Strategy's "Moneymarker": is STRC the Savior of Bitcoin or the Destroyer

25M TRADING VOLUME, 17204 BTCS

After more than two months of shock, there were finally signs of a breakthrough。

It's still old friend Michael Saylor who's leading the Bitcoin offensive, and this time he's using a new weapon: STRC。

Turning over Saylor's latest Twitter, you'll find he's doing content for STRC almost every day. This kind of bad publicity video by AI sends a clear signal: The man who pushed MSTR up on NASDAQ used the same marketing fire on STRC。

Why would he do that? Because STRC is now the only tool that Strategy can convert market money into BTC buys. Every large-scale BTC increase announced by Strategy over the last three months is directed to STRC。

WHAT IS IT

STRC, fully known as Variable Rate Series A Perpetual Stretch Prefered Stock, a permanent priority unit issued by Strategy, came online in November of last year。

It operates along the following lines:

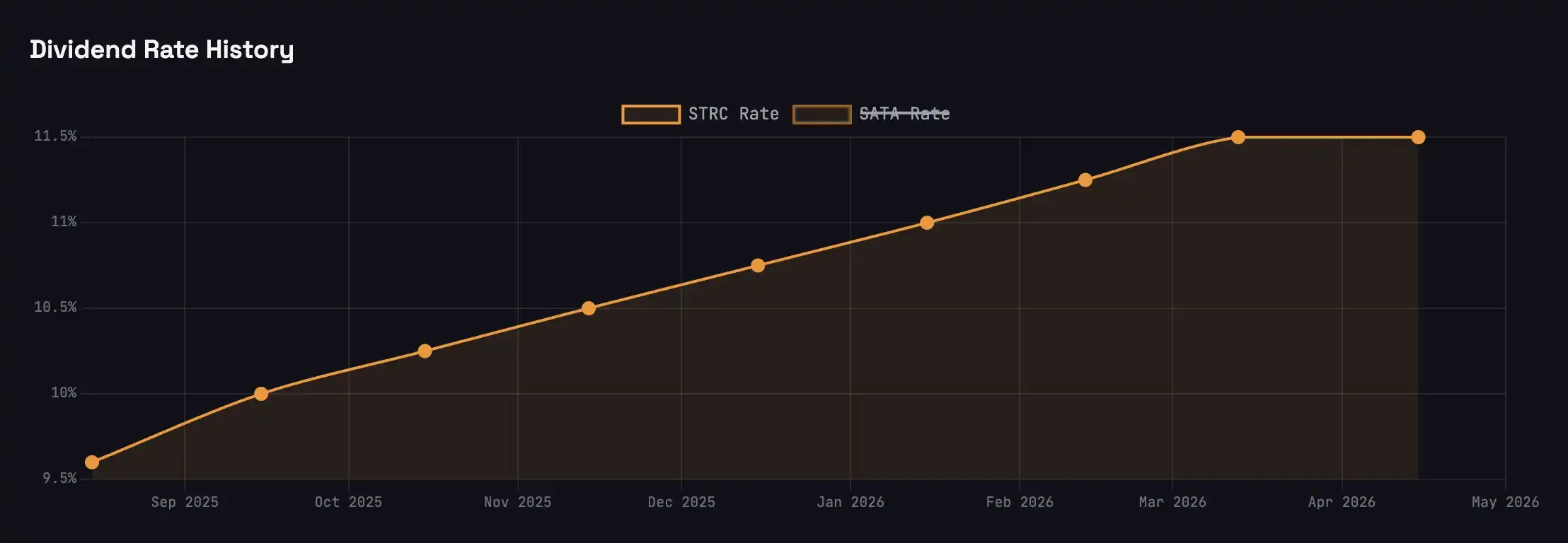

You spent about $100 on a share of STRC. Strategy's monthly cash contribution is 11.5 per cent, or approximately 96 cents per share per month. It never matures, Strategy does not have to repay the principal。

