The evolution of borrowing: Aave V4 and Morpho V2, who is DeFi's future

TL;DR

Background:Aave launched V4, Morpho advanced V2, and DeFi is entering a new architecture upgrade cycle。

EvolutionAve V2/V3 was born in the shared pool model, promoting multi-chain expansion and risk-segregation Morpho's “Treatment Revolution”

Three paradigms:MULTI-ASSET CAPITAL POOL, SEGREGATION OF THE MARKET + SCHEME RWA LENDING

Aave V4 VS Morpho V2:Aave, more like Big Bank on the Chain, Morpho, more like Asset Management Platform on the Chain

Risk:Vault/Curator Risk, Smart Contract and Operating Risk

Opportunities:THE LENDING MARKET BECAME A "COLLECTIBLE FINANCIAL BUILDING BLOCK" AND THE INSTITUTIONALIZATION BECAME A PRODUCT PATH. RWA BROADENING THE ASSET BOUNDARY WITH THE CREDIT SEGMENT

ConclusionsThe V4/V2 DeFi lending is moving towards a professional, modular, institutionally friendly financial operating system。

DeFi lending is entering a new architecture upgrade cycle. Both the two major DeFi lending agreements, Aave and Morpho, recently announced major upgrades: Aave V4 came online at the end of March and Morpho V2 officially landed in February. While the central-irradiated architecture of Aave V4 aims to achieve uniform mobility and depth in the RWA field, the sudden announcement today by Chaos Labs of withdrawal, previous departures of core contributors such as ACI, governance disputes and clearing irregularities has given rise to widespread questions; while the non-trustee Vaults V2 of Morpho V2 has significantly increased asset efficiency by 20-30 per cent through the Curator Scheme, the discussion of Curator ' s risk management and security contests has been equally intense. The simultaneous upgrading of the two agreements marked, on the one hand, the upgrading of the lending agreement from a “chain-based lending tool” to a more complex financial movement and credit stratification infrastructure. On the other hand, an alarm bell was sounded for ordinary encrypted investors: opportunities and risks coexisted, and upgrading was a profound test of capital efficiency, security and governance。

I. Understanding the DeFi Loan Agreement

1. Bottom logic of DeFi borrowing

DeFi's bottom logic of borrowing can be summed up in one sentence: to move traditional bank deposits to the chain and rewrite them in code。

In this system, the lender pays interest on the assets deposited in the agreement, while the borrower receives funds through the provision of excess collateral. The most significant difference with traditional finance is that the process is not based on manual auditing, credit evaluation or endorsement by a centralized institution, but is carried out entirely automatically by an intelligent contract. Financial flows, interest rate calculations and clearing mechanisms are all driven by pre-established rules and are highly transparent and verifiable。

This is why the threshold for DeFi lending has been significantly lowered - any wallet address holding an encrypted asset can participate without a permit。

2. Use of loan agreements

From an investor ' s point of view, the use of loan agreements is concentrated on two typical types of demand。

- The mortgage doesn't sell money: USERS CAN BORROW ASSETS SUCH AS BTC, ETH AS COLLATERAL TO OBTAIN LIQUIDITY WITHOUT ABANDONING POTENTIAL RISE SPACE, THUS AVOIDING ERROR DUE TO PREMATURE SALE。

- It's a chain: Users deposit idle assets into a loan agreement to secure a stable interest rate gain, which is seen as a “point deposit” or “base replacement” on the chain. This function has long served as the anchor of the underlying gains in the encrypted market where low-risk gain instruments are lacking。

- Finance market infrastructure: Almost all of the complex strategies are implemented on the basis of the mobility support they provide. For example, liquidators need immediate funds to participate in liquidation in order to obtain liquidation incentives; arbitragers need short-term liquidity to complete cross-market price differentials; and other agreements (e.g. derivatives, securitizers, income polymers) require a combination of collateral and loan interfaces to build their own product structure。

It can be seen that the lending agreement is not just a service end-user, but a “blood circulation” for the financial system as a whole。

