IOSG: Has the stable currency under the Red Sea been underestimated when it rose in silence

Tether earns a lot of money from the Grey Zone, while the compliance Circe builds the financial moat in a spirit of indignity。

Original title: Does the IOSG Weekly Brief rise silently and stabilize under the Red Sea Circle be underestimated

Original by Frank, IOSG Ventures

Circle vs Tether: 2026, full war

On December 12, 2025, Circe obtained conditional approval from the United States Monetary Supervisory Authority (OCC) for the establishment of the National Trust Bank, the First National Digital Bank. Once fully approved, this key milestone will provide trusted digital asset hosting services to the top global institutions, helping to stabilize the market value of the currency to accelerate to $1.2 trillion over three years. As a result of this momentum, Circe was successfully listed in 2025, together with the acceleration of the flow of USDC, making it the most stable issuer with which institutional investors are linked. To date, its valuation has reached $23 billion。

IOSG Ventures

Téther, the leader of the stable currency market, continues to maintain a high profitability of more than $13 billion, but his parent company faces persistent business credibility and regulatory pressures, such as the recent move by S&P to downgrade Tether’s reserve rating from “strength” to “weak” and the rejection of its acquisition offer by the Yuventus Football Club. On 29 November, the People ' s Bank of China convened a special conference to combat virtual currency transactions, in which it made clear that there were deficiencies in customer identification and anti-money-laundering, and that money-laundering, fraud and irregular cross-border transfers were often used, and that the focus of regulation was essentially on the offshore stabilization currency system represented by USDT. USDT is dominant in emerging markets such as Asia, Latin America and Africa, especially in East Asia, where it accounts for more than 90 per cent, with large flows occurring under the chain of P2Ps and cross-border finance activities, long out of the regulatory system, which is seen as a “grey dollar system” that increases the risk of capital flight and financial crime。

This post is part of our special coverage Syria Protests 2011

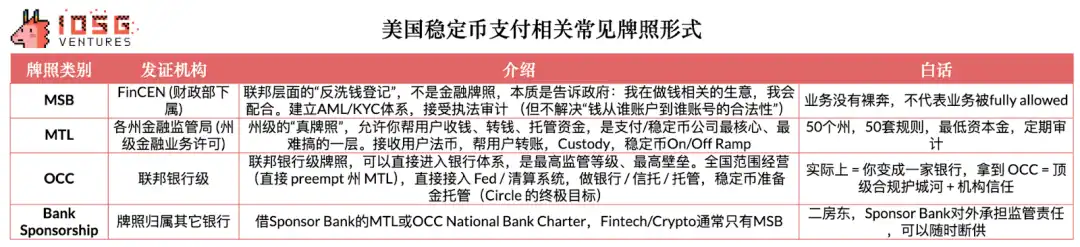

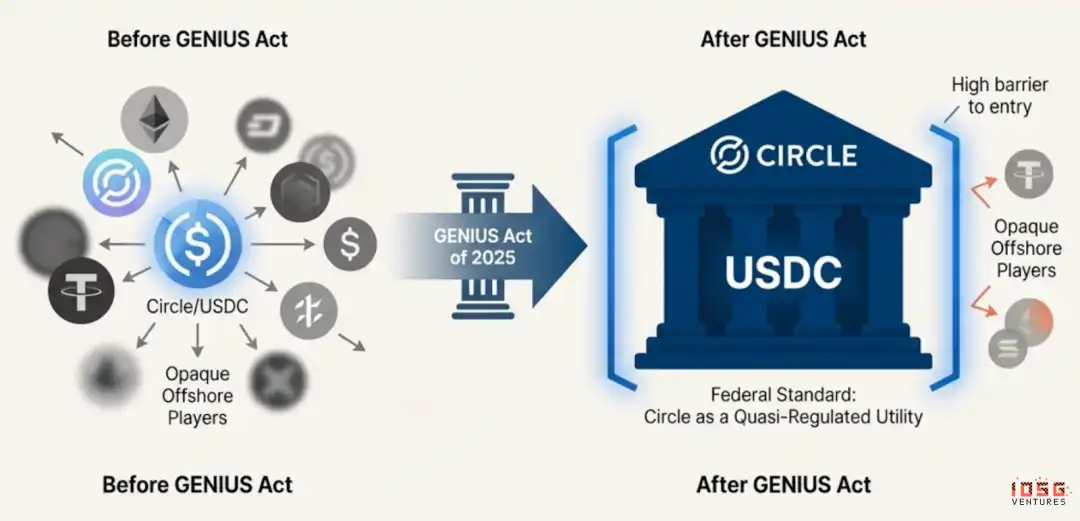

By contrast, the path taken by the United States and the European Union is not a total blow, but rather a high degree of compliance to bring the currency into the regulatory system. In the United States, for example, GENIUS Act explicitly requires that a stable currency must have a 1:1 high-quality reserve, monthly audit, federal or state licence, and prohibits the use of high-risk assets such as bitcoin, gold, etc. as reserves。

In other words, China wants to compress the "shadow dollar system of offshore stable currency" from the source, while Europe and the United States are trying to establish "controlled, compliant, and supervised digital dollar systems". Common to both paths is the reluctance to allow non-transparent, high-risk, unauditable stabilization currencies to take a systemic position. This means that compliance issuers such as Circle will have access to the financial system, and offshore stable currencies such as Tether will be gradually excluded from developed markets in the future. And that's why Tether recently began to develop its USAT, its first U.S. compliance stabilizer。

