IOSG: MSTR STRC DEPTH STUDY, 11.5% BTC FINANCING WHEEL BEHIND YIELD

@IOSG

Original link: https://mp.weixin.qq.com/s/Oj9HXOQJO-XV5j1k4yPoyg

Statement: For the purpose of reproduction, readers can obtain more information by linking to the original language. If the author has any objection to the reproduction, please contact us and we will proceed with the modifications requested by the author. Reproduction for information-sharing purposes only does not constitute any investment proposal and does not represent the views and positions of Wu。

Core viewsSTRC IS A WELL-DESIGNED FINANCING TOOL THAT TRANSFORMS THE DEMAND FOR SOLID HARVESTS INTO A BITCOIN BUYOUT PRESSURE. IN THE CATTLE MARKET, IT PROVIDES 11.5 PER CENT OF FLOATING EARNINGS AND LOWER PRICE VOLATILITY, BUT ITS RISK STRUCTURE IS ESSENTIALLY EQUIVALENT TO “SELLING DOWN OPTIONS” ON BITCOIN ASSET COVER, SO THAT WHEN BTC FALLS, IT DOES NOT REPLACE REAL FIXED-INCOME PRODUCTS。

The real vulnerability of STRC is not the BTC price, but the mNAV. Once MSTR's mNAV falls 1.0 times more than four weeks in a row, the wheel enters a passive mode downward spiral within three months. We're judging the probability that this trigger will appear in the second half of 2026 by about 70%, when the STRC will have a buy-in point of $85-90. If the trigger doesn't work, it means that Saylor has succeeded in creating a brand-new BTC raw credit tool class。

Background

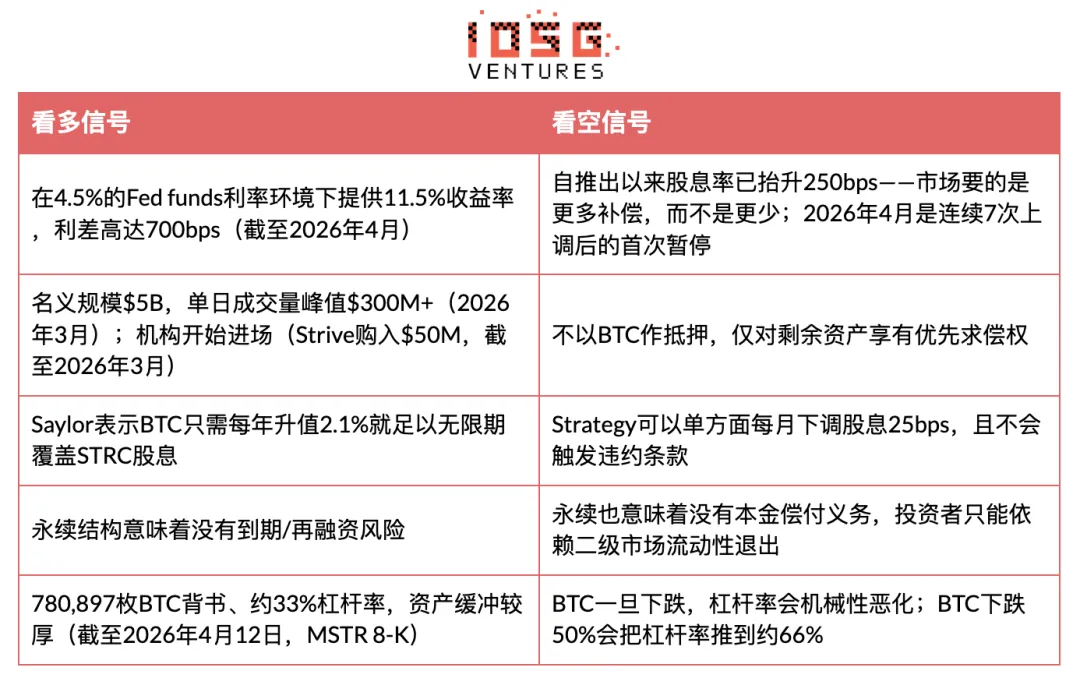

Strategy (former MicroStrategy) launched the STRC (“Stretch”) which is a sustainable priority stock of $100 in target face value, which maintains price stability through monthly floating dividends. As of 31 March 2026, STRC had a nominal size of $5B with a single-day trade peak of over $300M (data as of March 2026) and, since its launch, has provided more than $3.5B in BTC purchases for Strategy, its most important financing carrier. & nbsp on Strategy balance sheet as at 12 April 2026;780,897 BTCS33% leverageSTRC ATM REMAINING AVAILABLE AMOUNTS ABOUT $21.6BI don't know。