The stock price was anchored near the $100 nominal value by adjusting the rate of the rate: it fell and the rate went up and sucked the purchaser back; it went up and the rate went down and the price went down. The maximum monthly rate adjustment is 25 basis points。

Only when the STRC share is over $100 would Strategy be able to raise new equity funds in nominal terms - a precondition for the whole wheel. The bulk of the increase, net of the dividends reserve, was used to purchase BTC。

Saylor's name for the product is "Long-term high-yield credit", or "bitcoin-supported money market fund". At the time of the US debt return of about 3.5 per cent, STRC offered a three-fold return on US debt。

Flying wheel

A common misconception about Saylor is that he buys BTC with unlimited print money。

He can't. Saylor can't print money. He has to wait for the market to hand it over to him. For every extra share, STRC presupposes that real marginal buyers are willing to buy it at $100。

The buyer of STRC is essentially making a credit "trading", and the rate of return from STRC is 8 per cent higher than the national debt as compensation for Strategy's credit risk。

HOWEVER, MANY OF THE SRC BUYERS DO NOT KNOW THAT THEY BUY THE SRC FUNDS, WHICH WILL BE TRIPLY AMPLIFIED AND CHANNELLED TO THE BTC。

Strategy has an open financial target: 33% leverage。

The share of SRC, STRF, STRK, which is the source of funding for the company as a whole, remains at about one third, with the remaining two thirds coming from the MSTR general share. Saylor called this principle "intelligent leverage". This means that whenever Strategy gets $1 through STRC, in order to hold 33% of the leverage line, they have to combine MTRs of about $2 with BTC. 1 US$ STRC + 2 MSTR = 3 US$ BTC buy。

