Korea encryption market power transfer: traditional finance grabs digital asset entry

By Tiger Research

: Deep tide TechFlow

Original link: https://www.techflowpost.com/zh-CN/article/31828

Statement: For the purpose of reproduction, readers can obtain more information by linking to the original language. If the author has any objection to the reproduction, please contact us and we will proceed with the modifications requested by the author. Reproduction for information-sharing purposes only does not constitute any investment proposal and does not represent the views and positions of Wu。

Core elements

THE AGENCY'S ENCRYPTION ACTIVITIES HAVE GONE BEYOND MOU (MEMORANDUM OF UNDERSTANDING, WHICH REFERS TO COOPERATIVE INTENTIONS, TO THE SAME) TO SPECIFIC OPERATIONS AND EXCHANGE ACQUISITIONS。

INSTITUTIONS ARE SECRETLY INTENSIFYING COMPETITION FOR CRITICAL FINANCIAL INFRASTRUCTURE, INCLUDING STO STANDARD SETTING, STABILIZING CURRENCY PAYMENT TRACKS AND HOSTING MARKETS。

DOMESTIC INFRASTRUCTURE BUILDERS ARE BECOMING THE CORE PILLAR OF INSTITUTIONAL OPERATIONS, BUILDING A KOREAN-OWNED TRACK THAT MEETS THE CBDC FRAMEWORK AND LOCAL REGULATORY REQUIREMENTS AND REDUCES RELIANCE ON FOREIGN TECHNOLOGY。

The strategy of the Overseas Web3 Foundation to enter Korea has been completely transformed from retail community building to working with large enterprises and financial institutions, as traditional finance is accelerating to take over the market。

1. MOU ARMS RACE

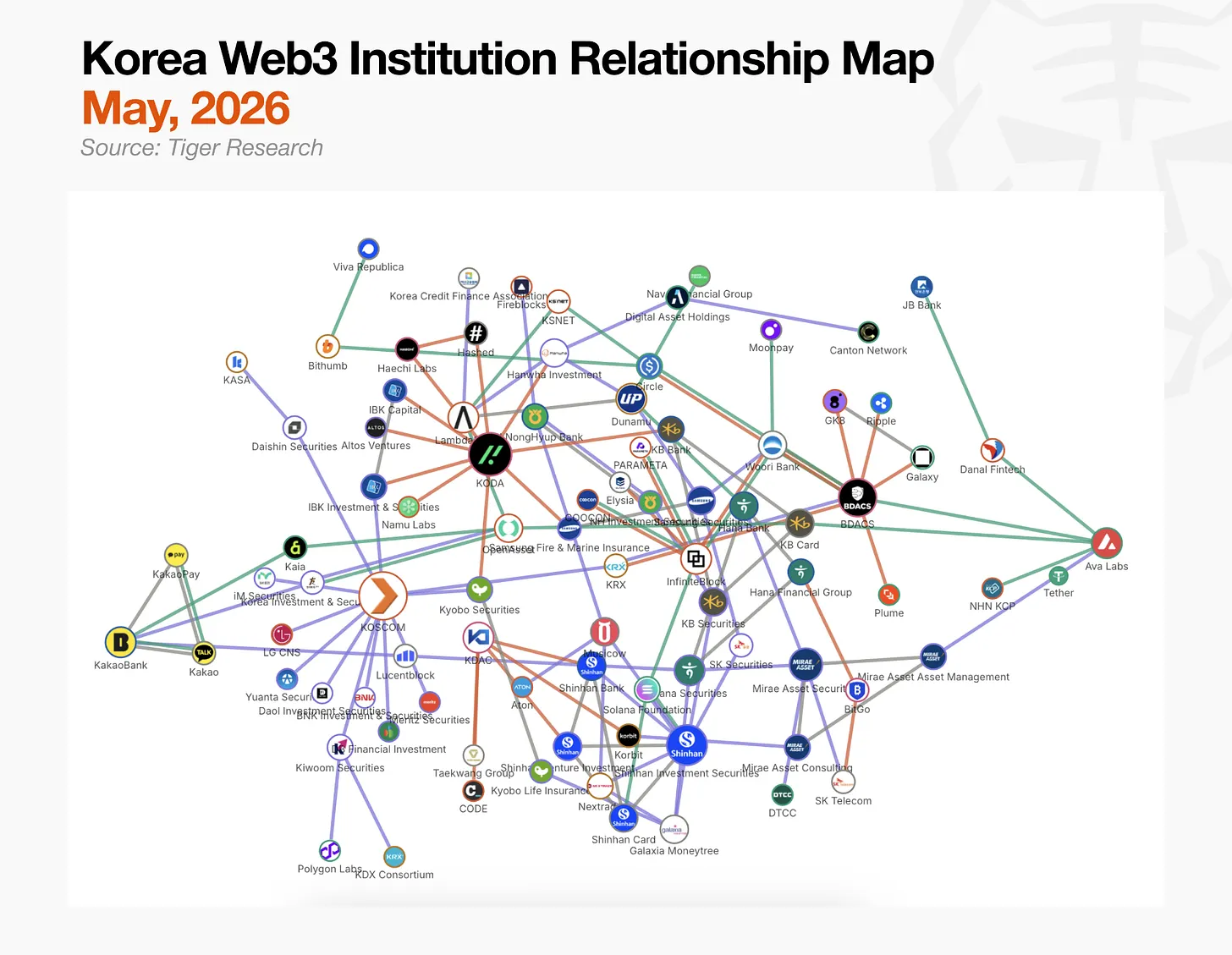

The above figure was prepared by Tiger Research, which mapped the connection in the encryption pattern of Korean institutions. But this structure is not easy to see. It is difficult to distinguish which lines represent active operations and which are simply MOUs, and the boundaries between the hub and the marginal participants remain blurred。

It is noteworthy that this complexity itself accurately reflects the current state of the encrypted market for Korean institutions. As the Tiger Research data sets confirm — 150 institutions and 196 partnerships — no hub has achieved dominant control of the market。

DOMESTIC INSTITUTIONS ARE ESTABLISHING THEIR POSITIONS IN THE MARKET AS A WHOLE BEFORE REGULATION BECOMES FULLY CLEAR. COMPETITION NOW REVOLVES AROUND THREE FRONTS: STABILIZATION CURRENCY, STO (SECURITIES ISSUANCE) AND HOSTING (ENCRYPTED ASSET STORAGE)。

