BitMart VIP Insight: Encrypted Market Review and Hotspot Analysis in March

Markets will continue to compete around inflation, non-farming and policy paths, and encrypted markets, though well-regulated, face macro-political pressures。

TL, DR

- In March, the macro-environment was emptied as a whole: the Fed maintained interest rates and released hawk signals; inflation was adhesive, oil prices went up and employment was weak, and interest rate declines were expected to shift significantly; and the US share was weakened by repeated tariff shocks and geo-risks, and risk assets were under overall pressure. Looking ahead to April, markets will continue to compete around inflation, non-farming and policy paths, and the encryption market, though well-regulated, is still under macro-political pressure。

- In March, trade volumes were “pulse-based + rapid fallback”, with multiple extremes of ups and downs but lack of continuity, indicating that funds were driven mainly by short-lines; and market-wide market values were mildly shaken, peaking at $2.45 trillion to $2.50 trillion, with insufficient overall kinetic energy。

- IN MARCH, BOTH THE BTC AND THE ETH SPOT ETF MOVED FROM NET OUTFLOWS TO NET INFLOWS, WITH ASSET SIZE REBOUNDING AT THE SAME TIME AS PRICES, WITH THE RETURN OF ETH FUNDS AND GREATER PRICE ELASTICITY, REFLECTING A MARGINAL RECOVERY OF RISK TO HIGHLY VOLATILE ASSETS, WHILE THE TOTAL AMOUNT OF THE STABILIZATION CURRENCY SHIFTED FROM CONTRACTION TO MILD EXPANSION, WITH A CLEAR CONCENTRATION TO THE HEAD, INDICATING THAT WHILE THE NEW LIQUIDITY WAS IN THE REFLOW MARKET, THE WHOLE WAS STILL IN THE PHASE OF PRUDENT RECOVERY RATHER THAN FULL-SCALE RISK EXPANSION。

- IN MARCH, THE BTC MAINTAINED AN INTER-ZONE SHOCK OF $62,000 – $74,000, CURRENTLY AT APPROXIMATELY $69,000 – $71,000, WITH THE OVERALL POSITION BETWEEN $65,000 – $67,000 OF SUPPORT AND $72,000 – $75,000 OF RESISTANCE, AND DIRECTIONAL BREAKTHROUGHS STILL NEED TO BE MATCHED BY MACRO-ENVIRONMENT; THE ETH PERFORMANCE WAS RELATIVELY WEAK, MAINLY AT $1,900 – $2,200, AND SHORT-TERM SLOWDOWN OF ETF FUNDS AND FALCON REPRESSION BY FOMC, WITH MORE THAN $2,200 TO BE STABILIZED; THE SOL WAS FIGHTING A FALL, OPERATING BETWEEN $82 – $7,000, CURRENTLY AT $88 – $92, WITH A STRUCTURAL UPSTAPPING PATTERN OF $88 – $92。

- The establishment of a digital asset classification framework jointly by the SEC and the CFTC, the explicit classification of 16 mainstream assets, such as BTC, ETH, as “digital commodities” and the introduction of the “Token Safe Harbor” concept, marked a significant reduction in regulatory uncertainty and provided a key legal basis for institutional entry. At the same time, BlackRock introduced the ETF (ETHB) formula, which distributes pledge proceeds, facilitating the evolution of encrypted ETF from price instruments to revenue assets, but security incidents such as Resolv also highlight the fact that industry risks are shifting from chain loopholes to chain infrastructure and private key management, and that the importance of the security system has increased further。

- In April, which will be a critical window of time for encryption regulation and legislation, if the CLARITY Bill is to make a breakthrough at the committee stage and move forward with the vote, it will work with the SEC/CFTC classification framework to create a complete regulatory closed loop that will significantly enhance the policy certainty of institutional entry; conversely, if progress is blocked, market sentiment may be phased in. At the same time, the upgrading of the Taifung Glamsterdam into the critical testing phase of the ETF ecological expansion is expected to support the medium-term ETH fundamentals and strengthen the long-term logic of institutional involvement in the Etherfam network。

1. Macro perspective

Policy orientation

ON 18 MARCH, THE FEDERAL RESERVE'S SECOND POLICY MEETING FOR THE CURRENT YEAR WAS CONVENED, WITH THE EXPECTED MAINTENANCE OF THE TARGET INTEREST RATE OF THE FEDERAL FUND AT 3.50 PER CENT TO 3.75 PER CENT. THE MOST MARKET-ORIENTED ASPECT OF THE MEETING WAS THE HAWK WORDING OF THE DOT-TAMP MAP AND THE POWELL RELEASE, WHICH SHOWED THAT THE MEDIAN RATE OF THE EXPECTED DECLINE IN 2026 WAS STILL ONE TIME, BUT THAT DIFFERENCES AMONG THE MEMBERS OVER THE PATH OF THE REDUCTION WERE SIGNIFICANTLY WIDENING (SOME MEMBERS WERE NOT EVEN EXPECTED TO DO SO). POWELL HIGHLIGHTED THE NON-LINEAR CHARACTER OF THE INFLATION FALL-OFF PROCESS AND WARNED ABOUT THE RISK OF A SUSTAINED UPWARD TREND IN TARIFFS AND ENERGY PRICES, MAKING CLEAR THAT THE POLICY COMMITTEE WAS NOT EAGER TO ACT AND WOULD REMAIN CAUTIOUS UNTIL INFLATION AND EMPLOYMENT DATA CLEARLY SIGNALED. THE FEDERAL RESERVE INCREASED THE PCE INFLATION PROJECTION FOR 2026 TO APPROXIMATELY 2.7 PER CENT, WHICH WAS HIGHER THAN PREVIOUSLY ANTICIPATED, FURTHER PRESSURING THE MARKET TO SET A FAST RATE DOWN DURING THE YEAR AND PRESSURING RISKY ASSETS, INCLUDING ENCRYPTED ASSETS, IN LATE MARCH。

