Graysdale researcher: 14 times the ratio, how much room is there for the Robinwood mark

By Michael Zhao, Zach Pandl

Other Organiser

Original link: https://www.techwork.com/zh-CN/article/31800

Statement: For the purpose of reproduction, readers can obtain more information by linking to the original language. If the author has any objection to the reproduction, please contact us and we will proceed with the modifications requested by the author. Reproduction for information-sharing purposes only does not constitute any investment proposal and does not represent the views and positions of Wu。

Imagine a start-up company killing an extremely competitive industry in less than three years. Last year's revenue was about $800 million, facing a huge potential market. The team was streamlined and the leverage for operations was extremely high. All of this was done when users of major markets, such as the United States, were still unable to use it。

That's Hyperliquid。

Figure: Exhibit 1, Hyperliquid is a breakout in the contemporary digital asset industry

At the heart of Hyperliquid is a decentralised exchange dedicated to permanent contracts, a derivative without maturity. The code-encrypting contract is already a big business: the industry-wide average daily trade in 2025 was about $20 billion. The market has long been dominated by Binance, OKX, Bybit and these centralized exchanges. Hyperliquid was the first decentrization project to actually take a share of the trade volume and the balance。

Continued market-grabbing for durable contracts alone would be sufficient to drive a significant growth of the platform. But Hyperliquid's ambition is far more than that. Although a lasting contract remains the main source of revenue, Hyperliquid today is a financial services platform covering many vertical areas。

Figure: Multiple financial services layout for Exhibit 2, Hyperliquid

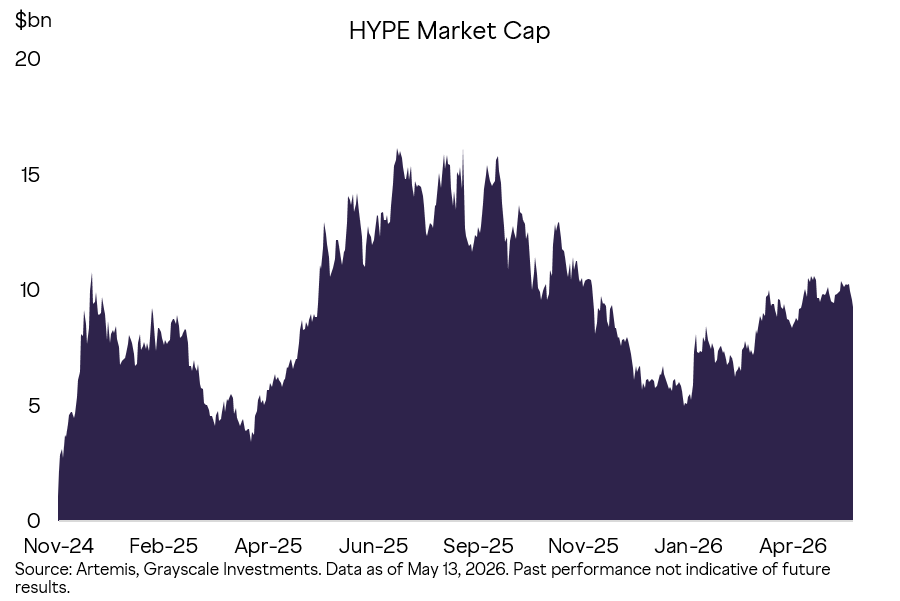

Like other block chain agreements, Hyperliquid is not a company and does not issue shares. Its tokens drive the entire network to gain value from transactions. The market value of HYPE is about $13 billion, with an encrypted asset 8th place by market value. The HYPE valuation multiplier is not high compared to comparable listed companies. Given the growth of the platform ' s users, the large potential market and the forthcoming deregulation, we believe that Hyperliquid still has significant up-to-date space。

Figure: Exhibit 3, HYPE market value trend since coming online

The basis of the contract

Although Hyperliquid had a bigger blueprint, it was the centralization of the contract transaction. This product was born in the encryption industry, and Grayscale thought it would eventually infiltrate traditional finance。

traditional futures have maturity dates. a crude oil futures contract, for example, provides for the delivery of a certain amount of crude oil at a given date. the participant whose hold is due is required to physically deliver or receive the subject-matter assets. if you only want to make a purely financial opening, the user needs to "roll" the position to a later contract before the expiry date。

There is no expiry date for the renewal of the contract and there will never be a delivery. It is designed to provide net financial exposure to targeted assets, usually 24/7, for hedgers and speculators。

