How can the benchmark interest rate of Cripto be achieved

This is not the case, but it is not the case, because it is not the case. Possible combinations in the future may be in the direction of: the monetization of the national debt as the bottom of the no-risk leg + the maturation of the CME base / Bitfinex term structure / the time curve of exchange of interest rates on the chain — or, alternatively, a governance neutral polymer index。

Original by: @BlazingKevin , Blockbooster Fellow

1. Cripto has no "base rate"

Crypto's leverage and financing in the world — trillions of dollars in leverage positions, mortgages, revenue products — is built on a curve of interest rates that is not uniform。

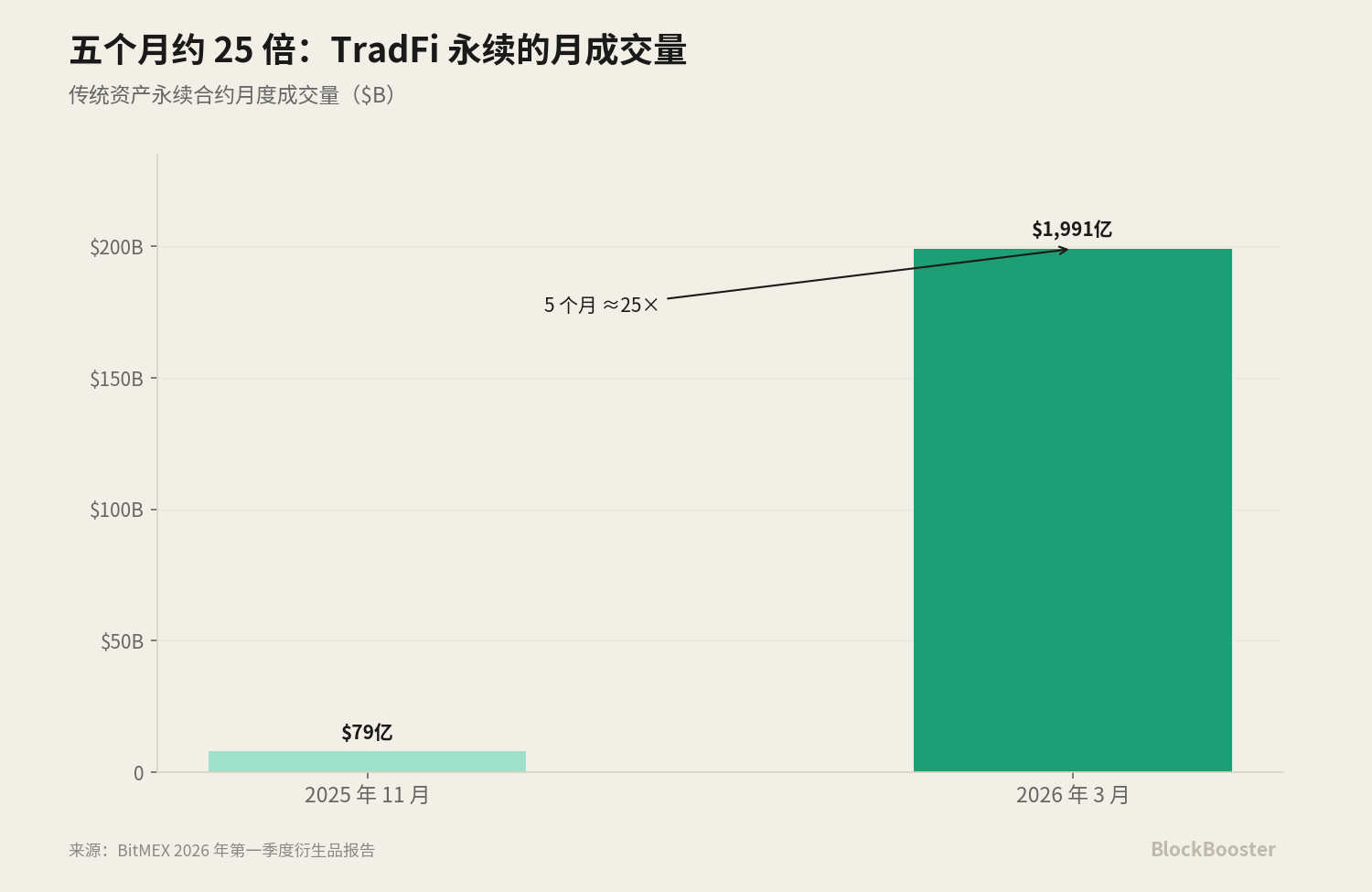

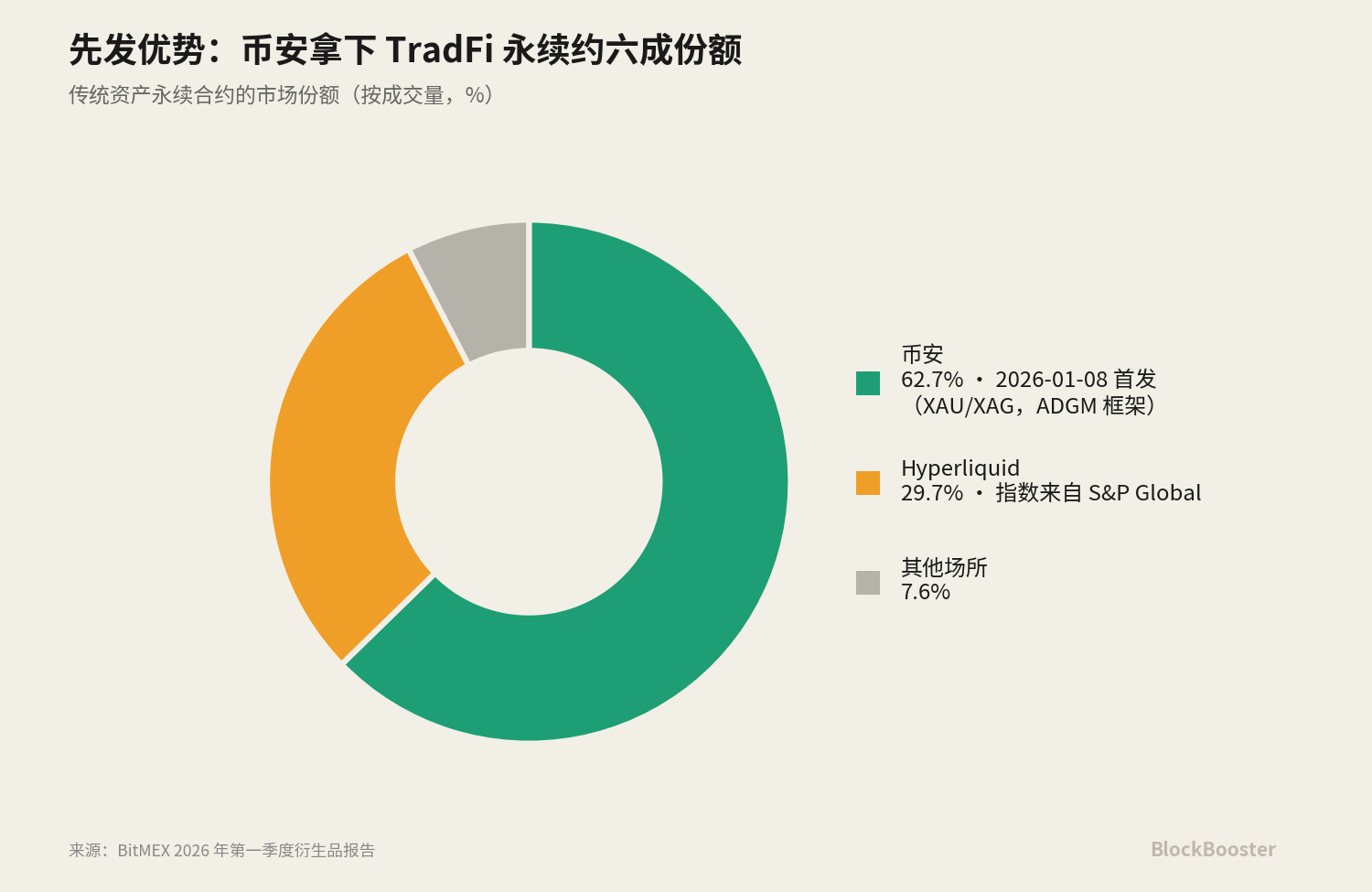

According to the BitMEX derivatives report for the first quarter of 2026, "traditional assets last" alone, the single-season trade has jumped from approximately $525.8 million at the end of 2025 to $30.7 billion in mid-March 2026, with a quarterly increase of about 5,556 per cent; its monthly trade has jumped from $7.9 billion in November 2025 to $199.1 billion in March 2026, a 25-fold increase in five months。