U.S. stock movement

IN MARCH, THE UNITED STATES STOCK WAS IN A DOWNWARD PATTERN OF SHOCK, WHICH WAS SIGNIFICANTLY WEAKER THAN AT THE BEGINNING OF THE YEAR. IN LATE FEBRUARY, UNITED STATES TRADE POLICY WAS TIGHTENED AGAIN, WITH MARKETS PLAYING AROUND UNCERTAINTY IN TARIFF POLICY AND RISK PREFERENCE FOR PHASING. IN MARCH, GROUND TENSIONS BETWEEN THE UNITED STATES AND IRAN CONTINUED TO RISE, BRENT CRUDE OIL PRICES WERE AT A RATE OF $100 PER BARREL, HIGH IN RECENT YEARS, EMBEDDING EARLY WARNING OF RECESSION FROM MULTIPLE INSTITUTIONS, AND A MARKED DETERIORATION IN MARKET SENTIMENT; IN MID-MARCH, THE LANDMARK 500 PHASE RETREAT, WITH A MARKED REVERSAL FROM THE HEIGHTS EARLIER IN THE YEAR, AND THE VIX PANIC INDEX WENT UP FAST, REFLECTING THE RISK THAT THE AGENCY WOULD CARRY OVER FROM TACTICAL GAINS TO BROADER DEFENSIVE. WHILE THERE HAS BEEN CONTINUED FRAGMENTATION WITHIN THE SCIENCE AND TECHNOLOGY SECTORS, AND AI CALCULATES AGAINST INFRASTRUCTURE DIRECTION, TRADITIONAL SOFTWARE, FINANCIAL TECHNOLOGY, ETC. HAVE BEEN SUBJECT TO REVALUATION PRESSURES AND OVERALL RISK PREMIUMS HAVE REMAINED HIGH。

Inflation data

ON 11 MARCH, THE UNITED STATES BUREAU OF LABOR STATISTICS RELEASED CPI DATA FOR FEBRUARY 2026: CPI INCREASED BY 2.4 PER CENT FROM YEAR TO YEAR, RISING BY 0.3 PER CENT FROM JANUARY; THE CORE CPI (EXCLUDING FOOD AND ENERGY) INCREASED BY 2.5 PER CENT FROM YEAR TO YEAR AND BY 0.2 PER CENT FROM YEAR TO YEAR, IN LINE WITH MARKET EXPECTATIONS. INFLATION DATA AS A WHOLE REMAINED ABOVE THE FEDERAL RESERVE TARGET OF 2 PER CENT BUT DID NOT GO FURTHER. IT IS A MATTER OF CONCERN THAT SERVICES INFLATION REMAINS ADHESIVE, WHILE THE MIDDLE EAST CONFLICT HAS PUSHED OIL PRICES UP RAPIDLY, BRENT OIL PRICES HAVE EXCEEDED $100 AND ENERGY-END INFLATION IS UNDER RENEWED PRESSURE. AS A RESULT, THE FEDERAL RESERVE REVISED INFLATION FORECASTS UPWARDS AT THE FOMC MEETING IN MARCH, RECOGNIZING THAT THE “LAST KILOMETRE” TASK WAS MORE CHALLENGING THAN EXPECTED, AND THAT THE NEED TO MAINTAIN HIGH INTEREST RATES IN THE SHORT TERM HAD INCREASED FURTHER。

Employment data

The February 2026 report on non-farm employment, published by the United States Department of Labor in early March, showed an unexpected reduction of about 90,000 people in non-farm employment, significantly weaker than market expectations, owing to the rare negative growth after the epidemic; unemployment rose to about 4.4 per cent and labour participation fell slightly. The decline in employment was mainly affected by strikes, fluctuations in the public sector and a slowdown in enterprise recruitment. The unexpected weakness of the job market has partly underpinned interest-rate expectations, but the “silent signals” that coexist with the decline in inflation and employment have placed the Fed in a dilemma: interest-rate cuts may fuel inflation, and inaction may exacerbate the economic downturn. Market expectations for the first interest-rate reduction point in the year have moved to a larger proportion in the second half of the year。

Political factors

IN MARCH, MULTIPLE UNCERTAINTIES AT THE POLITICAL AND POLICY LEVELS WERE INTERTWINED AND HAD A SIGNIFICANT IMPACT ON MARKET SENTIMENT. TRADE POLICY IN THE UNITED STATES CONTINUES TO BE REPEATED, AND UNCERTAINTY ABOUT TARIFF EXPECTATIONS IS DISTURBING BUSINESS PROFITABILITY AND SUPPLY CHAINS. AT THE SAME TIME, THE ESCALATION OF THE GEOGRAPHICAL SITUATION IN THE UNITED STATES AND IRAQ POSES THE GREATEST EXTERNAL RISK FOR THE CURRENT PERIOD, WITH OIL PRICES SURPASSING $100 DIRECTLY RAISING INFLATION EXPECTATIONS AND SUPPRESSING CONSUMER CONFIDENCE. IN THE AREA OF ENCRYPTION, DISCUSSIONS ON ASSET CLASSIFICATION AND LEGISLATIVE FRAMEWORKS ARE STILL TAKING PLACE AT THE REGULATORY LEVEL, AND THE MARKET HAS SOME OPTIMISTIC EXPECTATIONS FOR A LONG-TERM COMPLIANCE PROCESS, BUT IN THE SHORT TERM MACRO FACTORS CONTINUE TO DOMINATE PRICING. GOLD PRICES WERE FURTHER HIGH OVER THE PERIOD AND REMAINED CLOSE TO HISTORICAL HEIGHTS, REFLECTING THE CONTINUED STRONG DEMAND FOR RISK AVOIDANCE. OVERALL, GEOHAZARD RISK, TARIFF UNCERTAINTY AND FOMCA ' S POSITION CONSTITUTE TRIPLE PRESSURE, AND THE INFLUENCE OF POLITICAL FACTORS ON ENCRYPTED MARKET SENTIMENT IS GENERALLY NEGATIVE。

Next month's outlook

LOOKING FORWARD TO APRIL, THE MARKET WILL FOCUS ON THE MARCH CPI AND PCE INFLATION DATA AND THE MARCH NON-FARM EMPLOYMENT REPORT, WHICH WILL HAVE A DIRECT IMPACT ON THE FEDERAL RESERVE ' S POLICY JUDGEMENT AT THE MAY FOMC MEETING. IT IS A MATTER OF CONCERN THAT THE “STAGNATING” CONCERN HAS BECOME THE CENTRAL NARRATIVE OF THE MARKET AS A RESULT OF THE FALL IN EMPLOYMENT AND THE $100 OIL PRICE BREAKTHROUGH IN FEBRUARY, AND THAT RISK ASSETS WILL CONTINUE TO BE UNDER PRESSURE IF THE DATA CONTINUE THIS COMBINATION IN MARCH. THE GEOGRAPHICAL SITUATION IN THE UNITED STATES AND IRAQ IS ALSO A KEY VARIABLE FOR APRIL, AND IF THE SITUATION ESCALATES FURTHER, THE UPWARD SPIRAL OF OIL PRICES WILL INCREASE INFLATIONARY VISCOSITY AND INCREASE MARKET VOLATILITY. IN ADDITION, THE TERM OF THE FEDERAL RESERVE CHAIRMAN POWELL WILL EXPIRE IN MAY 2026, AND THE UNCERTAINTY OF SUCCESSORS WILL GRADUALLY BECOME THE FOCUS OF MARKET ATTENTION. IN TERMS OF ENCRYPTED ASSETS, THE REGULATORY LEGISLATIVE PROCESS (E.G. THE CLARITY ACT ADVANCES THE RHYTHM) AND THE BTC CASH ETF FLOWS REMAIN THE CORE OBSERVATION VARIABLE, AND THE ABILITY OF THE BTC TO SECURE CRITICAL SUPPORT AREAS AND MAINTAIN NET INFLOWS WILL DETERMINE THE COURSE OF THE NEXT PHASE。