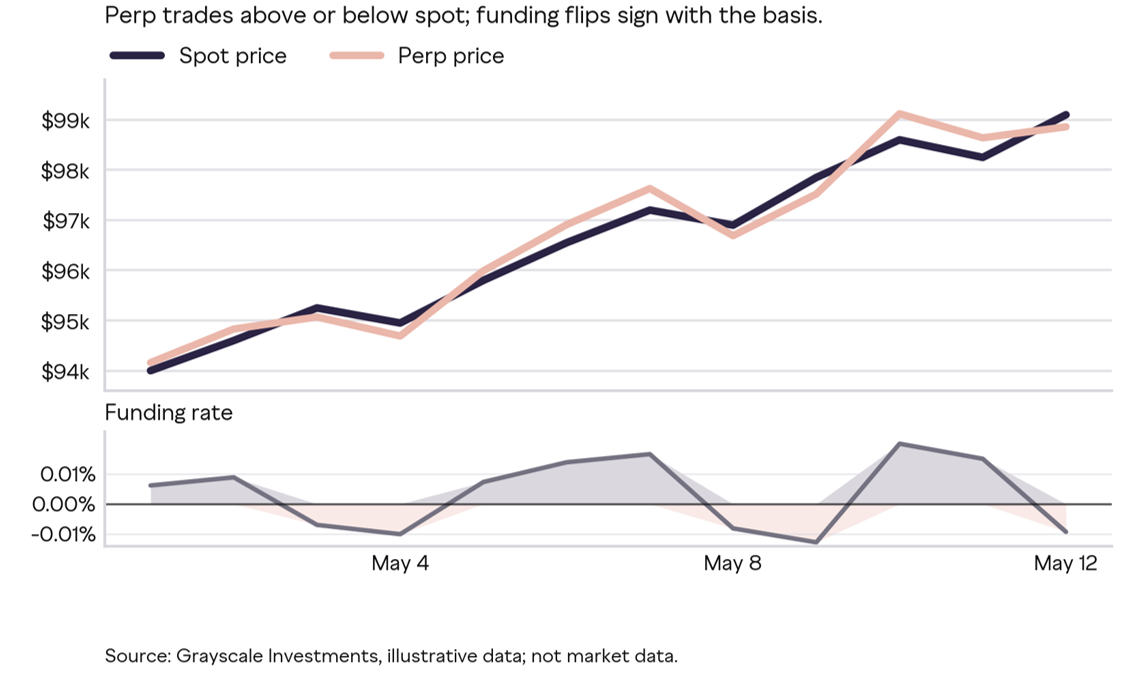

traditional futures have been able to anchor the price of the targeted assets because people have to deliver at maturity. the contract will never expire. how does it keep price tracking? the answer is the funding rate mechanism: a small fee is paid periodically between multiple and empty. when the price of a permanent contract is higher than the price of the spot, many payments are made to the empty; lower than the spot, in turn. the greater the deviation, the higher the cost。

Figure: Exhibit 4, Assets for which the fund rate mechanism anchors the price of the contract for perpetuity

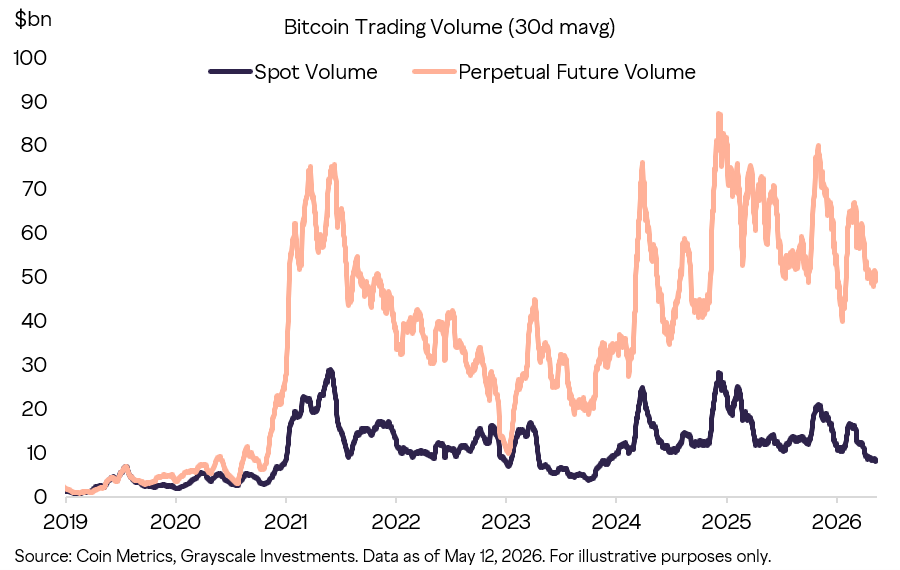

There is a natural connection between the contract and the encryption market. Encrypted assets are traded 24 hours a day and there is a strong demand from the diaspora and professional speculators, and new assets appear at a much faster rate than the currency in traditional futures exchanges. The renewal of the contract gives traders a simple way to express directional views, to flush the openings, and to leverage all day. It is now one of the core markets discovered by encrypted prices。

Figure: Exhibit 5, Global Bitcoin Extension Contract and Cash Transactions

THERE ARE A NUMBER OF CHANNELS THROUGH WHICH IT CAN LEVERAGE: TRADITIONAL BROKERAGE BOND ACCOUNTS, FUTURES WITH MATURITY DATES, OPTIONS, LEVERAGE ETFS. THE EXPERIENCE OF THE ENCRYPTION MARKET SHOWS THAT WHEN ALL OPTIONS ARE IN FRONT OF THEM, THE BULK WILL GIVE PREFERENCE TO THE RENEWAL OF CONTRACTS, LARGELY BECAUSE THEY ARE SIMPLE ENOUGH. A SIMILAR MIGRATION OF USERS IS EXPECTED ONCE MORE EXTENSIVE PLAYERS IN TRADITIONAL MARKETS ARE ABLE TO USE DURABLE CONTRACTS。

Hyperliquid breakthrough

Hyperliquid achieved a core breakthrough:Performance at the Centralized Exchange level + Transparency of block chains and self-custodyI don't know。