It's not like you're going anywhere

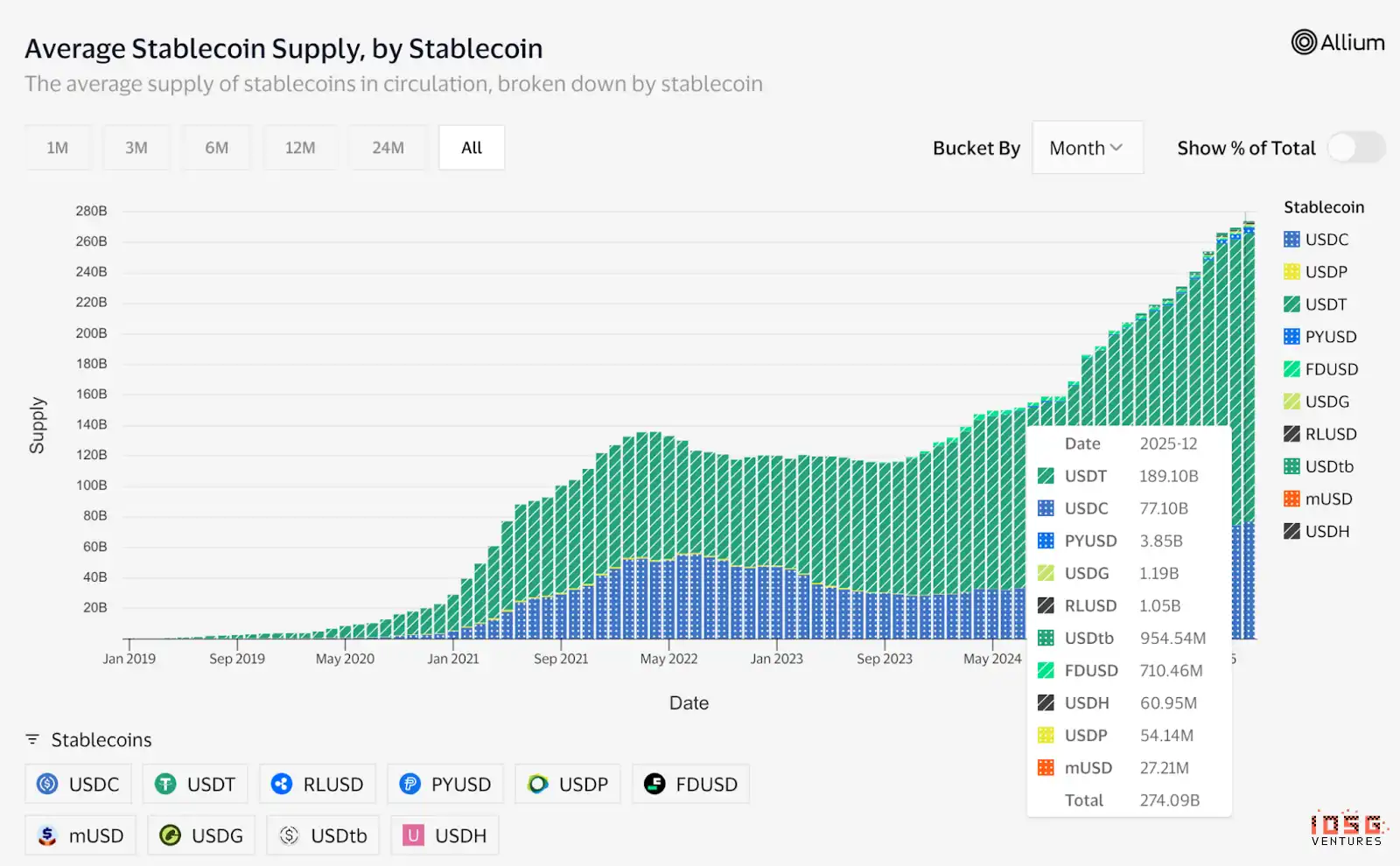

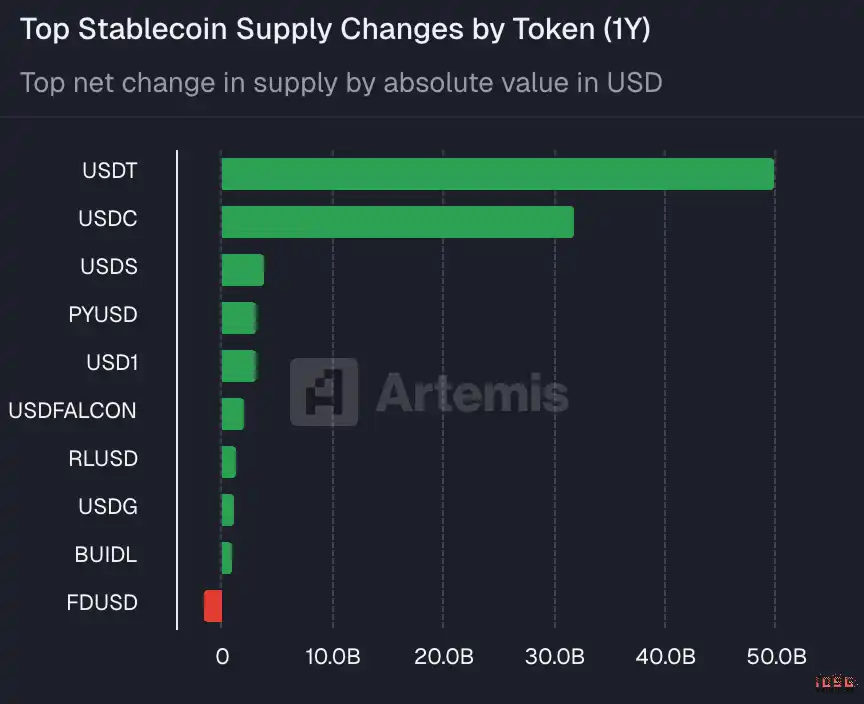

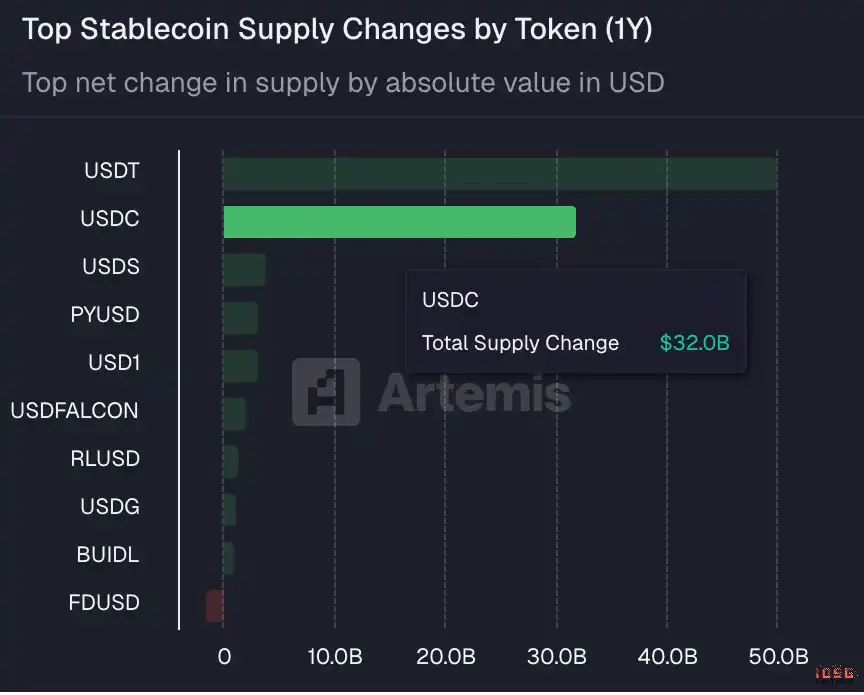

While Tether may remain dominant in offshore and emerging markets, over the past year, Circe's USDCNET SUPPLY ALSO INCREASED BY $32 BILLION, JUST $50 BILLION FROM THE USDSTI don't know。

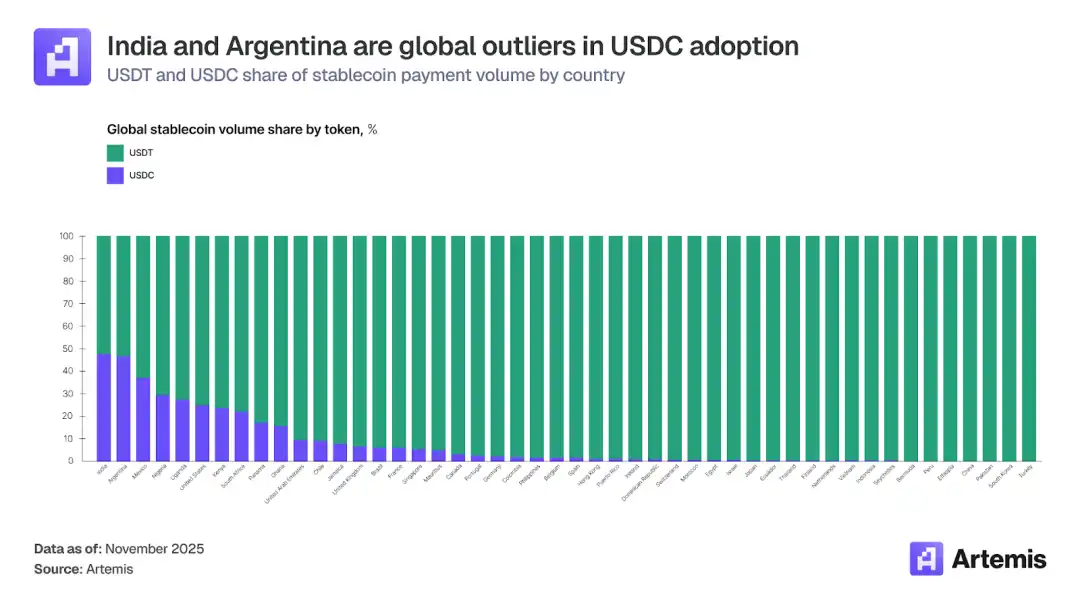

However, there has also been significant progress on the challenges of the offshore and emerging markets for Tether, with market shares reaching 48 per cent and 46.6 per cent in India and Argentina. The main reason for the increase in the position of the USDC in the offshore markets is due to the growth of encryption card operations over the past few years。

