2028 Global smart crisis: an experiment in financial history from the future

Author:CitriniResearch

Foreword

IF WE CONTINUE TO RESPOND TO AI'S EXPECTATIONS... BUT WHAT IF IT'S ACTUALLY A DROP SIGNAL

What follows is a situational assumption rather than precision prediction. It's not about creating panic, it's not about being an AI animist. The only purpose of this article is to model a relatively unexplored scene. Our friend Alap Shah raised the question, and we came up with the answer together. We wrote this part, he wrote two others。

IT IS HOPED THAT AFTER READING THIS PAPER, WHEN AI MAKES THE ECONOMY MORE AND MORE WEIRD, YOU CAN BE BETTER PREPARED FOR POTENTIAL LEFT-SIDE TAIL RISKS。

The following is a macro-memorandum released by CitriniResearch in June 2028, which details the evolution and after-effects of the “global smart crisis”。

Macro Memo: the consequences of adequate intelligence

CitriniResearch22 February to 30 June 2028

The unemployment rate announced this morning reached 10.2 per cent, 0.3 per cent above expectations. The market fell by 2 per cent as a result of this data, resulting in a cumulative fall of 38 per cent over the peak of October 2026。

Traders are numb. If it were six months ago, such data would definitely trigger a melting process。

Just two years。This is the time it takes for the economy to evolve from “risk-controllable” to “specific industries” to a model that none of us can recognize. This quarter's Macro Memorandum is an attempt to reconstruct this series of events — an autopsy report on the pre-crisis economy。

ONCE UPON A TIME, FANATICISM IN THE MARKET WAS WITHIN REACH. BY OCTOBER 2026, THE STANDARD 500 INDEX WAS APPROACHING 8000 POINTS, AND THE NASDAQ INDEX EXCEEDED 30,000 POINTS. THE FIRST WAVE OF LAYOFFS, TRIGGERED BY THE ELIMINATION OF HUMAN BEINGS, BEGAN IN EARLY 2026, WHEN THESE LAYOFFS PERFECTLY ACHIEVED THEIR INTENDED GOALS: PROFIT MARGINS EXPANDED, PROFITS WERE HIGHER THAN EXPECTED AND THE STOCK MARKET INCREASED SIGNIFICANTLY. A RECORD BUSINESS PROFIT HAS BEEN INVESTED DIRECTLY IN AI CALCULATIONS。

THE MACRO-INDICATORS AT THAT TIME REMAINED VISIBLE. NOMINAL GDP RECORDED ANNUAL INCREASES IN MEDIAN AND HIGH DIGITS. PRODUCTIVITY IS FLOURISHING. DRIVEN BY AI INTELLIGENTS WHO DO NOT SLEEP, DO NOT TAKE SICK LEAVE AND DO NOT REQUIRE MEDICAL INSURANCE, THE GROWTH RATE OF REAL OUTPUT PER HOUR HAS REACHED ITS HIGHEST LEVEL SINCE THE 1950S。

As the cost of labour disappears, the wealth of the powerful owners increases explosively. At the same time, real wage growth collapsed. Despite the Government ' s repeated bragging about record productivity, white-collar workers lost their jobs to machines and were forced to turn to low-paid jobs。

When the consumer economy began to crack, economic commentators spread a word -Ghost GDP: those outputs that are reflected in national accounts but have never been circulated in the real economy。

IN ALL RESPECTS, AI EXCEEDED EXPECTATIONS, THE MARKET WAS AI. THE ONLY PROBLEM IS THAT THE ECONOMY IS NOT。

WE SHOULD HAVE KNOWN THAT A GPU CLUSTER IN NORTH DAKOTA COULD PRODUCE THE OUTPUT OF 10,000 WHITE-COLLAR WORKERS IN MIDTOWN MANHATTAN, RATHER THAN AN ECONOMIC PANACEA. MONETARY FLOWS HAVE STALLED. THE HUMAN-CENTRED CONSUMER ECONOMY THAT USED TO ACCOUNT FOR 70 PER CENT OF GDP IS DYING. IF WE HAD ASKED EARLIER, “HOW MUCH WOULD MACHINES SPEND ON FREELY AVAILABLE GOODS?”, WE MIGHT HAVE FIGURED THAT OUT EARLIER

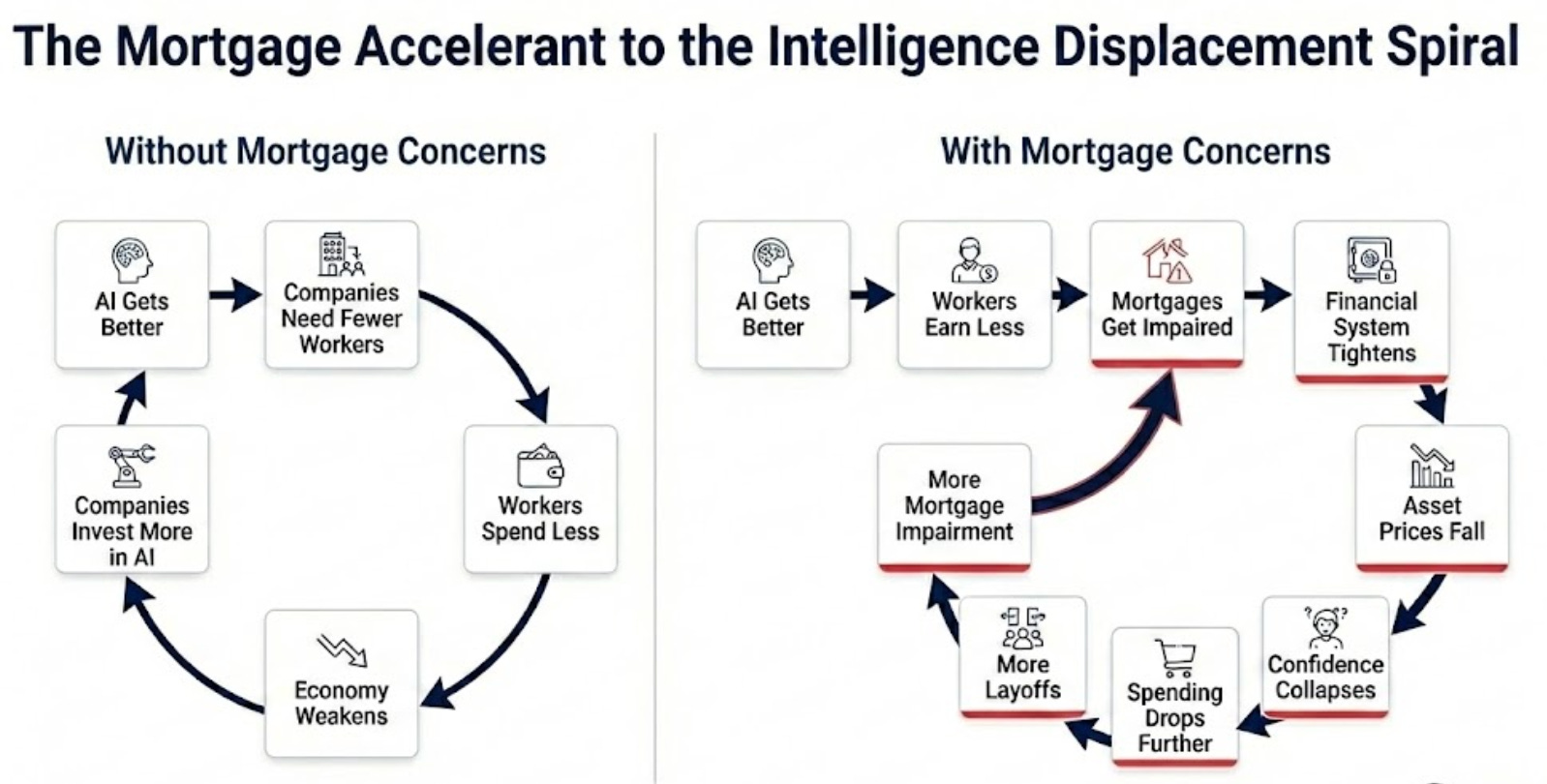

AI INCREASED CAPACITY, FEWER EMPLOYEES NEEDED BY THE COMPANY, MORE WHITE-COLLAR LAYOFFS, REDUCED STAFF CONSUMPTION, PROFIT-RATE PRESSURES FORCING BUSINESSES TO INVEST MORE IN AI, AND MORE IN AI CAPABILITIES ..