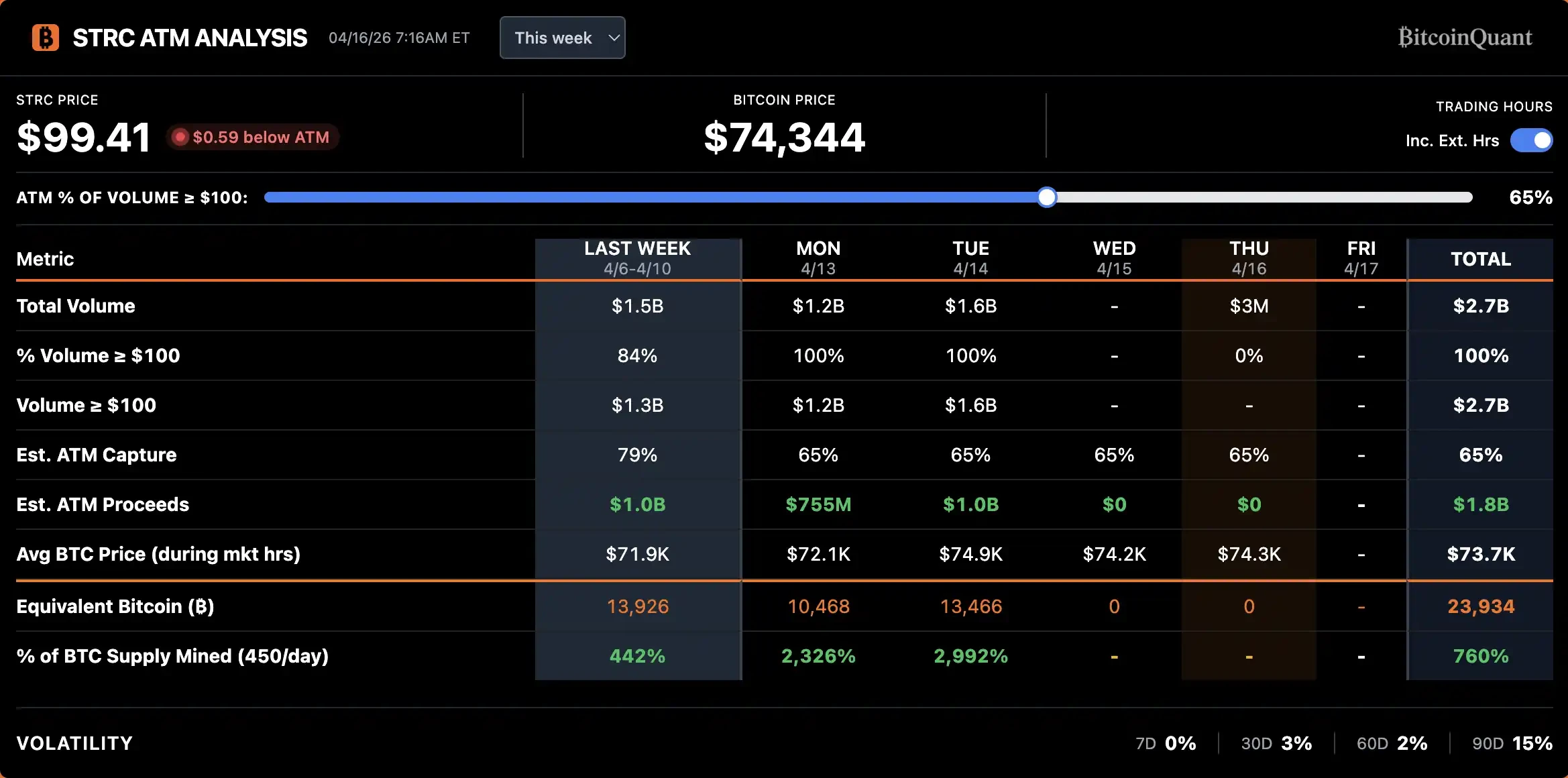

On April 14th, Strategy collected about $1 billion a day through STRC. Press three times the size of the BTC buyout of about $3 billion, which corresponds to the BTC increase of two weeks before the April break。

When the BTC falls, the collateral shrinks, and the credit risk of the STRC rises, Strategy has to raise the rate to compensate for the new level of risk. The higher the rate, the greater the pressure of cash flow, the higher the probability of default. This is an unstable feedback. Last October, in the period between $120,000 and $60,000 BTC's waist, the SRC rate was reduced from 7% to 11.5% on the way, before the purchase was pulled back。

The BTC, in turn, is more attractive and demand is further amplified when the BTC is steadily rising, the collateral is thicker, the credit quality is improved and the STRC is more attractive at the same rate of spread. In April, BlackRock's Prefered and Income Security ETF ranked Strategy's priority share as the second largest holder, raising its market value from approximately $200 million in March to $344 million, as a direct endorsement of Strategy's current credit position by the solid collection agencies。

Strategy's flyer has turned positive: more money to buy STRC → Strategy, supported by 3 times magnified BTC prices, stronger STC mortgage base, more attractive to buy STRC under a credit spread compression rate。

The arbitrage of the sabbatical day

PRIORITY SHARES HAVE DIFFERENT INTEREST-RATE MECHANISMS AND BONDS. THE BOND IS MAINTAINED ON A DAILY BASIS AND YOU ARE ENTITLED TO ONE DAY ' S INTEREST ON A DAILY BASIS; PRIORITY SHARES ARE ISSUED ON A FIXED DATE. FOR STRC, YOU GET A FULL 96-CENT MONTHLY DIVIDEND AS LONG AS YOU HOLD IT WHEN YOU CLOSE ON THE DAY BEFORE THE INTEREST DAY。

THIS GIVES A CLEAR ARBITRAGE WINDOW: A FEW DAYS BEFORE THE BREAK-OFF, THEY CAME IN AND BOUGHT, TOOK THE DIVIDENDS AND SOLD THEM THE NEXT DAY. DATA FROM THE LAST FEW MONTHS SHOW THAT THE AVERAGE DROP IN STRC AFTER THE ELIMINATION WAS ABOUT 20 CENTS, MUCH LESS THAN 96 CENTS OF DIVIDENDS PER SE. THE NET GAIN OF A SINGLE INTEREST-DEPRECIATION ARBITRAGE CAN BE APPROXIMATELY 40 TO 50 CENTS。