It's not like you're going anywhere

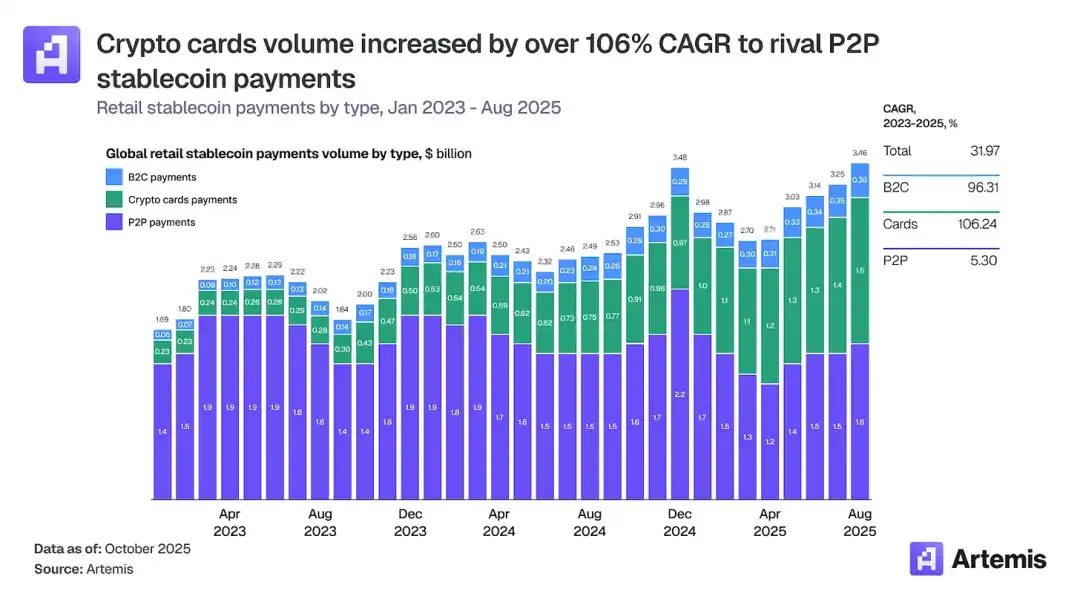

Encryption cards, which enable users to consume in traditional businesses using stable currency and encrypted currency balances, have become one of the fastest growing sub-markets in the area of digital payments. The volume of transactions increased from about $100 million per month at the beginning of 2023 to over $1.5 billion at the end of 2025, with a compound annual growth rate of 106 per cent. By year, the size of the market now exceeds $18 billion, which is no less than a point-to-point stable currency transfer ($19 billion) that grew by only 5 per cent over the same period。

It's not like you're going anywhere

The opportunity to stabilize the cards is not just a surprise but rather a solution to real demand in many offshore markets. In India, there are still many users who do not have access to credit through traditional banks, and encrypted currency-backed credit cards address this demand. At the same time, the Argentine population faced severe inflation and currency devaluation. Stabilized currency debit cards help people to preserve their value by holding assets linked to the United States dollar。

Because of the need to access the Visa or Mastercard network and thus transfer transactions to local businesses, USDC has logically become the most appropriate compliance and stabilization currency, thus obtaining a significant share of transactions in these stable offshore areas and countries。So we can also see that Circle and Tether are increasing competition in areas where they are good at each other, and it's hard to say who's in the short term。

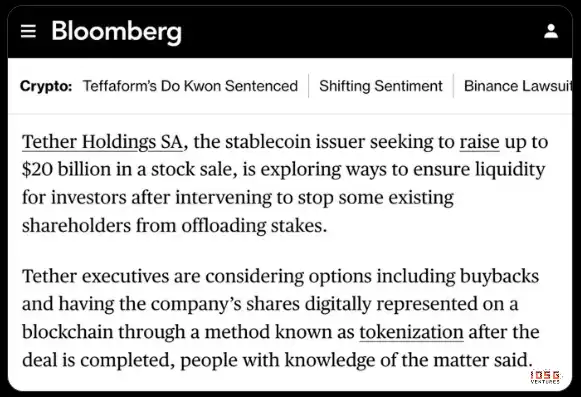

Of course, if the two are completely off the scale, USDT’s OTC Participation reaches 300B, along with Bloomberg’s news report, which recently made up $20 billion in its $500 billion valuation. And Circe's latest market price is 18.5 billion。

You're not going anywhere

The premium of this Tether valuation, in addition to its monopolistic position in the market, has many other factors, but the overriding factor is the advantage of the Tether business model, which does not need to be as subservient to Coinbase as it is to Circle. According to the Circle S-1 file, the USDC held on its platform could receive 100 per cent of the reserve income. For USDC outside its own platform, for example, USDC, which is stored on other trading platforms, DeFi agreements or individual wallets, the interest income generated is split 50-50 by Circe and Coinbase。

- I'm sorry

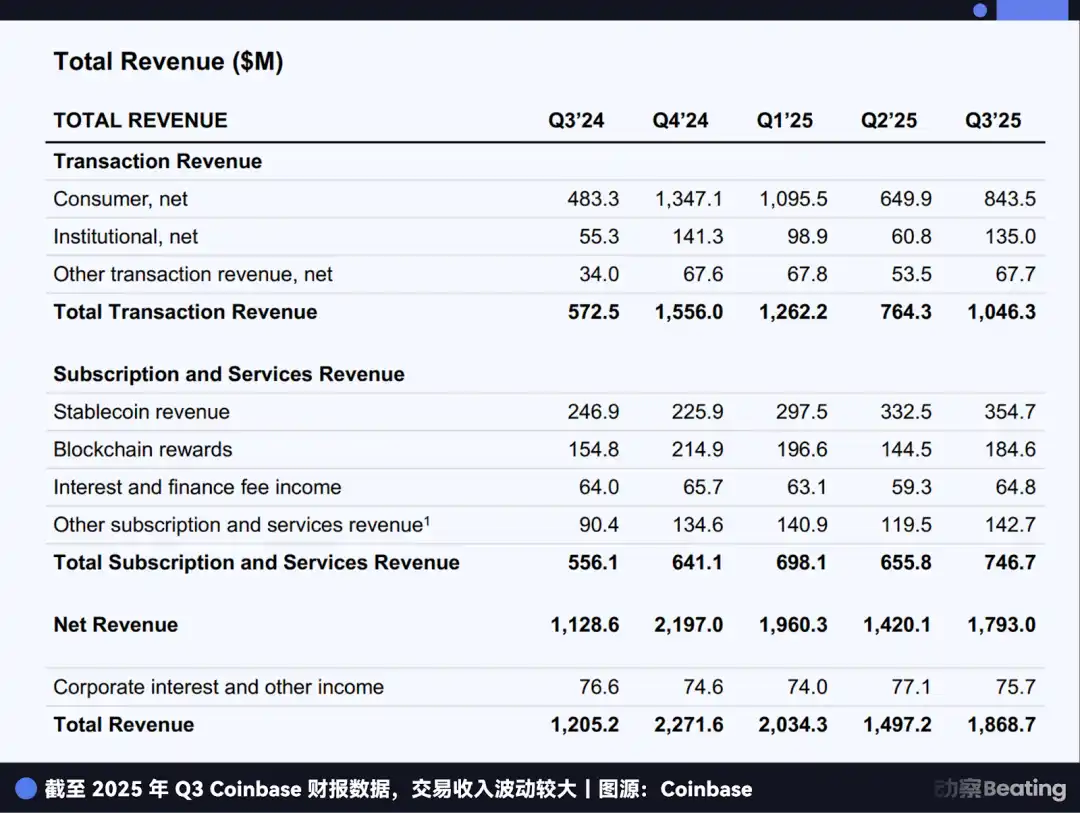

In 2025, Q3 Coinbase 's income amounted to 354.7M, 50 per cent of the interest income of Circle itself for the same period. In other words, every $2 interest that Circe earns is given to Coinbase。

