Big Escape: The Golden Exit Channel, lost in encryption

IN FRONT OF THE HIGH-QUALITY PROJECT, THE VC BEGAN TO MOVE FROM FILTER TO SELECTED

Original title: The Great Act of Crystal VCs

Photo by Catrina

Original by Peggy, Block Beats

The editor presses that when the "transmitting currency" is no longer valid, the encryption wind is beginning to lose its strongest logic。

over the past three cycles, tokens have been the central path to capital recovery and the magnification of returns. the industry has built a familiar set of rhythms around this premise: early financing, narrative expansion, online circulation, and price realization. however, the mechanism is becoming ineffective in the context of chain income becoming a new threshold, meme currency diversion liquidity, and the spillover of diaspora funds to more risky assets。

a more direct change is that returns on token projects are expected to be compressed, while the equity path is again attractive. early investors are beginning to be more cautious about the exit of the “currency” project, while later funding is directed towards the “web2.5” company with real income and expected m&as. the encryption industry is no longer in a relatively closed competitive environment, but is forced to enter the realm of playing with traditional financial technology funds。

IN THE PROCESS, A DEEPER QUESTION EMERGES: WHAT CAN VC OFFER WHEN CAPITAL ITSELF IS NO LONGER SCARCE

OVER THE PAST FEW YEARS, SOME OF THE MOST REPRESENTATIVE PROJECTS HAVE ALMOST BYPASSED INSTITUTIONAL CAPITAL BY ESTABLISHING NETWORK EFFECTS AND INCOME MODELS DIRECTLY. THIS MEANS THAT THE FUNDS ARE NO LONGER “PASSES” FOR ACCESS TO QUALITY PROJECTS. FOR THE FOUNDERS, THE INTRODUCTION OF VC DEPENDS ON WHETHER THE LATTER CAN PROVIDE CLEAR BRAND ENDORSEMENTS AND REAL INCREMENTS, NOT JUST BOOK MONEY。

Under the new market structure, encrypted windfalls need to find their own “product definition”. Otherwise, it would be one of the targets to be phased out during the cycle。

The following is the original text:

The encryption wind is at a watershed moment. The withdrawal of tokens has been the main source of excess returns over the past three cycles, but the model is now undergoing a substantial replacement. What kind of token is valuable is being revised in real time, while a uniform assessment framework has not yet been developed at the industry level。

So, what the hell happened

The change in the encryption market structure of this round is the result of a multiplicity of forces that have never existed in the same cycle before:

1/HYPE WAS BORN OUT OF NOWHERE AND FROM THE FLANKS HIT THE ENTIRE CURRENCY MARKET. IT PROVES ONE THING: THE PRICE OF A TOKEN CAN BE SUPPORTED BY REAL INCOME, WITH 97 PER CENT OR MORE OF ITS NINE OR TEN-DIGIT INCOME COMING FROM THE CHAIN. THIS CASE QUICKLY TRIGGERED THE MARKET’S COLLECTIVE DISILLUSIONMENT WITH THE “DISSEMINATION-DRIVEN, BUT WEAK” GOVERNANCE TOKENS – WHICH, ACCORDING TO ONE OF THE MOST IMPORTANT EXAMPLES, ARE BEING USED AS A TOOL FOR THE MANAGEMENT OF THE MONEY. I DON'T KNOW. FOR EXAMPLE, EARLY L1S AND "GOVERNANCE TOKENS" THAT WERE USED MAINLY TO CIRCUMVENT SECURITIES REGULATION BUT WERE DIFFICULT TO DISTRIBUTE DIRECTLY. ALMOST OVERNIGHT, HYPE HAS RESHAPED MARKET EXPECTATIONS: INCOME CAPACITY IS NO LONGER A SUBDIVISION BUT A MINIMUM THRESHOLD。

2/ Corresponding shocks to other projects: Prior to 2025, if a project had a chain income, it would often be treated as a security; and after HYPE, without a chain income, in the view of most hedge funds, zeroing the project is a matter of time. This has left the vast majority of projects, particularly non-DeFi projects, in a dilemma and hastily reoriented。

/ PUMP dropped a severe "supply shock" on the system. The feverishness of meme coins has led to explosive increases in the supply of tokens, fundamentally disrupting the market structure — attention and liquidity being severely distracted. In Solana alone, the number of new coins issued rose from about 2000-4,000 per year to a peak of 40,000-50,000, or about 20 times the size of a cake with little growth in liquidity. The same amount of money and attention that had sought high returns had begun to move away from holding the Shan dollar to trading in the short term for meme。