3. Two core competencies: pricing and risk segregation

From the point of view of the design of the mechanism, the complexity of the lending agreement can ultimately be attributed to two core competencies。

- Pricing capacity: Includes interest rate models, mortgage setting, liquidation thresholds and incentives. Together, these parameters determine the supply-demand relationship between finance and capital efficiency and are a direct manifestation of the competitiveness of agreements。

- Risk segregation capability: In a multi-asset, multi-market environment, preventing single-asset fluctuations or risk events from spreading to the system as a whole is a key proposition for the long-term evolution of lending agreements. The silo design, risk layering and independent market structure are all built around this objective。

II. Evolution of loan agreements

The evolution of the loan agreement is not simply a new function, but a new balance between the core sets of contradictions: Between efficiency and security, between decentrization and specialization, between open access and controllable winds. In a sense, the development history of DeFi borrowing is the process of re-engineering the mechanism around this triangle and the history of the rise of Aave and Morpho。

1. Origin phase (2018-2020): emergence of the shared pool modelIn June 2018, Compund officially launched the cToken mechanism, which is seen as the real starting point for DeFi lending. Users deposit assets such as USDC, ETH in a shared large liquidity pool, with the system automatically adjusting interest rates to supply and demand; borrowers lend money by depositing 150-200 per cent of excess collateral. This is the classic “peer-to-pool” (point-to-pool) model: for the first time in the world, the viability of “unlicensed borrowing” on the block chain has been demonstrated by the combination of very high liquidity and the availability of anyone。

Aave ' s predecessor, ETHLend, tried to match a pure P2P point in 2017, but in 2019 little was asked about it because of its inefficiency and high mobility fragmentation. Aave V1 came online in January 2020, introduced a capital pool structure and brought Flash Loans (Molniya) into DeFi for the first time as a key innovation, laying the stage for subsequent hegemony。

2. Breakout and iterative phase (2020-2023): Aave V2/V3 promoting multi-chain expansion and risk stratificationAfter the “Summer of DeFi” in 2020, mobile fragmentation and multiple hacking events exposed the short panel of single-pool patterns. Aave V2 (opened in December 2020) has expanded the bulk lightning loan (Batch Flash Loans), debt tokenization, mortgage swaps and direct repayments with collateral, and reduced gas consumption by 15-20 per cent. These upgrades have led to significant improvements in V2 capital efficiency, user experience and developer-friendlyness。

Aave V3 (online in March 2022) brings with it three major killer-level innovations: sequestering markets (e-mode, where assets of the same type, such as ETH and steh, can be used as collateral against each other), cross-chain Portal (support for multi-chain mobility transfer) and more intelligent liquidation parameters (LTV, Liquidation. Aave's accumulated borrowing exceeded the $1 trillion mark at the end of 2023。

Optimization and modularization phase (2023 to date): Morpho “Treaturing the Revolution”In 2023, Morpho emerged as the “interest-rate optimization level” for Aave and Compund, and by prioritizing P2P borrowers, the remaining funds retreated back to the pool, often yielding 0.5-2 per cent higher returns. Morpho V1 makes the market a separate market “one collateral asset + one loaned asset”: market parameters are immutable, risks are segregated within a single market and creation is not permitted. The V2 introduced in 2026 completely “externalized” risk management and pricing: Curator (specialists such as Gauntlet, Steakhouse, Bitwise) sets parameters such as interest rates, duration, LTV, and the agreement provides only Timelock's delayed changes, flash loan foreclosures and the Setinel daemon to ensure complete non-custody. The objective of V2 is to allow “markets rather than agreements” to determine interest rates and to support fixed interest rates/fixed durations, smoother cross-chains and closer to structured contracts for traditional credit。

III. Three main paradigms for DeFi lending

The lending agreement mechanism can be divided into three dimensions: how assets are aggregated, how risks are segregated, and how interest rates are formed. Along these three dimensions, the current DeFi lending can be broadly summarized into three dominant paradigms。

Multi-asset pools: a “standard model” for liquidity priorities

The first is the classic and most familiar model for users - the Pooled Money Market, represented by Aave, Compund。