Overview of the encryption market

Analysis of currency data

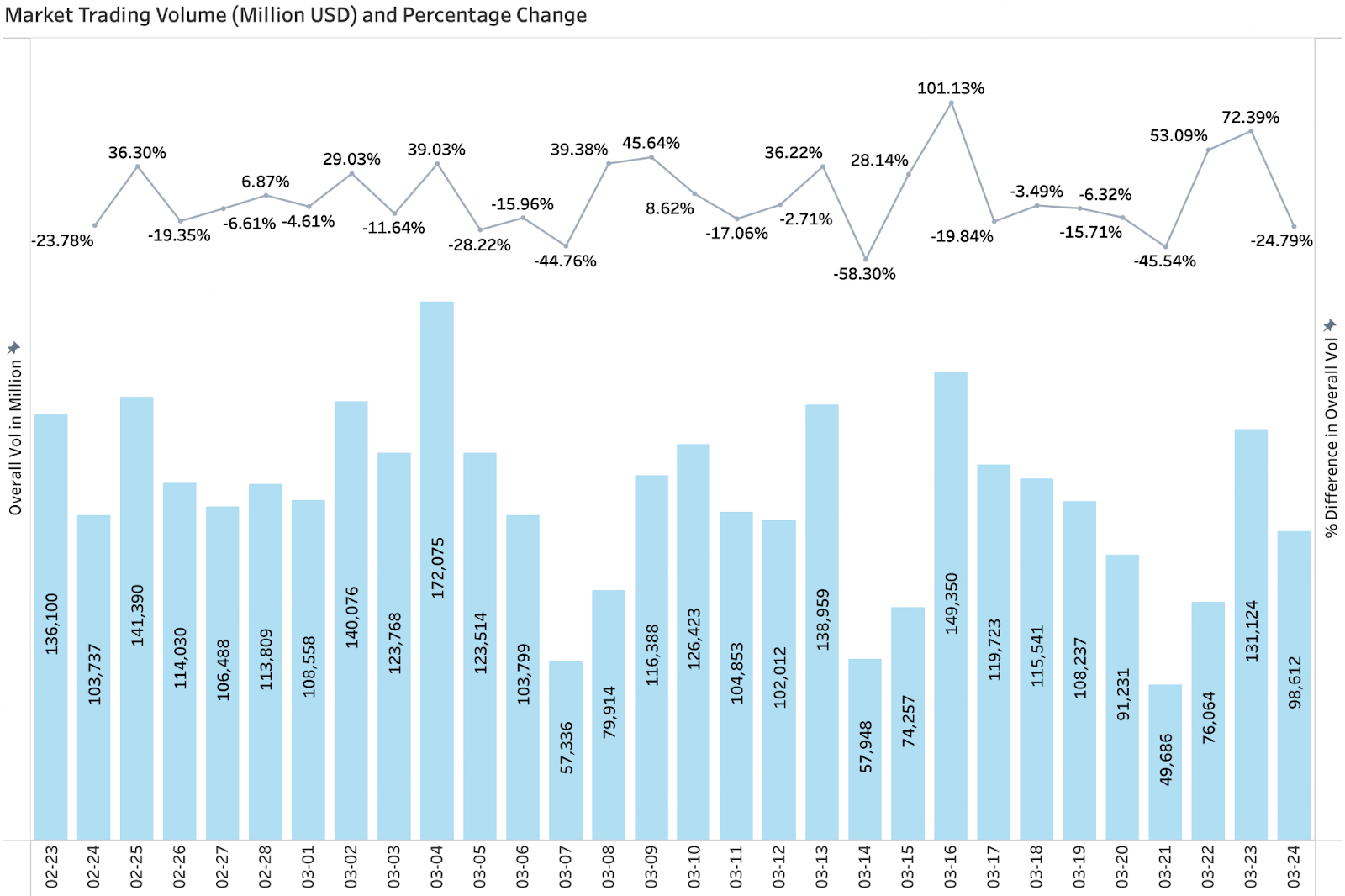

volume of transactions & daily growth rate

According to CoinGecko, the overall market turnover in March was marked by “pulse discharge + rapid fall”, with a significantly higher volatility than in February. The turnover from the beginning of the month to 4 March was rapidly amplified to a stage high (about $170 billion volume) and then fell rapidly; in mid-March, driven by market moods and events, it was again released, rising by 101 per cent a day on 16 March, but it remained insufficient for continuity and then re-entering the contraction zone. At the rhythm level, the turnover is highly concentrated on short-term emotional catalyzing or event shock windows (e.g., market volatility amplification or chain/security incident disturbances), while the remainder of the period is traded at a low and medium level, reflecting the fact that funds are mainly driven by short-line games and transactions, and that medium- and long-term incremental funding is still lacking. The turnover was further weakened later in the year, accompanied by a number of significant negative growth (e.g. -45 per cent, -24 per cent) and a marginal decline in market activity. Overall, while there was a stronger explosion in March than at a local point in February, there was a lack of continuity in volume, the market still did not have a steady trend towards release and the structural and event-driven dynamics continued to dominate。