- THE TOOL IS IN AN INNOVATIVE CATEGORY: IT LOOKS LIKE A MONEY MARKET FUND (PRICE STABILITY, HIGH RATE OF RETURN), BUT THE CREDIT RISK ASSUMED IS ENTIRELY FROM A SINGLE COMPANY, THE BTC HOLD。

Before moving on, let's make it clear where we might be wrong。

If our analysis is wrong, it will be because: the traditional collectors are really willing to accept the reverse risk for the 700bps spread; STRC is $50 billion in size over three years, becoming the real BTC yield curve; and Sailor has succeeded in converting the BTC securitization into an interest-bearing asset acceptable to the group. This result will represent the encryption of the case of the largest integration into traditional finance to date - an asset class that did not exist until 2025 and added $50 billion+。

- IN THIS OPTIMISTIC CONTEXT, THE INTEREST PAUSE IN APRIL 2026 IS NOT A WARNING SIGNAL, BUT A FEATURE: A MATURE INSTRUMENT BEGINS TO STABILIZE GAINS AFTER EARLY PRICE DISCOVERY IS COMPLETED, SIMILAR TO THE EARLY HIGH-YIELDING DEBT ETF, WHICH GOES DOWN WITH THE INTRODUCTION OF GRADUAL RE-PRICING。

02. Dismantling of arguments

STRC's core innovation: it transforms income-seeking funds into BTC buyout pressure. When the STRC transaction is close to $100, Saylor uses ATM for new distribution (about 40 per cent of the daily turnover), buys BTC with the money received, and issues MSTR common shares more than NAV (mNAV> 1x) for leverage. The end result is that a 100M STRC daily exchange can pry BTC purchases of about $120M。

But the weakness of the mechanism lies in its cyclical nature at the bottom: the STRC can be set at $100 because investors believe it is; and Saylor maintains this trust by increasing dividends. The anchor is not backed by collateral, but by confidence and is maintained by a continuous stock auction without a formal ceiling. Once that confidence breaks down, the auction becomes more expensive。

Evidence and comparison: STRC vs. other bitcoin convertibles

Critical Insight:For Strategy, STRC converts the demand for solid harvests into BTC accumulated fuel. For investors, it gives Sharp an optimised return in a benign environment, but hides a BTC's "sell and fall." The description of NYDIG is very precise: "It's similar to making an empty drop option on the bitcoin asset cover - by taking down the risk of BTC falling to erode the asset buffer in exchange for a gain."

WHEN DID HE DO WELL

STRC, WHEN DOES IT GET BAD

STRC WHEN WILL IT FALL: DEATH SPIRAL

THE KEY QUESTION IS: WILL STRC ENTER A SELF-REINFORCING DOWNWARD CYCLE? THE ANSWER IS YES, BUT SUBJECT TO CERTAIN CONDITIONS. THE MECHANISM HAS THREE INTERRELATED PATHS OF FAILURE。