4/ SUBSTITUTION OF FUGITIVE RISK FUNDS IS ALSO INCREASING RAPIDLY. THE MARKET, STOCK RENEWAL CONTRACTS, LEVERAGE ETFS, ETC. ARE DIRECTLY COMPETING FOR THE PORTION OF THE MONEY THAT ORIGINALLY WENT INTO ENCRYPTED STOCK. AT THE SAME TIME, THE MATURITY OF ASSET-BASED MONETIZATION TECHNOLOGIES ALLOWS INVESTORS TO LEVERAGE BLUE-CHORUS STOCKS THAT ARE NEITHER AT RISK OF ZERO, AS IS THE CASE WITH MOST OF THE BANKNOTES, BUT ARE SUBJECT TO STRICTER REGULATION, MORE TRANSPARENT INFORMATION AND LESS INFORMATION-FRIENDLY。

Together, these changes have resulted in a significant reduction in the currency life cycle. The cycle from the high to the low has been significantly shortened, and the "long-term hold" of the dispersed households has declined sharply, replacing it with faster financial rotation。

Core issues

Against this background, almost all of these investments are rethinking several core issues:

1/ Are we investing in equity, tokens or a combination of both

The biggest difficulty is that there is no mature paradigm of how the value of a token is accumulated. Even the head project like Aave, between DAO and equity structures, continues to be controversial。

2/ What is the best practice of chain value accumulation

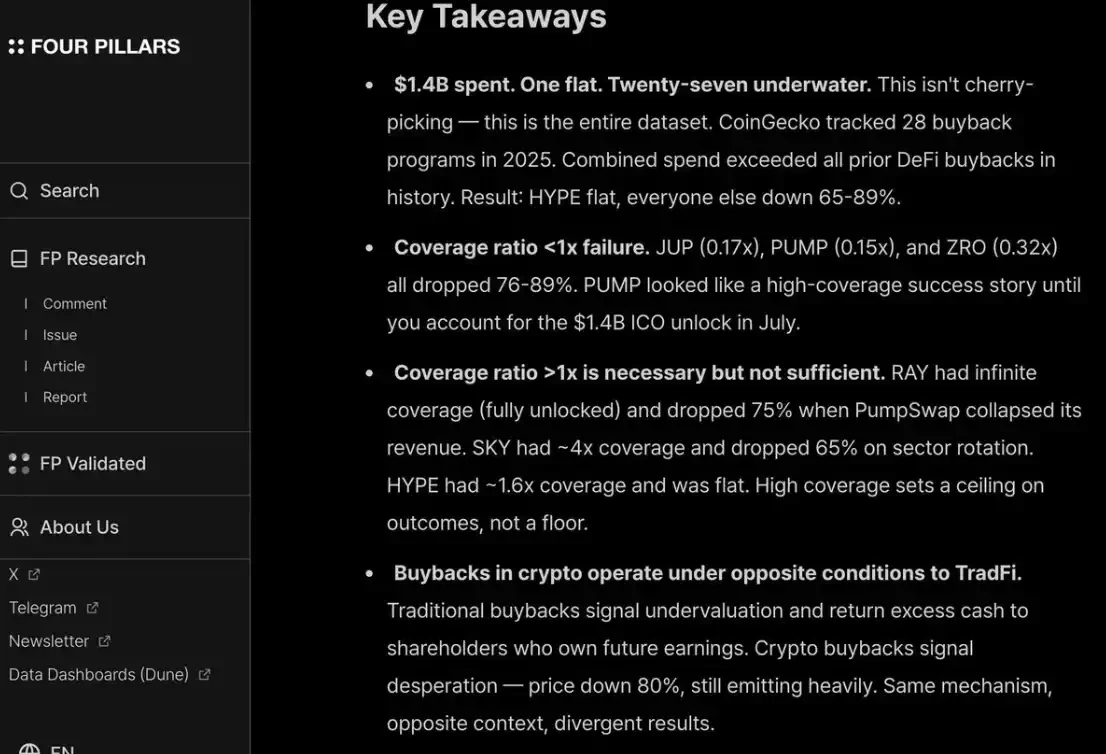

The most common current practice is to repurchase tokens, but "common" does not mean "right". We have long been opposed to the dominant buy-back logic: this mechanism is “toxic” and it can create dilemmas for those with real income capacity。

