This is a critical moment for Silicon sovereignty, and Intel must continue to add codes。

Intel, a full multi-phase project, could cost up to $119 billion. While SpaceX will provide initial capital, Intel must also make a meaningful contribution. Even a marginal capital package would mean tens of billions of dollars in additional funding requirements that were not in Intel’s capital spending matrix a month ago。

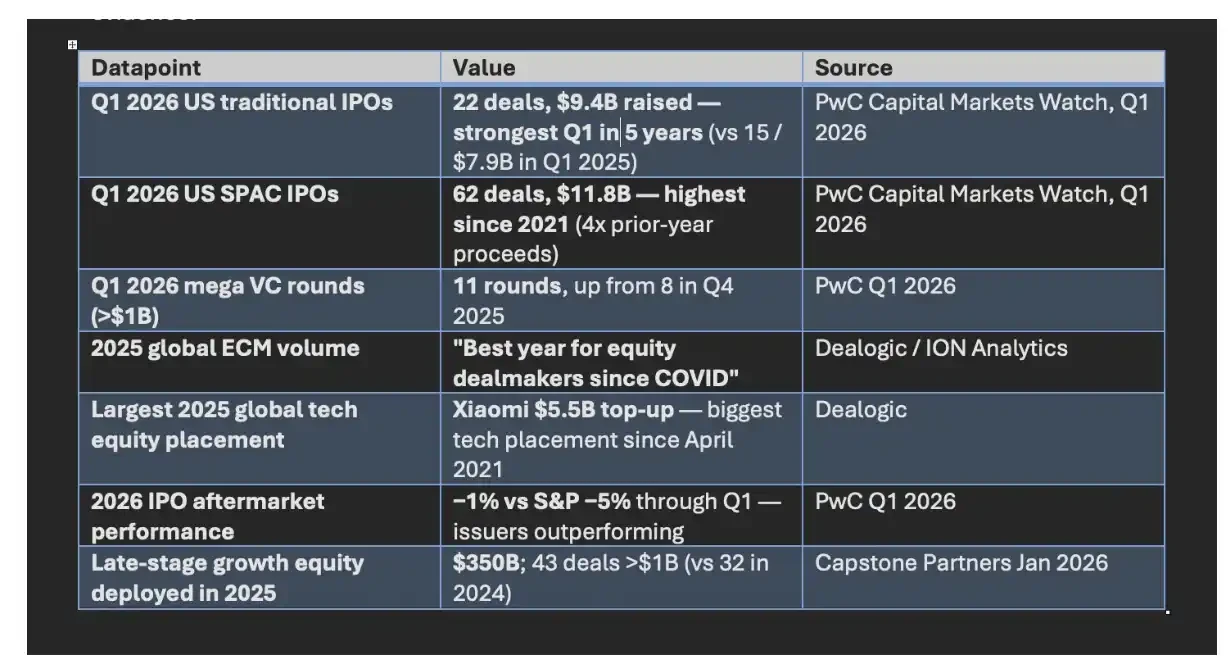

The time has come to end the financial work of the last decade and to issue stocks immediately. Because, while it's exciting to climb, it's very expensive. The current distribution window is the widest in recent times; if Cerebras could raise $5.55 billion, Intel could raise $25 billion. This view will only be stronger, as the market value of Intel is about $49.8 billion, which can support much larger follow-up distributions. According to our observations, this window seems to have been completely opened. Some data on other recent cases are provided below。

Trading window opened

In other words, the real question for Intel is no longer whether there is a story, but whether there is enough capital to make it productive. With strategic capital such as the United States government, soft silver, and British Weeda already in the air, and advanced supply in a tight window, equity financing is no longer merely a dilution of shareholders’ defensive actions, but may be an offensive option for Intel to re-establish its ambitions and stake its silica sovereignty. For Intel, missing this financing window may be more expensive than increasing itself。