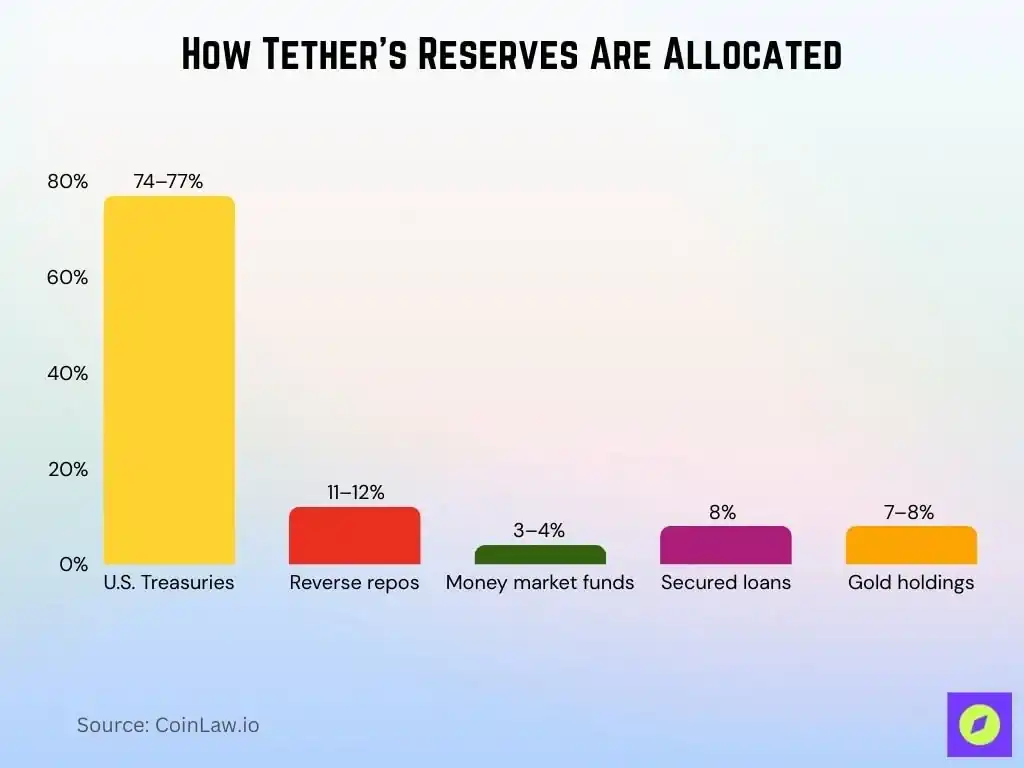

Besides the lack of differentiation, Tether's USDT has a huge advantage in not following collateral limits. If that is the extreme "conservative strategy" of the stock: 85 per cent are short-term dollar debts and overnight reverse purchase agreements of up to 90 days' duration, 15 per cent are cash and equivalents, all of which are held in the custody of Belet or BNY, and monthly audit reports are issued by the accounting firm Grant Thornton LLP, which covers and can be verified in real time by 1:1 of the turnover and reserves。

Source: CoinLaw

By contrast, we can see that the USDT collateral is more diversified than that of Circle, and thus has higher reserves, especially in the context of the spread of market evasive sentiment, and in the context of rising gold prices。

This is a question of whether the compliance and stability currency itself would be a good business, if it were to follow the "high compliance plus regulation white list" path

Circe financial report: total growth Q3

First of all, we can look back at the fact that Circe as the main money model and collection for a stable currency company. The Circle Stabilization Currency is 1:1 and is made of cash and short-term United States Treasury bonds, which can generate significant interest income in an environment of high interest rates。

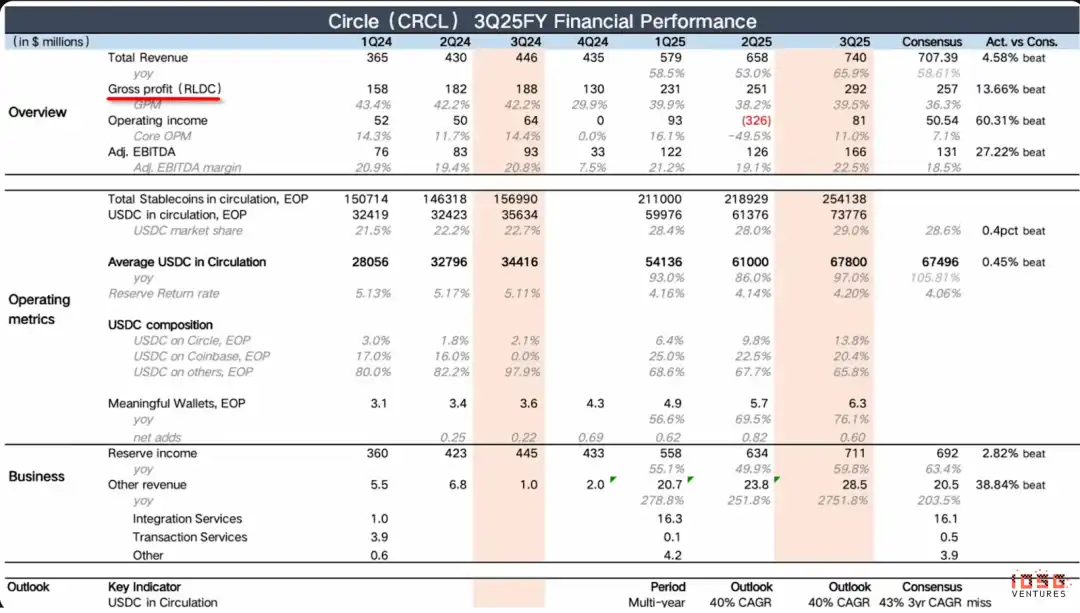

In the third quarter of this year, the income of Circle reached $740 M (of which interest income alone generated $711 M), defeating the 707M expectation that YoY (as compared to the previous year) would increase by 66 per cent, although the growth rate of MOM (as compared to the previous quarter, 13.6 per cent, fell slightly to 12.5 per cent overall。

The nearly doubling of flows by USDC and the 22.5 per cent profit margin of Adjusted EBITDA have resulted in a rare combination of growth and profitability, leading it to emerge in the area of financial science and technology as a model for a small number of industries with high growth and high profits。

Queen 3 Earthings

The company ' s total quarterly profit (RLDC) reached $292M this quarter, significantly exceeding market expectations and at a similar rate to the previous two quarters. RLDC (Renewue Less Distribution and Other Costs) is calculated as the total amount of profits received after deduction of distribution, trading and other related costs. The RLDC profit margin (RLDC Margin) is the RLDC as a percentage of total revenue and is used to measure profitability of core business。