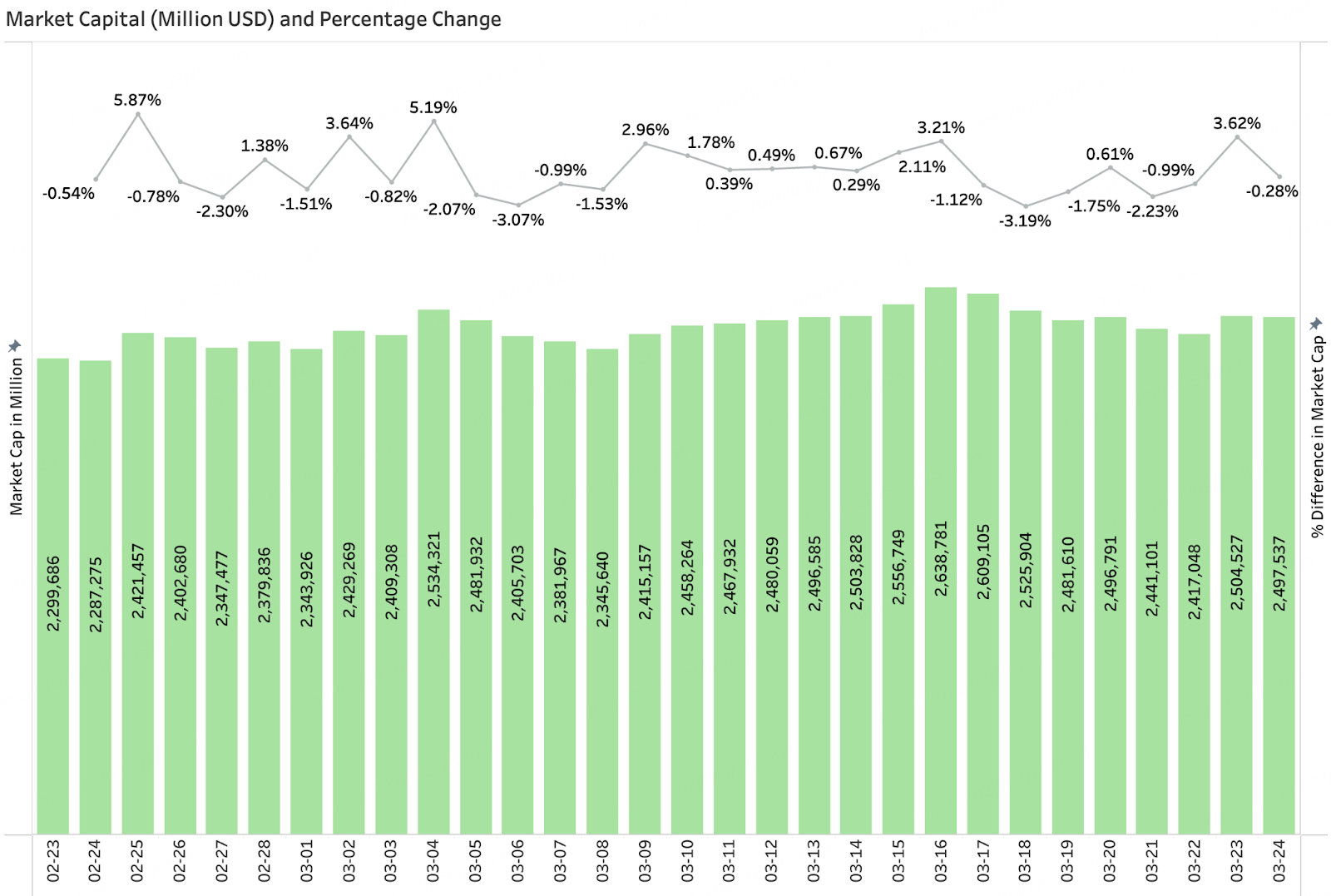

market value for full market & daily growth

According to CoinGecko, the total market value of the encrypted market in March presented an overall structure of “sliding back and forth after a shock”. At the beginning of the month, after a shock near the market value of approximately $2.3 trillion, it was gradually repaired and reached a phase high (approximately $263 trillion) in mid-March, during which the daily increase was relatively moderate, with most fluctuations remaining within ±3 per cent, indicating that the market had been rehabilitated but remained cautious. The March market value was more stable than in February, with no extreme single-day large withdrawals, reflecting a gradual mitigation of systemic risks. However, the market value fell again after the mid-term runoff, with recurrent shocks between $2.45 trillion and $2.50 trillion, reducing growth dynamics. Overall, the current market is in the post-rehabilitation stage of platform consolidation, the trend is weak, the funding risk preferences are still in the process of being repaired, and the follow-on trends will still depend on improved macro-liquidity, sustained inflows of ETF funds and further policy catalysts。

