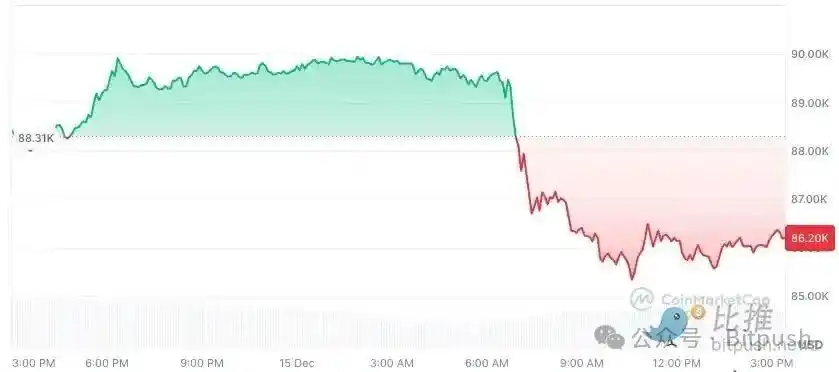

Bitcoin went down $86,000, but the drop just started

The Bloomberg intelligence strategist even gave a very pessimistic prediction that bitcoin would probably return to $10,000 in 2026。

Original title: "Bake fell back 10,000? One of Bloomberg's experts gave the most pessimistic predictions

Original by: Seed.eth, vs. Bitpush News

IN THE PAST WEEKEND, THE ENCRYPTION MARKET HAS NOT BEEN EMOTIONALLY REPAIRED. BITCOIN, AFTER MANY DAYS OF NARROW SHOCK, WAS CLEARLY UNDER PRESSURE FROM SUNDAY EVENING TO MONDAY'S UNITED STATES SHARE TIME. PRICES FELL AT A FULL LEVEL OF $90,000, WITH THE LOWEST DROP IN THE DISC NEAR $86,000. ETH DECLINED BY 3.4 PER CENT TO $2,980; BNB FELL BY 2.1 PER CENT; XRP FELL BY 4 PER CENT; SOL FELL BY 1.5 PER CENT AND FELL AROUND $126. OF THE TOP TEN ENCRYPTED CURRENCIES, ONLY TRX RECORDED A SLIGHT INCREASE OF LESS THAN 1%, AND THE REST IS IN A STATE OF RECALL。

IN TERMS OF TIME DIMENSION, THIS IS NOT AN ISOLATED ADJUSTMENT. SINCE MID-OCTOBER, WHEN THE HISTORICAL HEIGHTS WERE REFRESHED, BITCOIN HAS ACCUMULATED MORE THAN 30 PER CENT, AND EACH ROUND APPEARS TO BE BRIEF AND HESITANT. ALTHOUGH THERE WAS NO SYSTEMATIC OUTFLOW OF ETF FUNDS, MARGINAL INFLOWS SLOWED SIGNIFICANTLY, MAKING IT DIFFICULT TO PROVIDE AN "EMOTIONAL CHASSIS" TO THE MARKET AS THEY HAD BEFORE. THE ENCRYPTION MARKET IS MOVING FROM UNILATERAL OPTIMISM TO A MORE COMPLEX AND PATIENT PHASE。

Against this background, Mike McGlone, a senior Bloomberg Intelligence commodity strategist, released an update that put the current movement of bitcoin into a larger macro and cyclical framework and casts a high degree of uncertainty on the market:Bitcoin is likely to return to $10,000 in 2026It is one of the potential results of a special "deflation" cycle。

This argument is highly controversial not only because the numbers themselves are “too low” but because McGlone does not treat bitcoin as an independent encrypted asset, but rather re-examines it in the long-term system of “global venture capital – liquidity – return of wealth.”。

"Inflation deflation"? McGlone's not about encryption, it's about periodic turning points

The key to understanding McGlone's judgment is not how he sees the encryption industry, but how he understands the macro-environment of the next phase。

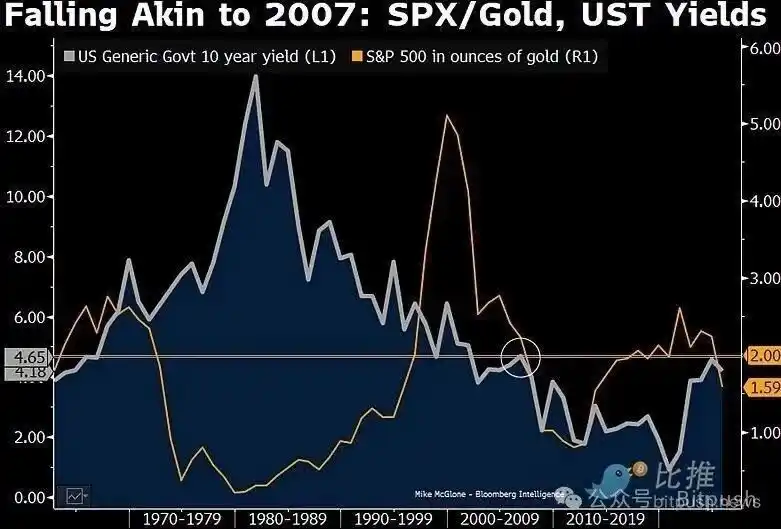

In its latest view, McGlone has repeatedly emphasized the concept of inflation / Deflation Impact. In his view, the global market was standing near such a critical node. As inflation peaks in major economies and growth forces slow, the asset-pricing logic is shifting from “counter-inflation” to “inflation deflation” – that is, the phase of overall price decline at the end of the inflation cycle. He wrote: "The downward trend in bitcoin is likely to recreate what happened in 2007 when the stock market faced Fed policy. I don't know