It is also noteworthy that financial institutions continue to buy shares in exchanges, a move that is interpreted as a confidence-driven grab until regulation is fully clear。

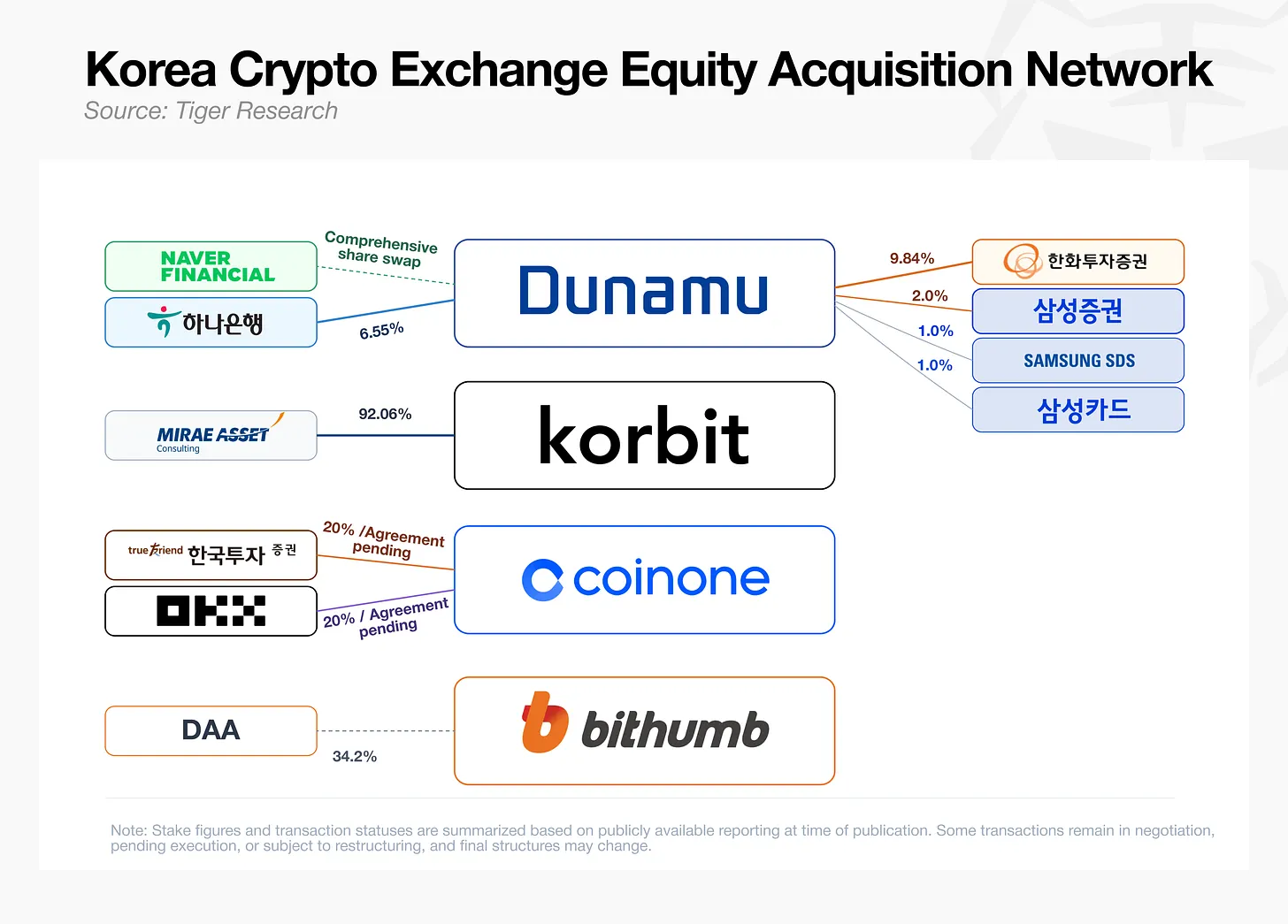

2. Exchange equity competition War

Less than 10 days after the Hanya Bank announced that it would buy approximately 1 trillion won (about $720 million) of the shares of the Upbit operator Dunamu 6.55 per cent, the Korean investment securities approved an additional 3.90 per cent acquisition. On 28 May of the same month, Samsung securities, Samsung SDS and Samsung cards jointly announced joint acquisitions of 4.0 per cent. The future asset counselling was contracted as early as February to purchase Korbit 92.06 per cent of shares, and there are reports that the Korea Investment Stock and Global Exchange OKX is discussing joint acquisitions of Coinone。

THIS COMPETITION REFLECTS THE REVALUATION OF ENCRYPTED EXCHANGES, WHICH ARE NOW SEEN NOT ONLY AS A PLATFORM FOR TRANSACTION COSTS, BUT RATHER AS KEY CUSTOMER POINTS FOR THE DISTRIBUTION OF STABLE COINS, HOSTING SERVICES, SECURITIES TOKENS AND RWA PRODUCTS。

BANKS AND SECURITIES COMPANIES ARE GRANTED INDIRECT ACCESS TO LICENCES SUCH AS VASP REGISTRATION, WHILE ENSURING THE USER BASE AND MOBILITY OF THE EXCHANGE. THE CURRENT EQUITY BATTLE IS ULTIMATELY A COMPETITION ABOUT WHO WILL CONTROL THE FRONT END OF THE FINANCIAL FRONT OF DIGITAL ASSETS。

