Is the "Golden Age" of the Global Central Bank over

The survey showed that 62 per cent of central banks were "buy and hold" and only 4.5 per cent had short-term tactical adjustments and that the official sector would not be like news-driven traders. 。

Original by Jo Wing

Original source:See you on Wall Street

The most popular market issue in the recent past is: is the global central bank selling gold? Is this 15-year-old official "golden hoarding" coming to an end

According to the Wind Track Trading Platform, Joni Teves, a Swiss silver strategist, made a clear judgement in a recent precious metals study released on April 2, that there is a structural shift in central banks and a very low probability of large-scale gold sales. Official institutions will maintain a net buy-in position, except that the pace of purchase will slow down mildly - the annual amount of money purchased is expected to be between 800 and 850 tons in 2026, slightly below the level of about 860 tons in 2025。

The report points to the most impressive sample in recent times — about 50 tons of gold sold in a few weeks in Turkey. Teves argued that Turkey’s official gold data mixed operational traces of commercial bank positions, swaps, etc., and that headlines alone infer that “the central bank starts selling” is a high risk, which should be judged by more disaggregated data。

At the price level, the Bank defines the short term as a "high noise": geo-situation information loops will keep gold prices shaking and rounding; but the medium-term logic will continue to point to new heights, and the average annual forecast of 2026 gold prices will be revised downwards to $5,000 (previously $5200, mainly a quarterly booking adjustment), maintaining the target price at year-end at $5,600 (set at the end of January)。

Consider "central bank money" as the main reason for this round of withdrawals, 800-850 tons more like "slow."

Market fears are specific: if the conflict in the Middle East is prolonged, oil prices push up inflation, growth weakens, and the currency depreciates, some central banks may be forced to sell gold to deal with pressure. The report does not deny that “individual central banks sell” may happen, but it emphasizes that this is not equivalent to a reversal of the official sector trend。

A key reminder given in the report is that it is not uncommon for a single month to be "sold" in the context of the continued increase in gold in the official sector over the past 15 years. The reasons may also be pragmatic – early-buying central banks do some tactical stopovers outside their core positions; high gold prices trigger rebalancing; and the “natural inflow” of gold-producing countries translates, at some point, into external deliveries. In other words, sales can be actions, not necessarily positions。

The baseline judgement is that net purchases remain, but at a slower pace. The details here are the official sector’s trading habits: they are more like “in-kind buyers” and often provide a bottom-up force when they retreat, allowing markets to stabilize faster and higher platforms; on the contrary, the official sector usually does not follow up and tends to intervene when prices are more appropriate and volatile。

This explains why the market suddenly feels "the central bank is missing" when volatility increases. The observation mentioned in the study is that the official sector and other long-term holders in the near future are more inclined to wait than to make up for each drop。

The Turkish narrative of selling "50 tons" has been amplified, and the price of gold is more driven by the United States dollar and real interest rates

Turkey’s case is sensitive because it seems to fit the narrative of “the central bank starts selling money.” But Turkey has some peculiarities: part of the change may be swapped rather than sold directly; and, more importantly, the Turkish Central Bank has long used gold as a policy tool to support liquidity management in the domestic banking system。

Part of the total gold disclosed by the Turkish Central Bank corresponds to the position of commercial banks. Adding more policies that allow banks and other entities to use gold in the financial system after 2017 does not mean that "total data changes" are tantamount to "central banks selling on the market". The report ' s recommendation was clear: trends would be discussed once more detailed data could be disaggregated。

In March, there was a "double uncertainty" in the trading environment: on the one hand, when Iran’s information fermented, the gold price was looking for a new stability after a sharp rise in January-February; and, on the other hand, the impact of the Middle East conflict on macro and asset pricing was non-linear, with long-term funding reluctant to bet。

In the short term, when strategic funds are not available for “fall-to-buy” purposes, it is easier for gold prices to return to the traditional framework: the dollar is strong, real US interest rates go up and the price is suppressed; many are further squeezed out, and even some empty power emerges. In addition, Chinese demand is supporting the downside at this stage, with a steady price of gold in the vicinity of $4,500 and a shock in the vicinity of $4,700。