# PHASE 1: BTC FALLING THROUGH $100 ANCHOR

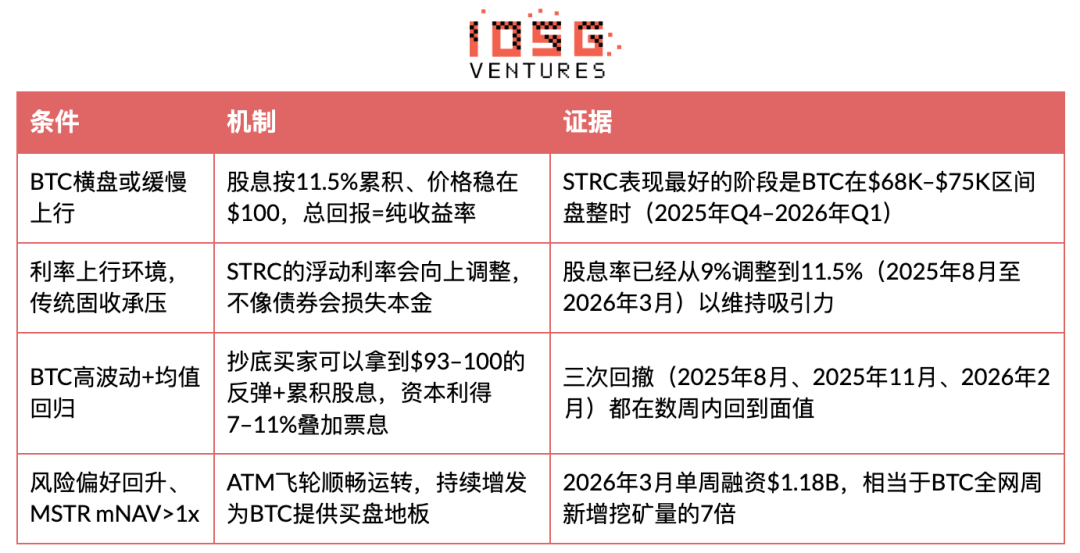

When the BTC crashes (e.g. 45% retreat from historical heights at the end of 2025), Strategy's leverage will go mechanically. Based on 780,897 BTC, 33% leverage rate (MSTR 8-K as of 12 April 2026), if BTC drops by 50%, the leverage rate is pushed to about 66%. At this point in time, the credit quality of STRC deteriorated, as its preferential claim to the remaining assets became thinner. The price fell $100. This has happened three times (August 2025: about $92, November 2025: mid-discretion low, February 2026: about $93), but each time the BTC rebounded quickly and pulled the anchor back。

# Phase two: a stock-up trap

Guidance submitted by Strategy to the SEC: 25bps per month if monthly VWAP is between $95 and $99; 50bps per month if $95 falls. From 9% to 11.5%, the dividends have risen cumulatively in about eight months (August 2025 to April 2026) 250bps, averaging about 31bps per month - This rate is faster than the re-pricing of the preferred shares of any similar company under stable market conditions. 2026, April was seven consecutive increasesFirst pauseI don't know. Two readings: (a) demand is steady — looking at more; and (b) Strategy has touched the traditional fixed buyer's sensitive ceiling for yield — looking empty. This is the single most valuable signal for the next 1-2 months。

If the BTC continues to be depressed, the dividends will have to continue up to attract the buyer back to the face. Under the 5B scale, an increase of 100bps would mean additional cash expenditure of about $50M per year; if STRC expands to $20B (the authorized ATM level), the cost per 100bps becomes $200M per year. The bear market, which lasts for more than six months under the current upward adjustment, will push the rate of return of the STRC to 13-15 per cent; at this level, the annual dividends expenditure of $20B would exceed $2.6-3 billion, draining a significant portion of the potential gains of the Strategy BTC reserve, forcing it to choose between “continue upward adjustment” and “renounce stabilization narratives.”。

There are no official ceilings on the rise in dividends, and this “no-cap” upward movement is precisely the point of focus on empty space。

# Phase three: mNAV falling 1 times and the wheel breaking

That's the real breakpoint. Strategy buys BTCs and leverages them with the issuance of MSTRs (mNAV> 1x) at prices higher than NAVs. If the BTC falls deep enough to double the mNAV, the distribution stock dilutes the value of existing shareholders, and Saylor cannot leverage the distribution. At that time, Strategy faced a difficult choice: (a) to continue issuing STRC at a higher rate of dividends and to accept a higher leverage; (b) to unilaterally reduce dividends (25 bps per month) by the terms of the SEC filing; and (c) to sell BTC into a falling market。

Saylor repeatedly stated that he would never sell BTC. BitMEX Research concludes that (b) is most likely to happen: “Strategy will not sell bitcoin, it will simply give up STRC's quest for stability. The pressure will be transferred to the STRC holder。

An early warning signal has been lit: on the week of April 6-12, 2026, the MMR ATM was increased to & nbsp;$ 0- All financing is done through STRC ($1.00B, 1,028 million shares; MSTR 8-K). The mNAV has reached the point where Saylor is not willing to take the risk of diluting ordinary shares. The third phase of the prefix has been partially triggered — the wheel is already operating on one leg。