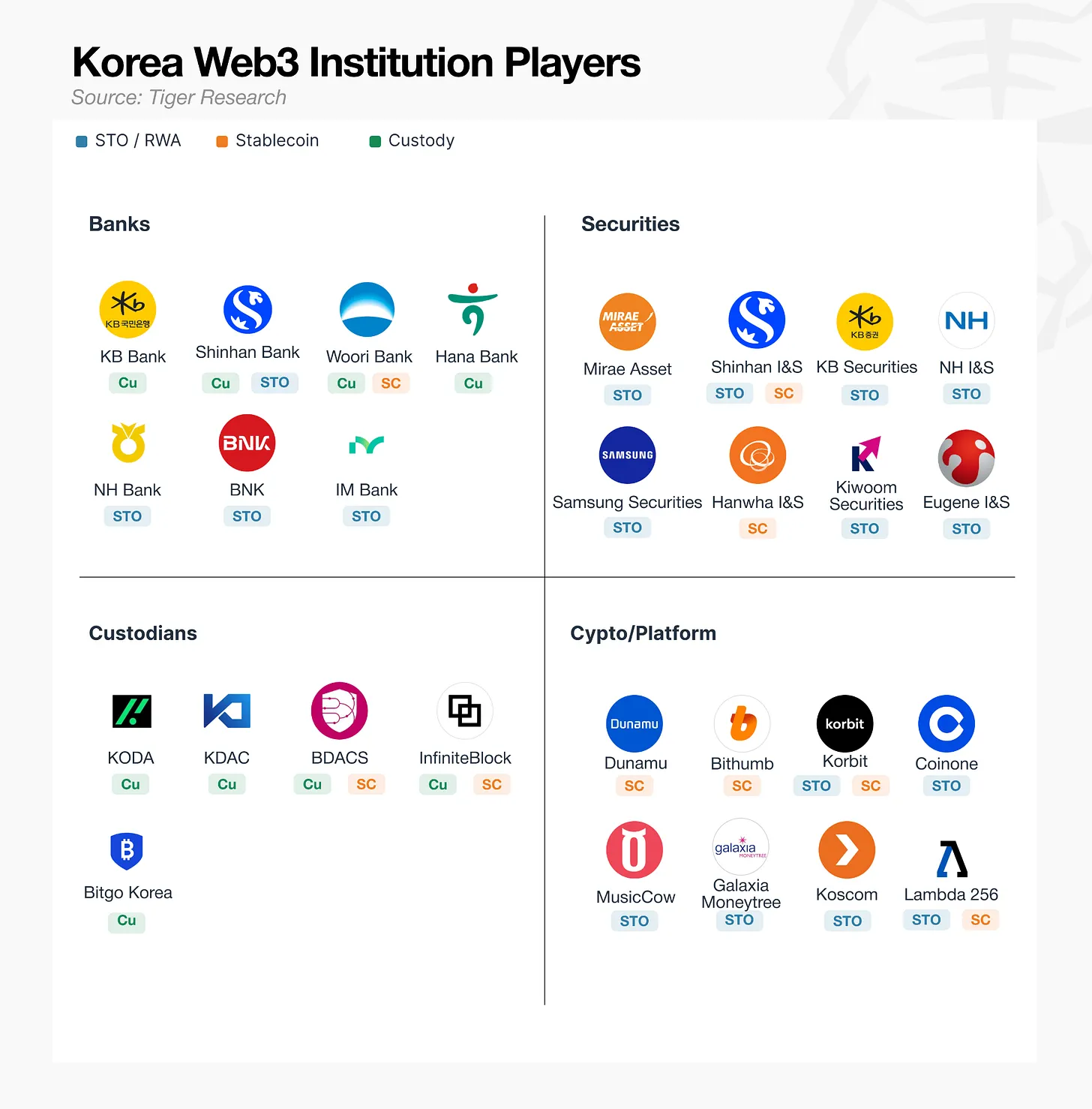

3. Korea Encryption Market by Industry

AN INDUSTRY-BY-INDUSTRY ANALYSIS OF THE RELATIONSHIP MAP REVEALED AN UNEVEN PATTERN. HOSTING OPERATIONS ARE MOST ACTIVE, WITH MANY PARTICIPANTS ALREADY OPERATING REAL-TIME SERVICES AFTER REMOVING REGULATORY BARRIERS. BY CONTRAST, RWA AND STO REMAIN LARGELY AT THE CONTRACT OR MOU STAGE PENDING THE ENTRY INTO FORCE OF THE RELEVANT LEGISLATION. THE STABILIZATION CURRENCY FACES SIMILAR STAGNATION AND THERE IS NO CLEAR STANDARD SETTER IN A POSITION TO DOMINATE THE MARKET。

Because of the different nature of the barriers in the various sectors, the strategies for breakthroughs vary. Some of the participants are consolidating domestic alliances pending regulatory opening. Others have turned to regulation to drive faster overseas markets and open alternative paths. The following section explores specific barriers and participant strategies for each sector。