The arbitragers will not miss this opportunity。

AS SHOWN IN THE FIGURE, THE AMOUNT OF EXCHANGE BEGINS TO CLIMB ONE WEEK BEFORE THE END OF THE INTEREST DAY, EITHER ON THE DAY OF THE END OF THE DAY OR ON THE DAY BEFORE THE END OF THE DAY. THIS ROUND IN APRIL IS SIGNIFICANTLY STEEPER THAN IN MARCH, INDICATING THAT MORE AND MORE FUNDS ARE BEGINNING TO PARTICIPATE IN THE STRC'S INTEREST RATE ARBITRAGE。

However, such arbitrage may not be a good thing。

FOR THE SRC PRODUCT ITSELF, TWO OR THREE WEEKS AFTER THE BREAK-OFF WILL ENTER THE "DEAD ZONE" — A SHRINKING LIQUIDITY, A WIDENING TRADE PRICE GAP, AND A STOCK PRICE OF LESS THAN $100 FOR A LONG TIME. THIS REPEATED LOSS OF ANCHORS ERODES THE LOCATION OF STRC AS A "MONEY MARKET PRODUCT" AND PUSHES IT INTO A MORE MONTHLY VOLATILE BOND PATTERN。

For Saylor, his BTC buys easy to be robbed with arbitrage. STRC growth concentrated on two weeks before the break, which means that he bought BTC moves focused on those two weeks。

Now arbitrage traders come in every month at the same time to buy STRC, and they know that Saylor is about to take the money to the spot market to clean up the BTC, so he can buy the BTC in advance, wait for Saylor to push up the price and raise the purchase cost for Saylor。

In the last two weeks, after the break, the Coinbase spot premium increased significantly

The solution would be to change the frequency of the yield from monthly to weekly, for example, by apportioning the arbitrage gains; or to introduce a more primary and more frequent derivative product that would spread out concentrated arbitrage。

As a matter of fact, Saylor acted quickly and announced on Saturday that Strategy had submitted a power of attorney to work out a change in the frequency of STRC dividends payments from monthly to semi-monthly. Annual dividends payment obligations and rates remain unchanged。

If the proposal is approved, the first half-month share will be released on 15 July。

According to Birtwise consultant Jeff Park, there is currently no half-monthly dividends mechanism for corporate bonds on the market, and the preferences of the diaspora investors for higher-frequency payments have been demonstrated by the success of products such as weekly dividends of ETF。

More deeply, Jeff Park sees this as a landmark step in the penetration of the vision of "flow payments" in the encrypted currency industry into traditional capital markets: The frequency of interest payments is in essence a reflection of the efficiency of currency dynamics into kinetic energy, and the digital monetary age should have broken artificial time-cycle limits。

IN HIS VIEW, STRC HAD SET A NEW PARADIGM FOR TRADITIONAL ENTERPRISES AND LOOKED FORWARD TO THE EVOLUTION OF FUTURE PAYMENTS FROM HALF A MONTH TO DAY AND EVEN INSTANTANEOUS。

DeFi's new narrative

The appearance of STRC brought a living water to the pale DeFi market。

DeFi's stable currency gains have been downhill for the past year. Aave's deposit on the stable currency is about 2% annually, Ethena's USDe and Sky's USDS are below 4%, and even Pendle's mainstream stable currency PT can hardly break 6%. This level of return corresponds to the risk exposure of the AI-era smart contract, and the risk returns have discouraged many DeFi veterans。

DeFi needs a credible, large enough source of revenue to pull Tradfi's money back into the chain, and STRC just provides this opportunity。

TWO PROJECTS ARE TRYING TO PACKAGE THE PROCEEDS OF STRC ON THE CHAIN:

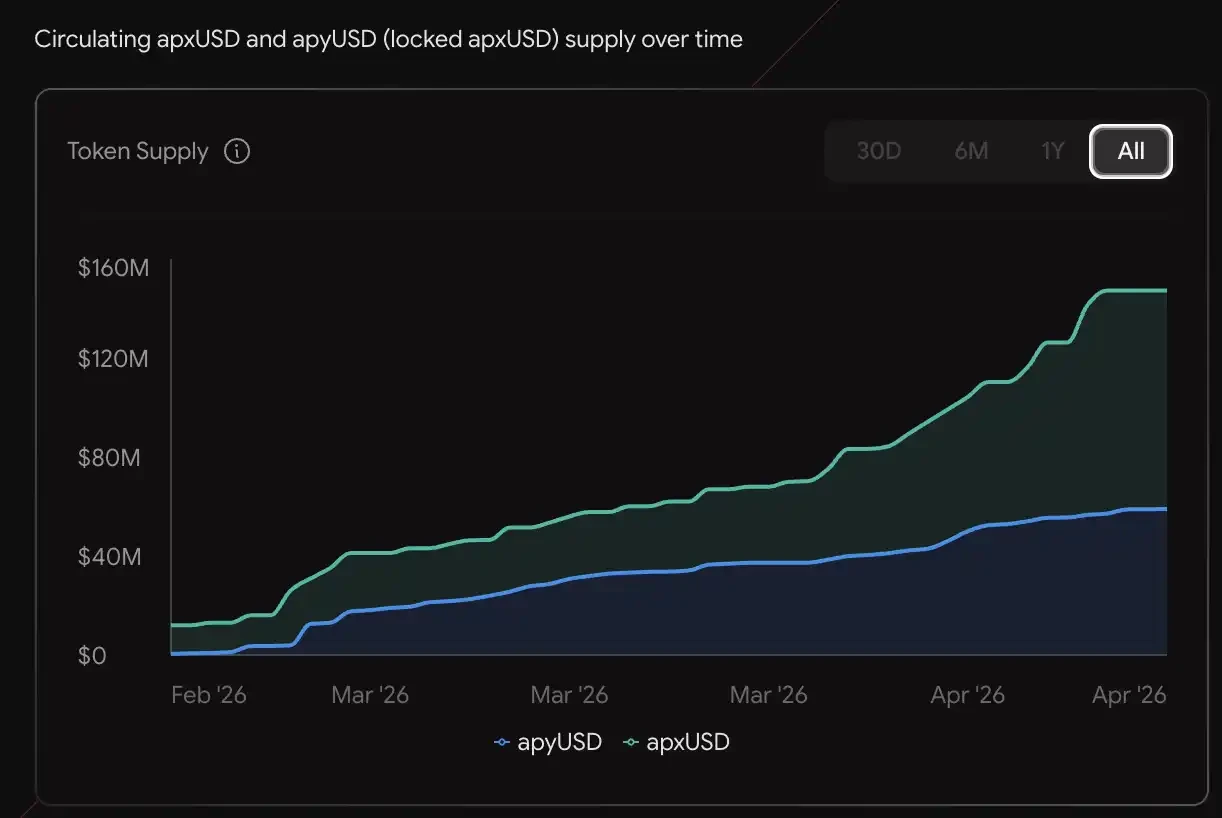

Apyx Protocol uses a two-currency model. ApxUSD is the base stabilization currency, supported by preferential shares and over-collateralization of United States debt such as STRC, SATA; apyUSD is the pledge version, which carries the underlying dividends and interest earnings and is now about 12.78 per cent annualized. The supply has reached $130 million, with corresponding gains and leverage on Pendle and Morpho。