# Quantified collapse

Why is this different from UST/Terra:UST relies on algorithmic casting mechanisms, supported only by endogenous coins (LUNA). STRC is supported by real BTC, and Strategy has discretion to choose lower dividends instead of mandatory liquidation. The STRC floor is not zero - it is the preferred claim for surplus assets in liquidation. But if the BTC drops over 60% and stays low, this floor may be well below $100。

The key variable is time。EACH PREVIOUS STRC RETREAT WAS REPAIRED WITHIN WEEKS BECAUSE THE BTC REBOUNDED. WHAT A REAL CRASH REQUIRES IS A CONTINUOUS BEAR MARKET (WHICH LASTS FOR MORE THAN THREE MONTHS UNDER $50K), ALLOWING THE STOCK-UP MECHANISM TO OPERATE LONG ENOUGH TO ERODE CONFIDENCE. THE LONGER STRC REMAINS BELOW FACE VALUE, THE LONGER ITS DIVIDENDS CONTINUE TO RISE, THE MORE IT IS LIKE A COMPANY EXTENDING ITS INCREASINGLY FRAGILE DEBT AT EVER HIGHER INTEREST RATES — A MODEL THAT HAS A VERY CLEAR ENDING IN CREDIT MARKETS。

Capital structure priorities:THE ORDER OF LIQUIDATION IS AS FOLLOWS: REVERSIBLE DEBT (APPROXIMATELY $8.2B) STRC RANKS BEHIND $8.2B UNCOLLATERALIZED DEBT AND STRF PRIORITY SHARES。

Industry perspective

“STRC risks are significantly higher than short-term United States debt ... When music stops, investors may feel offended.” — BitMEX Research, A Bit of a Stretch (November 2025)

“The appropriate way to assess STRC risks is to look at them in terms of governance and subordination, rather than simply focusing on the risk of payment.” — Greg Cipolaro, Director of Global Studies, NYDIG (March 2026)

“IT IS AKIN TO EMPTYING THE BITCOIN ASSET COVER OF A DROP OPTION — BY TAKING THE DOWNSIDE RISK OF BTC FALLING TO ERODE ASSET BUFFERS IN EXCHANGE FOR GAINS.” — NYDIG STUDY (MARCH 2026)

THE CORE DIFFERENCE IN THE ANALYSTS ' VIEWS IS HERE: LOOKING AT STRC AS THE SAFEST 11.5 PER CENT OF THE CURRENT MARKET FOR REVENUE; LOOKING AT EMPTYS AS BEING THE WRONG PRICED CREDIT RISK FOR PRODUCTS PACKAGED INTO THE MONEY MARKET. THE CORE CONCERNS OF LOOKING AT SPACE DIRECTLY CORRESPOND TO THE STOCK-UP MECHANISM DESCRIBED ABOVE: STRC DOES NOT SUDDENLY DEFAULT, BUT SLOWLY RE-PRICING -- – THE LONGER THE BTC GETS, THE MORE IT SLIPS FROM A QUASI-MONETARY INSTRUMENT TO A HARD-WON PRODUCT. THIS GRADUAL SLIDE IS THE REAL RISK, NOT THE COLLAPSE OF ONE NIGHT。

0.3 Inferences and projections

Bottom line:STRC is a truly innovative financial instrument that works very well in an environment that it is designed to do well — a smooth BTC with uplifts, open capital markets, mNAV> 1x. In this situation, it can provide 11.5 per cent of the manageable gains and is indeed attractive. But its downside structure is asymmetric: good times earn votes, bad times take on a centralized, single name BTC credit risk. It is not a substitute for national debt or diversified high-yield debt, but a bet that Strategy BTC accumulates leverage positions for the continued operation of the wheel - it is simply packaged into solid harvests。

Three new signals (as of April 2026)

#Signature One: An increase in dividends was suspended for the first time in April (CoinDesk, 1 April 2026)。

After seven consecutive increases in August 2025 to March 2026 (from 9% to 11.5%), Saylor maintained the dividends in April. Two readings are: (a) demand is stable at this rate of return and is seen to be high; and (b) Strategy has touched the traditional fixed buyer's yield-sensitive ceiling and is blind. This is the single most valuable signal for the month of May - June, and the point around which the mNAV trigger frame above revolves。

#SIGNATURE II: ON APRIL 6 – 12, MSTR ATM WAS INCREASED TO $0 AND ALL FINANCING WAS COMPLETED BY STRC ($1.00B; MSTR 8-K, APRIL 2026)。