This is a negative feedback loop without a natural brake. This is itHuman intelligence substitute spiralI don't know. White-collar workers watched as they suffered structural damage to their profitability (and, of course, their consumption capacity). Their income was once the cornerstone of the $13 trillion mortgage market — forcing underwriters to reassess whether quality mortgages remain safe。

SEVENTEEN YEARS OF ABSENCE OF A GENUINE DEFAULT CYCLE HAVE LEFT THE PRIVATE MARKET FULL OF SOFTWARE TRANSACTIONS SUPPORTED BY PRIVATE EQUITY (PE), ON THE ASSUMPTION THAT ANNUAL RECURRENT INCOME (ARR) WOULD REMAIN “RECURRING”. IN MID-2027, THE FIRST WAVE OF DEFAULT TRIGGERED BY AI SUBVERSION CHALLENGED THIS ASSUMPTION。

If such subversion had been confined to the software industry alone, the situation would have been manageable, but that was not the case. By the end of 2027, it threatened every business model based on intermediary services. A large number of companies built on human frictions have collapsed。

The system as a whole has proved to be a large associated aristocratic chain based on the expected increase in white-collar productivity. The crash in November 2027 merely accelerated all negative feedback cycles that already existed。

We have waited almost a year for the logic of “bad news is good news”. The Government has begun to consider introducing legislation, but public confidence in the Government ' s ability to deliver any form of relief has diminished. Policy responses had always lagged behind economic realities, but the lack of comprehensive plans was threatening the accelerated deflation spiral。

How did the crisis begin

At the end of 2025, the capacity of the proxy programming tool was scaled up。

A skilled developer using Claude Code or Codex can now replicate the core function of a mid-market SaaS product in a few weeks. Although not perfect, and not able to deal with all the peripherals, enough has been given to the Chief Information Officer (CIO) who reviews the $500,000 annual renewal of contracts to start thinking, “What if we build one ourselves?”

The fiscal year is usually the same as the calendar year, so corporate expenditure in 2026 was set in the fourth quarter of 2025, when “agent-like AI” was still a popular language. The mid-year review was the first time that a procurement team had taken a decision with clarity as to what those systems could actually do. Some watched their own internal team roll out the prototype within weeks, copying the six-digit SaaS contract。

That summer, we interviewed the procurement manager of a Fortune 500 company. He told us about his budget negotiations. The salesman would have expected to do the same thing last year: 5% a year, standard "your team cannot leave us." The procurement manager told him that he had been discussing with OpenAI to have its “frontier deployment engineer” use the AI tool to replace the vendor completely. They finally renewed their contract at a discount of 30 per cent. He said it was a good result. Those long tails, like Monday.com, Zapier and Asana, are much worse。

Investors are ready — and even expect — to be hit hard by the long-tail market. They may account for one third of typical enterprise technology warehouse expenditures, but they are clearly exposed to risk. However, the “recording system” should have been free from subversion。

It wasn't until Servicenow published the third quarter of 26, that the mechanism of reflexity became clear。

SERVICENOW NET ADD ACV GROWTH SLOWED FROM 23% TO 14%; ANNOUNCED LAY-OFFS OF 15% AND INITIATED THE STRUCTURAL EFFICIENCY PLAN; STOCK PRICES FELL BY 18% Bloomberg, October 2026

SaaS is not "dead." A cost-benefit analysis is still required to operate and support the internal architecture. But..Internal construction became an option, AND HAS BEEN FACTORED INTO PRICING NEGOTIATIONS. PERHAPS MORE IMPORTANTLY, THE PATTERN OF COMPETITION HAS CHANGED. AI HAS MADE IT EASIER TO DEVELOP AND PUBLISH NEW FEATURES, AND THEREFORE DIFFERENTIATION HAS COLLAPSED. OLD-FASHIONED FIRMS COMPETED FOR PRICES — BOTH CLOSE TO EACH OTHER AND WITH EMERGING POST-SHOWS. ENCOURAGED BY THE LEAP IN PROXY PROGRAMMING CAPACITY AND WITHOUT THE DRAG OF A LEGACY COST STRUCTURE, THESE NEW ENTRANTS HAVE BEEN RADICALIZING IN THEIR MARKET SHARE。

It was not until the financial paper was released that the interconnectivity of these systems was fully recognized. Service Now is a seat charge. When wealth 500 strong clients cut their jobs by 15%, they cancel their permits by 15%. The AI-driven layoffs that increase client profitability are mechanically destroying their own income base。

A company that automates sales workflows is being subverted by better automation of workflows, and its response is to retrench its staff and to use the funds saved to finance the very technology that is destabilizing it。

What else can they do? Waiting to die slowerTHE COMPANIES MOST THREATENED BY AI BECAME THE MOST RADICAL ADOPTERS OF AI。

This was obvious after the fact, but not at that time (not for me at least). Historical subversive models show that established firms resist new technologies, lose market shares to flexible entrants and then slowly disappear. That's what happened to Koda, Baathda and Blackberry. However, what happened in 2026 was different; old firms did not resist because they could not afford to。

FACED WITH THE 40-60 PER CENT DECLINE IN STOCK PRICES AND THE PRESSURE OF THE BOARD OF DIRECTORS TO ASK FOR EXPLANATIONS, AI THREATENED COMPANIES TO DO THE ONLY THING THEY COULD DO: LAY OFF THEIR STAFF, REDEPLOY SAVINGS TO AI TOOLS AND USE THEM TO MAINTAIN OUTPUT AT A LOWER COST。

EACH COMPANY'S RESPONSE WAS RATIONAL. BUT THE COLLECTIVE OUTCOME WAS DISASTROUS. EVERY DOLLAR SAVED ON STAFF CUTS IS FLOWING INTO AI CAPACITY, THUS MAKING THE NEXT ROUND POSSIBLE。

The software industry is just the beginning. When investors are still arguing whether SaaS ' valuation multipliers are at the bottom, they miss this reflexive cycle that has jumped out of the software industry. The same logic that justifies Servicenow ' s layoffs applies to every company with a white-collar cost structure。

When friction drops to zero

BY THE BEGINNING OF 2027, THE USE OF THE LARGE LANGUAGE MODEL (LLM) HAD BECOME A DEFAULT. PEOPLE ARE USING AI SMARTS THAT DON'T EVEN KNOW WHAT AN AI SMART BODY IS, LIKE PEOPLE WHO NEVER LEARN WHAT A CLOUD COMPUTING IS USING STREAMING MEDIA. THEY LOOK AT IT LIKE THEY DO IT AUTOMATICALLY OR SPELL-CHECK IT -- IT'S JUST ONE THING THEIR PHONES CAN DO RIGHT NOW。

Qwen's open source shopping robot is AI's catalyst for taking over consumer decision-making. In a few weeks, every mainstream AI assistant has come together for some sort of proxy business function. Model distillation means that these intelligent bodies can operate not only on cloud cases, but also on mobile phones and laptops, thus significantly reducing the marginal cost of reasoning。

What should have upset investors (but they did not) was that they did not have to wait to be awakened. They operate backstage according to user preferences. Business is no longer a series of discrete human decisions, but a continuous optimization process, representing every connected consumer 24/7 operating all-weather. By March 2027, the median number of American individuals consumed 400,000 Tokens per day -- 10 times as many as at the end of 2026。

The next link in the chain has begun to crack。

Intermediary。

Over the past 50 years, the United States economy has built a huge rent-seeking layer above human limitations: time, patience, brand familiarity to replace due diligence, and most people are willing to accept a bad price to avoid a few more clicks. The value of trillions of dollars depends on the persistence of these constraints。

At first it was simple. Smart bodies remove friction。

Those subscriptions and memberships that do not require automatic renewal even for a few months. The entry prices that were secretly doubled after the trial period. These are all redefined as “hostage crisis” where smarts can negotiate. The indicator that underpins the economy as a whole — average customer life-cycle value — has fallen significantly。

Consumer intelligence began to change the way consumer transactions operate almost all。

Human beings do not have time to compete on five competing platforms before buying a box of protein sticks. But the machine has。

Tourism reservation platforms are the first victims because they are the simplest. By the fourth quarter of 2026, our intelligent body was able to assemble a full journey faster and cheaper than any platform (flights, hotels, ground traffic, integrity optimization, budgetary constraints, refunds)。

The insurance renewal model has been completely re-engineered, and the whole model was originally dependent on the inertia of the insured. The intelligent body that revalues your coverage every year breaks the premium of 15-20% earned by insurance companies from passive renewal。

Financial recommendations. Tax preparation. Regular legal work. Any type of service provider whose value claim is ultimately attributed to “I will deal with complex matters on your behalf that you find boring” has been subverted, because intelligence does not feel that anything is boring。

EVEN THOSE AREAS THAT WE BELIEVE ARE PROTECTED BY THE “VALUE OF HUMAN RELATIONSHIPS” HAVE PROVED TO BE FRAGILE. IN THE REAL ESTATE SECTOR, BUYERS HAVE ENDURED 5-6 PER CENT COMMISSIONS FOR DECADES BECAUSE OF INFORMATION ASYMMETRIES BETWEEN BROKERS AND CONSUMERS. HOWEVER, ONCE THE AI INTELLIGENT BODY EQUIPPED WITH MLS ACCESS RIGHTS AND DECADES OF TRANSACTIONAL DATA IS ABLE TO COPY THESE KNOWLEDGE BASES IN AN INSTANT, THE BUSINESS COLLAPSES. A SELLER'S STUDY IN MARCH 2027 REFERRED TO IT AS “INTELLECTUAL VIOLENCE AGAINST INTELLIGENT BODIES”. THE MEDIAN COMMISSION FOR MAJOR METROPOLITAN BUYERS HAS BEEN REDUCED FROM 2.5 TO 3 PER CENT TO LESS THAN 1 PER CENT, AND MORE AND MORE BUYERS ARE NOT INVOLVED AT ALL WITH HUMAN BROKERS。