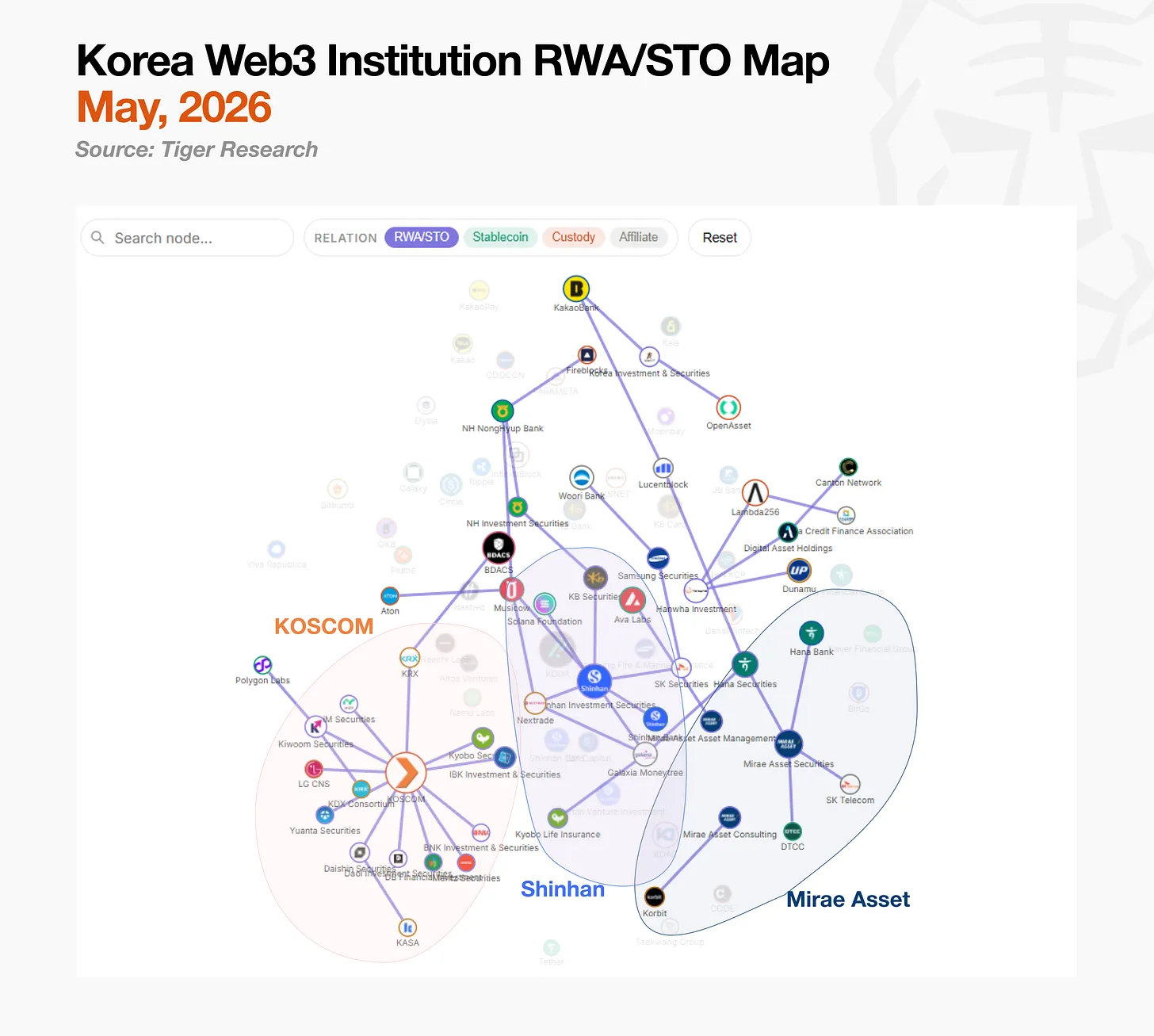

3.1. RWA/STO: LEGISLATION PASSED AND COMMERCIALIZATION OF INFRASTRUCTURE IS A BOTTLENECK

THE DOMESTIC STO MARKET IS DIVIDED INTO TWO CAMPS: THE KOSCOM-LED ALLIANCE AND THE NEW KOREA-LED FRACTURE INVESTMENT ALLIANCE. FUTURE ASSET SECURITIES FOLLOW AN INDEPENDENT PATH, USING OVERSEAS OPERATIONS RATHER THAN WAITING FOR DOMESTIC INFRASTRUCTURE。

KOSCOM, A CORE FINANCIAL NETWORK OPERATOR WITH 76.6 PER CENT OF ITS SHAREHOLDING, IS PURSUING A NEUTRAL INFRASTRUCTURE MODEL CONSISTENT WITH ITS FOUNDING MISSION TO PROVIDE A SHARED INFRASTRUCTURE FOR SECURITIES FIRMS. IT DID NOT SIGN A SOLE-SOURCE AGREEMENT WITH INDIVIDUAL ISSUERS, BUT RATHER CONSOLIDATED 11 SECURITIES FIRMS ON THEIR PLATFORMS WITH THE AIM OF DEVELOPING TECHNICAL STANDARDS FOR ISSUANCE AND DISTRIBUTION AND ENSURING INTERFACES WITH THE KOREA STOCK MANAGEMENT INTEGRATED HOSTAGE MANAGEMENT REQUIREMENTS。

New Korea investment securities quickly built their own STO ecosystem. Starting with the conceptual validation of Lambda 256 in 2022, it launched the joint platform PULSE in 2024 and officially launched the multiplatform account integration service in 2025. In 2025 alone, it participated as account administrator in 10 investment contract securities issues and obtained a controlling interest in the OTC Exchange NXT, establishing end-to-end pipelines within its own ecosystem from issuance to distribution。

THE FUTURE ASSET SECURITIES ARE COMPLETELY BYPASSED BY DOMESTIC INFRASTRUCTURE DEVELOPMENT AND GO DIRECTLY TO SEA. IT ISSUED DIGITAL BONDS IN HONG KONG, OBTAINED A RETAIL LICENCE FOR DIGITAL ASSETS FROM THE HONG KONG SECURITIES COMMISSION AND PLANS TO LAUNCH MTS FOR MARKET RETAIL INVESTORS IN JUNE. IN THE UNITED STATES, IT IS THE ONLY KOREAN SECURITIES FIRM TO JOIN THE DTCC-LED MONETIZATION WORKING GROUP, WHICH INCLUDES MORGAN CHASE, GOLDMAN SACHS AND BELED, TO PARTICIPATE IN GLOBAL STANDARD-SETTING DISCUSSIONS. WHEN DOMESTIC STO INFRASTRUCTURE IS EVENTUALLY ALIGNED WITH GLOBAL STANDARDS, THIS STRATEGY GIVES FUTURE ASSETS AN ADVANTAGE IN TERMS OF REGULATORY DOCKING AND NEGOTIATING LEVERAGE。

3.2. Stable currency: legislation rather than technology is a bottleneck

Participants in stable currency markets are more diverse than in other industries. Cards, exchanges, financial technology and infrastructure companies all enter through different routes, taking advantage of their respective strengths。