At the current BTC price level, mNAV has reached the point where Saylor is reluctant to take the risk of diluting ordinary shares to continue MSTR. The prefix of the third stage of the death spiral has been partially triggered — the wheel is operating on one leg。

#3: Last week the BTC bought an average price of $71,902 per item, which is lower than Strategy ' s historical cost of $75,577 per item (MSTR 8-K as of April 12, 2026)

Strategy is buying into a weak DCA. The wheel is still spinning, but every marginal buy is buffering against thinness, not thickness — in contrast to the build-up of the 2024-2025 round。

Investment recommendations

HOLD, WAIT FOR BETTER ENTRY POINTS AND BTC TO GO。

CURRENT STATUS: HOLD CURRENT POSITION, DO NOT HOLD HOLD UNTIL BETTER SIGNALS ARE AVAILABLE。MSTR's mNAV has been compressed to the nearest 1.0 times. STRC remains at $100 face value and pays 11.5 per cent dividends, reflecting that the dividends mechanism is still functioning as designed. But the security margin is very narrow。

Rebuilding condition:The BTC station is $70-75K, and MSTR mNAV is confirmed at more than 1.1 times for two consecutive weeks. At that time, STRC returns to re-entry conditions near the $100 nominal value. According to historical data, the following + subsequent BTC rebound combination of $95 has contributed 7-11 per cent of the accumulated interest on capital - but only in an environment where BTC could rebound within weeks (2025, August 2025, & nbsp; November, 2026, February). It is truly unknown whether the next retreat continues this pattern or foresaw a more sustainable bear market。

Exit signal:In any of the following cases, the sales assessment is initiated: (a) MSTR mNAV falls 1.0 times and lasts more than two weeks; (b) STRC VWAP falls below $95 for four consecutive weeks; (c) BTC drops $55K。

Suches

- Strategy.com — STRC Production Page

- https://www.strategy.com/strech

- CoinDesk -- "The Genius and the Danger of STRC"

- https://www.coindesk.com/business/2026/03/22/the-genius-and-the-danger-of-strc-how-strategy-s-new-funding-model-bends-so-it-doesn-t-break

- Crypto Narratives — "Understanding STRC: How Strategy turns yeard demand into BTC buying"

- https://cryptonartives.substack.com/p/understance-strc-how-strategy-turns

- "A Bit of a Stretch" STRC Analysis

- https://www.bitmex.com/blog/a-bit-of-a-strech

- "STRC's Sharpe Ratio of 3.08: Real Alpha or Standard Illusion?"

- https://www.ainvest.com/news/strc-bitcoin-backed-prifered-equity-promises-11-5-yield-sharpe-ratio-3-08-real-alpha-strident-ilusion-2603/

- Investopedia — "Meet Stretch: Michael Saylor's New Tool"

- https://www.investopedia.com/meet-strech-michael-saylor-s-new-tool-for-using-bitcoin-to-pay-a-big-dividend-here-s-what-to-know-11921210

- Blockonomi -- "STRC Rices $1.18B in One Week"

- https://blockonomi.com/strategys-strc-raises-1-18b-in-one-week-buying-seven-times-bitcoins-weekly-mined-supply/

- Seeing Alpha — "Most Undervalued Bitcoin Security"

- https://seekingalpha.com/article/48855379-strk-the-host-undervalued-and-versatile-bitcoin-security-today

- CryptoTimes – "Strategy's Bitcoin Empire: How Preferred Personals Are Redefining Corporation Finance"

- https://www.cryptotimes.io/2026/03/21/strategy-inc-s-bitcoin-empire-how-referred-perpetuals-strc-strk-strf-strd-are-redefining-corporate-finance/

- Benzinga — “Saylor: STRC Achieved Better Risk-Adjusted Returns Than NVDA, TSLA”

- https://cdn2.benzinga.com/crypto/cryptocurrency/26/03/515736/michael-saylor-strc-stock-achieved-better-risk-adjusted-returns-than-nvidia-tesla

Appendix

Timeline

Consistency — who can break prices

Strive's $50M purchase was mentioned, but there was no discussion of whether STRC had a few large institutional holders - If they rotate out of the game at the same time, will they crush the trade of a daily average of 258 m and press STRC self-realization below the face value? This is the risk of crowding。