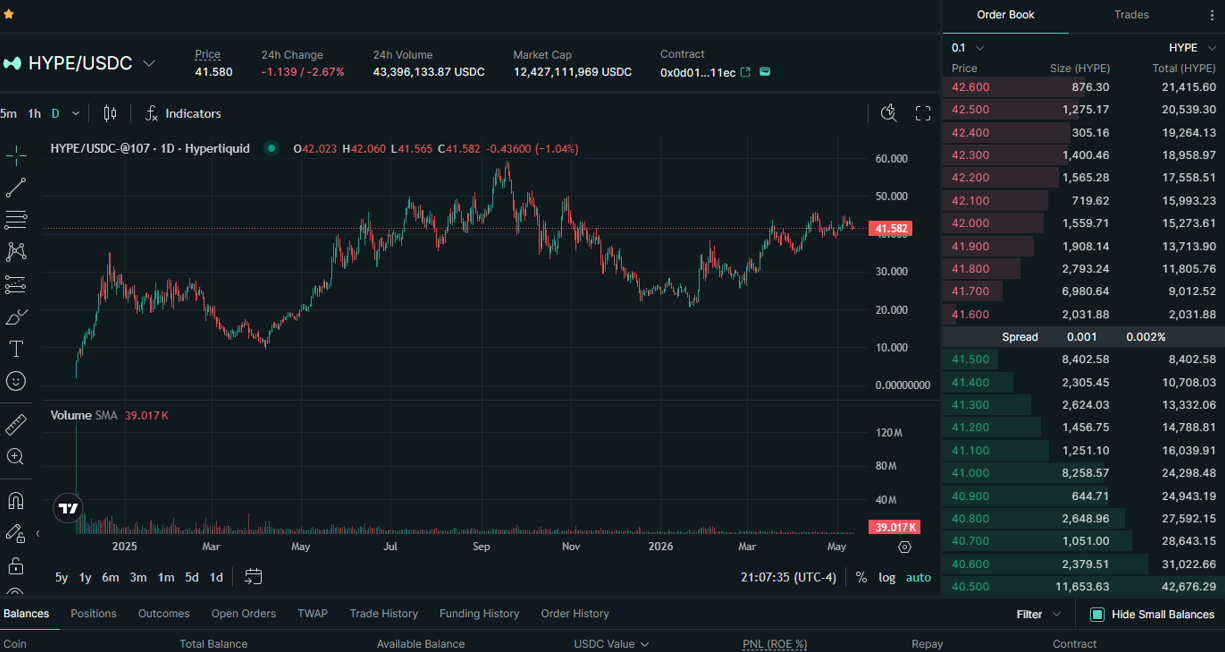

From the perspective of traders, there is little difference between Hyperliquid and the centralized exchange: deep order book, fast-transaction, familiar warehouse management interface. However, every Hyperliquid transaction is recorded in the chain, including liquidation, and the user remains self-hosting。

Figure: Exhibit 6, Hyperliquid trading experience close to the Centralized Exchange. Source: app.hyperliquid.xyz screenshot, May 12, 2026

Leverage transactions are the most brutal segmented track of the encrypted market, with extremely demanding users. Hyperliquid's success depends on product power。