We overestimated the value of “human relationships”. It has proved that the relationship is largely “a friction with a friendly mask”。

This is just the beginning of the destruction of the middle ground. Successful companies had spent billions of dollars on effectively using consumer behaviour and human psychological weaknesses, but none of that mattered now。

The machine that opts for price and suitability, doesn't care about your favorite application, doesn't care about the site that you've customarily opened over the last four years, and doesn't feel the attraction of carefully designed closure experiences. They will not be tired and accept the simplest option, nor will they acquiesce in “I always order here”。

This destroys a particular moat:Traditional intermediariesI don't know。

DoorDash (DASH US) is a typical example。

Programming smarts break down entry barriers to the introduction of off-sale applications. A capable developer could deploy a fully functional rival in a few weeks, and many did. By distributing 90-95 per cent of the distribution fee directly to the driver, they attracted the driver from DoorDash and UberEats. Multi-application dashboards allow casual workers to track entry lists from 20 or 30 platforms at the same time, thus eliminating the locking effect on which existing businesses rely. Markets become fragmented overnight and profit margins are reduced to almost zero。

Smarts accelerate both supply and demand for destruction. They empower their competitors and then use them. DoorDash literally means, "You're hungry, you're lazy, this is your application on the main screen." Smart body does not have a main screen. It will examine DoorDash, Uber Eats, the restaurant ' s own website and 20 newly developed alternatives so that the lowest cost and the fastest distribution can be selected each time。

The machine does not have customary application loyalty, which is the basis of the entire business model。

This is a strange verse, which is probably the only example of a smart body that has helped the white-collar workers who are about to be replaced. When they eventually became delivery drivers, at least half of their income was not paid to Uber and DoorDash. Of course, with the spread of auto-driving cars, the benefits of technology have not been sustained for too long。

Once intelligence controls the trade, they start looking for bigger prey。

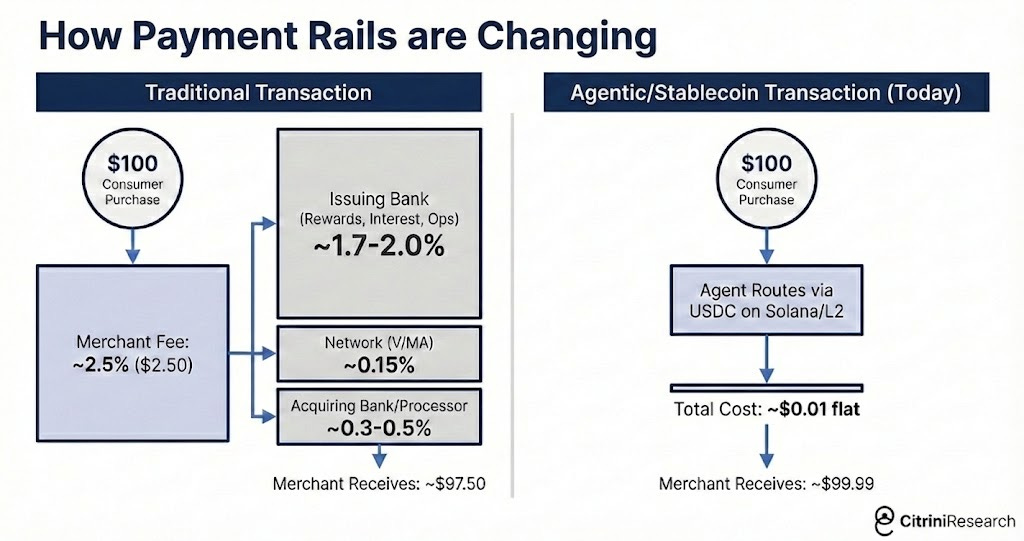

The potential for price and aggregation is limited. The biggest way to save money for users repeatedly (especially when intelligent bodies start trading with each other)Elimination costsI don't know. In machine-to-machine commerce, two to three percent of the card exchange rates became obvious targets。

Smart people start looking for faster and cheaper options than credit cards. Most chose to use the stable currency through Solana or the Taifung L2, where the settlement was almost instantaneous, while transaction costs were calculated at a fraction of a cent。

MasterCard 2027 First quarter: Net income growth 6% per year; Purchase volume growth slowed from +5.9% in the previous quarter to +3.4%; Management noted “intelligence-led price optimization” and “pressure for non-essential consumer goods category” • Bloomberg, 29 April 2027

MasterCard's first quarter of 2027 is a dead end. The proxy business went from a product story to an infrastructure pipeline story. The MasterCard fell by 9% the next day. Visa has also fallen, but the decline has narrowed somewhat after analysts pointed out that it is better positioned to stabilize the currency infrastructure。

Agent commerce circumvents exchange rates and poses a far greater risk to banks and single-business issuing agencies, which focus on issuing cards. These agencies charge the bulk of the 2-3 per cent fee and have established an entire business sector around incentive schemes funded by commercial subsidies。

American Express (AXP US) has been hit hardest; it faces double resistance: white-collar layoffs empty its client base, while intelligents bypass exchange rates to empty its income pattern. Synchrony (SYF US), Capital One (COF US) and Discover (DFS US) also fell by more than 10 per cent in the next few weeks。

Their moat is made of friction. And..The friction is returning to zero。

From industry risk to systemic risk

THROUGHOUT 2026, THE MARKET VIEWED THE NEGATIVE IMPACT OF AI AS A STORY OF THE “INDUSTRY LEVEL”. THE SOFTWARE AND CONSULTANCY INDUSTRY IS BEING HIT HARD, WITH PAYMENTS AND OTHER “PAYSTATIONS” SHAKING, BUT THE WIDER ECONOMY SEEMS TO BE SAFE. THE LABOUR MARKET, ALTHOUGH WEAK, IS NOT FREE TO FALL. THERE IS GENERAL CONSENSUS THAT CREATIVE DESTRUCTION IS PART OF ANY CYCLE OF TECHNOLOGICAL INNOVATION. IT WILL BE PAINFUL IN SOME AREAS, BUT AI WILL BRING MORE NET GAINS THAN ANY NEGATIVE IMPACT。

IN OUR JANUARY 2027 MACRO MEMORANDUM, WE POINTED OUT THAT THIS IS THE WRONG THINKING MODEL. THE UNITED STATES ECONOMY IS A WHITE-COLLAR SERVICE ECONOMY. WHITE-COLLAR WORKERS ACCOUNT FOR 50 PER CENT OF EMPLOYMENT AND DRIVE ABOUT 75 PER CENT OF DISCRETIONARY CONSUMPTION EXPENDITURE. AI COMPANIES AND JOBS THAT ARE DEVOURING ARE NOT ON THE EDGE OF THE US ECONOMYYeahThe United States economy itself。

“Technology and innovation will create more jobs while eliminating them”. This was the most popular and persuasive counter-argument at the time. It is popular and persuasive because it has been right for the past two centuries. Even if we cannot imagine what the future will look like, they will come。

THE ATM HAS REDUCED THE OPERATING COSTS OF BANK OUTLETS, RESULTING IN MORE BANK OUTLETS, WHILE THE NUMBER OF CASHIERS EMPLOYED HAS RISEN IN THE NEXT TWO DECADES. THE INTERNET HAS DESTABILIZED TRAVEL AGENCIES, YELLOW PAGES, AND ENTITY RETAILING, BUT IT HAS CREATED COMPLETELY NEW INDUSTRIES AND CREATED NEW JOBS。

I don't knowEvery new job needs to be carried out by human beings。

AI IS NOW A UNIVERSAL INTELLIGENCE THAT IS MAKING PROGRESS ON TASKS THAT WOULD OTHERWISE HAVE BEEN REDEPLOYED TO HUMANITY. THE PROGRAMMER WHO WAS REPLACED COULD NOT SIMPLY TURN TO "AI MANAGEMENT" BECAUSE AI ALREADY HAD MANAGERIAL CAPACITY。

TODAY, AI'S SMART BODY HANDLES RESEARCH AND DEVELOPMENT FOR WEEKS. DESPITE THE FACT THAT PROFESSORS AT BUSINESS SCHOOLS ARE TRYING TO SYNTHESIZE DATA INTO A NEW S CURVE EVERY YEAR, THE GROWTH OF THE INDEX LEVEL HAS CRUSHED OUR PERCEPTION OF POSSIBILITIES。

They prepared almost all the codes. The best-performing intelligent body is much smarter in almost everything than almost all humans. And they're getting cheaper。

AIIndeedNEW JOBS WERE CREATED. PHRASING ENGINEER. AI SECURITY RESEARCHER. INFRASTRUCTURE TECHNICIAN. HUMAN BEINGS REMAIN IN A CYCLE OF COORDINATION AT THE HIGHEST LEVEL OR CONTROL OF TASTE. BUT FOR EVERY NEW ROLE CREATED BY AI, IT HAS ELIMINATED DOZENS OF OLD ONES. AND THE SALARY OF THE NEW ROLE IS ONLY A FRACTION OF THE OLD ROLE。