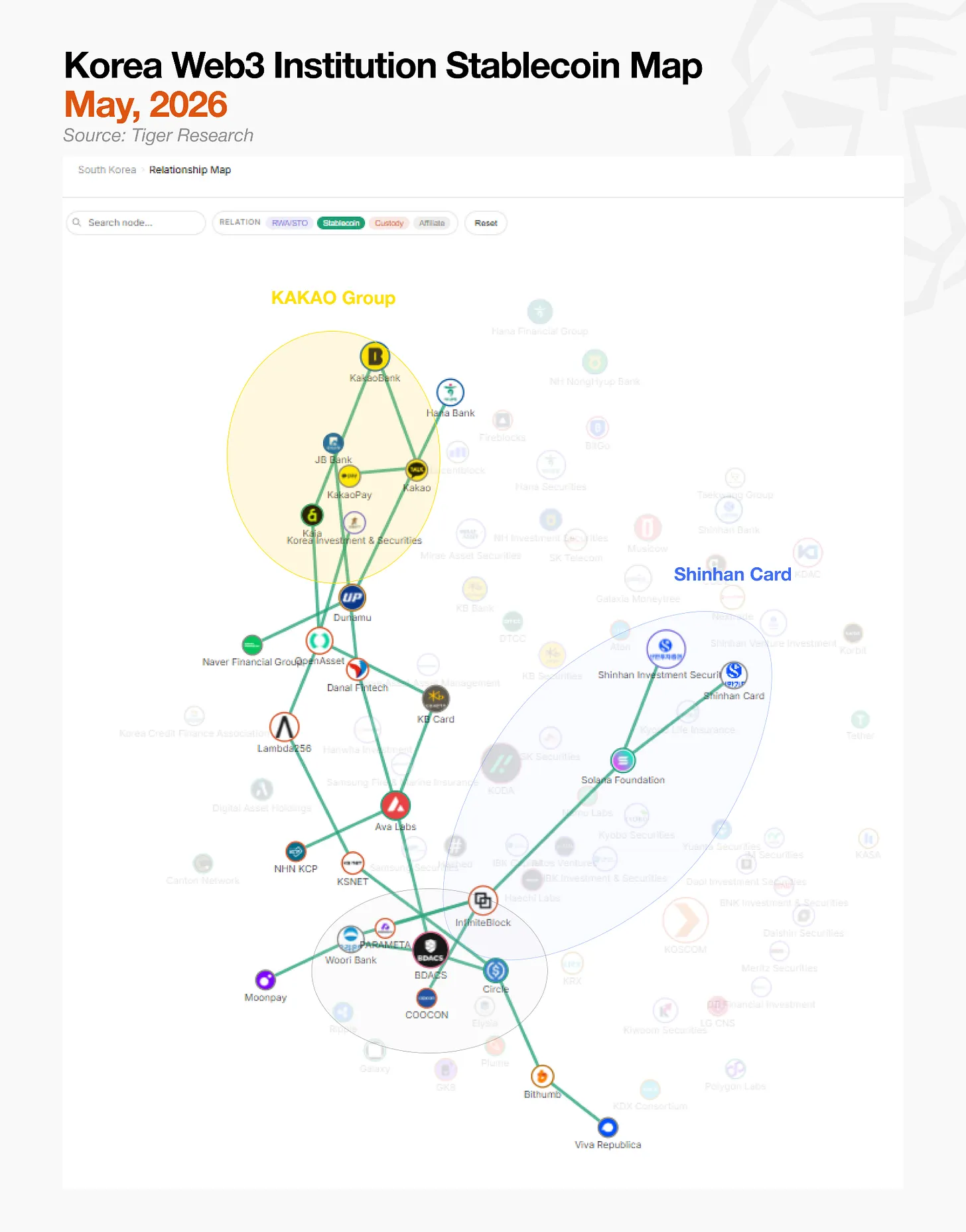

The largest group is Kakao Group. Kakao, KakaoBank and Kakao Pay formed a joint working group to construct a "super wallet" covering stable currency, encrypted currency and local currency. Their key asset is the infrastructure that has built up the Kaia public chain since the Grond X era. Kaia has deployed Tether (USDT) on its network and is testing real-time payments。

New Koreana focuses on moving its existing payment network to block chain tracks. In April, NKKC signed a MOU with Solana, although the technical infrastructure was earlier than the agreement. The company has completed a preliminary conceptual validation with Solana, Visa, Mastercard and Fireblocks and is now conducting advanced testing in six areas, including wallets and smart contracts。

The exchange camp is bypassing the Korean dollar through the dollar. Dunamu is developing a Korean dollar stabilization business based on its exclusive block chain, GIWA. In the face of the delay in regulating the Korean dollar, Bithum chose to first ensure the distribution of the dollar through partnerships with Circle and WLF. The joint Korean dollar stabilization plan with Toss was also under discussion, albeit slowly。

All camps are active but face the same regulatory barriers. The Central Bank of Korea is pushing for 51 per cent rule, requiring that only a bank-majority coalition be allowed to issue stabilization coins, while the financial technology company is seeking access, delaying government-government party consultations. Once the guide has been issued, it is expected that the camp receiving the most comprehensive public contact will gain market leadership。