In the same vein, the market expectations were defeated significantly, while the previous quarter was negative, mainly because of one-time equity incentives, SBC (staff remuneration) of 424M and Debt Extinguishment Charles of 167M (cost of early debt repayment). Thus, for more ease of comparison, we use Adjusted EBITDA, which is non-core, such as depreciation, amortization, taxes and equity incentives, plus one-time costs to reflect the recurring performance of the main operation. In terms of Adjusted EBITDA's performance, the year-to-year and ring-to-year increases were 78 per cent, 78 per cent and 31 per cent, and the market's expectations were significantly defeated。

As we can see, the core source of revenue for Circe is interest on reserve assets. However, this pattern is very fragile and can be directly affected by macro-interest rates. So the biggest challenge for Circe is to reverse a single fragile stable currency harvest in a short period of time and open up diversified revenue channels。

Circle Q3 Earnings

So, here's the thing about the growth of other incomes, and..Increase in the share of other income in overall revenue as long as these two continue to growAnd that means that Circle's collection pattern has been improving, but if these two rates are falling, it'll be a relative signal。

Other revenues can be seen to be 28.5M, which significantly exceeds market expectations. However, given that the base figure for the same period last year was only $1 million, the comparison is of limited interest. More meaningful ring data show that the rate of increase in this quarter is 20 per cent, up from 15 per cent in the previous quarter, indicating that the income block is actually growing rapidly. However, “other income” still accounts for less than 4 per cent of total revenue, and it will take some time to change the single income structure of Circle。

Nevertheless, it remains a positive signal。It is unrealistic to expect a fundamental shift in the revenue model to be completed in just half a year, and the current robust ring growth has provided a good start to future diversification。

Queen 3 Earthings

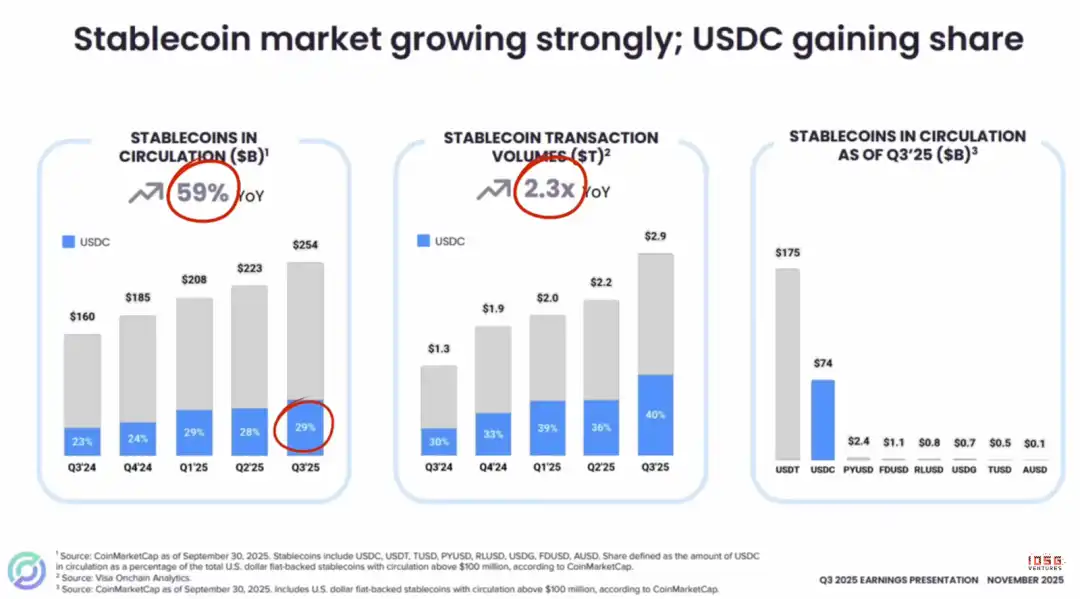

At a more macro level, stable currency markets are experiencing high growth, with overall liquidity increasing by 59 per cent over the same period, and chain transactions, which were 2.3 times higher than in the same period last year, indicating significant market potential。

In this context, the performance of the USDC has been particularly remarkable, with its market share steadily rising to 29 per cent. It is worth noting that the upward trend in USDC has not been interrupted even in the near future when it faces competition for emerging stable currencies such as Phantom $CASH。

There is a general concern in the current market that, as more and more stable currencies are issued, will the market make USDC no longer the best stable currency option? From the platform of "stabilizing currency issuance as service" (e.g. from Bridge to M0 to Agora) to the influx of a large number of firms, these phenomena seem to presage excessive competition in the industry (inner volume), thereby eroding long-term profitability. However, this view largely ignores a key market reality。

The increase in the market share of USDC is largely due to the favourable environment created by regulatory progress such as the Genius Act. As the leader of the compliance stabilization currency, Circle occupies a unique strategic high ground. On a global scale, whether in the United States, Europe, Asia or the United Arab Emirates and Hong Kong, where stable currencies are already regulated, mainstream institutions tend to have a trust, transparency and liquidity compliance infrastructure such as Circle as their preferred partner, otherwise their operations will be difficult to implement。

WE THEREFORE FIND IT DIFFICULT TO ESTABLISH OUR CONCERN THAT EMERGING STABLE CURRENCIES IN THE MARKET MAY CHALLENGE THE POSITION OF THE USDC MARKET. ON THE CONTRARYNOT ONLY HAS USDC BEEN ABLE TO SECURE ITS SECOND PLACE FOR A LONG TIME, BUT IT HAS BEEN BETTER ABLE TO USE ITS UNPARALLELED COMPLIANCE ADVANTAGE TO LAUNCH A SHOCK AT THE TOP OF THE MARKET, WITH A NETWORK-SCALE EFFECT BARRIER LIKELY TO REACH 2-3 YEARS。

Queen 3 Earthings

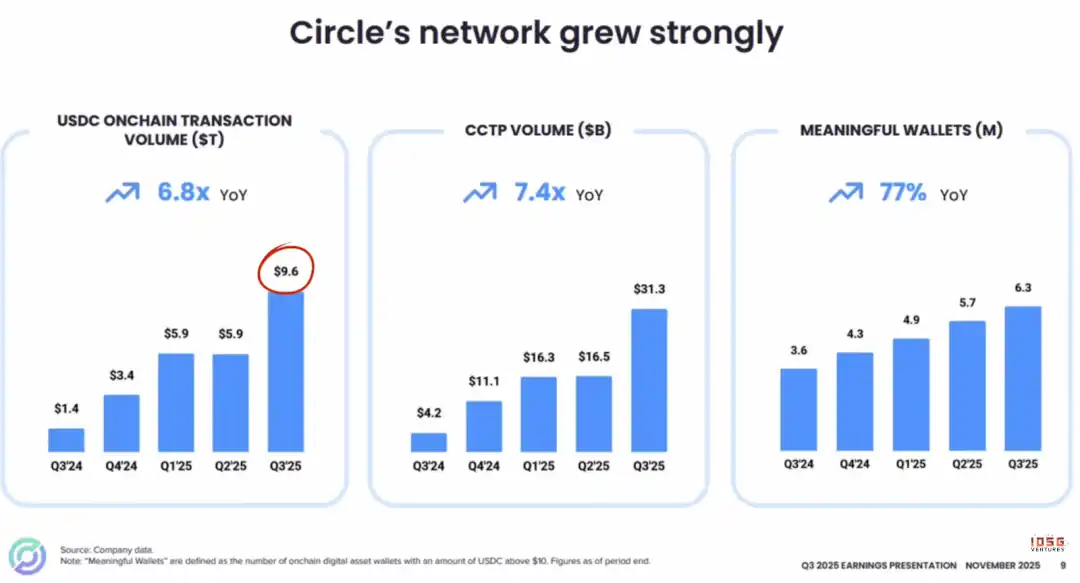

USDC IS EXPERIENCING EXPLOSIVE GROWTH IN CHAIN ACTIVITY. THE CHAIN OF TRANSACTIONS HAS SOARED TO $9.6 TRILLION, 6.8 TIMES THE SAME PERIOD LAST YEAR。