The core of this model is that funds are pooled by assets and that interest rates are automatically adjusted by algorithms according to supply and demand. Deposits from all users are pooled in the same pool from which borrowers borrow funds at interest rates that vary depending on the utilization factor. This design brings with it extremely high levels of liquidity and availability: immediate access, mature liquidation mechanisms and support for advanced functions such as lightning lending。

But the other side of efficiency is the “partial sharing” of risk. Although Aave V3 has applied a risk layer to different assets through isolation Mode and E-Mode, large fluctuations in a single asset may still have an impact on overall liquidity in extreme cases。

2. Separating markets + developing mechanisms: rebalancing efficiency and security

The second category is the fast-growing paradigm of isolation of markets + exhibition, represented by Morpho。

The central idea is to separate risks and then complement efficiency with structural design. In Morpho Markets, each market is usually a “single mortgage + single loan”, with fixed and independent parameters that naturally avoid risk transmission between different assets. This design is preferable to the traditional pool of funds in terms of safety。

The problem, however, is that complete isolation leads to fragmentation of mobility and a decline in user experience. To that end, Morpho introduced the Vault and Curator mechanisms: Curator was responsible for selecting the bottom markets and assigning parameters; Vault repackaged several isolated markets, presenting users with a one-key experience close to the “fund pool”; and dynamic staggering between different markets to increase revenue and utilization。

In terms of results, the model achieved a compromise: the rate of return was usually 0.5 per cent to 2 per cent higher than that of Aave; the risk was more nuanced; but at the same time, a new variable, Curator's managerial capacity and moral hazard, was introduced。

In other words, Morpho externalizes some of the risk management responsibilities originally assumed by agreement to “professional players”, which is essentially a step from “total decentrization” to “professional governance”。

RWA BORROWING: “NEW BORDER” CONNECTING TO THE REAL WORLD

The third category is currently the fastest-growing and most structurally significant direction - RWA (real world asset) lending. The key change in this model is that the source of collateral or cash flows is no longer limited to chain assets but rather comes from the real world, such as receivables, bonds, real estate or corporate financing needs. Typical projects include Maple, Goldfinch, Centrifuge, etc。

IN TERMS OF STRUCTURE, RWA LENDING FALLS BROADLY INTO TWO CATEGORIES:

- (a) Over-collateralization: the monetization of real assets as collateral (e.g. invoicing)

- Credit type/low collateral type: Dependency chain bottom-up, chain reputation or parts of KYC (e.g. Goldfinch ' s hierarchical pool structure)。

These kinds of agreements are closer to traditional finance in the wind logic:

- Gains are derived mainly from borrowing at fixed interest rates, usually at 4-8 per cent or higher

- Low relevance to encryption market volatility, with some degree of “cyclical resistance”

- But at the same time, there is greater reliance on the predictor, the legal structure and the compliance framework。

In terms of industry trends, RWA is becoming an important incremental source of lending paths: its TVL already accounts for more than 10 per cent of lending-type agreements, and Aave V4 has explicitly integrated RWA into the priority extension; Morpho is also working with Ondo, Apollo and others to introduce assets under the chain. It is foreseen that the development of RWA will drive DeFi lending from an “encrypted internal cycle” to a new phase of “chain-down integration”。

IV. AAVE V4 and Morpho V2: Two upgrading routes, two borrowing futures

If the main line of DeFi lending over the past few years has been to find a balance between efficiency, security and scalability, then Aave V4 and Morpho V2, representing two completely different answers. The former chose to “unique liquidity + modularization” and tried to turn itself into a hub for chain lending; the latter moved towards “non-hosting schemes + customized markets” and returned more pricing and risk management rights to market and professional managers。

1. Data performance on the chain

If the “lending track TVL” is used as the denominator, Aave is about half, Morpho is at the 10% + level; if the “global lending” is used as the denominator, Aave borrows more than 50%, indicating that it remains the backbone of the chain leverage and credit demand。