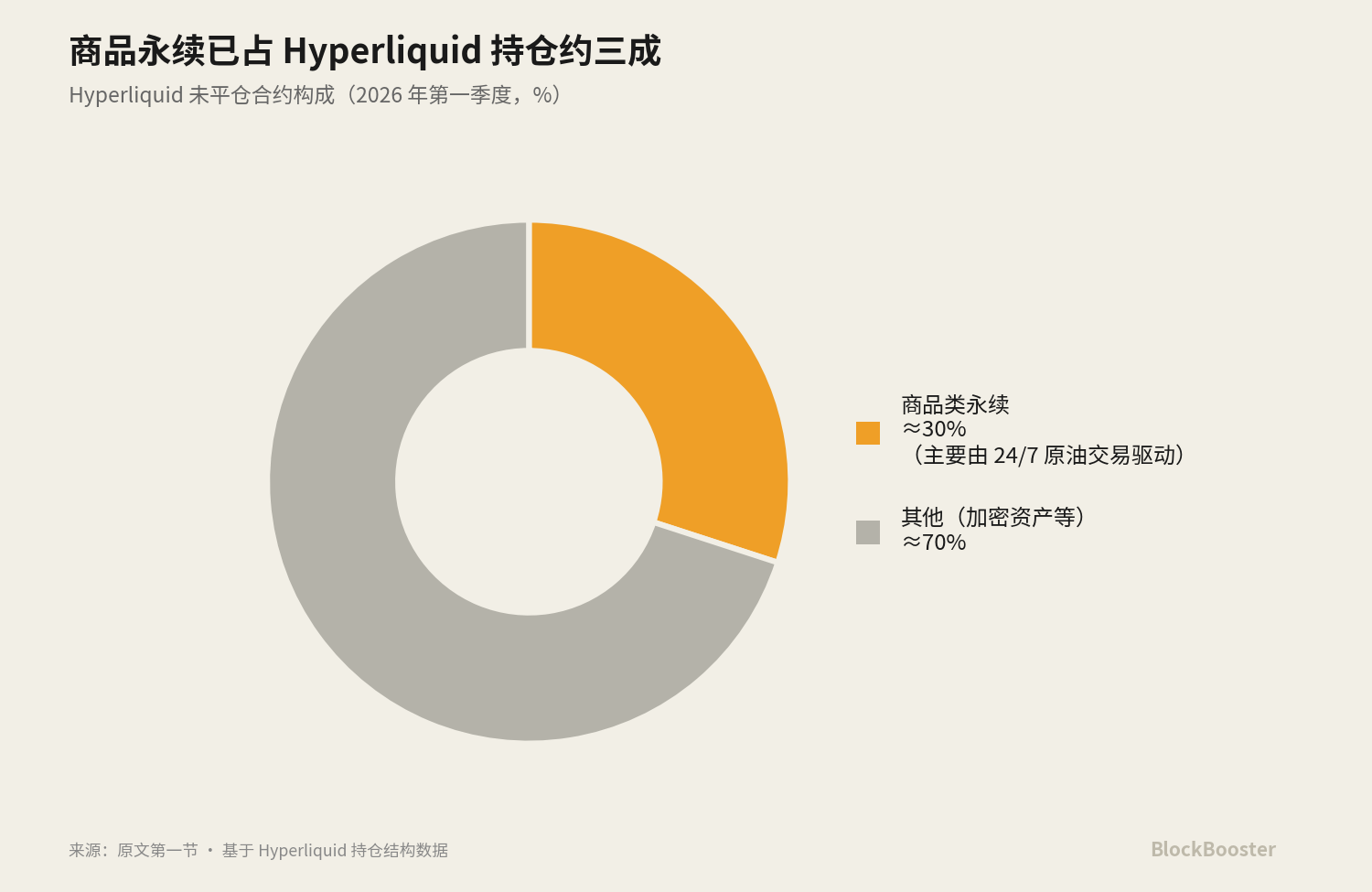

Hyperliquid processed approximately $172.63 billion in resuscitations and unsettled contracts of approximately $9.13 billion by DefiLlama's 30-day snapshot. In the first quarter of 2026, commodities have continued to account for about 30 per cent of the unsettled contracts of Hyperliquid, driven mainly by demand from the 24/7 crude oil trade。

The line of "traditional assets lasts forever." On January 8th, 2026, the coin went online and the TradFi contract was renewed, starting with the gold (XAUSDT) and the silver (XAGUSDT). With this wave, François took 62.7 per cent of the market share of TradFi, and Hyperliquid followed by 29.7 per cent。

Hyperliquid Index data for the sustainability of these traditional assets are derived from collaboration with S& P Global, which is leading to a regulatory review by the United States CFTC (Crypto is linked directly to the traditional index)。

At the same time, the market value of Ethena's USDe was about $4.5 billion to $5.9 billion in early June 2026。

These products are each reporting an interest rate or rate of return... - There's a permanent fund rate, a loan agreement with APR, sUSDE, a pledge rate of return and a coupon on the dollar-based national debt - but Crypto has so farWITHOUT HIS OWN SOFRI don't know. There is no single benchmark curve that is widely accepted and can be used as an anchor for pricing. Each exchange, and each agreement, is turning into a micro-financing market, offering its own prices without a public and credible reference between them。

What's the Crypto base rate

Look at three different sets of interest rates:

- Group I: base financing rate vs product yield vs derivative implied interest rate. **SUSDE's ASY is a product yield - a return to the holder; the Eternal Finance Rate is an implicit derivative interest rate - It is the cost to each other of multiple empty parties in order to maintain the constant price anchoring;** The benchmark financing rate should be a public reference that can be quoted and priced by numerous other products. ** Neither product yield nor derivative implied interest rates are benchmarks -They're base "downstream."This is the result of the accumulation of premiums and structures over the benchmark。

- Group II: Inter-night interest rate vs term interest rate. ** Establishing fund rate at 1 or 8 hours, which is essentially an overnight rate - It reflects only the cost of funds at this time to the next settlement point, without a time structure. It can't tell you the difference between the 30-day loan and the 90-day loan. It's just like SOFR itself is an overnight interest rate, and it's up to the futures market to spell out a term structure, Term SOFR。An interest rate with no term structure cannot support any fixed-income market in the medium to long term。

- group iii: real lending interest rate vs algorithms/implicit interest rate。Real bilateral lending deals (e.g. the Bitfinex bond financing drive, which is the real lender and lender-broker synthesis) and algorithm utilization pricing (e.g. Aave, where interest rates are calculated automatically through formulae for the utilization of the pool) are two fundamentally different price generation mechanisms. The former was voted by market participants with real money and silver, while the latter was a curve written by protocol designers in codes。

From these three groups, it is possible to distil the criteria that should be met by "a qualified benchmark":

Based on the real dealI don't knowThe bottom market is wide and deep enough(hard to be manipulated by a single participant)Governance independence(There is no conflict of interest between the manager and the priced market)Better have a time structure(Can support medium- and long-term pricing)。

THE BOTTOM OF SOFR IS THAT THE OVERNIGHT BUYBACK OF THE UNITED STATES BONDS IS A REAL DEAL, WITH A DAILY TURNOVER OF "MORE THAN $1 TRILLION A DAY." THIS IS..A real deal to buy back overnight. and the nominal amount that supports Term SOFRIt's completely different

Crypto is structurally homogenous using SOFR logic. In its research, the Bank for International Settlements (BIS) compared the chain mortgage-lending market to the "encrypted original money market", operating in a mechanism similar to the traditional tripartite buy-back — over-collateralization, liquidation at market value, rolling overnight. Since chain lending is structurally a buy-back type of secured financing, the Crypto benchmark is an appropriate synonym to be judged by the design of SOFR (a benchmark based on real buy-back deals)。