JOLTS UNITED STATES: JOB OPENINGS HAVE FALLEN BELOW 5.5 MILLION; THE RATIO OF UNEMPLOYED TO VACANT JOBS HAS RISEN TO ABOUT 1.7, THE HIGHEST LEVEL SINCE AUGUST 2020 Bloomberg, October 2026

THE RECRUITMENT RATE HAS BEEN WEAK THROUGHOUT THE YEAR, BUT THE OCTOBER 26 JOLTS DATA PROVIDE SOME DECISIVE EVIDENCE. JOB OPENINGS FELL BY 5.5 MILLION, A 15 PER CENT DECREASE OVER THE SAME PERIOD。

INDED: RECRUITMENT ANNOUNCEMENTS IN THE SOFTWARE, FINANCE AND CONSULTANCY INDUSTRIES HAVE DECLINED SIGNIFICANTLY AS THE PRODUCTIVITY INITIATIVE SPREADS Indeed Hiring Lab, 2026

White-collar vacancies are falling, while blue-collar vacancies (construction, health care, skilled workers) remain relatively stable. The loss of staff is concentrated in jobs where memos are written (for some reason, we are still operating), where budgets are approved and where the middle of the economy is maintained. However, real wage growth in both categories of the population was negative for most of the year and continued to decline。

The stock market continues to be less concerned about JOLTS data, and more concerned with General Electric Vernova, all of which has been sold in 2040, with a ripple of negative macro and positive AI infrastructure news。

However, bond markets (always smarter or at least less romantic than stock markets) began to price consumption shocks. The annual rate of return on sovereign debt began to decline in the next four months from 4.3 to 3.2 per cent. Nevertheless, the overall unemployment rate did not increase explosively, and the nuanced structure was still overlooked by some。

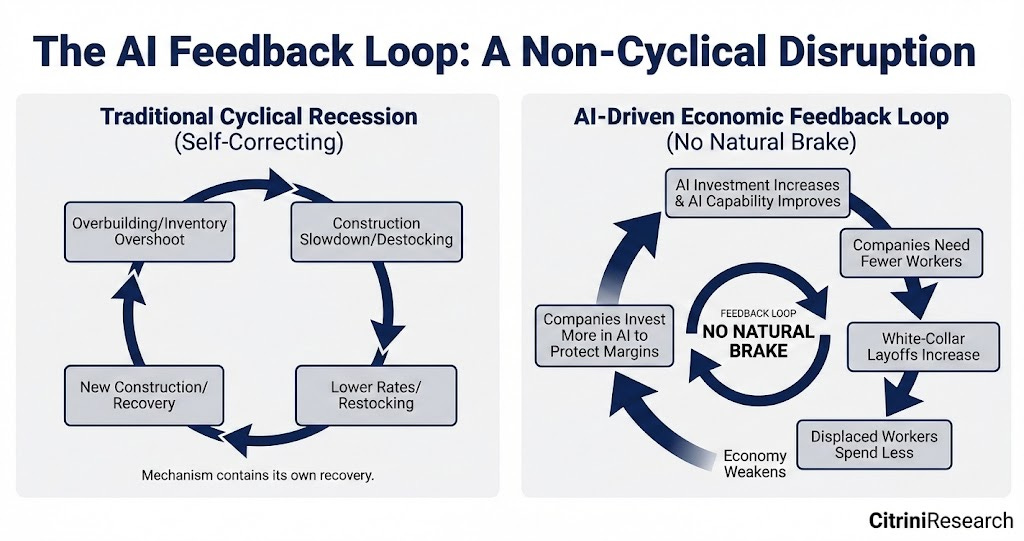

In the normal economic downturn, the causes eventually change themselves. Overconstruction led to a slowdown in construction, leading to lower interest rates, which in turn stimulated new construction. Excess stocks lead to the removal of stocks, which triggers re-entry. The cyclical mechanism contains its own seeds for recovery。

The causes of this cycle are not cyclical。

AI GETS BETTER AND CHEAPER. THE COMPANY CUTS STAFF AND THEN BUYS MORE AI CAPACITY WITH SAVED MONEY, WHICH ALLOWS THEM TO LAY OFF MORE EMPLOYEES. THERE WAS A DECREASE IN STAFF CONSUMPTION. COMPANIES THAT SELL GOODS TO CONSUMERS SELL LESS AND BECOME LESS POWERFUL, SO THEY INVEST MORE MONEY IN AI TO PROTECT PROFITABILITY. AI GETS BETTER AND CHEAPER。

A negative feedback loop without a natural brake。

Intuitively, it is expected that the decline in total demand will slow the construction of AI. However, this did not occur because it was not a capital expenditure (CapEx) of the facility style. This is an OpEx replacement. A company that used to spend $100 million per year on employees and $5 million on AI now spends $70 million on employees and $20 million on AI. AI investments have multiplied, but it has occurred as part of the reduction in total operating costs. Each company ' s AI budget is growing while its overall expenditure is shrinking。

IRONICALLY, EVEN THOUGH AI IS BEGINNING TO DETERIORATE IN A SUBVERSIVE ECONOMY, AI INFRASTRUCTURE COMPLEXES CONTINUE TO PERFORM WELL. NVDA IS STILL PUBLISHING RECORD REVENUES. THE BUILD-UP (TSM) IS STILL RUNNING AT 95%+. MEGA-SCALE CLOUD MANUFACTURERS CONTINUE TO SPEND $150 BILLION PER QUARTER ON CAPITAL EXPENDITURES FOR DATA CENTRES. ECONOMIES THAT HAVE FULLY HIGHLIGHTED THIS TREND, SUCH AS TAIWAN AND SOUTH KOREA, HAVE PERFORMED SIGNIFICANTLY BETTER THAN LARGER ECONOMIES。

India is the opposite. The country ' s IT services sector exports more than $200 billion per year, the largest contributor to India ' s current account surplus and the source of funding to offset its ongoing merchandise trade deficit. The whole model is based on a value proposition: the cost of Indian developers is only a small fraction of that of American counterparts. However, the marginal cost of AI programming smarts has collapsed to the point where they are essentially electricity bills. In 2027, the cancellation of contracts by Tata Consulting (TCS), Infosys and Wipro accelerated. As a result of the evaporation of services surpluses that anchored India ' s external accounts, the rupee to the United States dollar fell by 18 per cent in four months. By the first quarter of 2028, the International Monetary Fund (IMF) had begun “preliminary discussions” with New Delhi。

The destabilizing engines are growing stronger every quarter, which means that the rate of subversion is accelerating every quarter. There is no natural bottom in the labour market。

IN AMERICA, WE NO LONGER ASK HOW THE AI INFRASTRUCTURE BUBBLE WILL BREAK. WE STARTED ASKINGWhat happens in an economy based on consumer credit when consumers are replaced by machines。

Smart substitute spiral

THE YEAR 2027 WAS A LESS SUBTLE YEAR FOR MACROECONOMIC NARRATIVES. OVER THE PAST 12 MONTHS, IT HAS BECOME APPARENT THAT THE TRANSMISSION MECHANISMS OF THESE DISCONNECTED BUT APPARENTLY NEGATIVE TRENDS HAVE BECOME APPARENT. YOU DON'T NEED TO GO TO THE BUREAU OF LABOR STATISTICS (BLS) DATA. YOU JUST HAVE TO GO TO A FRIEND'S DINNER。

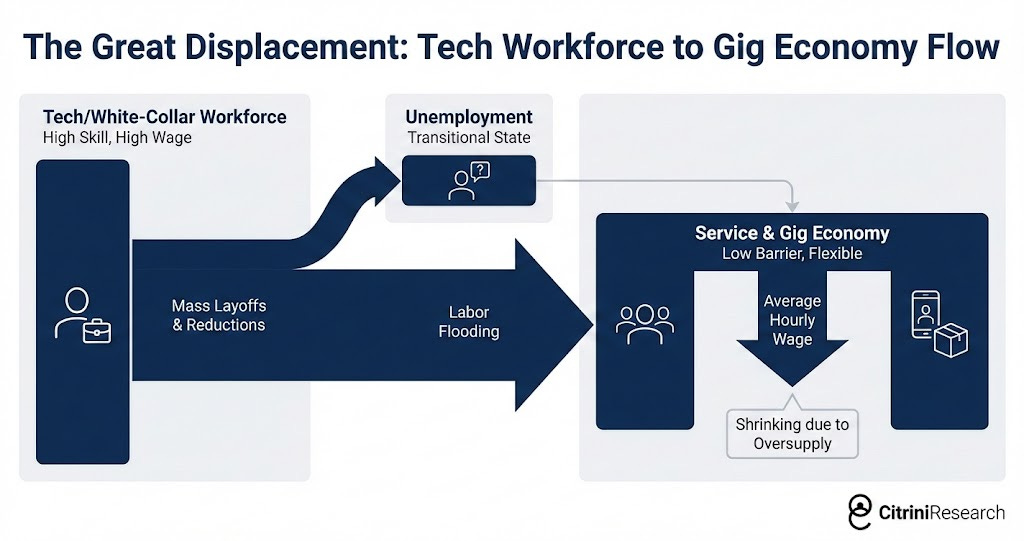

The replaced white-collar workers are not idle. They're downgraded. Many are employed in low-paid services and in part-time economic jobs, which increases the supply of labour in these areas and reduces wages there。