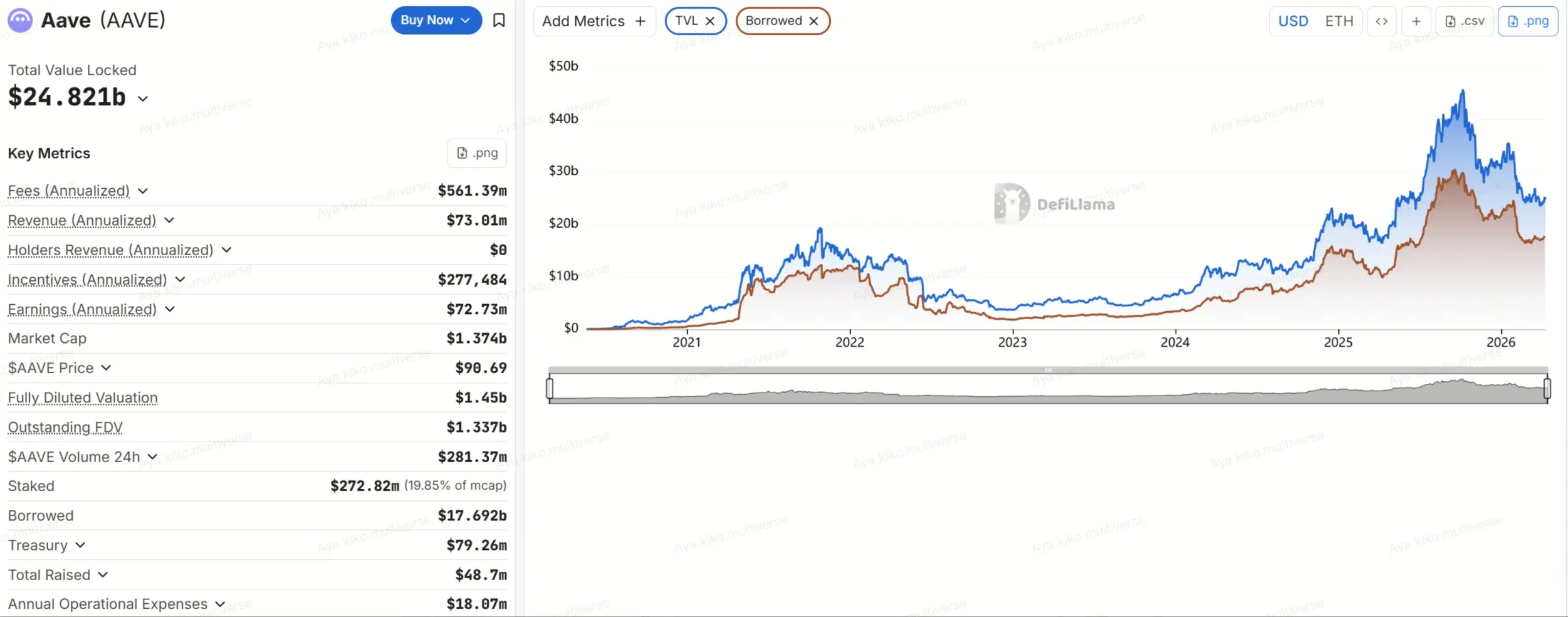

According to DefiLlama data, as at 9 April 2026, the DeFi Loan Track was approximately $51B, and the total Internet lending was about $34.4B. Aave's TVL is about $24.8B, loaned about $17.6B, of which the Taifeng represents about $20B, and the rest is distributed over multiple chains such as Plasma, Arbitrum, Base, Mantle, Avalanche。