3. WHAT ARE THE CHARACTERISTICS OF SOFR? WHY IS LIBOR DISABLED

LIBOR (LONDON INTERBANK INTERBANK LENDING RATE) WAS THE CORNERSTONE OF GLOBAL FINANCE. AT ITS PEAK, ABOUT $30 TRILLION IN FINANCIAL CONTRACTS (INCLUDING INTEREST RATE SWAPS, MORTGAGES, STUDENT LOANS, CORPORATE DEBT, ETC.) DEPENDED ON LIBOR IN FIVE CURRENCY ZONES. BUT LIBOR HAS A FATAL DESIGN FLAW:It is not based on real transactions, but is estimated to be a daily "self-reported" borrowing cost for a few quote lines。

THIS FLAW WAS COMPLETELY DETONATED AFTER THE 2008 FINANCIAL CRISIS. REGULATORY INVESTIGATIONS HAVE FOUND THAT SEVERAL LARGE GLOBAL BANKS HAVE SYSTEMATICALLY MANIPULATED THE LIBOR OFFER FOR THEIR DERIVATIVE POSITIONS。

THE MANIPULATION SCANDAL LED DIRECTLY TO THE ABOLITION OF LIBOR。

INSTEAD, IT IS SOFR. SOFR IS DESIGNED FOR ALMOST EVERY FLAW OF LIBOR'S "REVERSE ENGINEERING": IT'S NOT SELF-REPORTED, BUT BASED ONThe real deal in the overnight buyback of the dollar mortgage; IT HAS THREE BUY-BACK MARKETS (TRIPARTITE BUY-BACKS, GCF BUY-BACKS AND BILATERAL BUY-BACKS THROUGH THE LIQUIDATION OF FICC'S DVD SERVICES)Medium barterTHERE IS NO CONFLICT OF INTEREST BETWEEN THE MANAGER AND THE PRICED MARKET。

BUT SOFR HAS A "INNATE DEFICIT": IT'S OVERNIGHT INTEREST RATES, NO TERM STRUCTURE. THE MARKET NEEDS NOT ONLY "THE OVERNIGHT COST OF TODAY" BUT ALSO "THE EXPECTED COST OF FUNDS FOR THE NEXT THREE MONTHS" TO PRICE MEDIUM- AND LONG-TERM LOANS. SO CME CAME OUTCME Term SOFR- a forward-looking set of interest rates covering 1 month, 3 months, 6 months, 12 months, 4 tenor。

It uses SOFR futures transactional data to reverse the market's expectations of future SOFR paths, thus creating a forward-looking time curve. (SOFR futures for the construction of Term SOFR, representing approximately $2.3 trillion per day in the fourth quarter of 2023)

4. Selected candidate interest rates that could be discussed

There are many candidates for "interest rate" or "revenue" on the market, and the following one-by-one break can be discussed as to why some interest rates are clearly inappropriate as base rates and what can evolve。

And one of the axes running through all the disassembly -"Who has the right to decide.": Market weighting, algorithm utilization, or governance setting

4.1 Sustained fund rate (Hyperliquid / currency)

The sustainability rate is..Implicit price of leverage, driven by the difference between the spot and the perpetuity: It's an overnight interest rateNo duration structureI don't know。

When the spot market for TradFi is closed (e.g. stock on weekends, precious metals), the exchange cannot obtain a real spot price to calculate the financial rate. Currency is used to freeze index prices at the final spot price, instead of the EWMA mark price with a > 3 per cent cap; Hyperliquid is also converted to EWMA on weekends, with a cap on volatility by variety. In the closing period, the anchor of the price for eternity is actually oneProjectednot the real deal. when the market is reopened and real prices jump above this limit, a limit-up/limit-down appears. therefore, the price for closed-market periods is forecast, not a real anchor for arbitrage。

On May 29, 2026, the United States CFTC approved the Bitcoin Renewal Contract for Kalshiex, the first in the United StatesReally not dueThe regulation of bitcoin lasts forever, along with a policy statement on durability of contracts, a staff directive on 24/7 settlement of transactions, and a no-action position on Coinbase providing durability through Deribit. The point of this is:Regulated, liquidated by a central counterpartyThe sustainability means that its financial rates and base differences are generated in a context of compliance and security of settlement — this is a possible candidate for future encryption SOFR. Together with the aforementioned Hyperliquid-S& the P Global Index was reviewed by CFTC, constituting a signal that "supervising is approaching encrypted benchmarks"。