A friend of ours was senior product manager at Salesforce in 2025. Title, health insurance, 401k old-age pension, $180,000 per annum. She lost her job in the third round of downsizing. After six months of searching, she started driving Uber. Her income fell to $45,000. It's not about personal stories, it's about second-class mathematical effects. This dynamic is multiplied by the hundreds of thousands of workers in each major metropolitan area. Overskilled labour flows into the service sector and the casual economy have strained the wages of already struggling existing workers. The sector-specific subversion has deteriorated into wage compression across the economy。

The only remaining human-centred labour pool has yet to be amended, and it happens at the moment when we write these words. This is due to the fact that automatic delivery and auto-driving cars are swirling the economy of casual workers who absorb the first wave of replaced workers。

BY FEBRUARY 2027, IT WAS CLEAR THAT THE CONSUMPTION PATTERNS OF PROFESSIONALS WHO STILL WORKED WERE AS IF THEY WERE THE NEXT TO BE LAID OFF. THEY REDOUBLED THEIR WORK (MAINLY WITH THE HELP OF AI) JUST TO KEEP THEM FROM BEING FIRED, AND THE PROSPECT OF A PROMOTION OR A RAISE WAS DASHED. SAVINGS RATES HAVE INCREASED SLIGHTLY AND EXPENDITURES HAVE WEAKENED。

The most dangerous part is delay. High-income people have maintained normal appearances over two to three quarters, using their above-average savings. Hard data do not recognize the existence of the problem until it becomes an old story in the real economy. Subsequently, data to break this illusion were published。

America's initial unemployment benefit surged to 48.77 million, the highest level since April 2020 Ministry of Labour, third quarter of 2027

The number of applicants for unemployment benefits rose sharply to 48.77 million, the highest level since April 2020. ADP and Equifax confirmed that the vast majority of new applicants were white-collar professionals。

The 500 index dropped 6% in the next week. Negative macro-factors are beginning to dominate the river。

In the general economic downturn, unemployment is widespread. The suffering borne by blue-collar and white-collar workers is roughly equal to the share of the various groups in total employment. Consumption strikes are also widespread and will soon appear in the data, as low-income workers have a higher marginal consumption tendency。

During this cycle, unemployment was concentrated in the highest income distribution deciles. They account for a relatively small proportion of total employment, but they drive a disproportionate share of consumer expenditure. The top 10 percent of the income accounts for more than half of all consumer spending in the United States. The first 20 percent is about 65 percent. They buy houses, buy cars, take vacations, leave houses, pay tuition for private schools and renovate houses. They are the demand base of the entire non-essential consumer economy。

When these workers lose their jobs or accept a 50 per cent reduction in wages to move to available jobs, consumption strikes are huge relative to the number of jobs lost. White-collar employment fell by 2 per cent and turned into a 3-4 per cent effect on discretionary consumer spending. Unlike blue-collar unemployment, which usually has an immediate impact (you are fired from the factory and will cease consumption next week), the impact of white-collar unemployment is lagging behind but deeper, because these workers have savings buffers that enable them to maintain spending for several months before a fundamental shift in behaviour occurs。

BY THE SECOND QUARTER OF 2027, THE ECONOMY WAS IN RECESSION. THE NATIONAL BUREAU OF ECONOMIC RESEARCH (NBER) OF THE UNITED STATES DID NOT FORMALLY SET THE DATE OF COMMENCEMENT OF THE RECESSION UNTIL A FEW MONTHS LATER, AS THEY HAVE ALWAYS DONE, BUT THE FIGURES ARE CLEAR — WE HAVE EXPERIENCED TWO CONSECUTIVE QUARTERS OF NEGATIVE REAL GDP GROWTH. BUT THIS IS NOT A “FINANCIAL CRISIS” ... TEMPORARILY。

Related bets on the ass chain

Private Credit has grown from less than $1 trillion in 2015 to more than $2.5 trillion in 2026. A significant portion of this capital was deployed in software and technology transactions, many of which were leveraged by SaaS (LBO) based on the assumption that income would remain at the middle and high levels for all time。

these assumptions were already dead between the first proxy programming demonstration and the collapse of the software stock in the first quarter of 2026, but the book value of these assets (marks) did not seem to realize that they were dead。

When the transaction prices of many listed SaaS companies fell to 5-8 times EBITDA, the book value of PE-supported software companies on the balance sheet still reflected the acquisition valuation based on the multiple of income no longer available. Management gradually lowered the book value from 100 cents to 92, 85, while comparable companies in the open market gave a valuation of 50。

Moody's downgraded 14 issuers with 18 billion dollars in private equity-supported software debt ratings for “long-term income reversals caused by artificially intelligent competitive subversion”; this was the largest single-sector downgrade since the energy crisis in 2015 Moody's Investor Services, April 2027

Everyone remembers what happened after the demotion. Industry veterans have seen this script since the downgrade in 2015。

Software-supported loans began to default in the third quarter of 2027. PE Portfolios in the area of information services and consultancy follow closely. Several multibillion-dollar acquisitions involving well-known SaaS companies entered the reorganization phase。

Zendesk is conclusive evidence。

ZENDESK FAILED TO MEET THE DEBT CONTRACT DUE TO THE AUTOMATED EROSION OF ARTIFICIAL INTELLIGENCE-DRIVEN CUSTOMER SERVICES; $5 BILLION IN DIRECT LOAN FACILITIES WAS MARKED AT 58 CENTS; AND THE LARGEST PRIVATE CREDIT SOFTWARE DEFAULT RECORD EVER RECORDED Financial Times, September 2027

In 2022, Hellman & Friedman and Permira privatized Zendesk with $10.2 billion. The debt portfolio included $5 billion in direct loans, the largest ARR-supported credit facility in history at the time, led by Blackstone, with Apollo, Blue Owl and HPS in the loan consortium. The clear structure of the loan is based on the assumption that the annual recurrent income (ARR) of Zendesk will remain unchanged. In a situation where the leverage rate is about 25 times that of EBITDA, it makes sense only in this context。

By mid-2027, that premise no longer existed。

In most of the year, AI intelligence has started to handle client services autonomously. The categories defined by Zendesk (worksheets, routers, management of human passenger service interaction) have been replaced by systems that can solve problems without generating worksheets. “Annual recurrent income”, which is the basis for loan underwriting, is no longer recurrent, but is only income that has not left。

THE LARGEST ARR-SUPPORTED LOAN IN HISTORY BECAME THE LARGEST PRIVATE CREDIT SOFTWARE DEFAULT IN HISTORY. EVERY CREDIT COUNTER ASKS THE SAME QUESTION AT THE SAME TIME:Who else disguised the long-term reverse winds as cyclical

But that was the correct point of the initial consensus (at least at the beginning): it should have survived。

PRIVATE CREDIT IS NOT BANKING IN 2008. THE WHOLE STRUCTURE WAS CLEARLY DESIGNED TO AVOID BEING FORCED TO SELL. THESE ARE CLOSED TOOLS TO LOCK CAPITAL. LIMITED PARTNERS (LP) HAVE COMMITTED THEMSELVES TO A PERIOD OF SEVEN TO TEN YEARS. NO DEPOSITOR WOULD RUN AND NO BUY-BACK AGREEMENT WOULD BE WITHDRAWN. MANAGERS CAN HOLD DAMAGED ASSETS, RESOLVE THEM OVER TIME AND WAIT FOR RECOVERY. PAIN, BUT CONTROLLABLE. THE SYSTEM IS DESIGNED TO BEND, BUT NOT TO BREAK。

Blackstone, KKR and Apollo executives cite software risk exposures as only 7-13 per cent of assets. Risks are manageable. Every seller's report and Twitter credit volume V are saying the same: private credit has permanent capital. They can absorb enough losses to blow up leverage banks。

Permanent capital。This term appears in every financial conference and investor letter designed to reassure people. It became a spell. Like most spells, no one pays attention to more subtle details. Here's what it really means