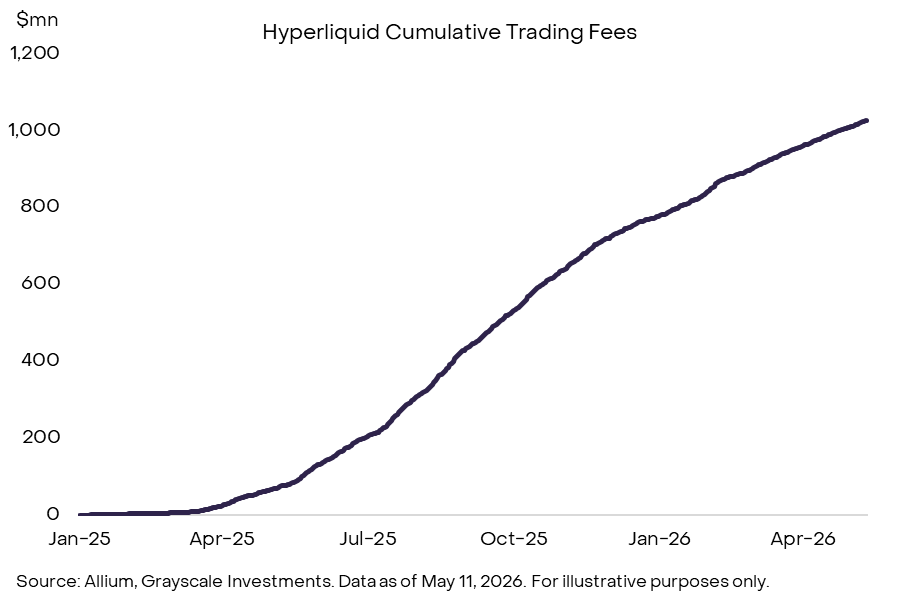

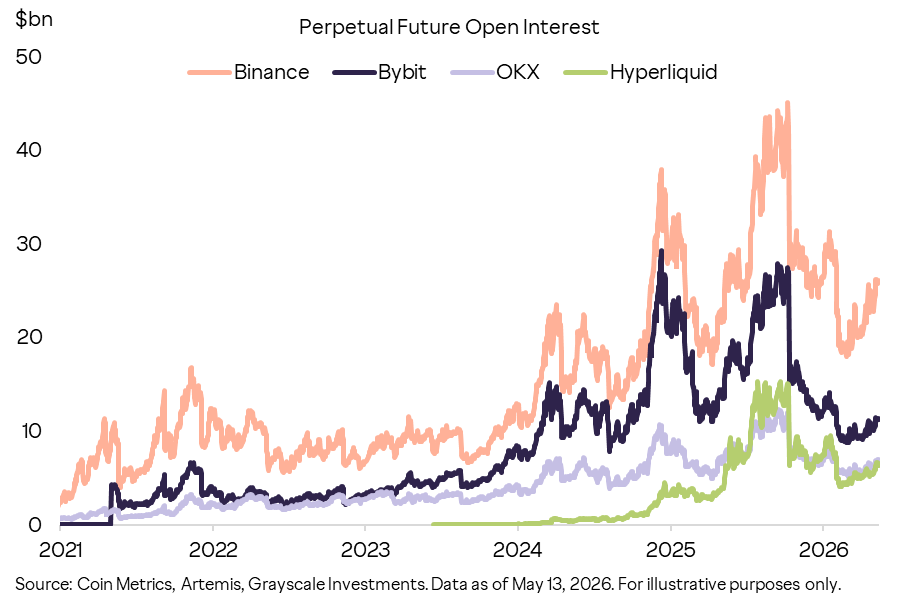

THE NUMBER SPEAKS: $2.9 TRILLION IN PERMANENT CONTRACT TRANSACTIONS IN 2025, AND ABOUT $7 BILLION IN CURRENT OPEN BALANCES, RANKED BY OI AS THE INDUSTRY'S THIRD OR FOURTH-LARGEST PERMANENT CONTRACT EXCHANGE. THE VOLUME OF TRANSACTIONS, THE UNEVEN AMOUNT, THE REVENUE FROM FEES AND MARKET INTEREST HAVE GROWN SIMULTANEOUSLY, AND THE PLATFORM HAS EXPANDED FROM A PURELY ENCRYPTED MARKET TO A BROADER RANGE OF TRADABLE ASSETS。

Figure: Exhibit 7, Hyperliquid has been included in the third or fourth-largest encrypted contract exchange

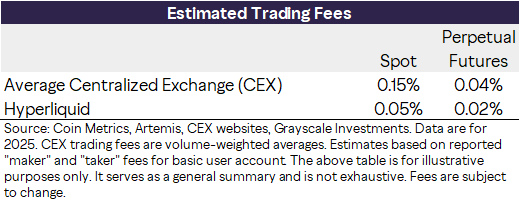

In terms of rates, Hyperliquid has all the cost advantages of centralized transactions. Based on 2025 BTC and ETH transaction data, the weighted average rates for CEX are 15 base points (bp), futures 4bp and Hyperliquid 5bp and 2bp, respectively。

Figure: Exhibit 8, trade volume weighted rate comparison. Note: Public marker/taker rate estimates based on base user accounts, excluding such factors as rate classification, discounts and order book depth

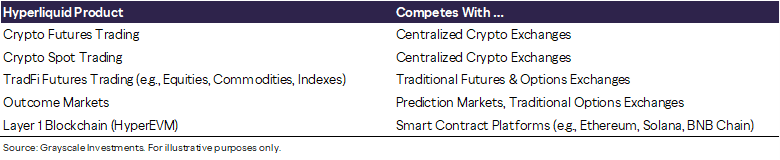

Of even greater concern is the fact that Hyperliquid has extended its product line beyond the encryption and sustainability contract through open structures。

The new functionality is usually introduced through Hyperliquid Improvement Proposals (HIPs), with products being deployed by third-party developers rather than by the Hyperliquid team itself。

HIP-3 allows developers to deploy new, sustainable contract markets, including non-encrypted assets such as stocks, bulk commodities, indices, etc. These markets are popular among users and have begun to act as a spot for post-price discovery of traditional traded assets. Bloomberg uses this framework directly to describe Hyperliquid’s long-term contracts, stating that its long-term contracts for crude oil, gold and silver “may signal the direction of these markets when mainstream transactions resume”. In another story, Bloomberg describes Hyperliquid as a "global-leverage commodity trading place"。