3 Data analysis on the chain

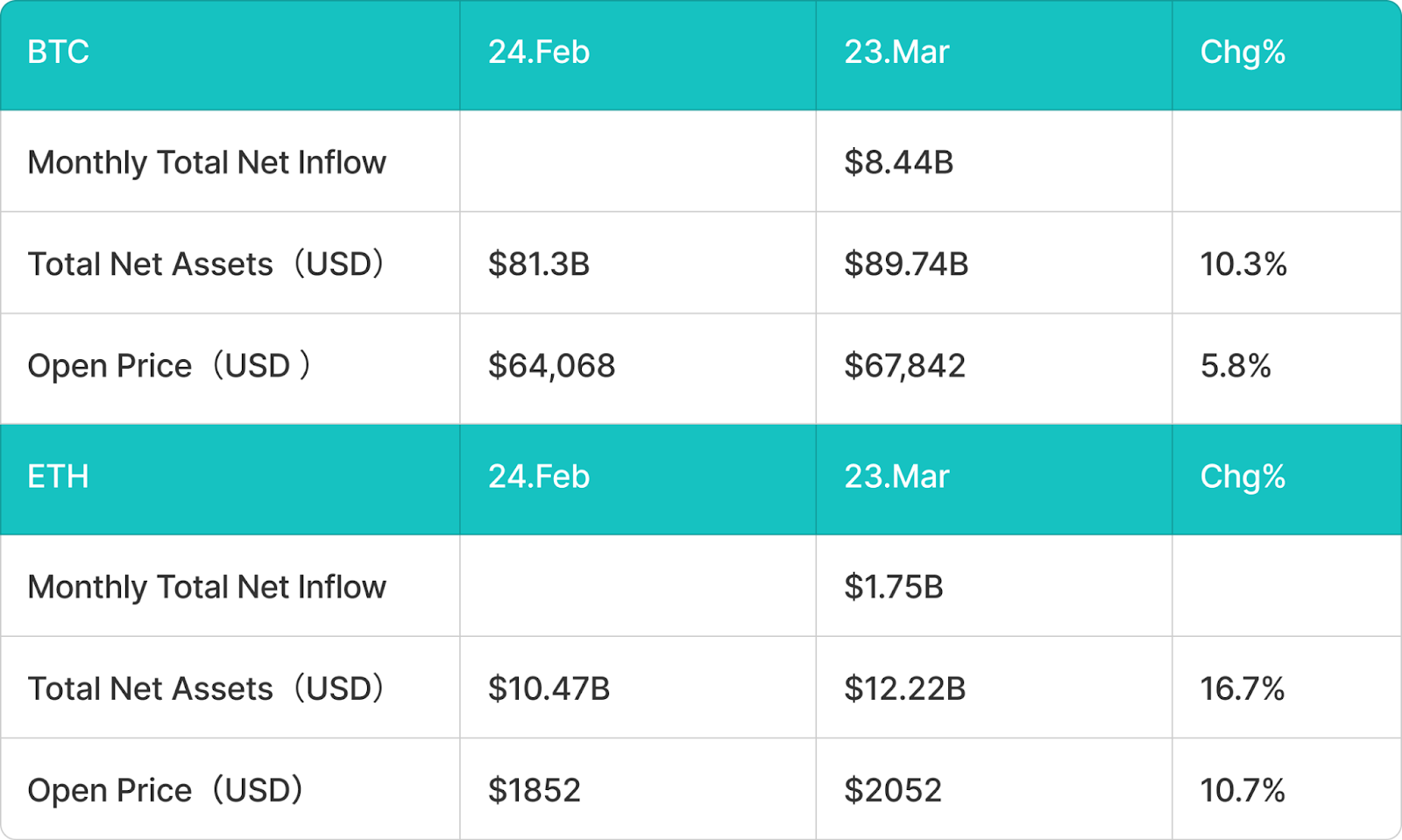

BTC, ETH ETF INFLOW AND EXIT ANALYSIS

IN MARCH, THE REAL BTC ETF BECAME SIGNIFICANTLY STRONGER, PRESENTING A TURNING POINT FROM NET OUTFLOWS TO NET INFLOWS. THIS MONTH, THE BTC SPOT ETF ACHIEVED A NET INFLOW OF APPROXIMATELY $8.44 BILLION, WITH TOTAL NET ASSETS RISING FROM APPROXIMATELY $81.3 BILLION ON 24 FEBRUARY TO $89,740 MILLION, AN INCREASE OF APPROXIMATELY 10.3 PER CENT IN THE RING. IN TERMS OF PRICES, THE BTC INCREASED FROM APPROXIMATELY $64,068 AT THE BEGINNING OF THE MONTH TO $67,842, AN INCREASE OF ABOUT 5.8 PER CENT. OVERALL, THERE WAS POSITIVE FEEDBACK FROM THE RE-INFLOW OF ETF FUNDS AND THE UPTURN IN PRICES, INDICATING THAT INSTITUTIONAL FINANCIAL RISK PREFERENCES HAD BEEN CORRECTED. COMPARED TO THE CONCENTRATION IN FEBRUARY, MARCH WAS MORE LIKE A PHASED RE-CONFIGURATION PROCESS, WHICH, ON THE ONE HAND, REDUCED THE RISK ASSET PRESSURE BY AN IMPROVEMENT IN THE MACRO-LIQUIDITY MARGIN, AND, ON THE OTHER HAND, LED TO A VALUATION APPEAL BY THE BTC FOLLOWING A SIGNIFICANT UPTURN IN THE PRECEDING PERIOD, WHICH LED TO THE RE-ESTABLISHMENT OF INSTITUTIONAL OPENINGS, THUS PRESENTING THE RESTORATION FEATURE OF “FINANCIAL RETURN PLUS PRICE STABILITY”。

IN MARCH, THERE WAS ALSO A MARKED IMPROVEMENT IN THE ETH SPOT ETF, WHICH SHIFTED FROM OUTFLOWS TO INFLOWS. THE NET INFLOWS OF ETH SPOT ETF THIS MONTH WERE ABOUT $1.75 BILLION, WITH TOTAL NET ASSETS INCREASING FROM APPROXIMATELY $10.47 BILLION TO $12.22 BILLION, AN INCREASE OF 16.7 PER CENT IN THE RING. THE ETH PRICE ROSE FROM $1,852 TO $2,052, AN INCREASE OF ABOUT 10.7 PER CENT. IN TERMS OF PERFORMANCE, BOTH ETH ' S FINANCIAL RETURN AND PRICE ELASTICITY WERE HIGHER THAN THE BTC, REFLECTING A GREATER TENDENCY FOR FUNDS TO COMPENSATE FOR VOLATILE ASSETS DURING THE RISK MARGIN RECOVERY PHASE. THE FACT THAT ETH WAS THE PRIORITY TARGET FOR RECOVERY IN MARCH, AS A PRIORITY FOR REPOSITIONED ASSETS IN FEBRUARY, BUT ITS OVERALL SIZE HAS STILL NOT BEEN RESTORED TO A HIGH LEVEL IN THE PRECEDING PERIOD, SUGGESTS THAT THE AGENCY IS NOW MORE TACTICAL IN NATURE AND REMAINS CAUTIOUS ABOUT ITS MEDIUM- AND LONG-TERM CONFIGURATION。