This was not the first time that he had sent a visual warning. As early as last November, he predicted that bitcoin would fall to the $50,000 threshold。

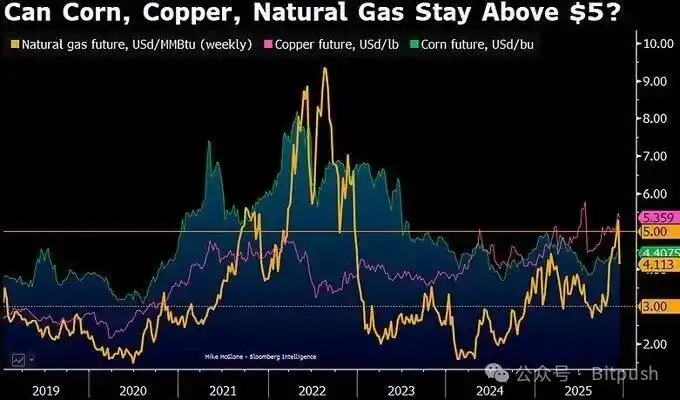

He noted that, around 2026, commodity prices could be around the "inflation-deflation line" or near $5 for a key axis of commodities such as natural gas, maize and copper, where only copper, an asset supported by real industrial demand, could remain on the axis by the end of 2025。

McGlone points out that when liquidity declines, markets re-draw the distinction between "real demand" and "financial premium". In his framework, Bitcoin is not a "digital gold" but an asset that is highly related to risk preferences and speculative cycles. When inflation narratives recede and macroeconomic liquidity tightens, bitcoin tends to reflect this change earlier and more sharply。

In McGlone, it seems that his logic is not based on a single technical position, but on the superimposed of three long-term paths。

First, there is the return of the values of extreme wealth creation. McGlone has long stressed that bitcoin is one of the most extreme amplifiers of wealth in the global monetary climate of the past decade or so. When asset prices have grown far beyond the growth of the real economy and cash flows in the long term, returns are often not moderate but rather dramatic. Historically, both the US dollar in 1929 and the technology bubble in 2000, there was a commonality at the top: markets repeatedly looked for “new paradigms” at the top, and the final adjustment, after all, tended to go far beyond the most pessimistic expectations。

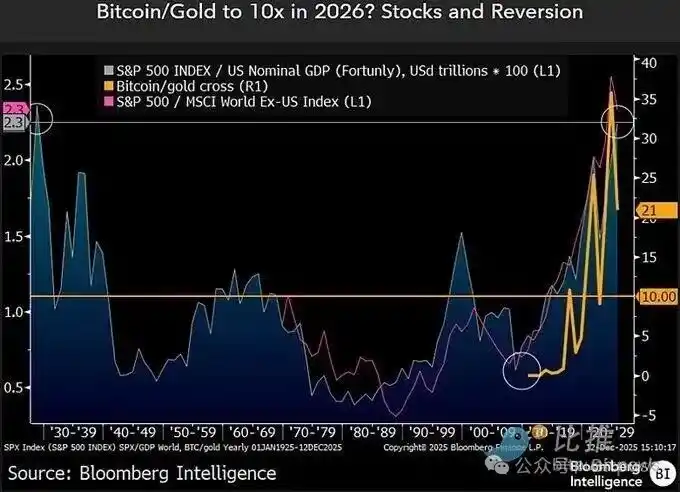

Second is the relative pricing relationship between bitcoin and gold. McGlone places special emphasis on the bitcoin/gold margin indicator. The ratio was about 10 times higher at the end of 2022, then rapidly expanding in the cattle market, reaching more than 30 times in 2025. But since this year, the margin has fallen by about 40 percent, to about 21 times. In his view, if deflation pressure persisted and gold remained strong because of the need to avoid risk, then the margin went back to historical space, not a radical assumption。

Thirdly, there are systemic problems with the environment in which speculative assets are supplied. Although Bitcoin itself has a clear aggregate ceiling, McGlone has repeatedly pointed out that the real deal in the market is not the "singleness" of Bitcoin, but the entire encrypted ecological risk premium. When millions of tokens, projects and narratives compete for the same risk budget, the entire block is often subject to uniform discounts during the deflation cycle, and bitcoin is difficult to completely separate from this revaluation process。