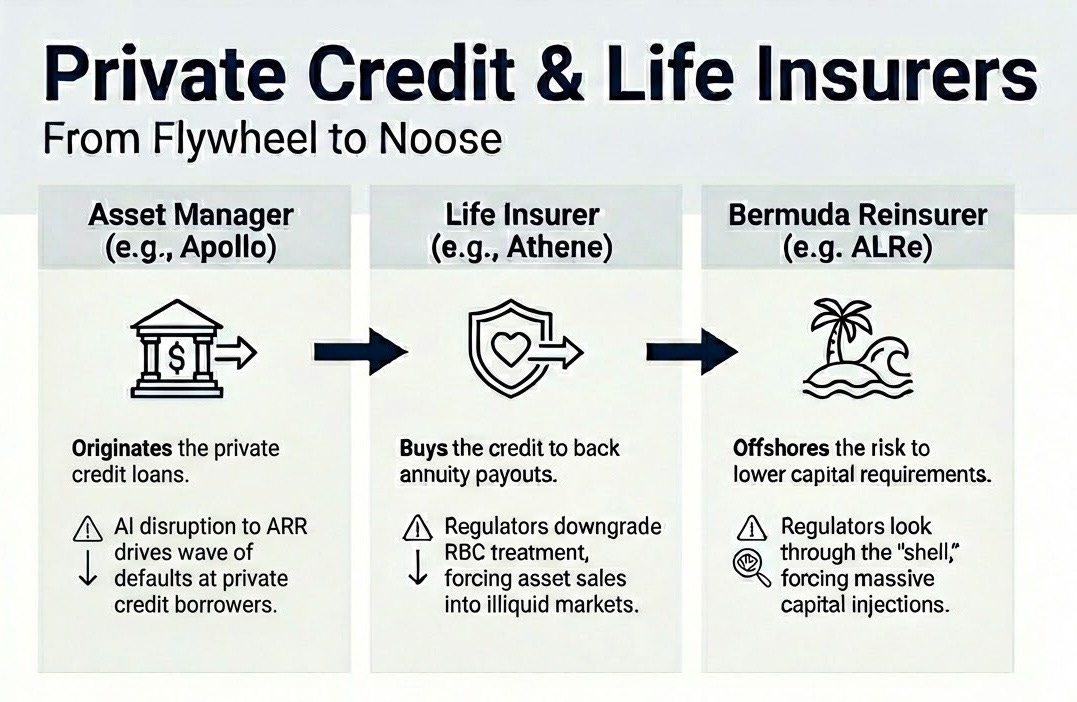

In the past decade, large alternative asset management companies have acquired life insurance companies and turned them into financial instruments. Apollo acquired Atene. Brookfield bought American Equity. KKR acquired Global Atlantic. The logic is elegant: annuity deposits provide a stable, long-term liability base. Fund managers invest these deposits in private credit they initiate and are paid twice — a margin in insurance and a management fee in asset management. A “cost-for-work” permanent motive that works well under one condition。

This presupposes that private credit must be secured。

The loss impacted on the balance sheet of holding non-current assets to meet long-term liabilities. “Permanent capital”, which should have made the system flexible, was not some sort of abstract, patient institutional capital and mature investor with complex risks。It's savings for American families, Main Street, STRUCTURED INTO AN ANNUITY TO INVEST IN SOFTWARE AND TECHNICAL INSTRUMENTS THAT ARE ALSO CURRENTLY IN DEFAULT AND SUPPORTED BY PE. THE LOCKING CAPITAL THAT CANNOT ESCAPE IS THE MONEY OF A LIFE INSURANCE POLICYHOLDER, AND IN THAT AREA THE RULES ARE SOMEWHAT DIFFERENT。

COMPARED TO THE BANKING SYSTEM, INSURANCE REGULATORS HAVE ALWAYS BEEN GENTLE — AND EVEN SOMEWHAT COMPLACENT — BUT THIS IS THE MOMENT OF ALARM. REGULATORS THAT ARE ALREADY DISTURBED BY THE HIGH CONCENTRATION OF PRIVATE CREDIT IN LIFE INSURANCE COMPANIES HAVE BEGUN TO REDUCE RISK-BASED CAPITAL (RBC) TREATMENT OF THESE ASSETS. THIS FORCES INSURANCE COMPANIES TO RAISE CAPITAL OR SELL ASSETS, BUT NEITHER CAN BE ACHIEVED ON ATTRACTIVE TERMS IN FROZEN MARKETS。

NEW YORK, IOWA REGULATORY BODIES TAKE ACTION TO TIGHTEN THE CAPITAL TREATMENT OF CERTAIN PRIVATE RATING CREDITS HELD BY LIFE INSURANCE COMPANIES; NAIC (NATIONAL ASSOCIATION OF INSURANCE SUPERVISORS) GUIDANCE IS EXPECTED TO ADD RBC FACTORS AND TRIGGER ADDITIONAL REVIEWS Reuters, November 2027

When Moody lowered the Athene's financial strength rating to a negative outlook, Apollo's share price fell by 22 per cent in two trading days. Maple, KKR, and so on。

THE SITUATION IS BECOMING MORE COMPLEX. NOT ONLY HAVE THESE COMPANIES CREATED THEIR INSURANCE PERMANENT MOTIVATIONS, THEY HAVE ALSO ESTABLISHED A COMPLEX OFFSHORE STRUCTURE DESIGNED TO MAXIMIZE RETURNS THROUGH REGULATORY ARBITRAGE. AMERICAN INSURANCE COMPANIES WRITE DOWN AN ANNUITY AND THEN HAND OVER RISK TO THEIR SIMILARLY OWNED BERMUDA OR CAYMAN AFFILIATE REINSURANCE COMPANIES, WHICH WERE FORMED TO TAKE ADVANTAGE OF MORE FLEXIBLE REGULATION TO ALLOW FOR LESS CAPITAL TO BE HELD IN THE SAME ASSETS. THE SUBSIDIARY RAISES EXTERNAL CAPITAL THROUGH THE OFFSHORE SPECIAL PURPOSE ENTITY (SPV), A LAYER OF NEW COUNTERPARTIES THAT INVEST WITH INSURANCE COMPANIES IN PRIVATE CREDIT INITIATED BY THE ASSET MANAGEMENT OF THE SAME PARENT COMPANY。

RATING AGENCIES, SOME OF WHICH ARE OWNED BY PE THEMSELVES, ARE NOT MODELS OF TRANSPARENCY (WHICH IS HARDLY SURPRISING). THE DEGREE OF OPACITY OF THE WEB OF SPIDERS CONNECTED TO DIFFERENT BALANCE SHEETS IS ALARMING. WHEN THE BOTTOM LOAN DEFAULTSWho did itThis question is simply not answered in real time。

The crash in November 2027 marked a shift from a potentially ordinary cycle to a more disturbing situation. At an emergency meeting of the Federal Open Market Commission in November, Federal Reserve Chairman Kevin Walsh called:“a large associated aristocratic chain based on expectations of white collar productivity growth.”

See, it was never the loss itself that caused the crisis. Rather, it admits (and confirms) these losses. In the area of finance, there is another area of greater importance, and we are increasingly afraid that it will be identified。

Mortgage problems

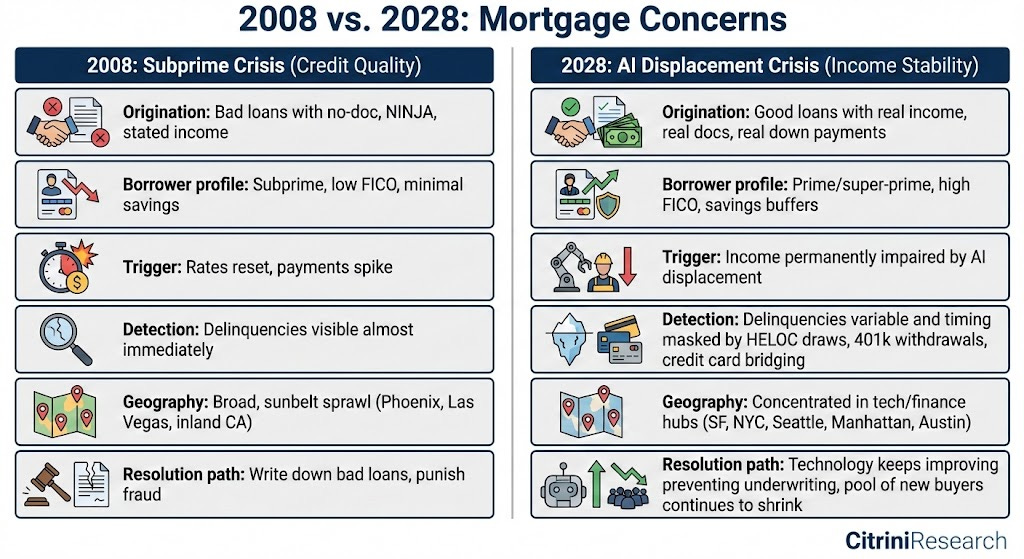

ZILLOW Housing Value Index shows a decline of 11 per cent in San Francisco, 9 per cent in Seattle and 8 per cent in Austin; Fannie Mae indicates an "early increase in default rate" in the ZILOW region, where over 40 per cent of the population is employed in science and technology/finance Zillow / Fanny Mae, June 2028

This month, the Zillow House Value Index dropped by 11 percent in San Francisco, by 9 percent in Seattle and by 8 percent in Austin. This is not the only worrying title. Last month, Fanny Mae pointed out that the “jumbo-healthy” postal code region had an early default rate - These areas are inhabited by borrowers with credit ratings in excess of 780 and are usually considered to be “ballistic” (very safe)。

The size of the United States mortgage market is about $13 trillion. Mortgage underwriting is based on the basic assumption that the borrower will be employed at a level of approximately current income for the duration of the loan. In most mortgages, this means 30 years。

The white collar employment crisis threatened this assumption by continuing changes in income expectations. We must now ask a question that seemed absurd three years agoIs the quality mortgage safe