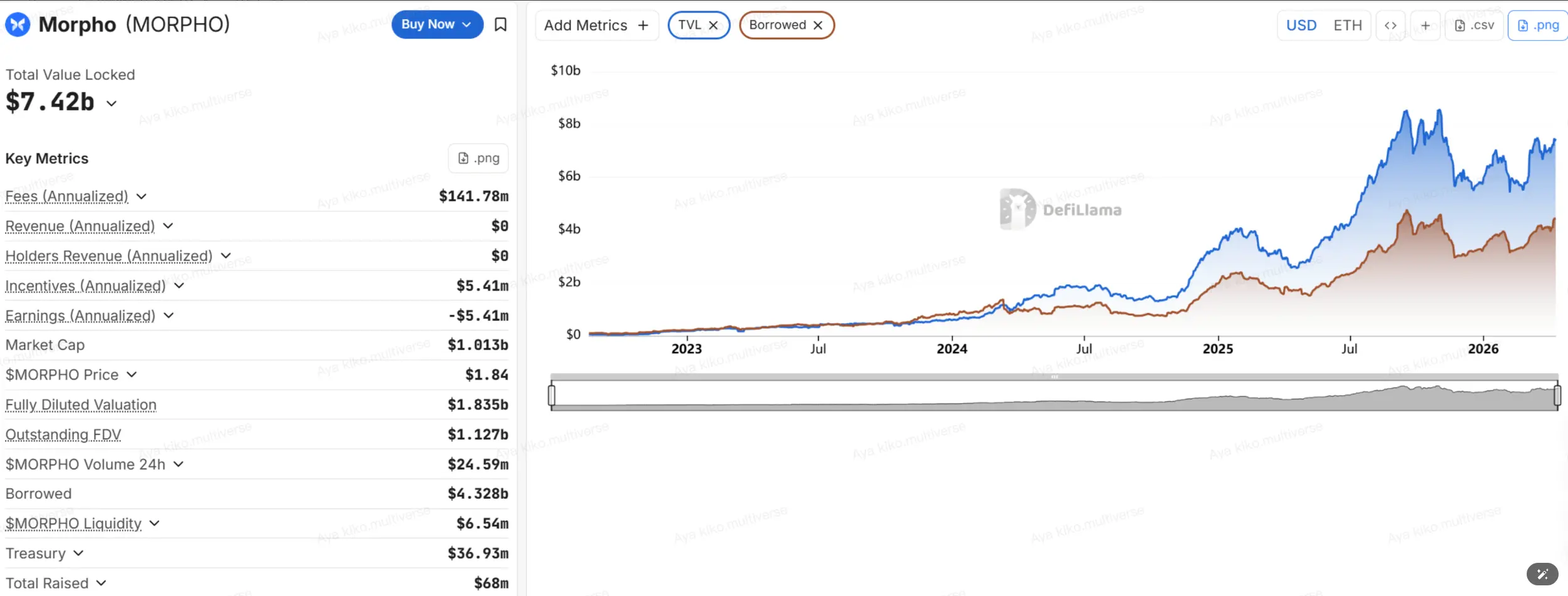

Source: https://defillama.com/protocol/aave Morpho about $7.4B, loaned about $4.3B, TVL is mainly distributed in the Ether Workshop (approximately $3.9B) and Base (approximately $2.3B), and also in Hyperliquid L1 and Arbitrum。

source: https://defillama.com/protocol/morpho

2. Aave V4: Reshaping liquidity with Hub-and-Spoke

The core change of Aave V4 is an attempt to address a long-standing problem of the V3 era: multi-market, multi-chain expansion-induced fluid fragmentation. Under the V3 model, users deposit their assets in a particular market in a chain, where liquidity essentially serves only that market, and when new markets start, they often have to redirect funds and be inefficient. Aave V4's programme is “Liquidity Hub + Spokes”: each network has a unified liquidity centre, with users entering the protocol through different Spokes, and Hub is responsible for the harmonization of account keeping, line control and core wind controls, thereby placing different strategies and asset types in different risk compartments while sharing liquidity。

The key points of Aave V4 can be summarized as three:

- Harmonization of liquidityReduced fragmentation of funds between different markets in the same chain and increased overall utilization。

- Modularized risk segregationSpoke can configure different parameters to avoid "all assets share a risk pot"。

- SAVE SPACE FOR INSTITUTIONS AND RWARWA Spoke can introduce stricter rules of access, trusteeship and foreclosure to prepare infrastructure for the chaining of real assets。