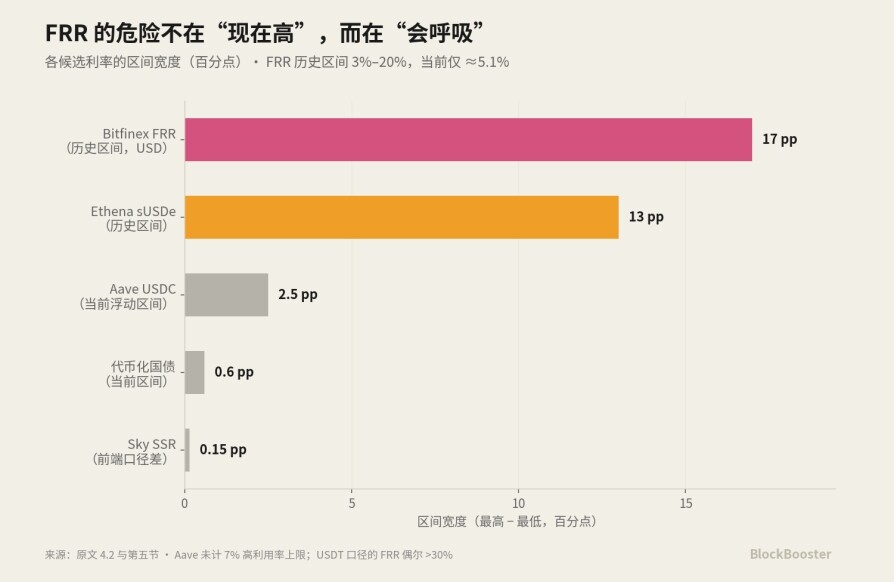

4.2 Bitfinex Bond Finance + FRR

This is Crypto'sOriginal dollar term finance marketI don't know。

The mechanism is as follows: Bitfinex operates a one-to-one bond financing market and the lender lends the money to the deposit dealer for interest. The key design is..The duration of the financing is 2 to 120 days (2 days, 7 days, 30 days), and the interest rate and duration must be matched。This means that Bitfinex's fundraisers are naturally made up of a short to long endReal loan curve: 30 days of money and 120 days of money at different prices, combined by real supply and demand. This is the very few real lending markets in the encrypted world with natural maturity structures。

And..FRR (Flash Return Late, lightning rate of return)THE REFERENCE RATE FOR THIS MARKET: FRR YESAll active fixed-interest financing is updated hourly at an average rate weighted by its sizeI don't know. In essence, it is the "Bitfinex version reference rate" - an index reflecting the average borrowing cost of the current market. The lender can directly choose to lend with FRR so that its interest rate automatically follows the market。

Bitfinex charges about 15 per cent of the loan proceeds (18 per cent); the minimum bill is $150. FRR byDaily interest rateQuoting, annualization at daily interest rates: FRR of Bitfinex USD, approximately 0.0136 per cent/day, annualization, approximately 5.1 per cent - substantially the same as the candidates for the national debt, Aave, SSR, etc。

It's his faultVolatility: USD BORROWING HAS EXPERIENCED SHARP FLUCTUATIONS BETWEEN ABOUT 3% AND 20% OF APRS, AND IS ASSOCIATED WITH A STRONG DEMAND FOR LEVERAGE。

This daily interest rate curve extends over different durations of 2 to 120 days and constitutes the original dollar finance curve in Crypto with a real term structure。

Bitfinex and Tether are parent companies iFinex and overlap management。This gives Bitfinex the best USDT liquidity in the whole encrypted world -- That's one of the reasons why its financing market is so deep; but at the same time, it alsoThe counterparty risk is concentrated in the same compound as the stable issuer riskI don't know. Borrowing Bitfinex's money, combining it with Bitfinex's set-up, denominated in Tether's price, under extreme circumstances by the same parent company - a highly self-contained structure。

While the Bitfinex finance market is the oldest and deepest source-dollar-term finance market in Crypto, its absolute size (stock of the finance pools versus the Japanese mix) is still much smaller than the trillions of dollars in exchanges in the previous lasting market。

By comparing FRR to LIBOR and SOFR, the dimension of "whether or not it's based on a real deal," FRR is actually cleaner than LIBOR, and FRR is weighted by scale based on real, settled interest-rate financing, which reflects real market behaviour. However, the FRR comes from a single exchange (concentration), operated by the same parent company, iFinex, which also controls the largest stable currency, Tether (conflict of interest), and the operator is the last lender (further concentration and conflict) of this market (with an established position). So FRR stepped on the two dimensions of concentration and conflict of interest, something that SOFR was about to eliminate。

4.3 DeFi Lending Rate (Aave / Morpho)

This is..Algorithm utilization pricingRepresentative: The interest rate is not determined by a bilateral arrangement, but by the utilization factor of the pool automatically calculated through a preset formula — the higher the utilization rate, the higher the interest rate. It floats in real time with borrowing needs。

The USDC deposit rate for the Aave main network fluctuates between 3.5 and 6 per cent with the utilization rate; the USDC vault on Morpho, managed by the curator, is about 5 to 7 per cent after deducting the cost of the exhibition。

4.4 MakerDAO / Sky Savings Interest Rate (DSR/USDS)

It's an agreementGovernance direct settingsThe "class policy rate". DSR (Dai Savings Rate) and USDS (Sky Savings Rate) of DAI are widely quoted as functionally similar to the policy rate set by a central bank - It was not triggered by market-based or algorithmic utilization, but by Sky's governance vote。

The governance setting of DSR/SSR, the market weighting of FRR, and the algorithm utilization of Aave constitute a comparison of three distinct interest rate generation mechanisms。