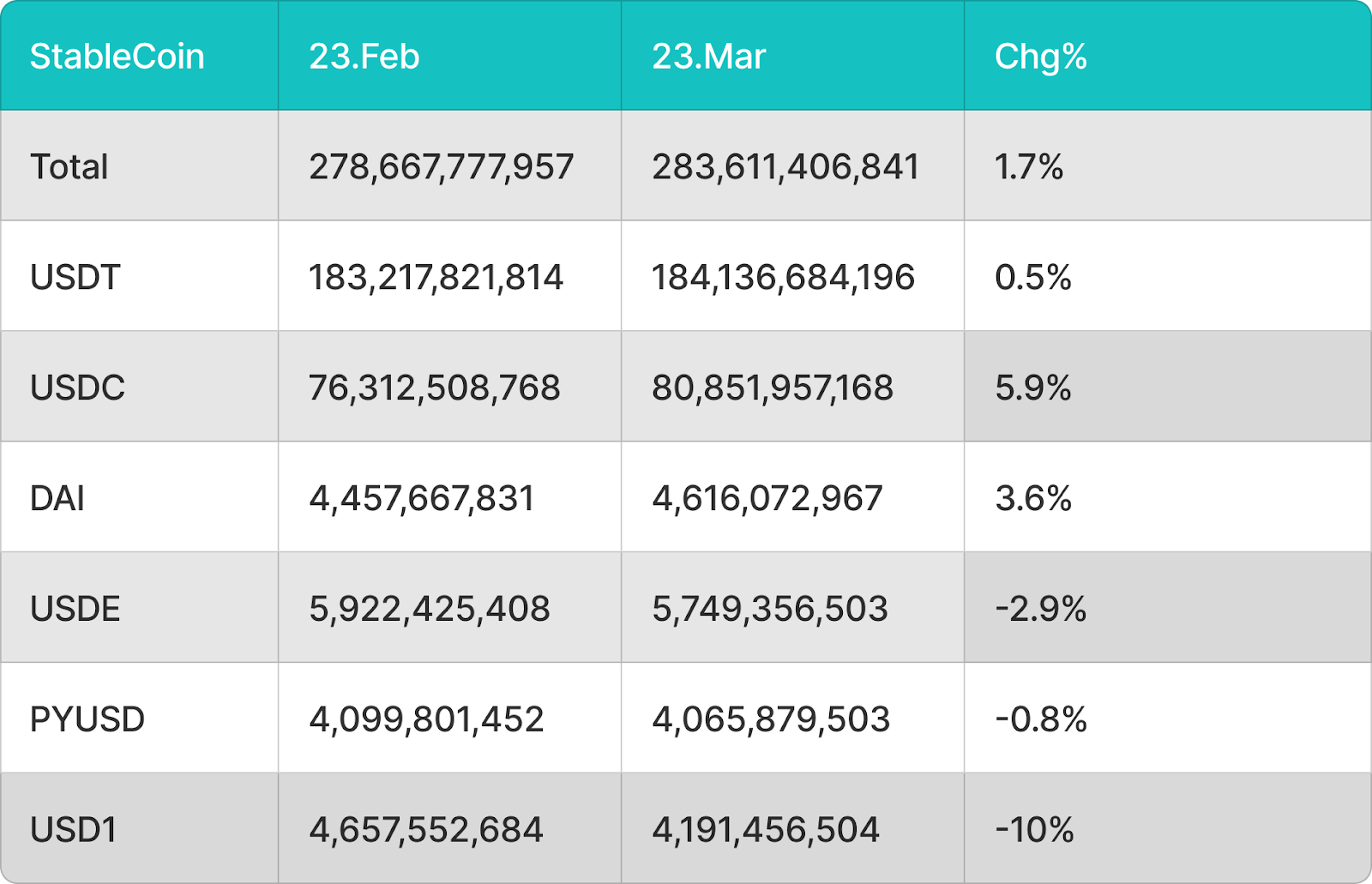

Analysis of inflows and outflows of stable currencies

IN TERMS OF CURRENCY STABILIZATION, OVERALL LIQUIDITY ROSE FROM APPROXIMATELY $27,868 MILLION TO $28,3611 MILLION IN MARCH, AN INCREASE OF ABOUT 1.7 PER CENT IN THE RING, FROM A SLIGHT CONTRACTION IN FEBRUARY TO A MODERATE EXPANSION, INDICATING A MARGINAL IMPROVEMENT IN MARKET LIQUIDITY. STRUCTURALLY, THE USDT GREW SLIGHTLY BY ABOUT 0.5 PER CENT, CONTINUING TO MAINTAIN ITS DOMINANT POSITION; THE GROWTH OF USDC BY ABOUT 5.9 PER CENT WAS MOST SIGNIFICANT, REFLECTING THE PREFERENCE FOR A COMPLIANCE-STABILIZED CURRENCY DURING THE RETURN PERIOD; AND THE GROWTH OF DAI BY ABOUT 3.6 PER CENT WAS RELATIVELY ROBUST. THE DECLINE IN USDE, PYUSD AND USD1 WAS ABOUT 2.9 PER CENT, 0.8 PER CENT AND 10 PER CENT, RESPECTIVELY, WITH THE MOST SIGNIFICANT CONTRACTIONS IN USD1, INDICATING A CONTINUING STRAIN ON DEMAND FOR NON-MAINSTREAM OR SPECIFIC ECO-STABILITY CURRENCIES. OVERALL, THE EXPANSION OF THE STABLE CURRENCY HAS BEEN ACCOMPANIED BY A MARKED CONCENTRATION OF FUNDS IN THE HEAD AND FURTHER STRUCTURAL FRAGMENTATION。

OVERALL, IN MARCH, THE MARKET WAS CHARACTERIZED BY REHABILITATION: BOTH THE BTC AND THE ETH SPOT ETF MOVED FROM NET OUTFLOWS TO NET INFLOWS, WITH THE SIZE OF THE ASSETS REBOUNDING AT THE SAME TIME AS PRICES; AND THE TOTAL AMOUNT OF STABILIZATION CURRENCY MOVED FROM CONTRACTION TO EXPANSION TO VALIDATE THE RE-ENTRY OF ADDITIONAL FUNDS. HOWEVER, STRUCTURALLY, FUNDING IS STILL CONCENTRATED ON MAINSTREAM ASSETS AND MAINSTREAM STABILIZATION CURRENCIES, INDICATING THAT IT IS STILL IN A RISK-BASED, CAUTIOUS RECOVERY PHASE, CLOSER TO A PHASE-BY-STAGE RECOVERY DRIVEN BY THE REPLENISHMENT, RATHER THAN A GENERAL UPWARD TREND。

Price analysis of mainstream currencies

BITCOIN (BTC) PRICE ANALYSIS

IN MARCH, THE PRICE OF BITCOIN WAS $62,000 PER $74,000 WIDE-BANDED. ON 25 FEBRUARY, AFTER A FIVE-WEEK NET OUTFLOW AND A QUICK REBOUND TO ABOUT $69,000, THE BTC ENTERED THE INTER-COORDINATION PHASE, WITH THE MAIN RESISTANCE CONCENTRATED ON $72,000 – $75,000, WITH REPEATED CONTACT DURING THE MONTH OF THE FAILED BREAKTHROUGH. KEY SUPPORT BELOW IS CONCENTRATED IN 65,000-$67,000 ZONES, WHICH WERE QUICKLY REPAIRED AFTER A SHORT TEST OF $63,000-$64,000 IN THE COURSE OF THE MONTH. ON 18 MARCH, AFTER THE DECLARATION OF THE FOMC EAGLE FACTION, THE BTC DROPPED BY ABOUT 5 PER CENT A DAY, RETESTING $67,000 TO $68,000 FOR SUPPORT, AND AS OF 27 MARCH IT WAS REPORTED AT APPROXIMATELY $69,000 TO $71,000, WHICH WAS STILL OPERATING IN THE INTERIOR. AN EFFECTIVE BREAKTHROUGH OF $74,000 AND STEADYNESS ABOVE IS EXPECTED TO OPEN UP TO $78,000 – $82,000; A FURTHER $60,000 – $62,000 MEDIUM-TERM SUPPORT IS POSSIBLE IF $65,000 IS MISSED BELOW. OVERALL, BITCOIN IS CURRENTLY IN AN INTER-TEMPORAL SHOCK PATTERN, MAINLY SUPPORTED BY $65,000-$67,000 AND $72,000-$75,000 FOR IMMEDIATE RESISTANCE, WITH DIRECTIONAL BREAKTHROUGH SIGNALS REQUIRING MACRO-ENVIRONMENT IMPROVEMENT。