Aave V4's problem comes precisely from its ambitions. A stronger structure means that governance, wind control and operational complexity rise simultaneously. The initial V4 configuration will consist of 3 Hub and 10 Spokes, and V4 and V3 are expected to run in parallel for 24 to 36 months。

And it's at this stage that Aave's governance dispute has erupted. The core contributors, such as BGD, ACI, Chaos Labs, announced successive departures or terminations of cooperation, in which Chaos Labs publicly stated that the more fundamental difference between the parties was “how risks should be managed”。

Morpho V2: Capability of “assets management” as agreement

In contrast, Morpho V2 upgrade logic is more restrained and "modularized". It is not a whole reorganization, but a step-by-step roll-out of Vaults V2 and subsequent Markets V2. The authorities have made it clear that Vaults V2 will go online first and will initially continue to allocate funds to the old Morpho market, once Markets V2 has landed completely, before providing initial depth liquidity for fixed interest rates and fixed-term markets。

The focus of Morpho V2 is not on making a larger pool, but on transforming “assets management” itself into a protocol-level capacity. Key changes include:

- The roles are more detailed: Owner, Curator, Allocator, Sentinel, in their respective roles, facilitate segregation of duties and institutional compliance。

- Curator became a central player: Responsible for the allocation of risk parameters, the setting of liquidity distribution boundaries and the appointment of Allocator for implementation。

- Non-custodial security enhancements: To minimize the worst-case scenarios through timelock, in-kind response driven by lightning, and sentinel emergency interventions。

One of the most important of these is that the Morpho protocol no longer provides “uniform wind judgement” for all users, but allows users to choose Curator themselves. In essence, users are not choosing a single market, but a “fund manager on the chain”. It's the biggest difference between Morpho and Aave。

The attraction of Morpho V2 is clear:

- Users can use the Vault one key and put in a professional strategy

- Policy parameters are transparent and auditable

- The rate of return is often higher than the traditional shared pool model

- The non-custodial exit mechanism is stronger and theoretically “ready to go”。

However, its cost is clear: the agreement risk was partially replaced by the administrator risk. This means that local risk events may still occur if the risk preferences of Curator are too high, capacity is inadequate, or the lines of defence are weak。

It is a matter of concern that lending agreements are being redefined by the “institutional portal”. There have been several agency-oriented cooperation and access since Morpho 2026: the cooperation agreement with Apollo Global Management allows it to access the MORPHO chain lending market under certain ceilings and restrictions; and the trustees/servers, such as Angelage Digital and Taurus, provide access to Morpho Vaults in compliance. Bitwise also enters Morpho ecology as a Curator, further reinforcing the narrative “Vault = product shell available to the institution”。

Two routes, essentially a trade-off

After all, Aave V4 and Morpho V2 are not the replacements, but represent the future of DeFi's borrowing:

- Aave V4 Select "Uniform + Extension": THE GOAL IS TO MAKE THE MAXIMUM MOBILITY NETWORK AND TO TAKE OVER FROM AGENCIES AND RWA

- Morpho V2 Select Module + Custom: The goal is to give more pricing and asset management rights to the market。

For ordinary investors, the more realistic way to understand is not “who is more advanced” but “who is better suited to your financial use”: bottom well, low volatility, value the size of the agreement, better for Aave; and more for Morpho, willing to study Curator, pursuing higher returns and more sophisticated strategies。

Risks, opportunities and the future

If, in the past, the market's understanding of borrowing agreements has remained at the level of “earth money for interest” or “mortgage for money”, then what really needs to be rediscovered after the Aave V4 and Morpho V2 era is the risk structure itself. At the same time, lending agreements are opening clear new opportunities: product modularization, institutionalized access, and credit expansion driven by RWA。

1. Risks and problems

1) Predicator and parameter allocation risk:Aave ' s case of wstETH in March 2026 has shown that even if the agreement itself did not have bad debts, it could trigger large-scale liquidations as long as there were minor deviations from the predictor or exchange rate parameters. More importantly, the proceeds of liquidation are often first taken by external liquidators, and the subsequent compensation, and how, ultimately, will depend on the governance will and the efficiency of implementation by DAO. For users, this means that “agreements are not bad” does not mean “user does not lose”。