THIS INCREASE WAS DUE TO THE SUCCESS OF ITS TRANS-CYBER TRANSFER PROTOCOL (CCTP). BY DESTROYING IT IN THE SOURCE CHAIN AND CASTING IT IN THE TARGET CHAIN, THE CCTP ACHIEVED A SEAMLESS AND UNIFORM FLOW OF USDC BETWEEN THE DIFFERENT BLOCK CHAINS, AVOIDING THE COMPLEXITY AND RISKS OF TRADITIONAL CROSS-CHAIN BRIDGES。

TAKEN TOGETHER, ALL INDICATORS CLEARLY POINT TO THE SAME CONCLUSION, WHETHER THE NUMBER OF CHAIN TRANSACTIONS, THE USE OF DATA BY THE CCTP OR THE INCREASE IN THE NUMBER OF VALID WALLETS (WITH A BALANCE GREATER THAN $10):THE RATE OF ADOPTION AND NETWORK SPEED OF USDC IS EXPANDING CONTINUOUSLY AND SIGNIFICANTLYI don't know。

I'm sorry

In the area of ecological cooperation, Visa announced on December 16 its opening of USDC stabilization currency clearing services to the United States network, allowing users of United States financial institutions (Cross River Bank and Lead Bank as the first users) to settle with Visa through the Solana block chain。

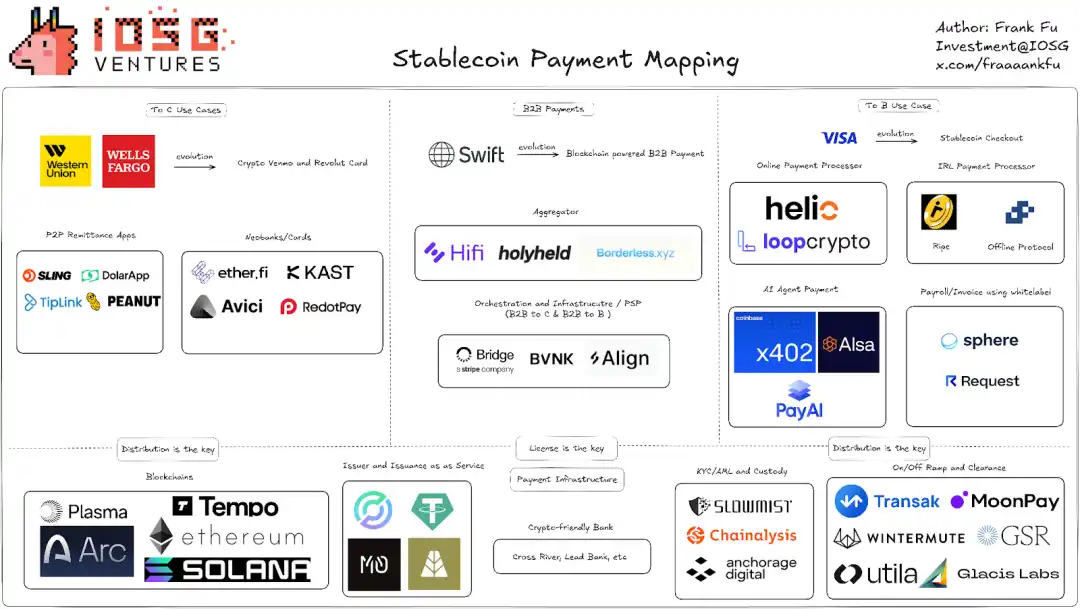

• A friend of B2B Payment Landscape will know that Cross River Bank and Lead Bank are among the United States-owned banks, one of the most friendly banks for encrypted currency in the United States, such as Cross River Bank and Lead Bank, as Sponsor Bank, supporting Baanx and Bridge, respectively, so that Finnech, who has no bank license plates, can "borrow" Their qualifications for issuing bank cards, and even for issuing white-marked bank cards, provide access to traditional payment networks such as the Visa/Mastercard Prince Membership network, which uses traditional payment channels such as VisaNet, MasterCardNet and ACH, FedWire, and RTP for monetary settlement purposes。

IOSG Ventures

The purpose of this cooperation is to increase the speed and liquidity of financial flows by converting all settlement transactions of the Visa card into USDC, without altering the experience of consumer brushes, by allowing banks and financial technology companies to settle seven days a week, replacing the traditional five-day window. In the past, while Visa has been able to authorize transactions in 150 million businesses around the world 24/7, settlements were still limited to bank hours, wire transfer deadlines and holiday arrangements. Bank holidays are authorized on Friday and settlement is not due until Tuesday。

For Visa, stabilization currency and block chains can be a new strategic entry rather than a threat for Visa. Visa's logic is simple: it's a big push on Stablecoin-linked Visa cards. For, regardless of the way in which payments are made, the consumer eventually buys or converts a stable currency into a French currency, which has to be liquidated through VisaNet’s network and then settled between banks。

At present, most of the encrypted currency cards are traded throughFrench settlement24/5 settlement remains the default option because it does not require commercial integration. The transfer of encrypted currency to the French currency is completed before settlement to the payment network, so that, when the transaction reaches the network, the transaction from the encrypted currency card is no different from the transaction from any other card payment, i.e., from the perspective of the merchant’s clearing house, it is all French currency, except that the advantage lies in the user’s entry to the end, i.e. to spend crypto and not rely on SWIFT。

It's not like you're going anywhere

Even if Visa had started the USDC settlement pilot and achieved a 24/7 settlement, it would not be a threat to Visa, but would be in its strategic interest. Access to stable currencies does not change the business logic at the bottom。All stabilization card transactions still have to go through VisaNet and pay "passage fees". Visa's core profit model is based on three main sources of revenue: an exchange fee (Interchange Fee) from the issuing bank, a billing service fee from the receiving bank and a network clearing fee from VisaNet. As a result, there was no need for Visa to issue its own stabilization currency. Its strategy is clear: it continues to access more stable coins (e.g. Bridge, Rain, Reap), supports more stable currencies (e.g. USDC, EURC, USDG, PYUSD) and connects more block chains (Ethereum, Solana, Stellar, Avalanche)。

There is only one goal: to get more traffic through their own networks. Visa's moat lies in its control of the commercial entrance. Regardless of how the transaction occurs on the chain, the "last mile" of French currency is always tied to VisaNet, the "one-wood bridge", and Visa is therefore firmly in control of the right to pay for the road. As at 30 November, the monthly transaction volume of the Visa stabilization currency settlement pilot operation had reached the milestone of annualization of $3.5 billion, an increase of approximately 460 per cent over the same period。

