The Korean encryption exchange was forced to "scramble the dog" after missing the currency stock wave

South Korea ' s regulatory measures aimed at protecting investors now pushes the encryption exchange to the most speculative corner of the market。

Original fromFour Pilars

Compile / Odaily Daily Planet Golem()@web3 golemI'm not sure

The editor presses: On June 16, the Korean Exchange, Bitumb, came on line with a local dog coin called Spacecoin, followed by Upbit with an outdated Meme currency SPX6900. There is a general perception in the community that the two tokens of Korea's two major encrypted exchanges are on the line because they coincide with SpaceX's stock code and the exchange wants to use it as a “dog” to attract trade。

AGAINST THE BACKDROP OF A WEAK ENCRYPTION MARKET AND THE SHIFT OF KOREAN ENCRYPTED INVESTORS TO STOCK EXCHANGES, THE SOUTH KOREAN EXCHANGE’S COLLECTIVE DECLINE IN Q1 PERFORMANCE IN 2026 MADE IT URGENT FOR THEM TO TAKE MEASURES TO SAVE THE DECLINE. HOWEVER, UNLIKE OTHER OVERSEAS EXCHANGES, WHICH CAN BE TRANSFORMED INTO A “GOODS EXCHANGE” WHERE A LARGE NUMBER OF OFFLINE TOKENIZED SHARES MEET THE NEEDS OF ENCRYPTED TRADERS, SOUTH KOREA CLASSIFIES TOKENIZED SHARES AS SECURITIES, THUS PROHIBITING SUCH TRANSACTIONS FROM BEING CARRIED OUT BY AN ENCRYPTED EXCHANGE, WHILE ALSO NOT ALLOWING AN ENCRYPTED CURRENCY FUTURES, DERIVATIVES, OR SPOT EXCHANGE TRADING FUND (ETF) TRANSACTION。

Korea's regulatory measures aimed at protecting investors have now pushed the encryption exchange to the most speculative corner of the marketI don't know. After all sources of income and new product lines, such as derivatives, monetized shares and forecast markets, are banned, exchanges, in order to increase the volume of platform transactions, tend to opt for “tub” coins that attract attention and are more speculative。

Upbit and Bitumb, "Pussy SpaceX Stock" online, shocked the Korean community

Bitumb and Upbit are online with a token similar to SpaceX stock code

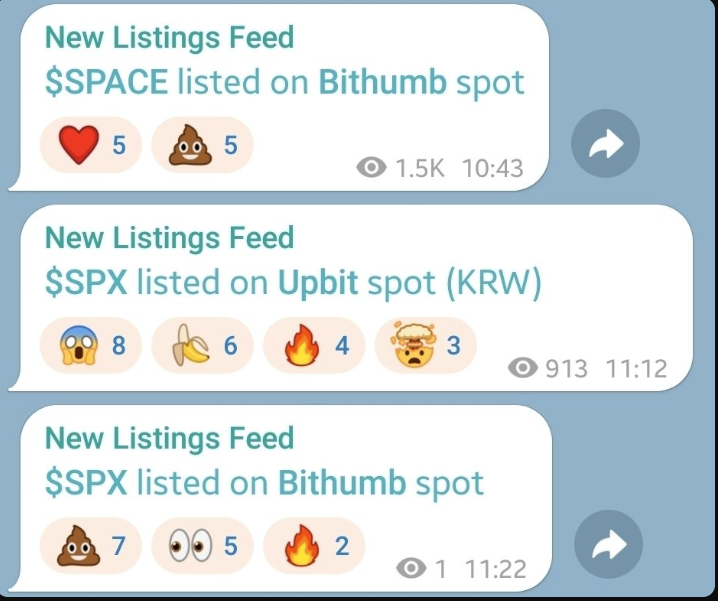

On the morning of June 16th, the most popular topics in the Korean community were Bithumb's unnamed project tokens, Spacecoin (SPACE) and Upbit, Meme coins SPX6900. One might ask, isn't that a common token announcement? The real trigger for community responses is not on the line itself, but on the token name and timing of both。

Four days ago, June 12th, SpaceX was listed in NASDAQ, stock code SPCX. As we all know, SpaceX’s IPO is the highest in history, and because stock-related issues are now dominant in Korea’s encrypted currency community, SpaceX has become the hottest in the field on weekends。

As a result, after Upbit and Bithumb issued currency announcements, a suspicion began to spread within the community that the token names and codes on the exchange were very similar to those of SAPX, in order to get heat and trade volumes. Although this connection is only a coincidence, this interpretation not only seems reasonable but also reflects the state of affairs on the Korean exchange。