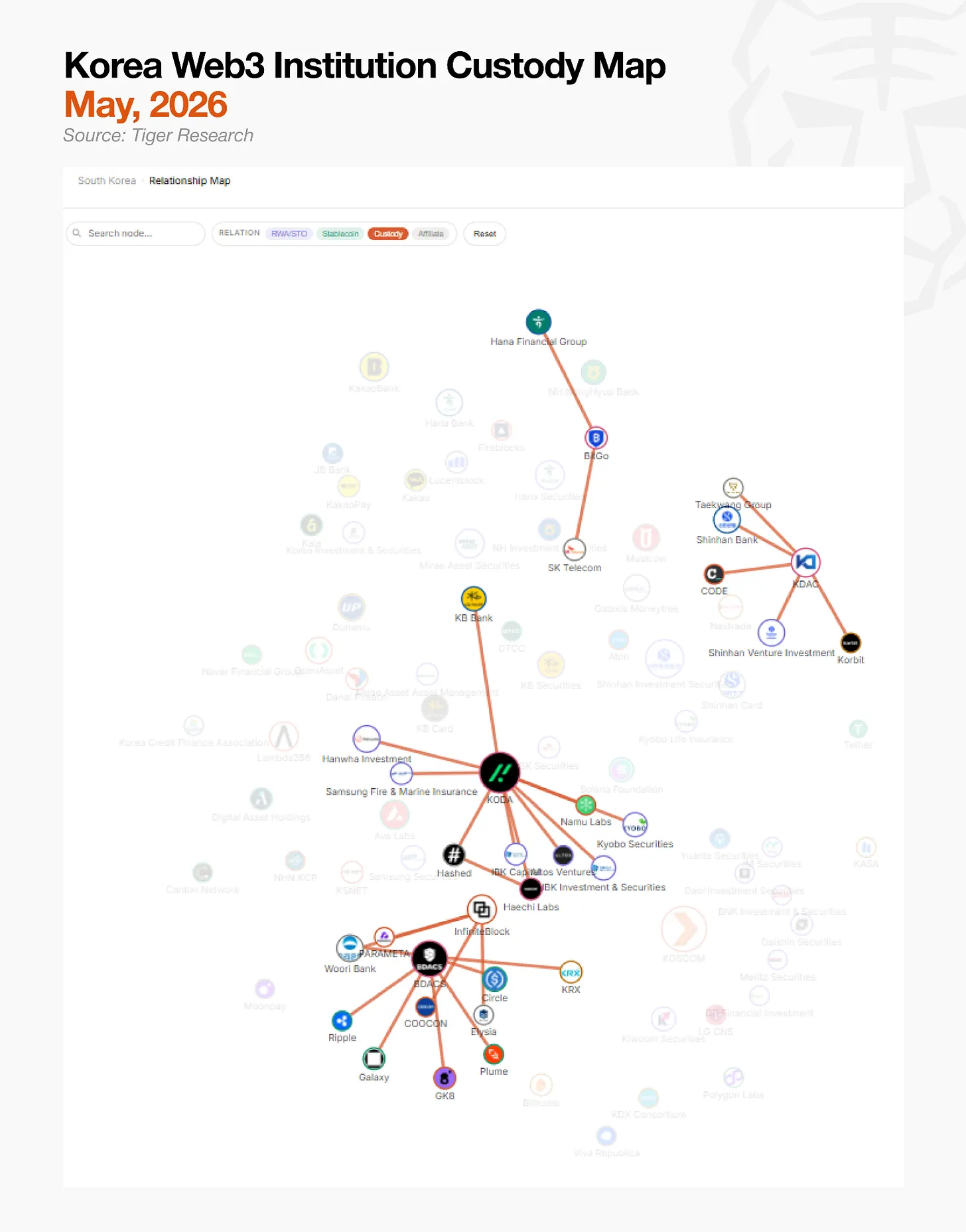

3.3. Hostage: the need for additional institutional capital

The hosting market is more structured than other industries. Each of the four trustees has secured domestic and international financial and technical partners to establish its market position。

KODA was created jointly by KB National Bank, Hasshed and Haechi Labs, combining traditional financial capital and encrypted original VC. The Korean investment securities, IBK capital and education securities were subsequently added as investors, and their stability was further enhanced by a dedicated hosting insurance agreement with the Samsung Fire Marine Insurance。

KDAC is a traditional financial-led custodian, with the Bank of New Korea and the NH Bank for Agricultural Cooperation as major shareholders. NH Bank for Agriculture, which was originally an investor in another custodian, Kardo, became KDAC shareholders after the merger. After the merger, KDAC shareholders included two of the five major banks in Korea。

BDACS adopts a unique approach centred on technology and partnership development. The hosting and payment infrastructure was extended through a partnership with the Bank of Friends and the International Digital Asset Infrastructure Corporation, including Galaxy and GK8, and it also signed a MOU with Circle to issue the Korean dollar stabilization currency KRW1 on the Arc block chain in Circle, and is the only VASP and key hosting partner in the KRX-led KDX coalition. BDACS is currently conducting a conceptual validation of KRW1 to position itself as a trustee for both hosting and payment infrastructure。

Bitgo Korea, with the technological strength of its global parent company, enters the domestic market. Bitgo Headquarters hosts more than $70 billion in assets and handles approximately 20 per cent of the world ' s currency chain transactions. At home, the Hanya Financial Group and SK Telecommunications each hold shares, making them custodians supported by financial and telecommunications capital。

Agencies have entered the market through their respective trusteeship relationships. However, all major custodians were reported to have experienced a net loss over the past year, indicating that they had been built ahead of the institutional capital inflows required to maintain operations。

TAKEN TOGETHER, THE BUILD-UP OF THE STO, THE STABILIZATION CURRENCY AND THE HOSTING INFRASTRUCTURE REVEALS A CLEAR COMMON CONSTRAINT: DOMESTIC INSTITUTIONS HAVE BUILT THE OPERATIONAL FRAMEWORK, BUT THE BOTTOM TECHNOLOGICAL INFRASTRUCTURE REMAINS LARGELY DEPENDENT ON OVERSEAS SOLUTIONS。

4. Infrastructure builders

Reliance on overseas solutions entails structural costs: as markets grow, a significant proportion of revenues will flow abroad in the form of technology licensing fees. Domestic infrastructure is also at risk of disruption if overseas partners change policies or increase costs。

THE MORE FUNDAMENTAL PROBLEM IS THAT AREAS THAT NEED TO BE ALIGNED WITH KOREA’S PARTICULAR REGULATORY ENVIRONMENT – SUCH AS THE ISSUANCE OF THE KOREAN DOLLAR, THE STO DISTRIBUTION RULES AND THE INTEGRATION OF DOMESTIC BUSINESS ACCOUNTS – CANNOT SIMPLY APPLY GLOBAL SOLUTIONS DIRECTLY. THIS IS WHY IT WILL BE ESSENTIAL FOR DOMESTIC TECHNOLOGY COMPANIES TO BE ABLE TO DESIGN AND CONTROL THE BOTTOM TRACK DIRECTLY IN ACCORDANCE WITH KOREA ' S REGULATORY FRAMEWORK ONCE THE RELEVANT LEGISLATION IS FINALIZED AND CAPITAL FLOWS BEGIN TO FLOW IN EARNEST。

Domestic companies that have identified this technology gap and are building specific financial infrastructure in Korea are already operating. The leading technology providers are as follows。

4.1. LG CNS

LG CNS is the most prominent of traditional IT service companies. Since the launch in 2018 of the "Monachain" Zone Chain Platform, it has developed operational experience by providing services to more than 220 local governments through the local currency platform of the Korea Money-Building Commune。

THIS PERMIT CHAIN EXPERIENCE TRANSLATES INTO ORDERS FOR CBDC AND STO PROJECTS. AS THE MAIN CONTRACTOR FOR THE CENTRAL BANK OF KOREA ' S CBDC PROJECT, HANJIANG, LG CNS IS DEVELOPING A GOVERNMENT SUBSIDY SYSTEM FOR THE USE OF DEPOSIT COINS. AS A RESULT OF THIS PROCESS, IT HAS BUILT UP THE CAPACITY OF THE CBDC AND PRIVATE DIGITAL CURRENCY SYSTEMS OPERATING ON A SINGLE NETWORK TO EFFECTIVELY TRANSPOSE SECURITY STANDARDS AND PROCEDURES FROM TRADITIONAL FINANCE TO BLOCK CHAINS。

The same logic is followed for the development of the joint KOSCOM STO distribution platform and the future assets securities STO platform. LG CNS does not directly issue assets but aims at three directions: building distribution and distribution platforms for banks, providing Saas to payment operators, including credit card companies, payment gateways and simple payment services, and developing digital asset payment platforms for securities firms. Once the regulatory framework is finalized, it appears to be the candidate most likely to have access to the infrastructure contract market。