ANALYSIS OF ETH PRICES

IN MARCH, THE SHOCK PATTERN WAS CONTINUED AT THE FARE PRICE, WITH OVERALL PERFORMANCE WEAKER THAN THE BITCOIN. ETH RETURNED TO THE AREA AT THE END OF FEBRUARY, APPROXIMATELY $2,050 AND ENTERED THE AREA TO SORT IT OUT, MAINLY AT $1,900 – $2,200, WHICH WAS REPORTED AS AT 27 MARCH. KEY RESISTANCE ABOVE IS CONCENTRATED IN THE FIRST INSTANCE IN SECTORS OF $2,250 – $2,350, WHICH CORRESPONDS TO SHORT-TERM DYNAMIC AVERAGES AND PRE-INTENSITY CLOSED AREAS, PREVENTING PRICES FROM GOING UP SEVERAL TIMES. THE FOLLOWING $1,900-$2,000 IS AN IMPORTANT SUPPORT AREA, AND IF THE CODE FAILS, IT MAY FURTHER EXPLORE THE KEY MEDIUM-TERM SUPPORT OF $1,700-$1,800. FOLLOWING THE FOMC EAGLE SIGNAL ON 18 MARCH, THE ETH SHORT-TERM PRESSURE SLOWED DOWN THE ETF PHASE AND FURTHER SUPPRESSED THE REACTIONARY ENERGY. GRADUAL STEP-UP OF OVER $2,200 WOULD BE AN IMPORTANT OBSERVATION INDICATOR TO JUDGE WHETHER TRENDS COULD BE CHANGED FROM WEAK TO WEAK, WHILE THE SHORT-TERM TECHNICAL SIDE REMAINED NEUTRAL。

Solana (SOL) price analysis

In March, Solana ' s overall performance was relatively stable, operating within the 82-$97 zone, showing some resilience vis-à-vis BTC and ETH. As at 27 March, SOL reported $88–$92, a small shock compared to the end of February. Short-term support is concentrated mainly in the 82-$85 zone, which has played a bottom-up role on several occasions in the recent past; the 95-$97 above is a critical resistance zone, corresponding to the high point of the mid-March period, and breakthroughs require strong trade-offs. If SOL can effectively stand above $90 and set a maximum of $97, it is expected to open up the repair path to $100-$105; otherwise, if $82 is missed, further medium-term support in the vicinity of $75-$78 may be explored. Overall, SOL remains highly volatile, and until macro-risk preferences improve, prices may continue to seek directional breakthroughs within the $82–$97 zone

This month's hotspot events

THE SEC/CFTC JOINTLY ISSUED AN EXPLANATION FOR THE CLASSIFICATION OF ENCRYPTED ASSETS AND 16 ASSETS WERE OFFICIALLY IDENTIFIED AS "DIGITAL GOODS"

On 17 March, the United States Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly published a 68-page encrypted asset classification interpretation document formally establishing a systematic regulatory classification framework for the digital asset market. The document identifies 16 mainstream encrypted assets of BTC, ETH, SOL, XRP, Cardano, Chainlink, Avalanche, Polkadot, Stellar, Hedera, Litecoin, Dogecoin, Shiba Inu, Tezos, Bitcoin Cash, Aptos, as "digital commodities", subject to the control of the CTC, which are clearly not securities. The overall framework divides digital assets into five categories: digital goods, digital collections, digital tools, stable currencies and digital securities, and only digital securities (i.e., tokenized versions of traditional financial instruments) continue to be subject to the full coverage of the SEC。

The joint classification explained that the market was seen as one of the most important regulatory breakthroughs in the encryption industry. In the same address, the Chairman of the SEC, Paul Atkins, announced the concept of a safe harbour clause for Token Safe Harbor, which would provide interim compliance protection space for agreements that had not yet been centralized. Following the release of the news, there was a positive response from mainstream encrypted assets, institutional compliance quickly reassessed the configuration of digital assets, and asset management companies indicated that they would expedite the integration of the BTC, ETH, SOL portfolio. There is a general consensus among analysts that this two-agency joint operation ended years of regulatory ambiguity and removed the core legal barriers to the next round of institutional entry。

BlackRock launched the ETF (ETHB) and the spot ETF entered the revenue age

On March 12, BlackRock, the world ' s largest asset management company, officially listed in NASDAQ as iShares Staked Etheum Trust ETF (ETHB), became the United States ' first spot ETF to distribute to investors the proceeds of the Taifung pledge. The product was opened with seed assets of approximately $107 million, with a first-day trade volume of about $15.5 million, and was listed with a chain pledge of approximately 80 per cent of the holdable ETH and a target pledge of between 70 and 95 per cent. With regard to the distribution of proceeds, ETHB allocated about 82 per cent of the pledge incentive to the holder on a monthly basis, at a rate of 0.25 per cent (with the initial $2.5 billion in size of 0.12 per cent on a temporary basis), with both ETH price openings and chain gains. The key difference with the traditional spot ETH ETF (e.g. ETHA under BlackRock) is that ETHB is the "revenue ETF" that will be introduced for the first time into the traditional fund structure for compliance with the PoS pledge mechanism of the Taifung。

The approved listing of ETHB is a direct product of the United States encrypted regulatory environment shift. Previously, the former Chairman of SEC, Gensler, had requested that all applications submitted for ETF to be removed from the pledge function; the current Chairman, the SEC, under the leadership of Paul Atkins, had approved the ETHB pledge structure without objection, while the entry into force of the GENIUS Act had cleared the compliance barrier for revenue-type encryption products. At the market impact level, the introduction of ETHB marked a shift in the United States-based digital encryption ETF paradigm from a "sole price tool" to a "revenue generation tool", directly competing with traditional income assets such as bonds, REITs, etc. The analysts pointed out that the rapid expansion of the ETHB would provide sustainable collateral demand support for the Taifeng network and promote more asset management companies to follow up on applications for similar products and open up new entry points for institutional involvement in the ecology of the Taifung。

Resolv Labs was attacked with private keys and there were frequent security incidents in the encrypted market