The problem is that its motivation was wrong from the beginning。

Traditional firms buy back stocks, often when growth investment opportunities are reduced or stock prices are underestimated; while the repurchase of encrypted projects is often forced to "immediately implement" — under pressure from the diaspora and market opinion — which is highly emotional and unstable. You could have just put out $10 million for the buyback, which could have been reinvested, and then the next day you were completely swallowed by the market because one of the traders had been flattened。

listed companies buy stock back at a time of underestimation; coin buybacks are often ambushed (front-run) and executed at local heights。

IF YOUR BUSINESS IS A B2B MODEL BASED ON BOTTOM INCOME, THIS BUY-BACK IS ALL THE MORE FUTILE. FROM MY PERSONAL POINT OF VIEW, AT A TIME WHEN ANNUAL INCOME IS LESS THAN $20 MILLION, REPURCHASES ARE MADE IN AN ATTEMPT TO PLEASE THE DISPERSED HOUSEHOLDS WITH LITTLE JUSTIFICATION — FUNDS THAT SHOULD HAVE BEEN PRIORITIZED FOR GROWTH。

i agree with a report/interception by fourpilars that even ten-digit buybacks can hardly make a substantial contribution to the project's long-term price base。

IN ADDITION, IN ORDER TO PLEASE BOTH THE DISPERSING AND HEDGE FUNDS, YOU HAVE TO REPURCHASE THEM IN A CONTINUOUS AND TRANSPARENT MANNER, LIKE THE HYPE. AS LONG AS THIS IS NOT POSSIBLE, THE MARKET WILL BE PUNISHED AS PUMP — ITS COMPLETELY DILUTED VALUATION (P/F) IS ONLY SIX TIMES MORE, BECAUSE THE MARKET “DOES NOT TRUST” IT. DESPITE THE FACT THAT IT HAS BURNED DOWN $1.4 BILLION OF REVENUES THAT COULD HAVE ENTERED THE TREASURY。

3/ "crypto premium" will be completely eliminated

This means that the valuation of all future projects may return to areas like traditional municipal companies — roughly 2-30 times their income。