Today, overseas platforms such as Coinbase, Binance and Bybit allow users to trade SpaceX and other foreign shares directly on the exchange, but due to regulatory constraints, the Korea Exchange is unable to provide such products, so they may have to build a token at least similar to SpaceX。

But this is not just a joke, it is a reflection of today’s difficult situation of Korea’s encryption exchange competing with its overseas counterparts。

Status of the Korean Exchange

Overall decline in performance, even losses

The South Korean two exchanges performed poorly in the first quarter of 2026。

Upbit 2026 Q1 Performance Source: FSS DART

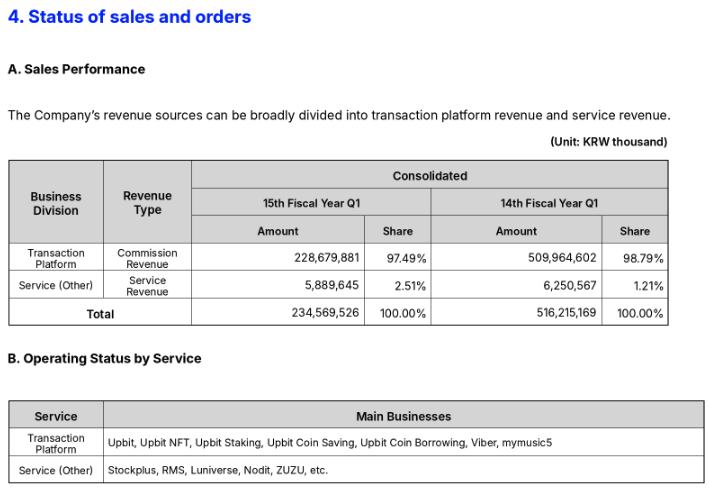

According to quarterly reports issued through the Korea Financial Supervisory Authority ' s electronic disclosure system in May 15, the combined revenue released by Dunamu, who operates Upbit, was 23.46 billion won, a decline of 54.6 per cent over the same period, a decline in operating profits of 77.8 to 88 billion won, and a decline in net profits of 78.3 to 69.5 billion won. Upbit’s fee revenue fell by 55.2 per cent to around 200 billion won, while operating costs rose by 22 per cent during the same period, resulting in a squeeze on profit margins。

Bithumb 2026 Q1 Performance Source: FSS DART

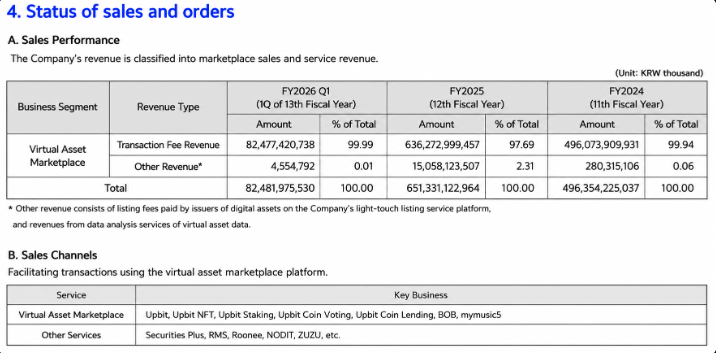

Bithumb is even worse. The first quarter saw a decline of 57.6 per cent to 82.5 billion won, a sharp decline in operating profits of 95.8 per cent to 2.9 billion won, a net corporate loss of 86.9 billion won, and a net loss for the second consecutive quarter. LossI don't know。The direct cause of the loss was a decrease of 87 per cent in fees revenue due to the shrinking volume of transactions. In addition, the Korean Financial Intelligence Agency (KOFIU) has imposed a fine of 36.9 billion won and a six-month partial closure for violating the Specific Financial Transactions Information Act, which is also reflected in its performance in the first quarter。

The biggest problem for the Korean exchange is that the revenue structure is almost entirely dependent on transaction feesI don't know. Transaction fees account for approximately 97.5 per cent of Dunamu ' s income and 99.99 per cent of Bithum ' s income, so they are in fact total income. However, rather than any oversight in the way the exchange operates, it is the regulatory environment (detailed below) in which Korean encrypted transactions face such a structure。

It's narrow in scope. It only supports encrypted spot transactions

Indeed, the operations that the Korea Encrypted Exchange is able to carry out are limited to encrypted spot transactions and are largely inaccessible to other areas, most of which are restricted, either expressly or implicitly. The following are the operations that the Korea Encryption Exchange is not allowed to perform:

- Currencyization stocksIn June 2026, the Korea Financial Services Commission and the Financial Supervisory Authority began to classify tokenized shares as securities rather than virtual assets. Regardless of the form of issuance, securities are governed by the Capital Market Act, under which only licensed electronic registries can register electronic rights. If an encrypted exchange that is not such a body issues or has a negotiable securities-type token, it is equivalent to an unlicensed business. In other words, the rapidly developing monetized stock abroad is an inadmissible asset in the structure of the South Korean currency exchange, and this is unlikely to change。

- Futures and derivatives: Korea's Encrypted Currency Exchange can only provide spot transactions and cannot provide domestic users with derivatives such as permanent futures or options. This is not so much an express legal prohibition as a shadow of an earlier attempt. Coinone, one of the five major South Korean exchanges, started operating four-fold-leveraged contractual trading services in December 2016 for about a year. By the end of 2017, the service had been completely closed as government regulatory measures and police investigations began. In 2018, the police viewed the service as a gambling activity on the grounds that it operated without the authorization of the financial supervisory authority, and referred Chief Executive Officer Cha Myung-hoon and others to the prosecution for the offence of running casinos, and even arrested 20 users for gambling with a value of over 3 billion won. Three years later, the case was closed in 2021 and was not prosecuted for lack of evidence. Since then, however, there has been no encrypted exchange in Korea involving leverage or futures trading。

- Self-regulating covert circumventionTHE KOREA ENCRYPTION EXCHANGE IS REGULATED BY THE DIGITAL ASSET EXCHANGE (DAXA), WHICH CONSISTS OF FIVE KOREAN WON EXCHANGES. ITS LISTING CRITERIA INCLUDE THE LACK OF TRANSPARENCY RESULTING FROM DE-LABELLING, THE POSSIBILITY OF SECURITIZATION AND THE POSSIBILITY OF MONEY-LAUNDERING. THESE STANDARDS EFFECTIVELY EXCLUDE PRIVACY CURRENCIES THAT EMPHASIZE ANONYMITY AND LEAD TO AN EXCHANGE AVOIDING BEING MOUNTED AS A TOKEN OF SECURITY. FOR THE SAME REASON, ASSETS THAT COULD TRIGGER SECURITIES OR GAMBLING DISPUTES, SUCH AS EXCHANGE TOKENS OR FORECAST MARKET TOKENS, ARE RARELY PRESENT ON THE KOREAN EXCHANGE。

In sum, almost all the new areas in which overseas exchanges are expanding, such as encrypted derivatives, monetized shares, and private currency and forecast markets, are restricted in Korea。

Korea Exchange is lagging behind in competition with the Global Exchange

Did the Korean exchange lower the currency

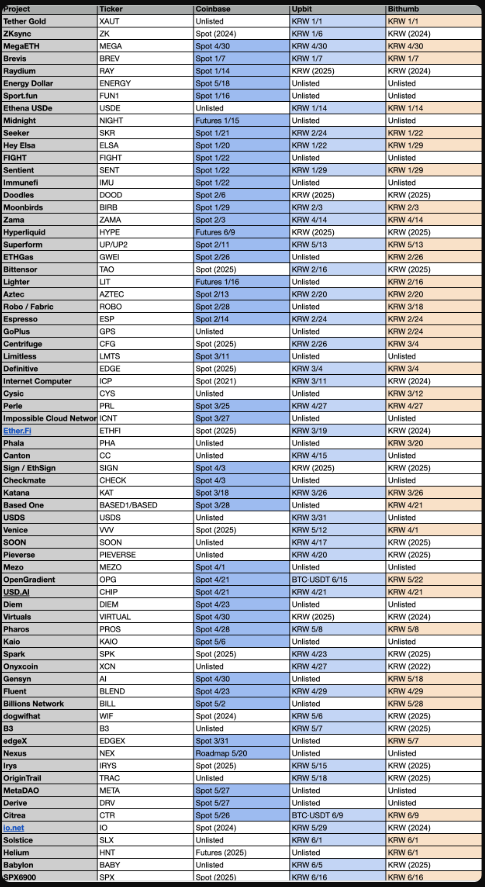

The community recently accused Upbit and Bithumb of relaxing the currency clearance criteria, and the following table is a complete comparison of Coinbase, Upbit and Bithumb's 2026 online tokens:

Coinbase, Upbit and Bithumb on line in 2026 Source: Four Pilars (@c4lvin)