The bottom logic of central bank holding money: no sale

The World Bank ' s Fifth Biannual Reserve Management Survey (2025) explains a much lower issue: what central banks think about gold. The survey covered the warehouse up to December 2024, with 136 institutions participating at the highest level, and for the first time separate gold chapters。

Several figures make clear the boundaries of central banks’ behaviour: about 47% of central banks decide to hold gold with a "historical legacy" of about 26% based on qualitative judgement; only about a quarter of gold is included in the formal strategic asset allocation framework。

More critically, only about 4.5 per cent will make short-term tactical adjustments to gold reserves, while gold investment styles are dominated by buying and holding (about 62 per cent). This image means that even if the pace of buying is slow, the official sector is not like a group of news-driven, frequent-turned traders。

More than half of the drivers listed "decentralization" as the most important cause; about 35 per cent of the local gold purchase plans and about 32 per cent of the geo-risk; and only about 6 per cent of the "mobility demand" as the cause. The official sector ' s justification for gold does not lapse due to recent fluctuations。

Short-term shocks are inevitable, but the New High is still the main line

Back to the level of trade, gold is not a straight-line path to increase: it may continue to be rolled up and spiralling in the coming weeks, as markets constantly re-evaluate geo-risks. However, it believes that the two lines that drive the financing of gold in the medium to long term — the combination of growth and inflation risks, the persistence of geo-stretching — are turning “difference to gold” into a more general combination。

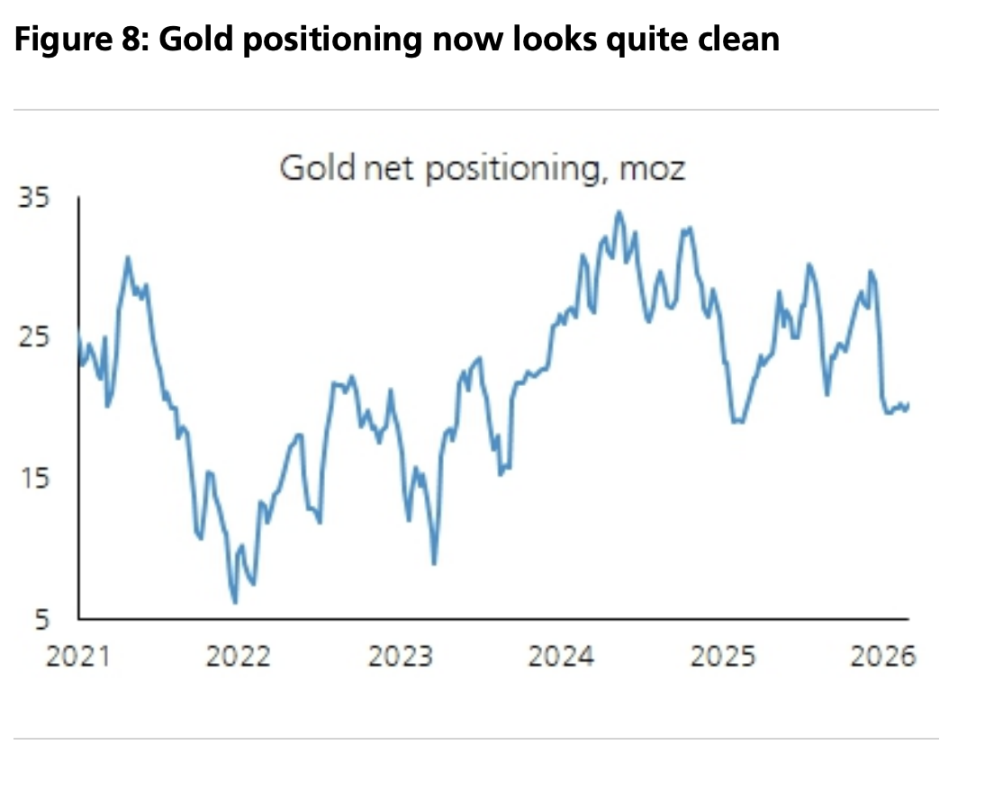

Within this framework, the price anchors given in the report are: an average annual gold price of $5,000 in 2026 and an end-of-year target of $5,600. At the same time, it was mentioned that speculation has become “cleaner” and that long-term participants are still under-represented; if retreats occur again, they are closer to a “strategic warehouse window” rather than a signal of the end of the trend。