2) Governance and organizational risk:In the past, many investors have defaulted on the maturity of head agreements and the stability of the team, but Aave's recent departure of many core service providers has exposed the other side: As agreements grow larger, risk management ceases to be a technical issue and becomes a matter of budget, voting rights, accountability mechanisms and organizational structure. For ordinary users, this risk ultimately manifests itself in three things: whether parameters are still being maintained at a high quality, whether rapid synergies can be achieved in times of crisis, and whether budgetary resources are buying security or growth。

3) Vault/Curator Risk:This is particularly important in the Morpho system. Vaults V2 has moved the traditional management industry's “authorization segregation, time-delayed operation, investor protection” to the chain through such mechanisms as Owner, Curator, Allocator, Sentinel, Timelock, Veto. But the existence of a mechanism does not mean that the risk disappears. What it really requires is that users be willing and able to examine the governance structure behind Vault — who is Owner, who is signing more, how long is it? If this is not possible, “non-hosting” does not mean “risk-free”, but simply shifts risk from the level of agreement to that of administrator。

4) Smart contracts and running risks:These include code loopholes, logical flaws, border triggers, cross-contract interaction anomalies, and congestion and delays at the enforcement level on the bottom chain of extremes. Agreements such as Morpho have indeed adopted multilayered security practices such as formalization certification, fuzzing, code auditing and leakage rewards, but no team can prove that “risks are completely eliminated”. In chain finance, it is even more true that risks can only be dispersed, eased, delayed, but difficult to completely eliminate。

2. Opportunities and space

What increases with risk is the new space that lending agreements are opening up。

1) The lending market is moving from a “uniform product” to a “collectible financial building block”I don't know. The Hub-and-Spoke structure of Aave V4 essentially uses liquidity as a public base, allowing markets with different assets, different risk classes and different business objectives to share the same liquidity framework; while Morpho V2 brings the chain closer to the product form of the traditional credit market by giving further pricing power to the market and Curator and introducing fixed term, fixed interest rates, etc. Future lending agreements may no longer be a single product but a set of bottom-up financial engines。

2) Institutionalization is no longer mere narrative but is becoming a clear product pathI don't know. The cooperation of institutions such as Apollo, or the entry of Bitwise, Steakhouse, Gauntlet as a Curator, suggests that chain lending is gradually embedded in a more familiar institutional workflow and compliance framework. In the past, DeFi was more like a market between encrypted original users, and now it is trying to take on larger, more professional, more demanding processes and privileges。

3) RWA IS WIDENING THE ASSET BOUNDARY OF THE LENDING AGREEMENT WITH THE CREDIT HIERARCHYI don't know. Although RWA Lending's TVL is still significantly smaller than traditional encrypted mortgage lending in its current calibre, it means much more than size itself. What is really important is that a product paradigm closer to a realistic credit structure has begun to emerge on the chain: a layered pool, trust management, down-chain cash flow, down-chain recovery mechanisms. The target of the loan agreement services will also gradually be extended from “purely encrypted collateral assets” to broader rights to proceeds and cash-flow assets。

Concluding remarks

The V4/V2 DeFi lending is no longer a simple “chain depositor”, but is becoming a central engine for the migration of traditional financial infrastructure to the chain. It marks the transition of the encrypted world from a “rubbery high-yield experiment” to a “specialized, modular, institutionally friendly financial operating system”。

Aave and Morpho's two upgrade paths together answered the same macroproblem: Should chain lending be more like a superbank or an open asset management platform? The answer is perhaps integration — RWA will inject real world credit, cross-chain unification will break the mobility island, and institutional-level non-host mechanisms will lower the entry threshold. This evolution ultimately points to a broader future: DeFi is no longer the exclusive playground for encrypted First Nations, but rather the structural restructuring of global capital to achieve “unlicensed and efficient” financial services。