On 22 March, a serious security incident occurred in Resolv Labs, the Decentralized Gains Stability Pact. By invading its cloud infrastructure, the attackers obtained the privileged private key of hosting AWS KMS, thus bypassing the normal casting mechanism, illegally embroiling some 80 million USRs with very low collateral, and encumbering about $25 million in a short period of time through the Curve Mobility Pool, resulting in a sharp fall in the USR price from US$ 1 to US$ 0.025 within 17 minutes. The incident did not stem from a chain of smart contractual loopholes, but rather from a failure of chain key management and infrastructure security, highlighting the significant risk of centralizing the core private key in a single cloud service environment。

From a broader perspective, the Resolv incident is not an isolated case. Recent security incidents, including the resurgence of attacks against Solv Protocol, have shown that the pattern of attacks in the encryption industry is undergoing a structural shift: traditional smart contract loopholes have declined, while “Web2 attack vectors” such as private key leaks, cloud service intrusions and social engineering have become the mainstream, accounting for more than 76 per cent of stolen funding sources. In combination with historical-level losses amounting to approximately $17 billion in 2025 and the trend towards the frequency of large-scale events, the industry has entered a new phase of “under-chain security decision cap”, and the DeFi agreement has to raise key management of multiple signatures, hardware security modules and the overall operating security system to the same level as a chain audit。

Next month's outlook

THE CLARITY ACT LEGISLATES FOR A KEY WINDOW IN APRIL OR THROUGHOUT THE YEAR

April will be the decisive point for the CLARITY Bill to land in 2026. The Galaxy Digital research department has made it clear that if the bill fails to complete the Commission's proceedings by April, the probability of its adoption within the year will be "very low"; the core dispute of the bill is whether the stable currency can pay market interest — the banking sector advocates strict restrictions on passive earnings, while the encryption industry seeks to preserve the space for compliance gains. On 10 March, the Senator announced a compromise negotiation on this provision, and Minister of Finance Bessent sent a signal that stabilization currency legislation was expected to be signed into law in the spring of 2026. If the April negotiations succeed and the plenary vote is advanced, together with the joint SEC/CFTC classification of 17 March, they will constitute a complete closed circle of the historic breakthrough of the current round of encrypted regulation, providing unprecedented policy certainty for the institutional configuration. If the pace of legislation lags behind again, the "alternate replacement" effect will be a gradual suppression of market sentiment。

Speed up the upgrading process of the Taifung Glamsterdam and pledge ETF ecological acceleration

The upgrade of the Taifung Glamsterdam was listed by the Foundation as a core priority in the first half of 2026, with the target window entering the critical phase of testing network validation in about June and April. The core objectives of the upgrade, which is the largest technological hierarchic in size since "The Merge" was to raise each block of Gas from a ceiling of 60 million to 200 million, to target 10,000 TPS (approximately 10 times the current level), to reduce the cost of complex smart contracts by about 78.6 per cent, and to introduce parallel transaction processing and chain block construction mechanisms to significantly optimize the MEV structure. If the core EIP of the testing network advances smoothly in April, it will significantly strengthen the medium-term ecological expectations of the ETH and underpin the relatively weak prices of the ETH in the near future. At the ETF level, following the listing of ETHB, applications for similar products from Franklin Templeton, Grayscale and others will enter the SEC audit window, and in April there may be a follow-up to the approval of products, further expansion of the ecological dimension and market impact of the ETF pledge and the provision of sustained collateral demand support for the Taifaf network。

Powell's term of office has been replaced by Walsh, and monetary policy continuity is in doubt

The term of office of Federal Reserve Chairman Jerome Powell will officially expire on 15 May 2026. On 30 January, Trump nominated Kevin Walsh, former member of the United States Federal Reserve, to take over, and if the Senate confirmation process is successfully completed, Walsh will take office in May. This handover will enter the final political game window in April, with the Senate confirming that the voting nodes and wording will be interpreted at a high market level。

WALSH'S POLICY POSITION IS A DOUBLE-EDGED SWORD FOR THE ENCRYPTION MARKET. HIS HISTORY HAS BEEN LABELLED AS "HAWKS", ADVOCATING FOR REAL INTEREST RATES TO BE RAISED AND FOR THE FED'S BALANCE SHEET TO BE REDUCED, A POSITION THAT, IF IMPLEMENTED AT THE POLICY LEVEL, WOULD SILENCE RISKY ASSETS SUCH AS BITCOIN; BUT HIS RECENT STATEMENTS HAVE BEEN SOFTENED, CITING AI-DRIVEN PRODUCTIVITY INCREASES WOULD LEAD TO STRUCTURAL DEFLATION, PROVIDING SPACE FOR INTEREST-RATE REDUCTIONS, IN LINE WITH TRUMP'S LOW INTEREST RATE CLAIMS. WITH REGARD TO THE ATTITUDE OF ENCRYPTED ASSETS, WALSH’S POSITION WAS SOMEWHAT CONTRADICTORY: HE HAD PUBLICLY DESCRIBED ENCRYPTED MONEY AS A “SOFTWARE DISGUISED AS A CURRENCY,” CHARACTERIZING THE RISE OF THE BTC AS A “SPECULATIVE BUBBLE” OF LOOSE MONETARY POLICY; ON THE OTHER HAND, HE HIMSELF HAD AN INVESTMENT RECORD OF A ENCRYPTED START-UP COMPANY THAT SUPPORTED CENTRAL BANK INVOLVEMENT IN THE DIGITAL CURRENCY AREA, WHICH WAS GENERALLY ASSESSED BY ANALYSTS AS “PRACTICAL RATHER THAN HOSTILE.”。

FOR THE ENCRYPTED MARKET, POWELL'S DEPARTURE ITSELF REMOVED A KNOWN POLICY ANCHOR, WHILE WALSH REPRESENTED A LARGER UNCERTAINTY PREMIUM. IF WALSH'S SIGNAL OF A DOVE RELEASED DURING THE APRIL HEARING IS CONFIRMED, THE MARKET MAY BE ABLE TO PRE-PRICING THE INTEREST RATE REDUCTION EXPECTED IN THE SECOND HALF OF 2026, WHICH WILL BOOST THE ENCRYPTED ASSETS; IF ITS HAWK STANCE IS REINFORCED, THE CURRENT INFLATIONARY VISCOSITY AND OIL PRICE PRESSURE WILL DOUBLE-REPRESS RISK PREFERENCES. THIS PERSONNEL VARIABLE, WHICH PARALLELS THE LEGISLATIVE WINDOW AND MACRO-DATA OF THE CLARITY ACT, CONSTITUTES ONE OF THE THREE CORE OBSERVATIONS OF THE APRIL ENCRYPTION MARKET。