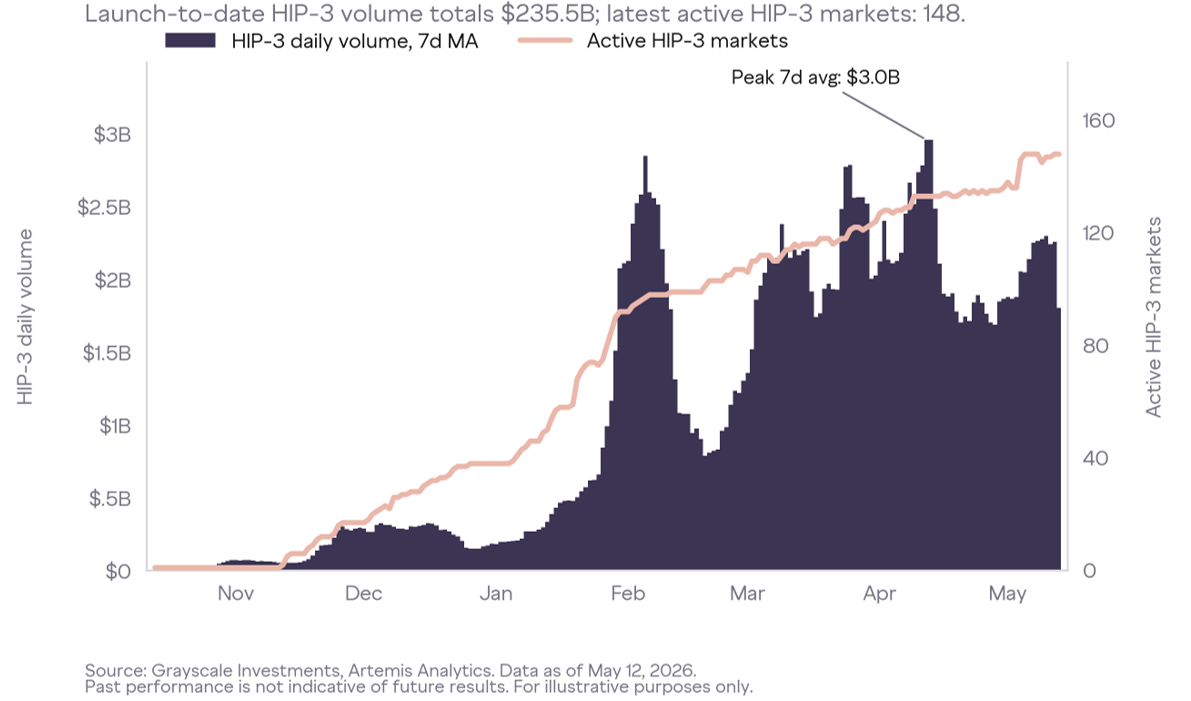

Trade volume data confirm this location. During the silver boom in February, silver HIP-3 contract turnover was reported to exceed $4 billion. At some point on February 5th, the nominal volume of HIP-3 long-term silver contracts was approximately 1% of COMEX silver transactions. During the period of crude oil volatility in the Middle East, the HIP-3 contract for the renewal of crude oil exceeded $4 billion in 24 hours on 9 April, at one point exceeding the amount of the Bitcoin contract for the renewal. An officially authorized bill 500 contract is now also traded through HIP-3 on Hyperliquid, including weekends. Since it went online, the cumulative volume of HIP-3 transactions has exceeded $230 billion, with more than 140 active transactions currently under way。

Figure: Exhibit 9, HIP-3 Extension of Hyperliquid from encrypted forever contracts to broader asset classes

HIP-4& nbsp; further extended to the outcome market (outcome markets), similar to the binary option for forecast market contracts. These contracts are also deployed by third-party developers, but transactional activities continue to generate fee revenue for Hyperliquid。

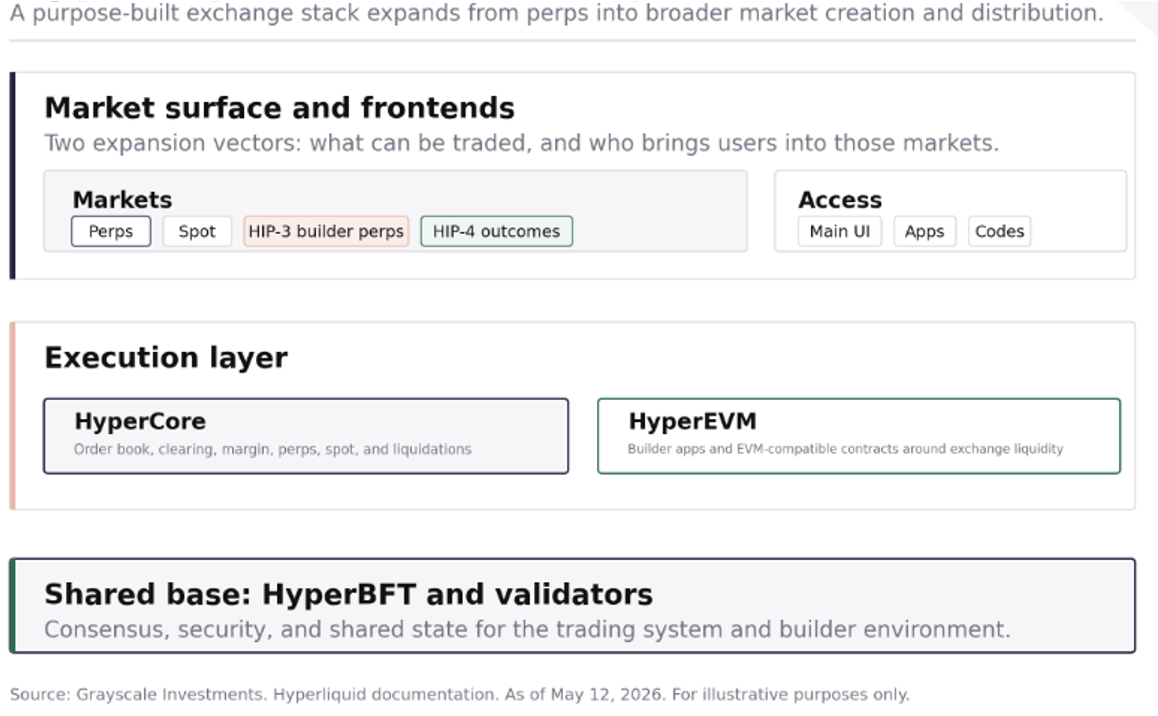

Hyperliquid Technical Architecture

The bottom structure revolves around two core components:

HyperCore is a trading system that includes order bookings, liquidations, permanent contracts, spot, deposit and liquidation environments. this is the main part of how traders interact directly。

HyperEVM& nbsp; is an environment at the developer level that provides an EVM compatible development interface with the Hyperliquid system. The strategic intent is to allow the application of the liquidity, user and asset base built around what has been created by the exchange, rather than starting with a cold network without primary financial activity。

HyperBFT& nbsp; is the consensus level of the commissioning certificate of interest and is responsible for cybersecurity。

The key is the design choice: Hyperliquid is not a universal public service application, but a dedicated chain and implementation vault that optimizes the performance of the exchange, with the aim of making the chain experience competition with a centralized trading infrastructure。

Figure: Exhibit 10, Hyperliquid as a framework for market platforms

Five elements of success

Hyperliquid was opened to the public in August 2023, earlier than the United States listing of Bitcoin ETP, when DeFi as a whole was at a low point. Its success is not the product of speculative bubbles, but rather because it solves a specific problem better than most encrypted infrastructure projects: making chain transactions truly available to high-frequency traders。

Five key factors:

Product focus。& nbsp; Hyperliquid is built around the business scene of a contract renewal rather than as one of many applications. This allows products to give priority to what is most important to active traders: fast-down orders, reliable deals, clear position displays, familiar exchange interfaces。