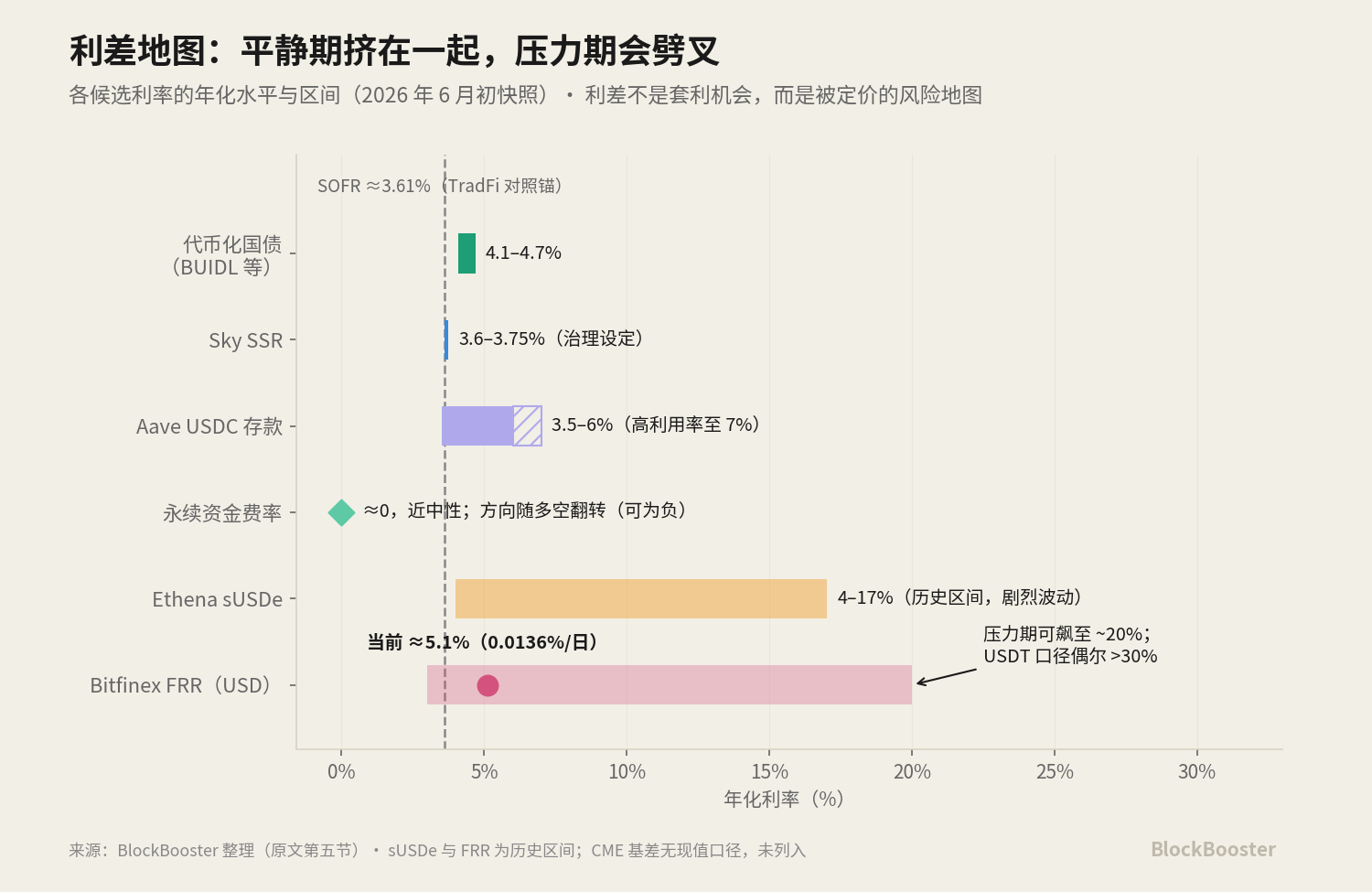

Governance sets vs market weighting vs algorithm utilization - each of these three mechanisms has different credibility problems and risks of manipulation, and a benchmark for a mature market should come from the one that is most difficult to manipulate (market weighting is a real deal and sufficiently broad). At the current level, the SSR was reduced from 4.75 per cent in governance at the end of April 2026 to about 3.6 per cent to 3.75 per cent at the beginning of June (the governance set mechanism moves along the Fed's path); USDS flows were about $11 billion。

4.5 GAINS ON NATIONAL DEBTS BY CURRENCYIZATION (BUIDL/BENJI ET AL.)

It's about 4-5% of a "risk-free leg" and it's a qualified candidate for "encrypted no-risk benchmark." BlackRock's BUIDL, Franklin Templeton's BENJI, etc., chained the interest-rate gains on the dollar debt. In current values, the main national debt-dimension coins (BUIDL, USDY, USDM, USYC, etc.) paid about 4.1 per cent to 4.7 per cent of ASY in April 2026, with a three-month rate of return on US debt. Its yield is almost direct to the traditional risk-free interest rate。