IN BLOCK CHAIN INFRASTRUCTURE COMPANIES, DSRV EMERGED BY DIRECTLY HELPING FINANCIAL INSTITUTIONS TO ACCESS THE CHAIN INFRASTRUCTURE. AS A CERTIFIER AND INFRASTRUCTURE COMPANY OPERATING ON OVER 70 BLOCK-CHAIN NETWORKS, DSRV MANAGES MORE THAN 4 TRILLION WON (ABOUT $2.9 BILLION) OF ASSETS, RANKED FIRST AMONG SOUTH KOREA'S TAIFENG PLEDGE AND TOP 10 GLOBALLY。

A key development is its expansion from nodal operation to a whole institutional chain infrastructure. Through DSRV Portal, financial institutions can access wallets, payments, monetization, hosting and pledge functions through the API and dashboard interfaces. Without building its own nodes and security infrastructure, financial companies can access user wallets, institutional wallets, periodic payments, token distribution, destruction, transfer and lock-in, hosting and pledge capabilities。

Confidence mechanisms have also been put in place. DSRV was the first to obtain VASP, ISMs and SOC 1 Type 1 certification, directly meeting the regulatory, safety and operational control requirements of financial institutions. In practice, this means that external infrastructure providers bear the security, internal control and operational risks of purses that financial companies bear most when they provide services along the deployment chain。

Its partnership is oriented towards payment track construction. DSRV, together with SBI Ripple Asia, has developed a remittance infrastructure in line with Korean regulations. Cooperation with Circle to develop the USDC framework for issuance, foreclosure and settlement of institutions that bypass the exchange. A stabilization currency payment infrastructure agreement was signed with BC Card to link the traditional card payment network to the block chain。

DSRV HAS RECENTLY COMPLETED A ROUND B FINANCE OF 30 BILLION WON (APPROXIMATELY $21.7 MILLION) TO ACCELERATE TECHNOLOGY DEVELOPMENT。

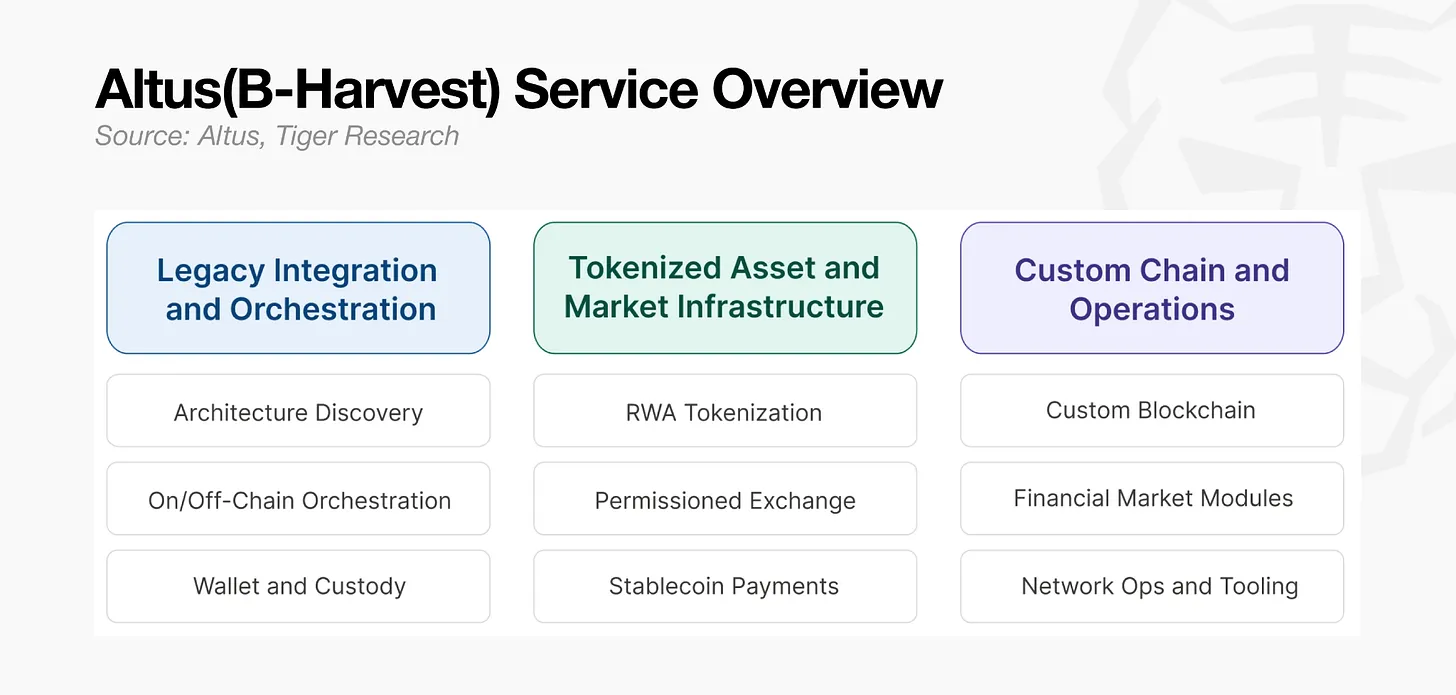

Altus (formerly B-Harvest)

Altus (formerly B-Harvest) operates in an integrated layer between the legacy systems of financial institutions and the block chain environment. Founded in 2018, it contributed to the development of the EVM chain based on Cosmos SDK, an organization of over 40 engineers and researchers who directly built production networks including Canto, Crest, Stable and Ault。

Altus processed protocol works and core architecture for Ault Blockchain, an agency dedicated to RWA, trading and payment L1. In 2025, it contributed EVM integration, performance improvement and security audits to the Bitcoin pledge L1 Babylon to support its production readiness。

Its financial institution solutions originate on the same level. Altus was built from scratch in accordance with the requirements of the financial industry: the chain-up layer connecting the legacy systems and block-chain implementation environment, the RWA monetization, the licensing exchange, stable currency payments and settlements, and the institutional wallet and hosting infrastructure。

Current in-house research and development takes place in parallel: the Canton Network architecture supporting inter-agency selective data disclosure, and the modular block chain framework Commonware Stack, which targets 1 million TPS。

The three companies have different advantages from different locations. LG CNS leads by financial IT credibility, DSRV by block chain certifier infrastructure, Altus by protocol design capability. But all companies have the same objective: to acquire core operating systems before large-scale inflows of institutional capital. The determining factor is how much credible build-up experience each company can accumulate before markets are fully open。