Market selection。& nbsp; Hyperliquid draws attention to the market of the online traders “most wanted to trade now”, especially long-tailed high-heat assets outside BTC and ETH。

Platform flexibility。 HIP-3 allows developers to directly deploy a new market for permanent contracts, transforming the currency-up model from a centralized gatekeeper to an open market creation system。

Distribution network。The & nbsp; Hyperliquid ' s builder code and front-end models give third parties a reason to import users into the same mobility pool rather than to spread them to isolated locations. The economic benefits are already considerable: through the integration of the builder code, Hyperliquid will continue the contract, Phantom has accumulated approximately US$ 17.7 million from road-trading fees。

Communities。The token allocation incentive for & nbsp; Hyperliquid is for platform users, not venture investors or pre-selected insiders. This created a different structure for early holders — traders, market participants and developers — who would have had reason to follow the project. This is important in a race track where trust is scarce。

None of these advantages can be decisive in isolation, but together they explain why Hyperliquid has become a few encryption applications that can be measured in terms of actual usage rather than vision。

Hyperliquid can consolidate barriers to competition through interaction between mobility, distribution and development incentives. The greater the volume of transactions, the better the liquidity and the quality of transactions, the greater the number of users and third-party front-ends. Builder code and HIP-3 give external developers an economic incentive to move back to the same mobility pool. This has created a potential network effect, which is difficult for new entrants to replicate: liquidity attracts distribution, which leads to more transactions, which in turn enhances the economic basis of the agreement。

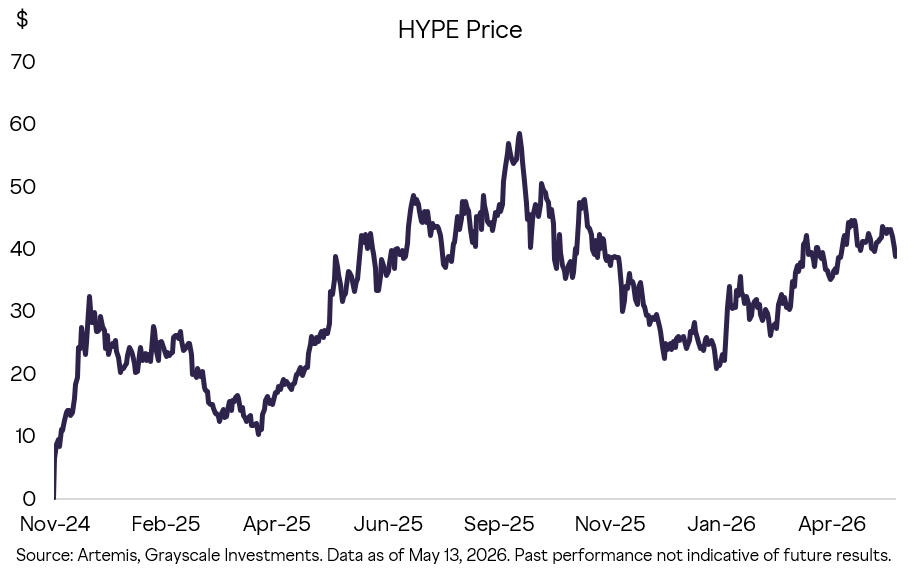

HYPE TOKEN

HYPE token drives the whole Hyperliquid ecology。

THE PROJECT HAD NO TRADITIONAL VENTURE CAPITAL, AND ABOUT 30 PER CENT OF THE COIN SUPPLY HAD BEEN DROPPED TO EARLY USERS. THIS DETERMINES WHO CARES: THE INITIAL GROUP OF HOLDERS IS HIGHLY BIASED TOWARDS USERS, TRADERS AND COMMUNITY MEMBERS WHO ALREADY UNDERSTAND THE PRODUCT。