Every previous mortgage crisis in the history of the United States has been driven by one of three reasons: excessive speculation (lending to people who cannot afford to buy a house, e.g. 2008), interest rate shocks (i.e., rising interest rates have made adjustable interest rate mortgages unaffordable, e.g., in the early 1980s) or partial economic shocks (a single industry collapses in a single area, e.g., the oil industry in Texas in the 1980s or the automobile industry in Michigan in 2009)。

NONE OF THIS APPLIES TO THE CURRENT SITUATION. THE BORROWER QUESTIONED WAS NOT A SUB-PRIME. THEY HAVE 780 POINTS OF FICO CREDIT RATING. THEY PAID 20% OF THE DOWN PAYMENT. THEY HAVE GOOD CREDIT RECORDS, STABLE WORK RECORDS, AND THEIR INCOME IS VERIFIED AND RECORDED AT THE TIME THE LOANS ARE ISSUED. THEY ARE BORROWERS WHO SEE EVERY RISK MODEL IN THE FINANCIAL SYSTEM AS A CORNERSTONE OF CREDIT QUALITY。

In 2008, the loan was bad on the first day. In 2028, the loan was good on the first day. It's just that the world changed after the loan was written. People are borrowing money for a future they can no longer afford。

In 2027, we marked the early signs of invisible pressure: withdrawals from the House Net Value Credit Line (HELOC), 401 (k) pension withdrawals and credit card debt surges, while mortgage repayments remained in their current state. As a result of unemployment, recruitment freezes and cuts in bonuses, these high-quality families watched as their debt earnings doubled。

THEY MAY STILL REPAY MORTGAGES PROVIDED THAT ALL DISCRETIONARY EXPENSES ARE STOPPED, SAVINGS ARE VACATED AND ANY MAINTENANCE OR IMPROVEMENT OF THE HOUSE IS DEFERRED. TECHNICALLY, THEIR MORTGAGES ARE STILL CURRENT, BUT ONLY ONE STEP AWAY FROM GETTING IN TROUBLE, AND THE TRAJECTORY OF AI CAPACITY INDICATES THAT THE SHOCK IS IMMINENT. THEN WE SAW A SHARP RISE IN ARREARS RATES IN SAN FRANCISCO, SEATTLE, MANHATTAN AND AUSTIN, ALTHOUGH THE NATIONAL AVERAGE REMAINED WITHIN HISTORICAL NORMALITY。

We are now at the most critical stage. If the marginal buyer (i.e. the person likely to connect) is healthy, the fall in the house price is manageable. Here, marginal buyers are responding to the same loss of income。

Despite growing concerns, we have not yet been caught up in a full-scale mortgage crisis. Although the rate of non-compliance has increased, it remains well below the 2008 level. The real threat lies in itDevelopment trajectoryI don't know。

Today, the smart replacement spiral has two major financial boosters to accelerate the real recession。

LABOUR SUBSTITUTION, MORTGAGE CONCERNS, VOLATILITY IN THE PRIVATE MARKET. EACH IS MUTUALLY REINFORCING. WHILE THE TRADITIONAL POLICY TOOLKIT (INTEREST-RATE REDUCTION, QUANTITATIVE EASING QE) CAN ADDRESS THE PROBLEM OF THE FINANCIAL ENGINE, IT CANNOT SOLVE THE PROBLEM OF THE REAL ECONOMY, WHICH IS NOT DRIVEN BY TIGHT FINANCIAL CONDITIONS. IT IS DRIVEN BY AI, WHICH REDUCES HUMAN INTELLIGENCE SCARCITY AND VALUES. YOU CAN REDUCE INTEREST RATES TO ZERO AND BUY ALL MORTGAGE-BACKED SECURITIES (MBS) AND DEFAULTED SOFTWARE LEVERAGE TO BUY DEBTS..

But that doesn't change a fact:A Claude smart body can complete the work of a product manager with an annual salary of $180,000 at a cost of $200 per month。

If these fears become a reality, the mortgage market will collapse in the second half of this year. In that case, we expect that the current stock market retreat will eventually be comparable to the global financial crisis (from peak to bottom 57 per cent). This will lower the 500 index to about 3,500 points - This is the level we've never seen since November 2022, the first month of ChatGPT。

It is clear that the income assumptions supporting $13 trillion in residential mortgages have suffered structural damage. It is not clear whether policies can intervene before the mortgage market fully digests the implication. We are full of hope, but we cannot deny those reasons that upset us。

Time versus Time

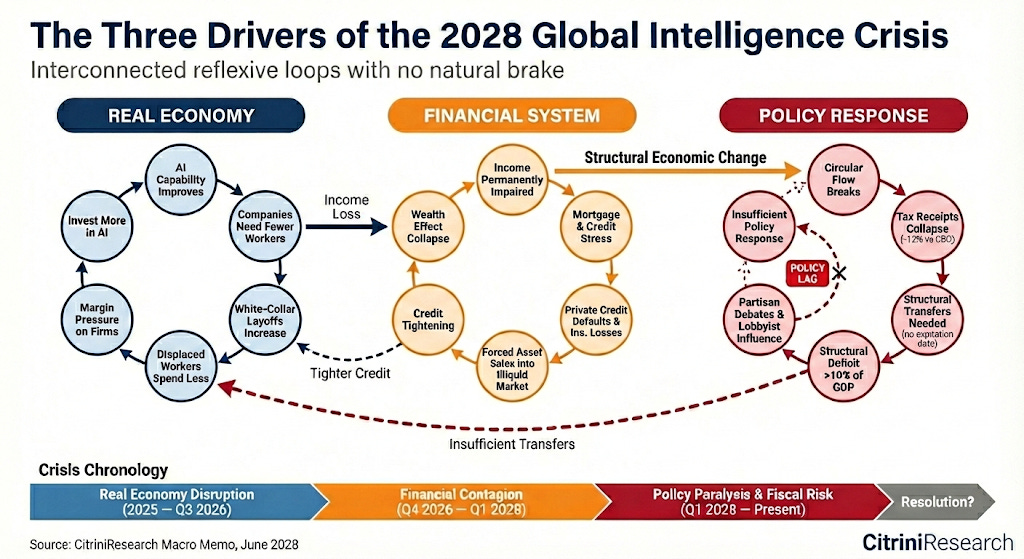

THE FIRST NEGATIVE FEEDBACK CYCLE TOOK PLACE IN THE REAL ECONOMY: AI INCREASED CAPACITY, GROSS WAGES CONTRACTED, CONSUMPTION WEAKENED, PROFITABILITY TIGHTENED, ENTERPRISES PURCHASED MORE AI CAPABILITIES AND AI INCREASED CAPACITY. THE CRISIS THEN SPREAD TO THE FINANCIAL SECTOR: INCOME LOSSES HIT MORTGAGES, BANK LOSSES TIGHTENED CREDIT, WEALTH EFFECTS COLLAPSED AND FEEDBACK CYCLES ACCELERATED. BOTH WERE EXACERBATED BY THE GOVERNMENT ' S LACK OF AWARENESS AND RESPONSE TO THE CRISIS。

