Is the stock market going down this week

Who's most dangerous this week

This week ' s global market is dominated by Japan ' s interest rate hike and the Fed Conference. For venture assets, this week is not meant to be a modest one。

Three months ago, Wall Street was discussing when the interest rate would fall. The market was willing to give face to the new president, inflation was going down, employment was going down, and interest-rate cuts were a matter of time. But the financial world is so volatile that the scripts that we all wanted were useless。

IN MAY, CPI ROSE TO 4.2 PER CENT THE SAME YEAR, 0.5 PER CENT THE RING, 3.9 PER CENT THE ENERGY PRICE, AND THE CORE CPI REMAINED CLOSE TO 2.9 PER CENT. NOR WAS THERE ANY REASON FOR THE FED TO IMMEDIATELY TURN AROUND, WITH AN INCREASE OF 172,000 IN NON-FARMERS IN MAY, AND AN UNEMPLOYMENT RATE OF 4.3 PER CENT. THIS MEANS THAT THE FED IS NOW FACED WITH AN AWKWARD COMBINATION: INFLATION IS RISING AGAIN, JOBS ARE NOT FALLING SHARPLY, AI INVESTMENTS ARE STILL SUPPORTING ECONOMIC RESILIENCE, INTEREST RATES ARE FALLING FOR WEAKER REASONS, AND THE CONDITIONS FOR HIGHER RATES ARE ACCUMULATING。

At the same time, the Central Bank of Japan convened a policy meeting on June 15-16, and the market has already used the 25 basis points increase as a benchmark. According to Polymarket's "Bank of Japan Regulation in June", the 25bp interest rate increase is about 98.3 per cent, with the same rate of about 1.45 per cent and an increase of about 0.55 per cent over 50bp。

IT SHOULD BE RECALLED THAT JAPAN ' S PREVIOUS INTEREST RATE HIKES HAD HAD A CONSIDERABLE IMPACT ON THE OVERALL FINANCIAL MARKET. AND THIS TIME, FACING A TUESDAY HIKE FROM JAPAN AND A THURSDAY FED FOMC MEETING, WILL THE MARKET FALL

Walsh, the Fed's interest rate is rising

Let's see the Fed first。

The possibility of a reduction seems to be close. In Polymarket, “No interest rate decline in 2026” is about 70.35%, “No interest rate reduction by July” is about 2.35%, and “No interest rate reduction by December” is about 23%. Seven adults will bet once this year. At the end of the year, the ceiling of 3.75 per cent was maintained at approximately 37 per cent, 4.00 per cent, approximately 32.5 per cent, 4.25 per cent, approximately 11.25 per cent, 4.50 per cent and above, approximately 3.35 per cent, and over 47 per cent。

The market's judgment of Walsh is based on a basic consensus that he won't do anything at his own premiere, this week's FOMC meeting. The interest rate risk is still concentrated after three quarters. Polymarket has several entries that illustrate this consensus:

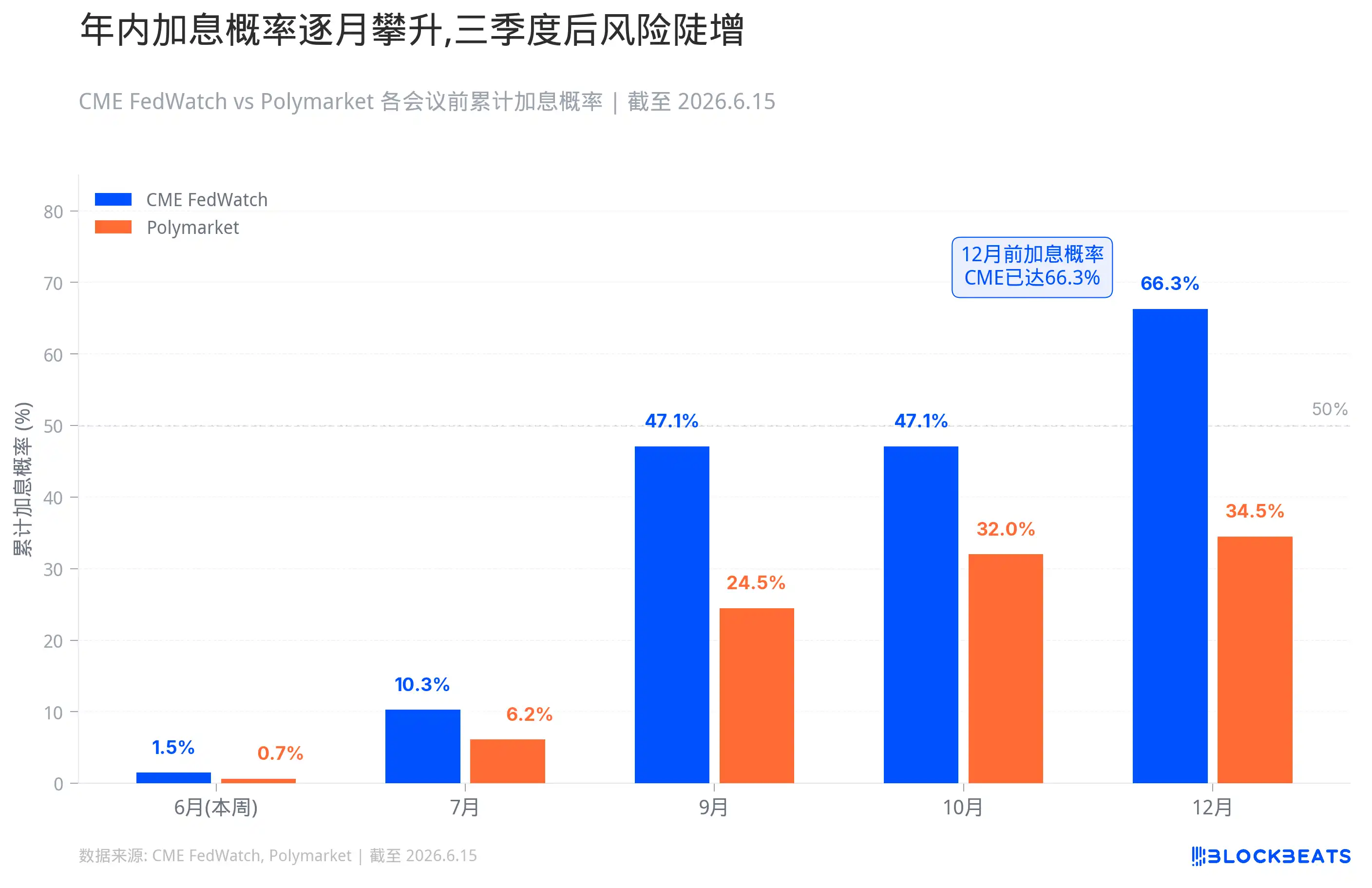

“Fed rate hike in 2026?” shows that the probability of an increase of interest at any time in 2026 is about 34.5 per cent; “Fed rate hike by...?” shows that the interest rate increase by June was about 0.65 per cent, 6.15 per cent before July, 24.5 per cent before September and 32 per cent before October; in the “Fed decision in July”, the interest rate increase by 25 bp was about 3.15 per cent, 0.3 per cent above 50 bp, or 93.5 per cent; and “What will the Fed rate be at the end of 2026?” the maximum interest rate at the end of the year was about 37 per cent, 4,00 per cent, 32.5 per cent, 4.25 per cent, 11.25 per cent, 4.50 per cent and more than 3.35 per cent。

More specific probabilities and data look. The probability of an increase in interest rates by 29 July is about 10.3 per cent, 47.1 per cent by 28 October and 66.3 per cent by 9 December. Polymarket is more conservative, "Fed rate hike in 2026?" to 34.5%, about 24.5% before September and about 32% before October. For this month's probability, CME Fedwatch remained unchanged at 98.5 per cent and Polymarket at 99.55 per cent。

This week, the United States probably stayed at the same rate, but "no action" and "no tightening" are different things。

If Walsh admits at the launch that the inflation risk has re-pressed growth concerns, if the dotage map changes the 2026 interest-rate hub from a flat to even-up, and if the words “the interest-rate bias” in the statement are removed, the market will itself tighten for the Fed。