Figure: Exhibit 11, HYPE price trends since coming online

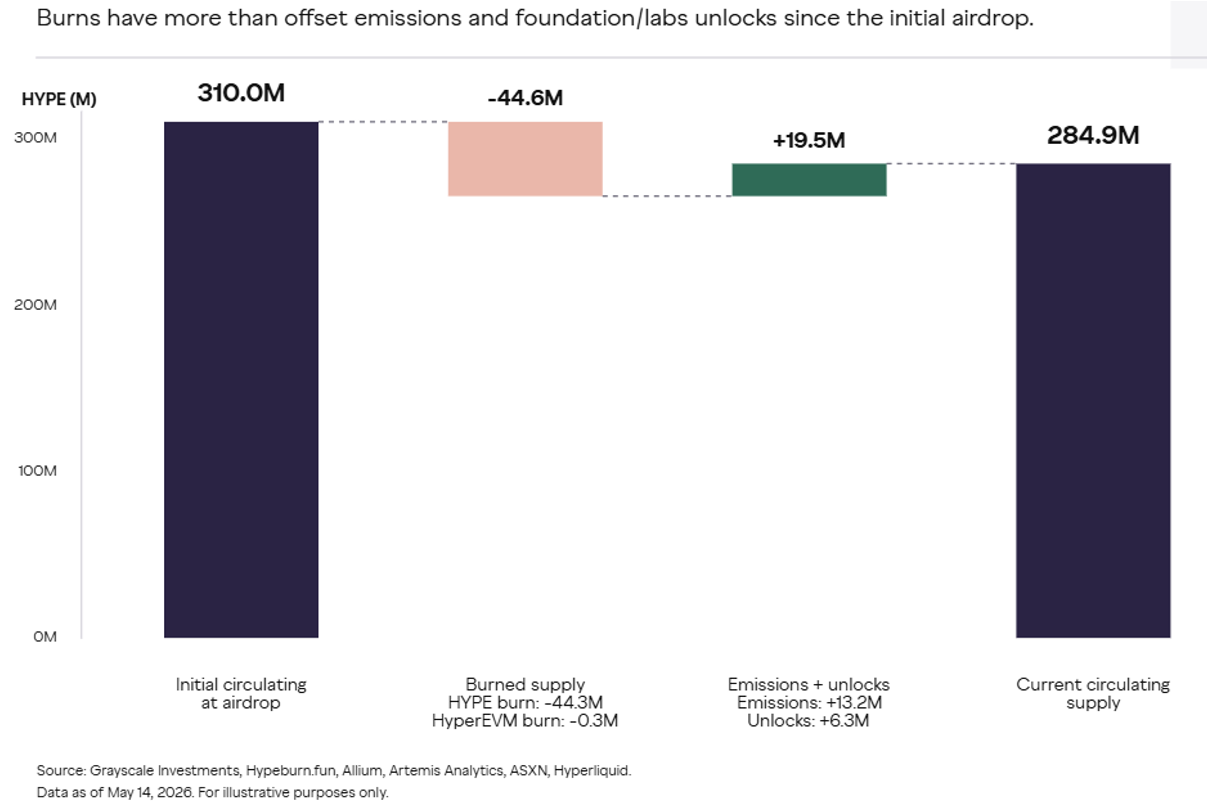

The value of HYPE is derived from transaction fees and functional uses. Hyperliquid Labs confirmed that 99 per cent of the fees were entered into the Assistance Fund (Asistance fund), which converted the fees to HYPE and destroyed the held HYPE. The destruction of tokens is similar to repurchases in traditional stock markets. The supply of hype in circulation has been declining as destruction exceeds additional distribution。

Figure: Destruction, emissions and supply changes in Exhibit 12, HYPE

THE ECOLOGICAL USES OF HYPE INCLUDE:

The pledge and the authenticator are involved in: hype secures the network by pledging to the certifier。

Gas Fees:& nbsp; is the original gas token for HyperEVM and the base and priority charges for HyperEVM are destroyed。

Fee discount:& nbsp; Pledge HYPE can reduce transaction costs。

Market creation collateral:The HIP-3 deployers must maintain 500,000 HYPE pledges to operate the permanent contract market for the deployment of the bilder, which is the security of both the capital and the quality of the market. The HIP-4 results are online and the role of the HYPE may be further deepened if similar models are not allowed to be deployed。

HYPE binds a site where transactional activities, handling fees and the needs of developers can be measured. The more transactions are processed at the site, the more important the schedule of rates, the level of pledge, the mechanism of the builter economy and the aid fund. The more HyperEVM, HIP-3 and HIP-4 expand the platform boundary, the greater the utility and potential value build-up of HYPE。

Valuation space

Hyperliquid is a unique platform providing a range of financial services, which makes it challenging to effectively assess its upper spaces. But, on the basis of reasonable and comparable criteria, Grayscale believes that both the platform and the token have substantial growth potential。

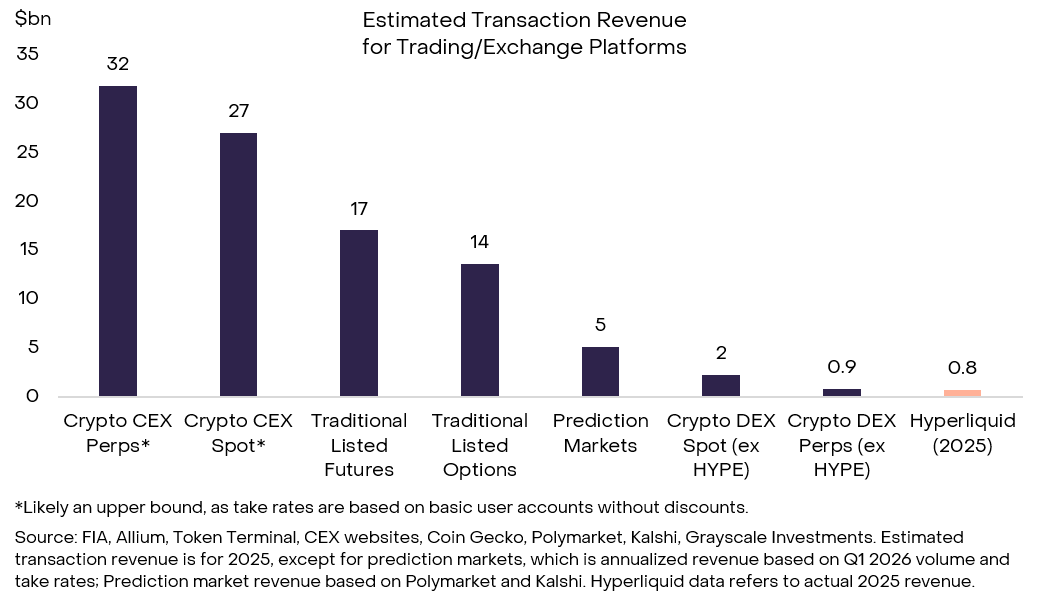

The figure below compares the income of Hyperliquid with a range of trading platforms, including the Centralized Encrypted Exchange, the Traditional Cash and Derivatives Exchange and the Forecast Market. Hyperliquid ' s revenue of about $800 billion in 2025 was considerable, but only about 2 per cent of the total transaction income from the encrypted contract for perpetuity. If Hyperliquid's non-encrypted products are used on a sustainable basis, it is likely to enter the wider derivatives exchange industry's revenue pool of approximately $35-40 billion per year。