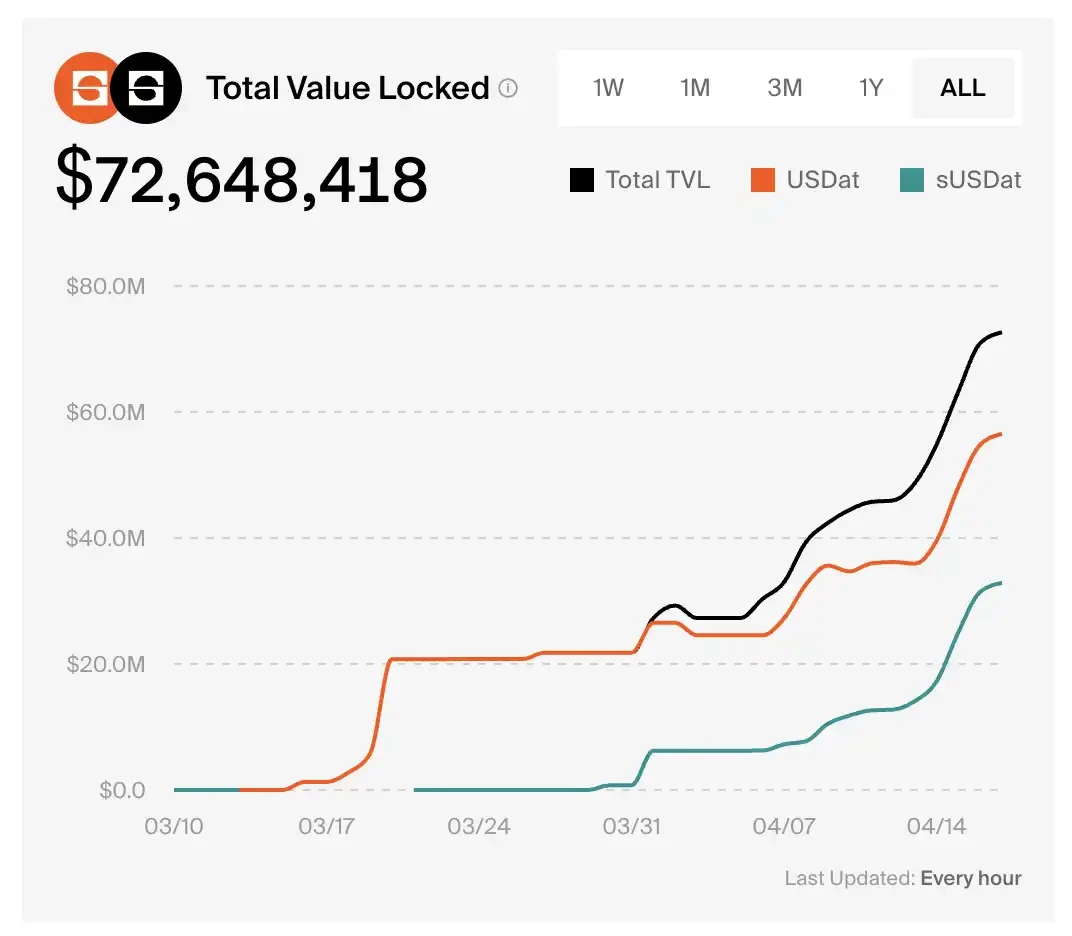

Saturn Credit's sUSDat is a pledge interest-stabilized currency to carry the proceeds of STRC, and the agreement TVL has been running from zero to $72.6 million over a month。

PT-sUSDat has a current annualized rate of return of 9.2 per cent, according to Pendle Practise。

What's wrong

The more successful this well-designed financial machine works, the more difficult it is to avoid。

Strategy's currently holding BTC is close to 3.5 per cent of the total and continues at billions of dollars a month。

BTC, WHAT WAS THE ORIGINAL VALUE PROPOSITION? A MONETARY ASSET THAT IS DECENTRALISED AND DOES NOT DEPEND ON ANY SINGLE ENTITY AND THAT NO ONE CAN UNILATERALLY MANIPULATE。

WHEN THE PERMANENT PRIORITY OF A LISTED COMPANY BECOMES BTC — A DECENTRALISED, NON-DEPENDENT ENTITY THAT CANNOT UNILATERALLY MANIPULATE A MARGINAL PURCHASE OF MONETARY ASSETS, IS BITCOIN DEPARTING FROM ITS ORIGINAL FORM