5. Dispersion, institutional entry

The recent surge in cooperation announcements should not be interpreted as ordinary business outreach. These are positioning actions: institutions take advantage of enabling arrangements before regulation is finalized and then use them to influence the final shape of the regulatory framework. The current cooperative competition is more regulatory design than market competition。

THE KOREAN ENCRYPTION MARKET HAS BEEN SIGNIFICANTLY RESTRUCTURED IN JUST SIX MONTHS. THE TRUSTEESHIP CAMP HAS BEEN FORMED, THE STO COALITION HAS BEEN FORMED, AND THE MAJOR FINANCIAL HOLDING COMPANIES HAVE TAKEN ACTION TO ACQUIRE SHARES IN THE EXCHANGE. AT THE SAME TIME, THERE HAS BEEN A SIGNIFICANT DECLINE IN BULK TRANSACTIONS. THE TOTAL VOLUME OF TRANSACTIONS ON THE FIVE MAJOR KOREAN EXCHANGES DECREASED BY APPROXIMATELY 48 PER CENT OVER THE SAME PERIOD. THE FOCUS OF THE MARKET IS RAPIDLY SHIFTING FROM THE DIASPORA TO INSTITUTIONS。

This shift has also changed the way overseas encryption foundations approach Korea. Just as Solana was adopted as a partner by the Xinhanka, Avalanche was adopted by future assets, and foundations entering the domestic market shifted their main focus from exchange transactions to cooperation with financial institutions and large enterprises. The model of community meetings, which had promoted mobility, was no longer effective。

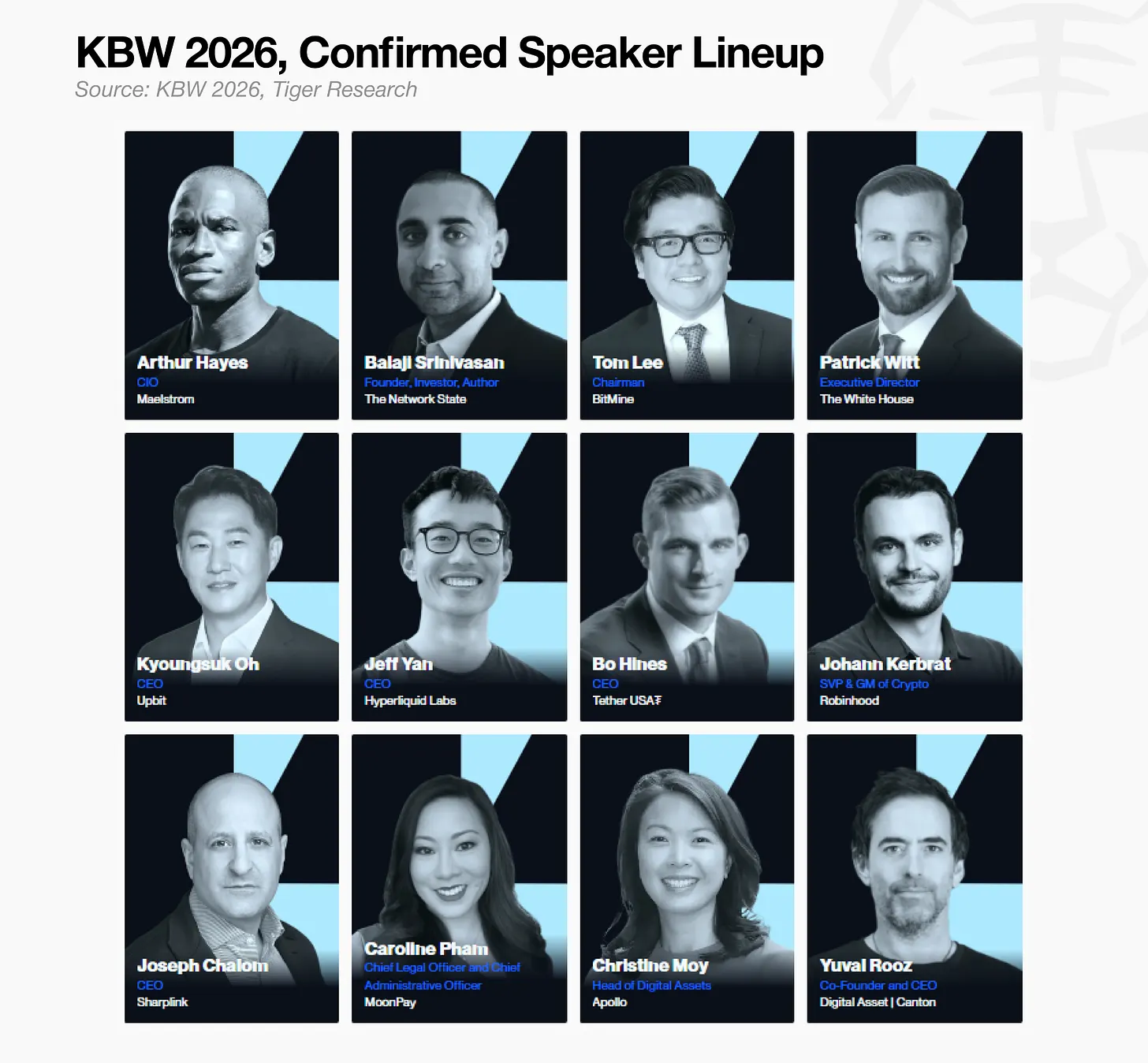

THE OUTCOME OF THIS MARKET RESTRUCTURING IS EXPECTED TO APPEAR AT KBW 2026 IN SEOUL IN SEPTEMBER 2026, AN EVENT THAT ALWAYS REFLECTS THE PREVAILING MARKET CONDITIONS. CHECKING THE LIST OF IDENTIFIED SPEAKERS, TRADITIONAL FINANCIERS ARE IN THE MAJORITY. IN THE PAST YEAR, THE OFFSHORE FOUNDATION HAS STIMULATED COMPETITION FOR NEIGHBOURHOOD ACTIVITIES THROUGH TOKENS, AND THIS YEAR'S FOCUS IS EXPECTED TO SHIFT TO SUBSTANTIVE BUSINESS DISCUSSIONS。

Tiger Research is the official research partner of KBW 2026。