Figure: Exhibit 13, Hyperliquid Revenue versus Exchange Industry

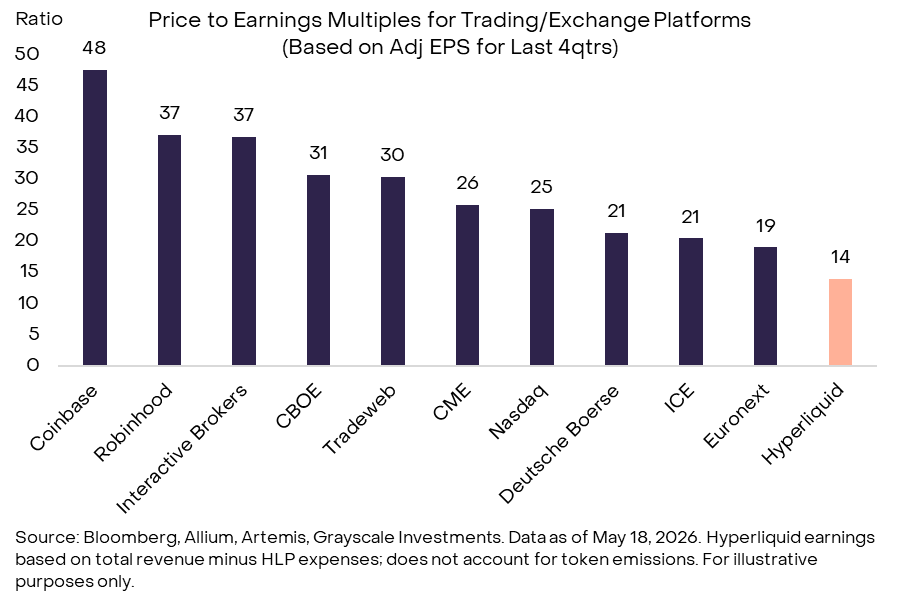

HYPE is not a stock, but can be roughly compared with traditional stocks in the relevant industries. Based on four quarterly gains up to Q1 in 2026, the current HYPE valuation is approximately 14 times greater. The valuation multipliers vary widely among exchange listed companies, but the multipliers for high-growth companies such as Interactive Brokers and Robinhood are 35-50 times。

Figure: Exhibit 14, Hyperliquid valuation multiples less than comparable equity companies

U.S. Surveillance: End-of-life contract coming in

Hyperliquid is at the intersection of two regulatory gaps in the United States: a lasting contract and a decentralised exchange. Both areas are now moving towards a clearer framework。

The contract is practically unavailable in the history of the United States. They are not explicitly prohibited, but cannot be covered in a clean manner by the Merchandise Transactions Act (CEA). CEA is a federal statute governing bulk commodities and derivatives, with clear requirements for liquidation, deposit and registered trading premises. This ambiguity has led to law enforcement against the hub and DeFi platforms, and explains why Hyperliquid operates overseas and has imposed a geographical blockade on United States users。

But the situation is changing rapidly. CFTC ' s recent statements, combined with the actions of Coinbase, Kraken, Robinhod and Kalshi, show that regulators are actively promoting the introduction of durable contract products within the compliance framework. The legal key is the question of classification: whether the contract is considered futures or swaps under the CEA? The choice of modalities by regulators to clarify this classification (rule-making, guidance or non-enforcement relief) will determine the timing and durability of market access。

In the short term, regulatory progress may give priority to centralized registered trading places. In the medium term, however, CFTC rule-making, guidance or non-enforcement relief may open the way for Hyperliquid to provide a compliant, durable contract product in the United States and reduce reliance on purely overseas access。

At the same time, the type of exchange function of Hyperliquid has involved it directly in the debate about how the DeFi agreement would regulate. The United States currently does not have a rulebook specifically designed for DEX. Regulators apply the existing SEC and CFTC frameworks on a functional basis, with the core principle being that "decentreization does not amount to immunity"。

In the case of DEX, which is centred on derivatives, this means more rigorous scrutiny and clear barriers to direct institutional involvement — currently mainly through intermediaries or offshore channels. Legislation in progress, such as the CLARITY Act, points to a more structured, role-based digital asset market framework, including a clearer distinction between agreement-level activities, front-end operators, intermediaries and registered trading places。

This distinction is essential for Hyperliquid: as a non-hosting infrastructure, its core agreement may eventually be treated differently from the interface or entity that facilitates user access. These proposals have yet to create a fully viable regime for a lasting contract in the chain, but they represent the path to this goal - In particular, it should be accompanied by targeted safe harbour provisions, clearer definitions of brokers, and tailor-made rules for chain market structures (e.g. bonds, financial rates and 24/7 transactions). Regulatory direction is to introduce innovation within the fence, while the positioning of Hyperliquid — open, globalized, non-honorable — is in line with policy discussions around keeping unlicensed access while introducing appropriate market protection。

Risk

HYPE investors should be mindful of conventional risks and risks specific to some Hyperliquid platforms:

HYPE has an annualized price volatility rate of about 80 per cent, which is about 40 percentage points higher than bitcoin. Hyperliquid certifiers are assembled more centrally than other block chain networks and operate on closed source software. The growth potential of Hyperliquid depends in part on changes in regulation of financial services in the United States, and if regulation is not loosed, the platform may be limited to other jurisdictions and growth has a ceiling。

Conclusions

Hyperliquid cannot find direct pairs in encryption and traditional finance. It provides a compelling vision for the future of block-chain finance: an open architecture platform, based on unlicensed innovation, adherence to DeFi principles of transparency and self-custody. At the same time, it is built around an optimized core application and has proved successful with actual user data. If it can sustain implementation, retain and grow communities, and benefit from regulatory change, Graysdale believes that Hyperliquid has the potential to become a financial services giant。