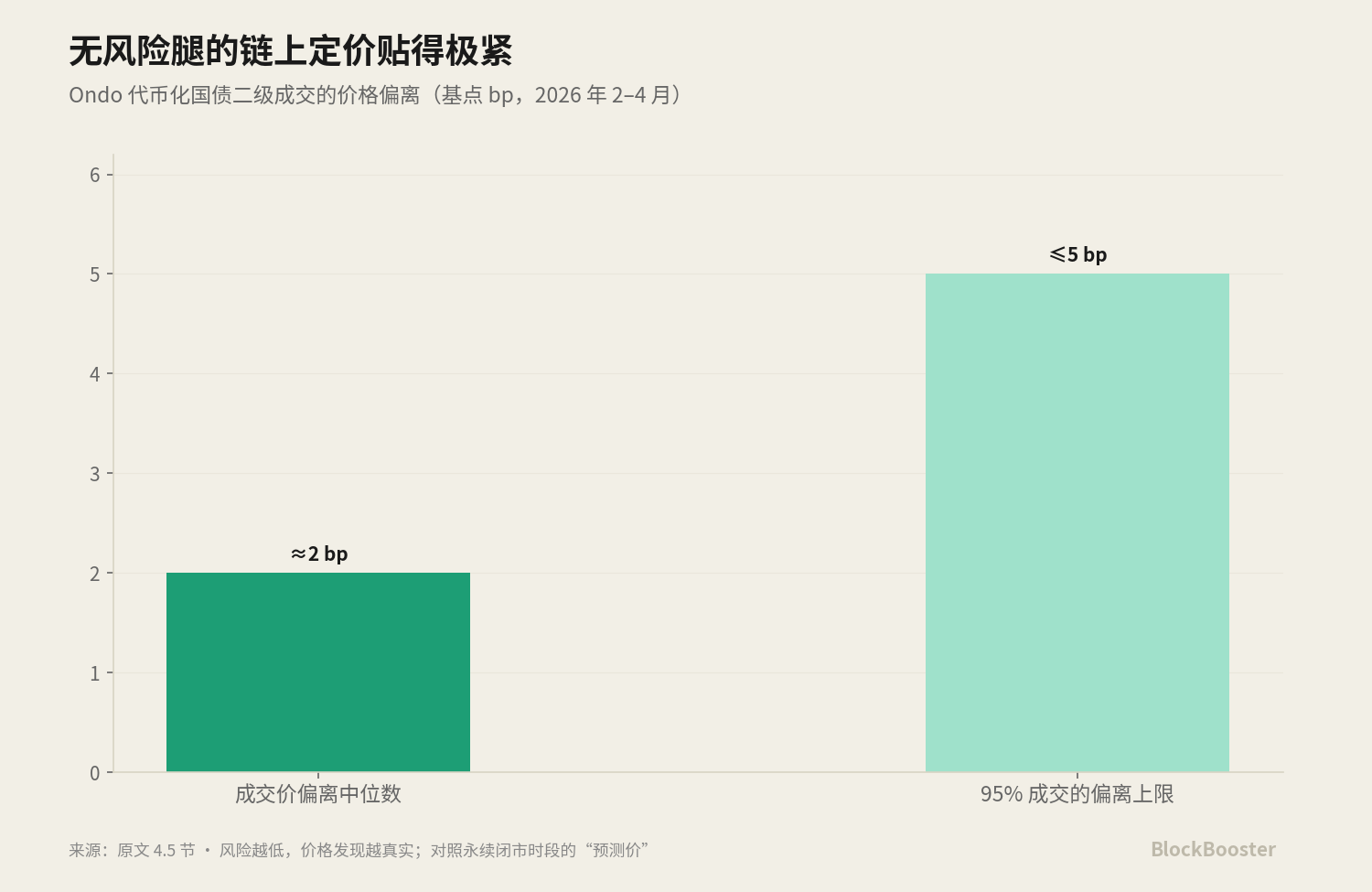

The second-tier market price of the "risk-free leg" itself is very tight - in the case of Ondo's monetized national debt, which varied from about 2 basis points to 95 per cent within 5 basis points between February and April 2026. This means that when the bottom asset is sufficiently standard, sufficiently risk-free, the chain price can be very accurate; by contrast, the "prices" of high-risk species, such as perpetuity, are full of predictive elements during closed market hours — the lower the risk, the more the price is real; the higher the risk, the more the price is speculative。

4.6 Ethena sUSDE

It's a permanent fund rate plus collateral proceedsSecuritizationI DON'T KNOW. ITS ASY, WHICH IS HIGHLY DEPENDENT ON THE LEVEL OF A SUSTAINABLE MARKET FINANCIAL RATE, IS ESSENTIALLY AN IMPLICIT INTEREST RATE REPACKAGING RATHER THAN THE BENCHMARK ITSELF。

Put together seven candidates: they measure different things (leveraging emotions, real borrowing, algorithm utilization, governance policies, risk-free votes, institutional arbitrage), each with different risks (liquidation, counterparties, smart contracts, governance, credit) and priced by different subjects。

None of them fulfils the three conditions of "broad calibre + term structure + governance independence"。

This is the current status of the Crypto base rate: none of the pieces can stand alone as anchors。