The first reaction was the short-end dollar debt. 2 The annual and annual rates of return follow the Fed’s path directly, and the short-end rates of return will go up once the market has switched from “lower interest rates later” to “possibly higher interest rates later”. The dollar will also be supported, and the strong dollar itself is a global tightening。

THE U.S. SHARES ARE THE MOST SENSITIVE OF HIGH-VALUE GROWTH AND LONG-TERM ASSETS. THE HIGHER THE INTEREST RATES, THE LESS VALUABLE THE FUTURE CASH FLOW WILL BE, THE MORE EXPENSIVE THE FINANCING WILL BE, THE LESS WILLING THE MARKET WILL BE TO PAY A PREMIUM FOR STORIES THAT HAVE NOT YET BEEN REALIZED. THE LOGIC OF SMALL CAPITALIZATIONS, MICROPLEDGES AND NON-PROFIT TECHNOLOGY SHARES IS MORE FRAGILE, AND THESE COMPANIES EAT CHEAP MONEY, AND ONCE THE MONEY IS NOT CHEAP, THE FIRST VALUATION COLLAPSES。

If there was a real tail situation, 98.5 per cent of the "no change" price under which the Fed had a direct interest rate hike, the impact would be very severe. Short-end interest rates jumped, the United States dollar surged and leverage positions were forced to reduce risk. Not to say that it will happen, but the probability means that no one will react if it does。

After all, the importance of Walsh’s "first show" has been magnified by the market, and another important factor is that he may change the way the Fed communicates. Timiraos, a long-standing Federal Reserve stalker, has made the question clear: For Walsh, symbolic adjustments, such as dot-temping, the language of statements, and the rhythm of press conferences, can be made quickly, but a real change in the Fed ' s communication system requires long-term persuasion and internal collaboration. This week's meeting could be the first step。

It's across the Pacific. It's Japan's increased spell

And look at Japan, the Central Bank of Japan, on June 15-16, Polymarket increased interest by 98.3 per cent on 25 basis points. If you land, the policy rate rises from 0.75 to 1 per cent, the highest since 1995。

The logic of Japan being pushed to this point is straightforward. The conflict in the Middle East pushed up oil prices, with Japan being a typical energy importer, and weak yen magnifying import costs. Wages are rising, service prices are rising, and inflation is expected to begin to loosen. If interest rates continue to be low, the market wonders whether the Central Bank of Japan still cares about inflation。

The interest rate hike itself is not suspense, but an important concern is that, over the past few years, large amounts of global funds have been borrowing low-interest yen in exchange for United States dollars or other high-yielding assets, buying United States debt, shares, credit, and, indirectly, high-variant risk assets. This structure is based on the premise that interest rates in Japan are low enough, Japanese yen financing is cheap enough and central banks slow enough. That is, if the market considers Japan’s interest rate normalization to be continuous, arbitrage will become fragile, the Japanese yen will be squeezed, and global leverage will begin to contract。

The fear of Japan's increased interest in the market is not an empty wind. Almost every attempt by the Bank of Japan to raise interest rates from near zero in the last two decades or more has caused trouble in the global market。

The first was in August 2000. The Central Bank of Japan has increased interest rates from zero to 0.25 per cent, and the timing has just hit the peak of the US Internet bubble. Within three months of the hike, NASDAQ fell 35%. The Japanese economy, too, was not able to carry it itself, and quickly slipped back into recession, and the yen had to reduce interest rates to zero in 2001。

The second was from 2006 to 2007. In two steps, the interest rate was raised to 0.5 per cent, the first in July 2006 and the second in February 2007. The time line is almost perfect for the gestation period of the US subprime mortgage crisis. In the summer of 2007, the United States subprime mortgage began to explode, and in 2008, Lehman fell and the global financial crisis erupted. Japanese silver was once again forced to reduce interest rates to zero。