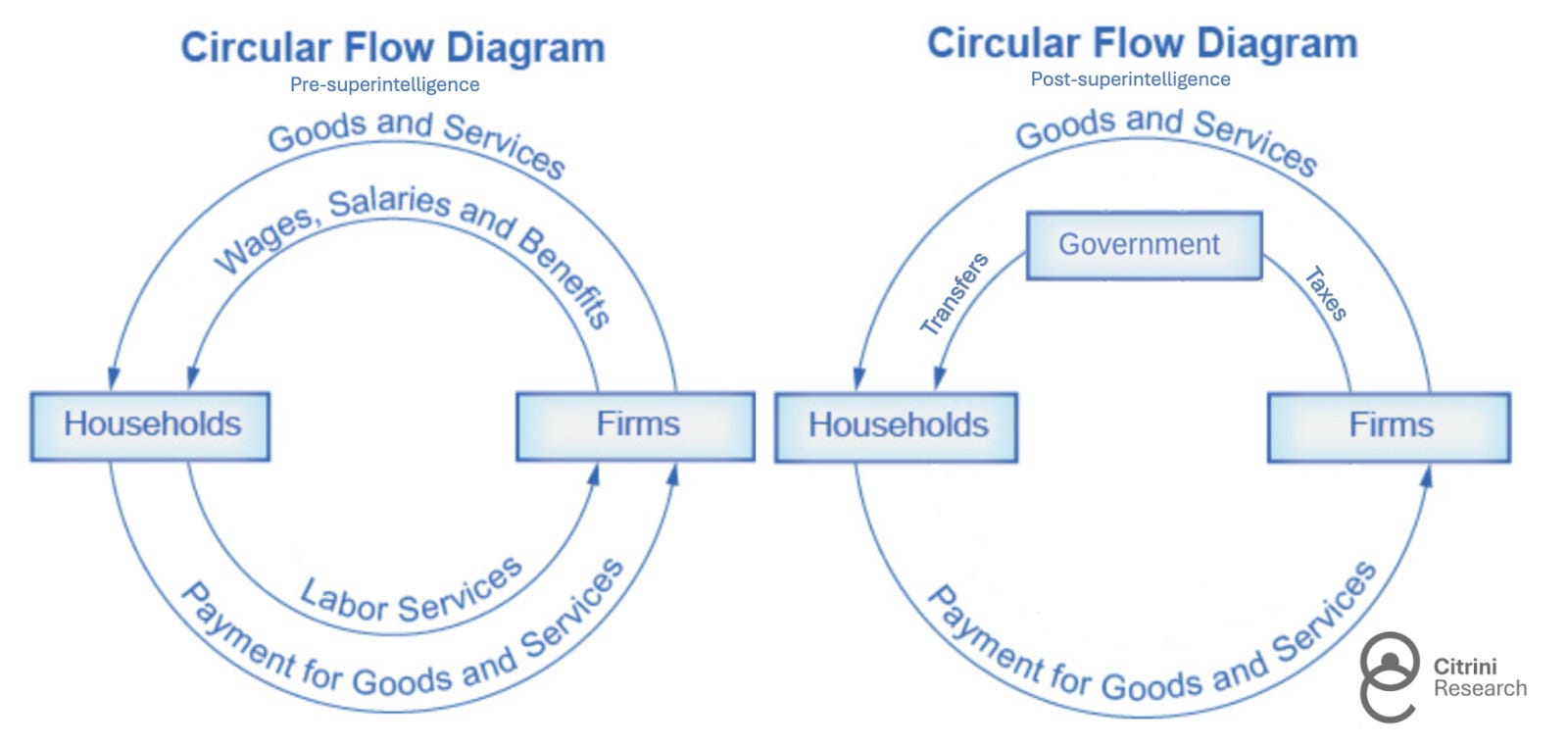

Our systems are not designed for such crises. The federal Government's income base is essentially a human time tax. People work, companies pay them, and the Government takes a portion of it. In normal years, personal income tax and wage tax are the pillars of government revenue。

UNTIL THE FIRST QUARTER OF THIS YEAR, FEDERAL REVENUE WAS 12 PER CENT LOWER THAN THE BENCHMARK FORECAST OF THE CONGRESSIONAL BUDGET OFFICE (CBO). WAGE TAX REVENUES ARE DECLINING AS FEWER PEOPLE ARE ABLE TO EARN THE HIGHER WAGES THEY USED TO EARN. INCOME TAX REVENUES ARE DECLINING AS THE ABSOLUTE INCOME EARNED BY PEOPLE HAS BECOME STRUCTURALLY LOWER. PRODUCTIVITY SURGES, BUT RETURNS GO TO CAPITAL AND COMPUTING RATHER THAN LABOUR。

THE SHARE OF THE LABOUR FORCE IN GDP FELL FROM 64 PER CENT IN 1974 TO 56 PER CENT IN 2024, A SLOW DECLINE OF 40 YEARS DRIVEN BY GLOBALIZATION, AUTOMATION AND THE STEADY EROSION OF WORKERS ' BARGAINING POWER. HOWEVER, IN THE PAST FOUR YEARS, WHEN AI BEGAN TO MAKE PROGRESS IN INDEX LEVELS, THE PROPORTION FELL SHARPLY TO 46 PER CENT. THIS IS THE BIGGEST DROP EVER RECORDED。

OUTPUTS STILL EXIST. HOWEVER, IT NO LONGER RECYCLES ITS BUSINESS THROUGH FAMILIES, WHICH MEANS THAT IT NO LONGER PASSES THROUGH THE UNITED STATES INTERNAL REVENUE SERVICE (IRS). CYCLE FLOWS ARE BREAKING, AND THE GOVERNMENT IS EXPECTED TO BE INVOLVED IN REPAIRING THE PROBLEM。

As in every economic downturn, expenditures have increased while incomes have fallen. But the difference is that expenditure pressures are not cyclical. Auto stabilizers (automatic stabilizers) are designed to respond to temporary unemployment and are not structural alternatives. The system pays benefits on the assumption that workers will be reintegrated into the job market. But many will not, at least not be able to re-enter the workforce at a level close to their previous wages. During the new covid, the government did not hesitate to accept the 15% deficit because it was recognized as a “temporary” situation. However, groups requiring government support today are not experiencing a reversible epidemicThey are permanently replaced by an evolving technology。

It is precisely at a time when government revenue collection from households has decreased that the Government needs to transfer more money to families。

The United States will not default. It produces the currency it consumes, the same currency it repays borrowers. But that pressure has already appeared elsewhere. Municipal bonds show worrying signs of fragmentation in their performance from the beginning of the year to the present. There is no state income tax, but general liability municipal bonds issued by income tax-dependent states (mostly Blue County) begin to price the risk of default. Politicians quickly noticed this, and the debate about who should be saved quickly turned into a partisan one。

To be sure, the government has long recognized the structural nature of the crisis and has begun to consider bipartisan proposals for what they call the Transition Economic Act: a framework for transferring payments directly to unemployed workers by combining deficit spending with taxes on AI’s reasoning。

The most radical option on the table goes further. The Share AI Prosperity Act proposes to establish public claims for the benefits of an intelligent infrastructure, ranging from sovereign wealth funds to royalties on AI ' s output to finance household transfers. As expected, private sector lobbyists have warned in the media of the catastrophic downturn that this would bring。

THE POLITICAL GAME BEHIND THE POLICY DISCUSSIONS IS EXTREMELY COMMON AND IS CHARACTERIZED BY POPULAR FAVOURITISM AND MARGINAL POLICIES. THE RIGHT-WING REBUFFS THE TRANSFER AND REDISTRIBUTION OF WEALTH AS MARXISM AND WARNS THAT TAXING ARITHMETIC IS TANTAMOUNT TO GIVING CHINA THE LEAD. THE LEFT SIDE WARNED THAT A TAX CODE DRAFTED WITH THE HELP OF VESTED INTERESTS WOULD ONLY BE DISGUISED CUSTODIAL CAPTURE. FISCAL HAWKS TALK ABOUT UNSUSTAINABLE DEFICITS. DOVES, ON THE OTHER HAND, POINT TO AUSTERITY POLICIES TOO EARLY IN THE WAKE OF THE GLOBAL FINANCIAL CRISIS (GFC) AS A PRECEDENT. AS THE PRESIDENTIAL ELECTION APPROACHES THIS YEAR, THIS DIVISION WILL ONLY BE FURTHER AMPLIFIED。

When politicians argue, the fabric of society is torn apart far beyond the legislative process。

The “occupation of Silicon Valley” campaign is a microcosm of widespread public discontent. Last month, demonstrators blocked the entrances of Anthony and OpenAI San Francisco offices for three consecutive weeks. Their numbers are increasing, and the demonstration attracted even more media coverage than the unemployment data that triggered the protests。

It is hard to imagine that the public will hate anyone more than bankers in the aftermath of the global financial crisis, but AI lab is trying to break this record. Moreover, from the point of view of the general public, such hatred is justifiable. The rate of accumulation of wealth by the founders and early investors of AI has overshadowed the Golden Age. The gains from the productivity boom are almost entirely attributable to the owners of the calculus and the laboratory shareholders operating above, which magnifies the level of inequality in the United States to unprecedented levels。

Each side has its own perceived villain, but the real villain is time。

AI CAPABILITIES EVOLVE FASTER THAN INSTITUTIONS ADAPT. POLICY RESPONSES ARE ADVANCING AT AN IDEOLOGICAL RATE, NOT AT A REALISTIC RATE. IF THE GOVERNMENT DOES NOT AGREE ON THE CORE OF THE PROBLEM AS SOON AS POSSIBLE, THE FEEDBACK CYCLE DESCRIBED ABOVE WILL REPLACE THEM IN THE NEXT CHAPTER。

The end of the smart premium

Throughout modern economic history, human intelligence has been the most scarce input factor. Capital is abundant (or at least replicable). Natural resources are limited but can be replaced. The progress of technology is slow enough, and human beings have time to adapt to it. Intelligence alone — that is, the ability to analyse, make decisions, create, convince and coordinate — is something that cannot be replicated on a large scale。

The inherent premium of human intelligence stems from its scarcity. Every system in our economic system, from the labour market to the mortgage market to the tax code, has been designed for this hypothetical world。

Now we're going through the end of this premium. In an increasing number of missions, machine intelligence is becoming a competent and fast-paced alternative to human intelligence. The financial system — after decades of optimization and adaptation to a world of scarce human minds — is being repricing. Such repricing is painful, disorderly and far from over。

But re-pricing does not amount to a collapse。

The economic system can find a new balance. How to get there is one of the remaining tasks that can only be carried out by human beings. We have to get this right。

For the first time in history, the most productive assets in the economy have brought fewer jobs than more. No one's analytical framework is applicable because none is designed for “a world where scarce elements become extremely abundant”. We must therefore create a new framework. The timely establishment of these frameworks is the only important issue。

But you didn't read this article in June 2028. You were reading it in February 2026。

The Standard 500 index is near historical heights. The negative feedback cycle has not yet started. We are convinced that some of these scenarios will not become a reality. We are equally confident that machine intelligence will continue to accelerate. Human intelligence premiums will shrink。

As investors, we still have time to assess how much of the portfolio is based on assumptions that will not survive the decade. As a society, we still have time to be proactive。

The canary in the mine is still alive。