5. Self-build spread maps discuss:

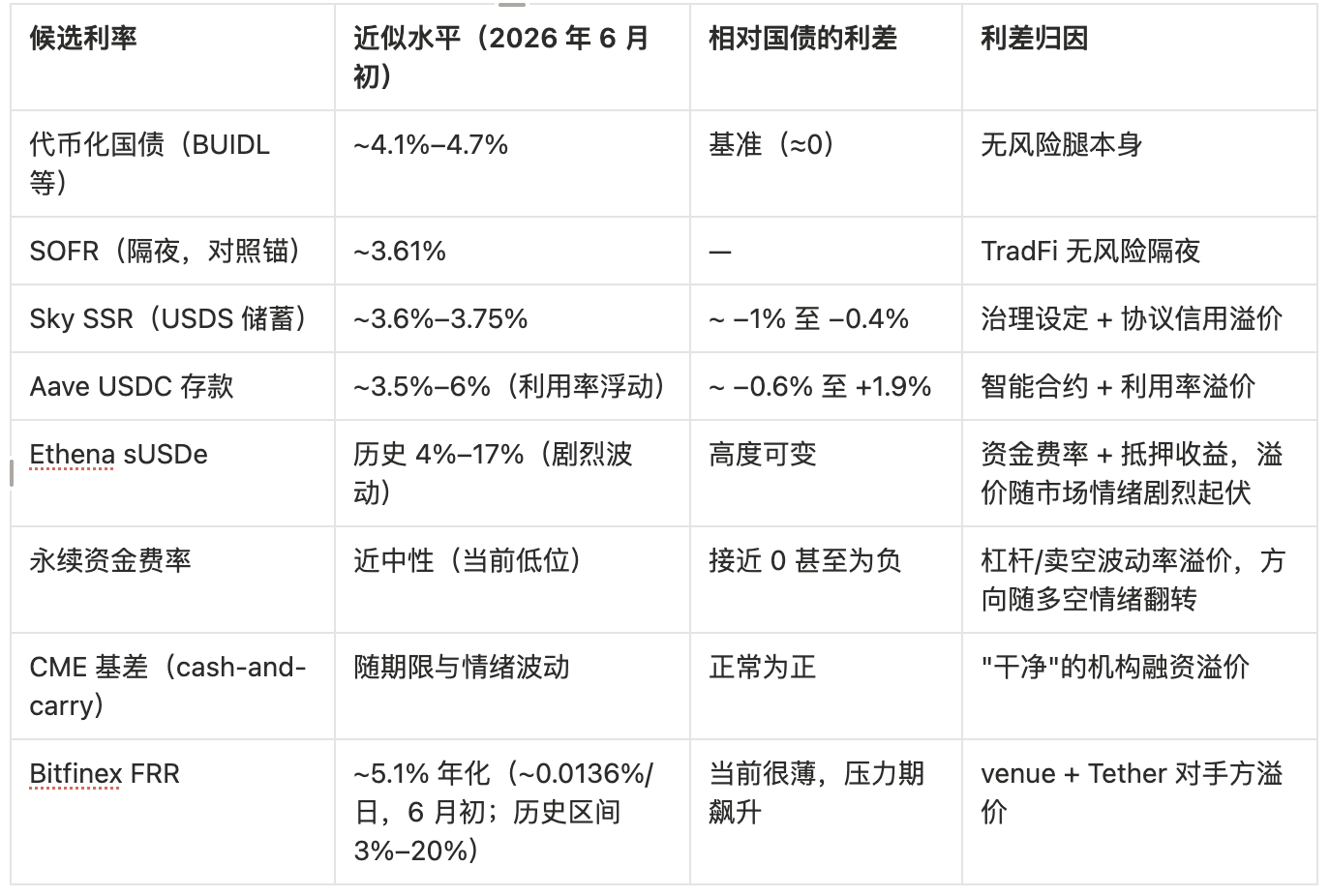

Place the above candidate rate in parallel with the same or comparable period, giving a numerical snapshot with a cut-off date:

Candidate rate Approximate level (early June 2026) Interest spreads on national debt Interest margin attributionMonetary State Debts (BUIDL, etc.) ~4.1 per cent - 4.7 per cent Benchmark (≈0) no-risk leg itself SOFR (overnight, against anchors) ~3.6 per cent ~ TradFi no-risk overnight Sky SSR (USDS savings) ~3.6 per cent - 3.75 per cent ~ -1 per cent - governance set + protocol credit premium Aave USDC deposits ~ 3.5 per cent - 6 per cent (utility floating) ~ 0.6 per cent - +1.9 per cent Smart contracts + utilization premium Ethena susde 4 per cent - 17 per cent history (violability) ~ 3.6 per cent - 3.75 per cent - ~ collateral gain with market sentiment ~ close to (current low) ~ 0 per cent - 6 per cent + 6 per cent + + + + + + + + 6 per cent + + + + + + + + 6 per cent + + + + + + + + + + + + + + + + +

Write the logic of this table into attribution:

- Evolving fund rates - National debt gains - Leverage/Frost Volatility premium

- Bitfinex FRR - National Debt Gains ≈venue risk premium + Tether Competing Premium

- Aave Loan Rate - National Debt Gains

- DSR/SSR - NATIONAL DEBT GAINS

- CME BASE DIFFERENCE - NATIONAL DEBT GAINS ≈ CLEAN INSTITUTIONAL FINANCING PREMIUM

Look at Bitfinex's FRR. It is currently about 5 per cent annualized, and is almost attached to the monetized national debt (~4.5 per cent), Aave (~4–5.5 per cent), SSR (~3.6 per cent) — the margin is thin. FRR seems nothing special, like other candidates. But..THE DANGER OF THE FRR IS NOT ITS "HIGH FLUCTUATIONS."I DON'T KNOW. USD BORROWING INTEREST RATES HAVE BEEN SWINGING SHARPLY BETWEEN 3% AND 20% APR: IN A PERIOD OF CALM LIKE THIS, IT HAS RECEDED TO NEAR A RISK-FREE INTEREST RATE; AND ONCE IT ENTERS A PERIOD OF HIGH LEVERAGE, HIGH DEMAND OR MARKET PRESSURE, IT SURGES RAPIDLY。

Using such interest rates as anchors for the pricing of the entire market means that the anchor itself can jump sharply at times when stability is most needed。

In traditional finance, if the two instruments reflect the same risks and give different interest rates, the arbitragers quickly enter to flatten the spreads. However, in Cripto, spreads are structural risks that are priced by the market。

According to the BIS work paper: Crypto's carry can be very large -Sometimes more than 40 per cent per year, and it fluctuates sharply over time; and at the time of pressure, it is violently reversed - the CME carry once fell - 50% during the FTX crash. Crypto presentsNegative facilitative gains(investor prefers to hold futures rather than spot), which is the opposite of commodity markets - similar to someGovernment bond marketsDynamics (balance sheet binding makes derivatives more attractive than holding spot). In other words, Crypto carry is large and is not flattened by arbitrage because it is difficult for regulated capital to hold cash, to participate only through futures, and because arbitrage capital is scarce because of bonds and liquidity risks。

Summary

This is not the case, but it is not the case, because it is not the case. Possible future combinations in the following directions:Currencyization of the national debt as the base of a risk-free leg + the term curve spelled out by CME base / Bitfinex term structure / interest rate swaps on the chain— Or, a governance neutral aggregate index。

The logic of the former is that risk-free legs should naturally be anchored by assets that are closest to risk-free, while the duration curve needs to be congregated from sources that already exist and have a time-limited structure; the logic of the latter is that rather than relying on any single source, it would be better to use a neutral index that aggregates multiple sources to circumvent concentration in design。