THE THIRD TIME WAS ON 31 JULY 2024. THE YEN INCREASED THE INTEREST RATE FROM 0% TO 0.25%, WHICH WAS SMALL, BUT THE MARKET REACTED EXTREMELY. ON 5 AUGUST, THE DAY AFTER 225 SINGLE-DAY FALLS BY 12.4 PER CENT, THE LARGEST DECLINE SINCE THE BLACK MONDAY OF 1987. KOREA KOSPI TRIGGERED A MELTING PROCESS, AND NASDAK AND THE PUMP 500 DROPPED 3.4% AND 3% RESPECTIVELY. VIX PANIC INDEX GOES OVER 65. THE TRANSMISSION MECHANISM FOR THAT CRASH WAS CLEAR: THE JAPANESE YEN WAS TRIGGERED BY AN INTEREST RATE HIKE, THE ARBITRAGE TRANSACTION TO BUY OVERSEAS ASSETS WITH THE YEN WAS FORCED TO SETTLE DOWN, STOCKS WERE SOLD BACK TO THE JAPANESE YEN, AND COLLECTIVE SALES WERE SET TO STEP. IN ORDER TO SUPPLEMENT THE BOND, THE FUND MANAGER SOLD EVEN THE GOLD AND THE BTC “RISK AVOIDANCE ASSETS”. IN THE CONTEXT OF THE LIQUIDITY CRISIS, THE RELEVANCE OF ALL ASSETS IS CLOSER TO 1. THE TRAGEDY OF THAT DAY'S MARKET IS STILL FRESH。

So more importantly, what will the Japanese government suggest at tomorrow's launch: how much will interest rates actually rise

Who's most dangerous this week

As noted earlier, most of the global market performance of the Bank of Japan has declined over the past three cycles of interest-rate hikes。

In fact, however, the interest rate hikes do not in and of themselves have to be broken up, which are generally the case with other vulnerabilities. For example, the years 2000 and 2007 were years of bumping into a bigger bubble in other countries. August 2024 was over-anticipated and the market position was too late to react. But after a few market preparations, nothing happened。

This time, 25 basis points have been priced to 98.3 per cent, with little room for surprise. Based on experience in December 2024 and January 2025, the rate of interest rate increases per se was smoothed down. But this time there are two additional variables。

First, the Governor is hospitalized with infective hepatic cysts and is expected to be released in the absence of this meeting and after the meeting. According to public reports, Vice-President Nishiro Noboru will serve as Acting Chairman of the meeting, and Vice-President Ono-Nagata will preside over the launch. This arrangement would probably not change the course of the increase. However, the market is not as familiar with the communication style of the field as it is with the field, and the volatility of the interpretation is magnified. The phrase "the future will be judged by the data" and the phrase "the interest rate will still be in place" appear to be very different and a completely different signal for traders。

SECONDLY, THE UNITED STATES MET THE SAME WEEK. THERE'S ONLY ONE DAY BETWEEN THE MEETING AND THE MEETING. IF THE MARKET REACTS MILDLY AFTER THE INCREASE IN THE INTEREST RATE, THE NEXT DAY, WHEN WALSH MOVES OVER THE EAGLE, THE TWO LAYERS OF PRESSURE WILL OVERLAP. CONVERSELY, IF THE MARKET IS ALREADY STRAINED AFTER THE INCREASE IN INTEREST RATES BY THE JAPANESE SILVER BANK, A FURTHER FIRE IN THE CASE OF THE WALSH, THE SHORT-TERM MOOD MAY BE OVERREACTING. THE TWO CENTRAL BANKS ARE BACK-TO-BACK WITH THE RESULTS, AND THE SCHEDULE ITSELF IS WIDENING VOLATILITY。

We analyze each asset:

The dollar debt should be the first species to react this week. Short-end rates of return follow the Fed's path directly,2 with the most sensitive periods of years and 1 year. If Walsh’s release is to be replaced by hawks, dots, and short-end yields, it reflects the market’s re-pricing of “lower interest” and even “higher interest per year.” The long end is more complex, and the 10-year period is not necessarily synchronized with a huge increase. If the market starts to fear that high interest rates will crush the economy, the yield curve may on the contrary be even more flat or even more inverted. On the Japanese side, if Uchida suggests that interest rates will continue to increase, so will Japan’s domestic debt yield be pushed up, and if the US$ 113 trillion held by Japan is loosed, it will in turn affect supply and demand in the US debt market。