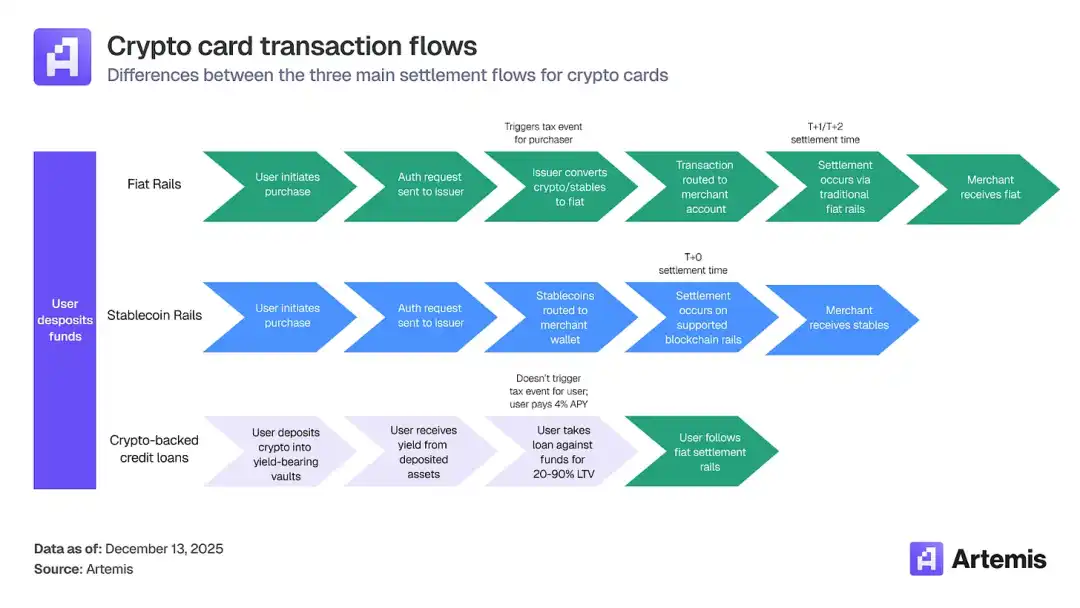

:: Traditional processes: brushing cards → VisaNet authorizes → VisaNet to liquidate → interbank settlements (T+1~T+3, via the banking system)

:: Stable currency settlement process: brush cards VisaNet authorized liquidation of VisaNet clearing USDC settlement (real time, chain)

• But if Visa does not participate: user → stable currency wallet · business takes USDC → Visa directly through ·

For Circle, this cooperation consolidated its institutional endorsement as the top compliance and stability currency and opened up an important channel for it from encrypted original users to traditional financial institutions. However, due to the extremely high liquidity and short sedimentation periods of such settlements, the contribution to the interest income of Circle in the short term has been negligible. According to Didier's estimates, the resulting “work stock balance” represents only about 0.09% of the current USDC total distribution。

Thus, the short-term value of this cooperation lies in the “painting of pipelines” and its long-term potential depends on a significant increase in future financial flows through the pipeline, thus generating more substantial revenue for Circe. In short, Circle & nbsp; is "friending" around to expand the use of USDC. At the end of the transactional asset, we also see USDC access to both Kraken, Fireblocks and Hyperliquid, which are trading platforms for retail, institutional and chain users. At the same time, companies are accelerating their cooperation with the banking infrastructure and the retail end of the digital dollar。Together, these initiatives have enhanced the network effect and application landscape of Circe, laying a solid foundation for the transformation of its future income model。

Queen 3 Earthings

Strategic transition 2026: from "bunk" to "ecological"

Ours: Circle's 2025 Year in Review

In the analysis of the financial statements, we have mentioned that the delay of Circle is to expand other revenues, as well as a brief reference to the CCTP. From the strategic layout published by Circle 2026, we can see clearly how it works。

Of these, I personally believe that the categories of other income most promisingly promoted in the relatively short term are these:

• Transactional services: This includes casting/foreclosure fees, large transfer charges, etc. To understand the potential of this part of the revenue, we need to see the macro-data behind it: this year, USDC's stable currency network has reached a staggering $4.6 trillion total. Through Circle Mint, a large-scale USDC casting and foreclosure service was provided to trading platforms and institutions, with a transaction fee of 0.1 to 0.3 per cent, and the operation ' s revenue of Q3 in 2025 amounted to $3.2 million. Of these, self-researched CCTP Cross-chain and Technical Services has supported the seamless transfer of USDC across 23 public chains, charging 0.05 per cent of the cross-chain amount and contributing income of US$ 2.8 million in 2025。

• The RWA Derbyization Service, which collects 0.25 per cent of its annual management fee through the acquisition of the National Treasury Debt Fund (USYC) launched by Hashnote, is currently managed on a scale of US$ 1.540 billion. When it first acquired in January last year, over 97 per cent of the USYC National Monetary Debt Funds were purchased and held by Usual Protocol as its reserve asset for USD0 stabilization, but after the acquisition, Circle is introducing USYC into more trading platforms, such as distribution channels, to enhance its role as a compliance-living asset。

One of the most remarkable recent developments is Deribit access USYC. Deribit, the leading encryption derivative trading platform, has now supported USYC as a full-ware guarantee for trading futures and options。

This integration has multiple advantages:

• Mortgages can generate gains while safeguarding trading space

• Lower opportunity costs than the use of non-revenue stable currencies

:: The value added of collateral may reduce overall transaction costs

:: Maintain liquidity and be available for extraction whenever required

For active traders, this means that your "free" transaction funds can continue to generate revenue for you, even as a guarantee. This is not possible under the traditional bond model。

If one looks at the longer term, the most promising category of additional income for the longer term is that of Circle:

First, Circe built its own Arc public chain: ARC public testing network is now online, and more than 100 businesses around the world are participating in testing, many of them well-known and large. Management expects that the main network will be officially online in 2026. All participants in the developers ' ecology have seamless access to the infrastructure, while the public chain will be further integrated with the platforms under the Circe flag. In addition, management is actively exploring the possibility of introducing an ARC original token。

Queen 3 Earthings

Its central significance is:

Vertical integration: trade media (USDC)+ channel (Coinbase, Visa)+ clearing layer (ARC public chain)

2. Value capture: In the past, USDC ran on the Ether, Solana, and Gas, MEV, and ecological values were taken away from other public chains; ARC allowed Circle to take back those values

You're not going anywhere

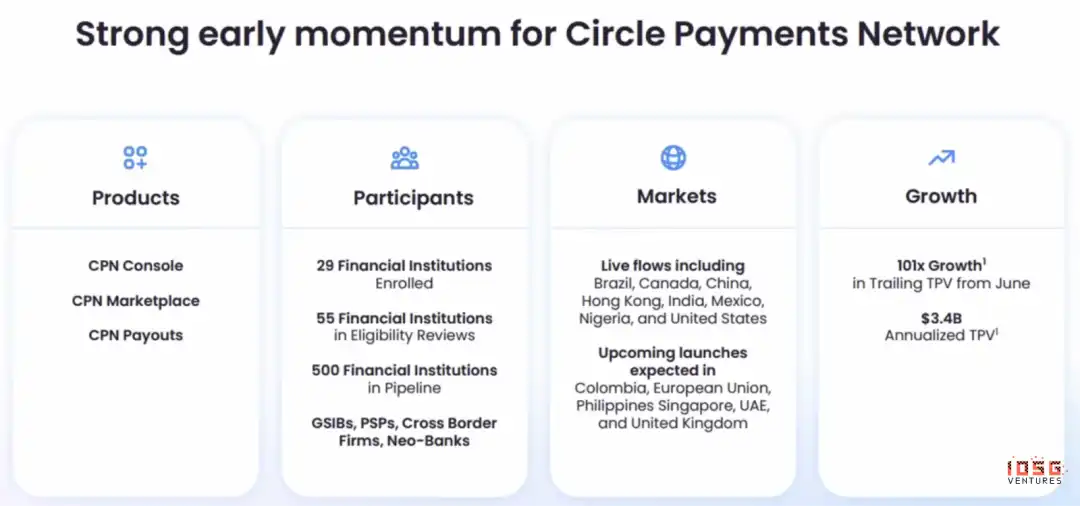

Second, CPN (Circle Payments Network), an agency-oriented B2B payment network that provides USDC-based cross-border payment and settlement services to large enterprises and financial institutions。