It is important to note that Mike McGlone is not the emptiness of the encryption market. As a senior commodity strategist, Bloomberg has long studied the cyclical relationship between crude oil, precious metals, agricultural products, interest rates and risk assets. His predictions are not always accurate, but their value is that he often raises structural reversals when market sentiment is most consistent。

In his latest statement, he also took the initiative to revisit his "mistakes", including underestimating the time of the gold breakthrough of US$ 2,000 and the deviation between the rate of return on the US debt and the US stock tempo. In his view, however, those deviations were counter-copier certificates: the market was the most prone to misperception of trends before the turn of the cycle。

Other voices: differences are widening

Of course, McGlone's judgment is not market consensus. In fact, the attitude of the mainstream institutions is clearly divided。

TRADITIONAL FINANCIAL INSTITUTIONS, SUCH AS SCRAMBLING, HAVE RECENTLY SIGNIFICANTLY LOWERED THE MEDIUM- AND LONG-TERM TARGET PRICE OF BITCOIN, DOWN FROM $200,000 TO ABOUT $100,000 FOR 2025, WHILE ALSO ADJUSTING THE IMAGINATION SPACE FOR 2026 FROM $300,000 TO ABOUT $150,000, I.E. INSTITUTIONS NO LONGER ASSUME THAT ETF AND ENTERPRISE CONFIGURATIONS WILL CONTINUE TO PROVIDE MARGINAL BUYS BETWEEN PRICE ZONES。

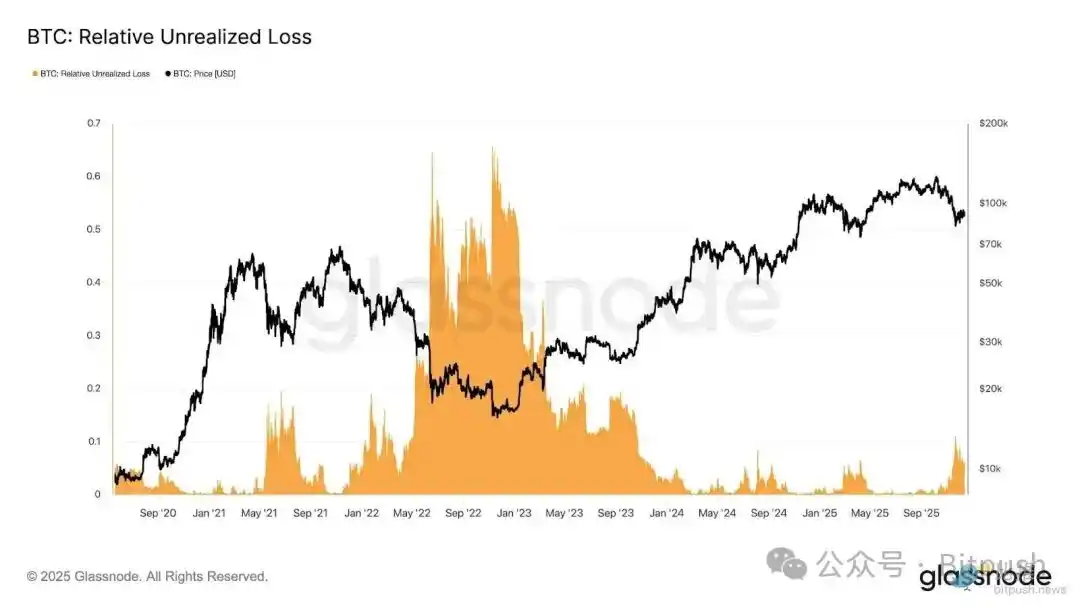

According to Glassnode, bitcoin has now triggered market pressure between $80,000 and $90,000 between shocks, which is more intense than it was at the end of January 2022. The relative unrealized losses on the current market are approaching 10 per cent of the market value. Analysts further explained that such market dynamics reflect a current state of "liquidity constraint, sensitivity to macro-shocks" which is still not achievedTypical Bear City is completely soldLevel。

10x Research, which is more quantitative and structural, provides a more direct conclusion: they believe that Bitcoin is in the early stages of the bear market, with chain indicators, financial flows and market structures showing that the next cycle is not yet over。

In terms of the larger dimension of time, the current uncertainty of bitcoin is no longer a problem of the encrypted market itself, but is embedded in the global macro cycle. Over the next week, many strategists will see the key macro window period at the end of the year – the European Central Bank, the British Central Bank, and the Bank of Japan will publish interest rate resolutions successively, while the United States will be receiving a series of delayed employment and inflation data that will provide a late “realty test” for the market。

At the December 10 conference, the Fed had already sent an unusual signal: not only did it lower 25 basis points, but three negative votes were rare, and Powell was more bluntly likely to overestimate employment growth in the previous months. This week’s intensive macro-data will reshape the market’s core expectations for 2026 – whether the Fed will continue to reduce interest rates or will have to press the pause button for a longer period. This answer may be more important for risk assets than for any single asset multi-space debate。