THE DOLLAR RATE IS SUPPORTED. THE FED'S CALIBER HAWK PUSHES UP THE RETURN ON DOLLAR ASSETS, DXY GOES STRONG. THE INTEREST GAIN FROM THE JAPANESE SILVER IS THEORETICALLY GOOD IN JAPANESE YEN AND IN UNITED STATES DOLLARS, BUT THE ACTUAL DIRECTION DEPENDS ON THE CALIBER: IF THE JAPANESE SILVER WERE TO BE ADDED AND THE DOVE SIGNAL RELEASED, THE YEN MIGHT NOT GO UP AND FALL, BUT THE DOLLAR INDEX WOULD BE STRONGER. WHEN THE TWO CENTRAL BANKS MEET THE SAME WEEK, THE RELATIVE MOVEMENT OF THE UNITED STATES DOLLAR AND THE YEN WILL BE VERY SENSITIVE, WITH THE RATE OF FOREIGN EXCHANGE MARKET VOLATILITY LIKELY RISING. THE ASIAN AND EMERGING MARKET CURRENCIES WILL BE PRESSURIZED, AND THE STRENGTHENING OF THE DOLLAR ITSELF IS A GLOBAL TIGHTENING THAT WILL DRAIN OFF THE LIQUIDITY OF THE DOLLAR ABROAD。

It'll be obvious that the American stock is divided. The high-value growth unit, AI long-term assets, small capitalization, microcarding, non-profit technology units are the most vulnerable. The higher the interest rate, the less valuable the future cash flow will be, the more expensive the financing will be, the less the market will be willing to pay a premium for the story that is not. Russell 2000 and the companies that live on cheap money are the first to suffer. The banking unit response is more complex and short-term spreads may benefit, but it may not be good if the curve continues to upside down and credit risk increases. Defensive stocks are in sharp decline, but utilities and REITs, such as “class bond assets”, are also valued at high interest rates. If the two central banks are hawks at the same time this week, US shares and Japanese shares will be under pressure, especially with regard to the significant index of technological power。

The day share is in a special situation. The interest rate hike in Japanese silver itself is bad news for Japanese exporting enterprises, as the Japanese yen's strength erodes overseas profits. But if the interest rate increases and rhythms are within expectations, the daily stock does not necessarily fall significantly, as the experience of December 2024 and January 2025 illustrates. The real risk is also post-session communication, which may continue to normalize if Ueda hints to do so。

Gold will be pulled by two forces. Real interest rates are rising and the dollar is stronger, usually for gold, but if the reasons behind the increase are energy shocks, geo-risks and inflation that run out of control, the need to avoid risk holds up the price of the money. This week, the probability of a high rate of gold shocks depends on what the market is more afraid of: fear of rising interest rates, or fear of inflation. While crude oil is more dependent on supply and demand and geography, the conflict in Iran is still fermenting, and if the increase is due to higher oil prices that drive inflation, oil may not fall immediately. But if market demand starts to slow down, industrial metals and crude oil will continue to contract。

Credit and real estate are slow variables, but the direction is clear. High-yielding debt spreads can increase, financing costs are higher, and commercial properties, REITs, and mortgage-sensitive assets are under pressure. Emerging markets with high dollar-to-dollar debt ratios will also suffer even more, and capital flight pressures will rise。

The encryption market is also under pressure in this macro-level context. BTC is in the vicinity of $65,000, $72,000 at the beginning of June, and has fallen all the way to about $61,500 since the CPI was announced, and has only rebounded in the last few days. The position itself was unstable, and on June 5, when it fell by $62,000, the chain closed more than $1.5 billion, and bitcoin cash ETF net-out $2.7 billion a week. Prices have returned, but the silo structure is not healthy. BTC has a part of the macro asset attribute that does not necessarily collapse when it comes to interest rates, but it is difficult to grow independently. ETH, SOL, Yamato, Meme, and Small Market Values are more vulnerable, and these assets feed on liquidity spillovers and risk preferences, and high Beta assets are the first to be cut off once the market begins to recompile cash, short-term debt, and IMF returns are attractive. Contract market rates have fallen, chain-based risk preferences have cooled, and have appeared once in early June。