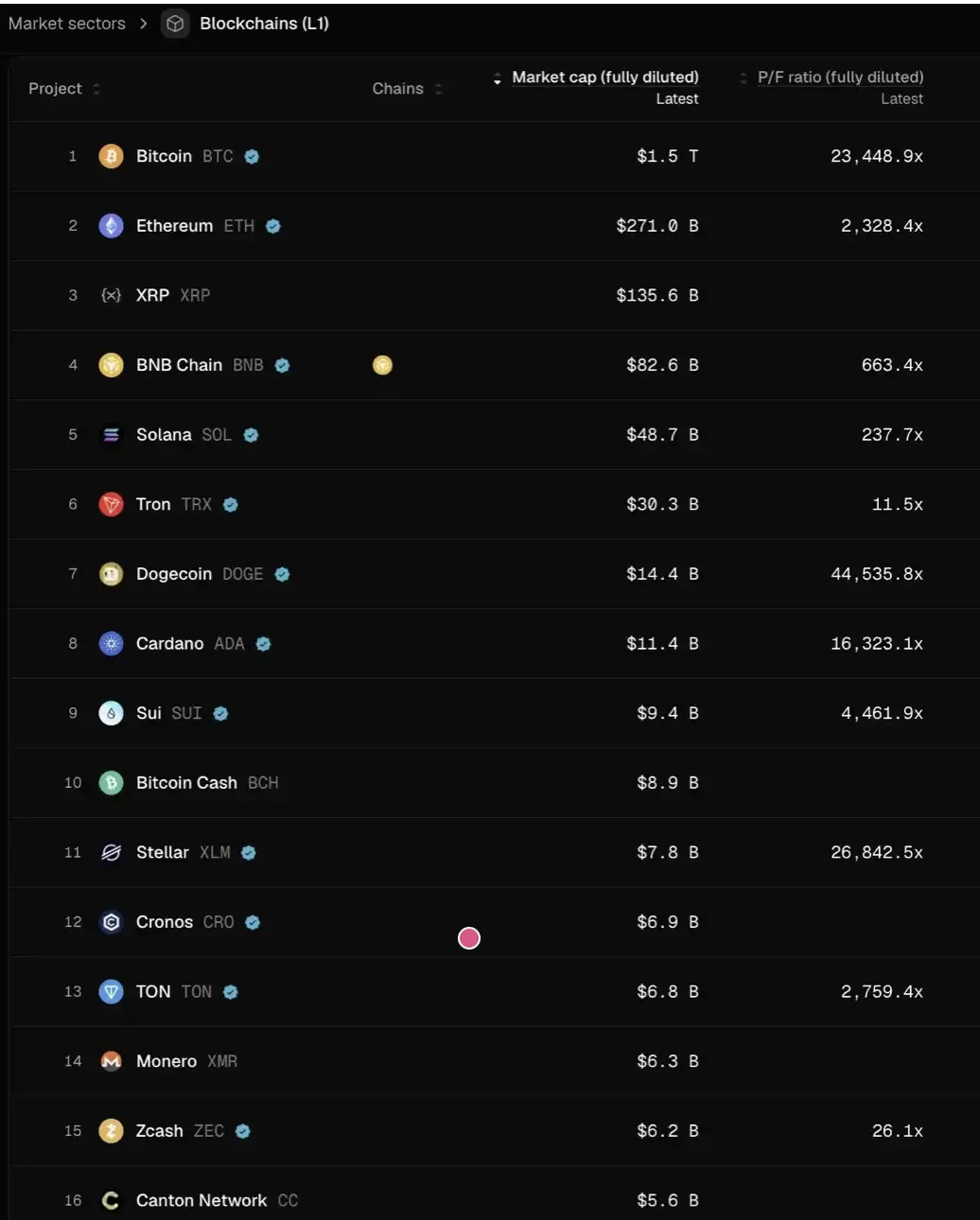

Think about what this means: if this judgement is true, most L1 prices, at current levels, may need to fall by more than 95% to match this valuation system. There are only a few exceptions — such as Tron, Hype, and other DeFi projects with real income — that can be relatively stable。

and this has not taken into account the additional push caused by the unlocking of coins。

I personally do not think that the situation will come that far. The HYPE actually created a “unusual” market expectation that investors would become impulsive about whether early projects had an “online or income/user growth”. This is a legitimate requirement for payments, DeFi, and “continuing innovation”; but for “subversive innovation”, it would have taken time to build, publish, grow, and truly generate income。

Over the past two cycles, we have quickly moved to another extreme — to bet on the DeFi project — from over-tolerance of “subversive technologies” to the highly abstract narratives of the new L1, Flashbots/MEVs, which are 8-9 rounds of financing, “hopium”. This is inherently an overcorrection。

But the clock will turn back。

For the DeFi project, pricing "quantitative fundamentals" is indeed a sign of industry maturity; but for non-DeFi tracks, "qualitative fundamentals" cannot be ignored: culture, technological innovation, subversive ideas, security, decentrization, brand values, and industry connectivity. These dimensions are not simply reflected in TVL or chain buyback data。

So, what happens next

The returns for token projects have been significantly reduced, while equity-type operations have not experienced the same level of cooling. This division is particularly evident in early and long-term investments:

At an early stage, investors became more price-sensitive to projects that “future exit in tokens”; at the same time, interest in equity-based projects increased significantly, especially in the context of the current relatively friendly M&A environment. This is in stark contrast to 2022-2024. At that time, the exit was the default path, with the assumption that the "valuation premium would continue"。

At a later stage, investors with brand advantages and resource capabilities in the encrypted original language are moving away from a purely "crypto-native" project and betting on more "web2.5" companies – whose valuation logic is more anchored in real income growth. It also brings them into an unknown competition field: the need to compete directly with cross-border funds and traditional Web2 financial science and technology funds (such as the Libbit Capital or the Foundations Fund), which accumulate more deeply in traditional financial contexts, portfolio synergies and early project acquisition capacity。

the whole encryption industry is entering a "attribution period"。

WHO CAN STAY DEPENDS ON THEIR ABILITY TO FIND THEIR OWN PMF IN THE MINDS OF THEIR FOUNDERS – A PRODUCT THAT IS NOT ONLY FINANCIAL BUT ALSO A COMBINATION OF BRAND IDENTITY AND REAL EMPOWERMENT。

For quality projects, VC needs to "sell yourself to the founder" in order to qualify for Cap table. Particularly in the past few years, some of the most successful projects have hardly relied on institutional capital (e.g. Axiom) or even had no financing (e.g. HYPE). If a VC can only provide money, it's almost destined to be marginalized。

THE VC, WHO IS TRULY ENTITLED TO REMAIN ON THE CARD TABLE, MUST ANSWER TWO QUESTIONS CLEARLY:

First, what is its brand identity — why the best founders come to the door

Second, where is its value increase — ultimately determining its ability to win that deal。