If ARC is the bottom operating system, then CPN is the top level application. Three major products have been launched: CPN Console, CPN Marketplace and CPN Payouts。

WHAT'S CPN TO SUBVERT

TRADITIONAL CROSS-BORDER PAYMENT CHAINS: SWIFT + CORRESPONDENT BANK + LOCAL CLEARING SYSTEM (E.G. US ACH)

• IF THE SETTLEMENT IS SETTLED IN A STABLE CURRENCY, THE INTERMEDIARY ABOVE CAN BE SAVED — CPN (MAOIST) MAINTAINS THE BOOKS OF THE PARTICIPANTS DIRECTLY WITHIN THE NETWORK

:: By contrast, Airwallex, while bypassing SWIFT and the correspondent bank (through pre-positioning pools in various countries), still relies on local clearing systems and requires bank accounts

• THE ULTIMATE VISION OF CPN: NOT EVEN BANK ACCOUNTS

Although currently CPN has accumulated about 500 potential clients. However, management has made it clear that the goal at this stage is not to realize, but rather to focus on the quality of users and the continuous expansion of the network. With the future network effects, there will be sufficient space to charge far less than the traditional model — that is at the heart of the Circle's second growth curve。

Conclusion: the moat and long-term value of the Circle

Circe has demonstrated a significant competitive advantage in the area of stabilization currency, with core values derived not only from USDC itself but also from the payment and settlement ecosystems it constructs. The future stable currency market is likely to be "Winner takes most" and Circle has taken the lead through the three moats:

1. NETWORK EFFECTS: USDC HAS THE WIDEST COVERAGE AND OPTIMAL INTEROPERABILITY, CREATING A POWERFUL ECO-SHIP. IF USERS OR BUSINESSES DO NOT HAVE ACCESS TO USDC, SIGNIFICANT OPPORTUNITY COSTS MAY BE LOST。

LIQUIDITY NETWORKS: USDC HAS THE BEST AND MOST EXTENSIVE INTEGRATED LIQUIDITY NETWORK TO PROVIDE STRONG SUPPORT FOR TRANSACTIONS AND SETTLEMENTS。

3. Regulatory infrastructure: Circe has obtained 55 regulatory licence plates, the most compliant stable currency at present, and has built a strong compliance river. In the United States, bills such as Genius Act and a clear regulatory framework provide a great deal of compliance certainty for Circle, which many other encryption companies do not have。

Notebook LLM General

With stable currency markets predicting a total circulation of $2 trillion in 2030, Circle is expected to maintain its dominant position in the digital dollar ecology, depending on its core moat and capacity of implementation. In spite of the challenges of a low interest rate environment, a single income model and high-scoring costs, Circle is shifting its business model from a simple spread income model to a network service and infrastructure model centred on USDC. Its highly compliant path may increase operating costs in the short term, but in the long term it can consolidate regulatory advantages that capture the value of traditional global financial and institutional markets。

This logic is similar to China’s mobile payment pattern: micro-credit payments and payment treasures occupy almost all day-to-day payment scenarios, and if a merchant fails to access these two major payment instruments, it loses a large number of customers, seriously affecting revenue. This explains why emerging forms of payment, such as tremors, are difficult to expand rapidly in a short period of time — even if the product is powerful, lacks a user base and a commercial access network, it is difficult to create a critical mass to initiate eco-ships。

SIMILARLY, USDC HAS ESTABLISHED A SIMILAR “PRE-EMPTIVE ADVANTAGE” IN THE DIGITAL DOLLAR PAYMENT AND SETTLEMENT ECOLOGY, WHOSE NETWORK EFFECTS AND INTEROPERABILITY MAKE IT DIFFICULT FOR NEW COMPETITORS TO SHAKE THEIR CURRENT POSITION. FOR BUSINESSES AND INSTITUTIONS, ACCESS TO USDC IS NOT ONLY A TRADE FACILITATION BUT ALSO A NECESSARY CONDITION FOR MARKET ACCESS。

Among other advantages, the Circe own business model has very high marginal benefits and scalable revenues。

Interest income generated by the reserve for the stable currency would be scaled up rapidly as its issuance grew, while its operating costs grew at a much slower pace, with very high marginal profits。

And Circe has been able to sustain the leadership of the crisis on several occasions, and has been recognized by his team. During the USDC decoupling crisis caused by SVB in 2023, its strong crisis management and implementation capacity was demonstrated. In 2023, the Silicon Valley Bank (SVB) collapsed, and a portion of the USDC reserve was held in SVB, and the market was once concerned about the security of the USDC reserve of US$1:1, resulting in a short decoupling of USDC (falls $1). Circle's core actions at the time:

:: RAPID DISCLOSURE OF FACTS: A CLEAR STATEMENT OF HOW MUCH FUNDS ARE EXPOSED TO SVB, RATHER THAN AMBIGUITY

• Continuous updating of information: keeping up-to-date with the market rather than "missing"

• Unequivocal commitment results: emphasize that even if there were losses, Circe would go under USDC's 1:1 payment

The team succeeded in stabilizing market confidence through decisive and transparent communication. The company is also recruiting some experienced leadership, the most recent in the 202-5 year, president of the former CFTC, Heather Tarbert, who served before joining CircleAssistant Secretary, United States TreasuryHigh-level positions in government。

From a short-term perspective, Circle still faces some structural and market-level pressures. First, as global monetary policy moves into a declining interest-rate cycle, the downward movement of interest rates will directly compress the revenue source at the centre of reserve interest, making it significantly more sensitive to macro-interest-rate changes in the short term; at the same time, the company ' s current income pattern is relatively homogeneous, it is dependent on the size and interest rate levels of the USDC, and it lacks a sufficiently diversified buffer of non-interest income. Second, in order to maintain the volume of flows and network effects of USDC, it would be necessary for Circe to pay a higher share of the profit-making costs to distribution channels such as trading platforms and payment platforms, which could further erode profit space during the slowdown in growth。

At the market level, stock prices have continued to weaken in the recent past and are operating below the 50-day average, at $80 per share, reflecting a cautious short-term financial mood and a continuing technical strain. The main reason for this is the release of IPO after 2 December 2025, 180 days after that date. The scale of the embargo is so large that it can be described as a full-flow-level shock that, prior to its release, the share in market circulation represented only about 17.2 per cent of total equity. With the lifting of the embargo, virtually all shares could theoretically be traded, and the flow drive increased by almost 400 per cent. The pressure on sale following the release came mainly from early investors and management, whose shareholding costs were mostly under $10. The insider can continuously reduce by 10b5-1 trading plans. For example, the director Patrick Sean Neville sold 35,000 shares at $90/unit on 12 December 2025。

In addition, the greatest short-term risk for Circe lies in the fact that many investors would therefore choose to be empty in the period of the lower interest rate, using Circe as a hedge interest rate. However, the potential growth point of Circe is its diversified ecosystem, which is not just a distributor of USDC, but is also building an integrated financial science and technology ecosystem that includes payments, trading, and Web3 services, which helps to increase its sources of income and target its users。

Overall, while the long-term value of Circle is clear, volatility needs to be tolerated in the short term, and technical and macro-uncertainities may result in continued volatility. Taken together, the current equity price of Circle is somewhat undervalued compared to its intrinsic value. Currently, the DCF model on Wall Street gives an inherent value range of $142 per share, which is higher than the current market price, indicating that it has some security margin at the basic level. It is worth noting that, because of the stable, well-regulated and relatively manageable nature of Circe cash flows, the WACC of Circe is only 4.02 per cent, a level closer to low-risk, highly predictable public utility companies with highly predictable cash flows, rather than typical high-volatility or encryption firms, reflecting that capital markets have seen their core cash flows as stable and defensive assets。