In terms of the number of online tokens, Coinbase leads. Coinbase has built up assets that are not available on many South Korean exchanges, and a large proportion of them offer not only spot transactions but also contractual transactions that offer trading opportunities earlier than other trading platforms. Coinbase is actually more active in terms of frequency and timing。

In 2026, a significant portion of the large number of new Korean Won coins installed on Upbit were previously online on Bitumb, such as Bittensor (TAO), Internet Company (ICP), Ether.fi (ETHFI), O.net, dogwifhat, Spark (SPK) and Babylon, which were mostly on Bitumb. They are not newly issued assets, but rather tokens that already exist on the market, and they are included on the platform only after the UPbit is put on the table, which may make the UPbit's shelf not new enough。

The real reason for this perception of the decline in the quality of tokens is not the decline in standards per se, but the erosion of the volume effect of the above currencyI don't know. In an environment of rapidly drying up transactions resulting from the listing of single tokens and the increasing scarcity of new assets worth listing, Upbit maintains the speed of the currency through the use of existing coins at Bitumb。

Ultimately, the complaints of Korean users are not so much about a particular name as about the differences they feel in convenience compared to other markets, which have updated products such as monetized shares。

Korea Exchange is excluded from SpaceX public feast. Outside

At the same time, the direction of large overseas exchanges is the opposite. They are working to break the limitations of virtual assets by creating what is known as the Everything Exchange, a single application that can trade all assets。

The most striking of these is Coinbase. In its letter to shareholders in the fourth quarter of 2025, Coinbase stated that, in addition to encrypted currency and derivatives, it had started trading shares and ETFs in applications and had opened up some 300 million assets to early users with the aim of integrating traditional and digital assets into a unified portfolio experience. The letter also emphasized that Coinbase had become the first company in the industry to launch 24-hour United States-renewal contract products, thereby increasing its share in derivatives markets。

It's more direct when it comes to money. Since 1 June 2026, currency has opened United States stock transactions to eligible users, who can directly trade more than 7000 United States listed shares and ETFs. In addition, it has introduced bStocks, which monetize United States shares to one place in order to stabilize currency settlements, which can be retrieved to the user ' s own wallet and support round-the-clock transactions。

Bybit joins the xStocks Alliance and goes online with tokenized shares created by a regulated Swiss issuing agency, which track the coins supported by real shares and trade around the clock with stable coins。

In general, the overseas encryption trading platform has focused on monetizing shares. The difference in the South Korean and foreign trading environment is most evident in SpaceX's listing, which is a test of currencyization stock competition for overseas exchanges, with pre-contracting products and tokenization stocks。

Within 24 hours of the listing of SpaceX-related products, transactions in the entire encrypted currency market amounted to approximately $9 billion, of which $5.6 billion had been sold by the family alone。

By contrast, Korea’s encryption exchange is not allowed to participate in this feast, whether it be a monetized stock, a permanent contract, or any product tracking SpaceX. When the world's major exchanges deal billions of dollars around the same hotspot, the Korea Encryption Exchange has no access to it。

The Korean exchange is under pressure. Gas

For an exchange that cannot compete with the rest of the world in terms of product types, the only remaining battlefield is the encryption market. The revenue of the South Korean exchange is in fact dependent on spot transaction fees, and the only way to boost transactions in an environment where derivatives and stocks are neither available nor available is to turn on coins that attract investors’ eyes at the right time。

Korea ' s strict regulation of the encryption exchange is aimed at protecting investors. It treats leverage transactions as gambling and prohibits them, filters out securities-type tokens whose power structures are not transparent and excludes assets that can easily be used for money-laundering or price manipulation from the examination of the currency。

However, as this protection mechanism deprives the exchange of its sources of income and product lines on a case-by-case basis, their only remaining means is to go online and encrypt the spot. As the volume of transactions in the encrypted market shrinks, the more the South Korean exchange tends to go online with more focused and thus speculative assets. Protection at the product stage will eventually fuel the influx of speculative assets at the upfront currency stage, a trend epitomized by the fact that the two main exchanges are on line with SpaceX stock codes。

The deeper problem is that even such protection mechanisms are not entirely effective. Korean investors who want to buy permanent contracts or tokenized shares will not easily give up their demand, and they will turn to overseas platforms such as Money Ann, Bybit and Hyperliquid。

In other words, South Korean regulation by itself does not eliminate high-risk transactions by investors, but simply pushes high-risk transactions outside markets that the Korean authorities cannot regulate。WHEN TAX AND CROSS-BORDER INFORMATION EXCHANGE (CARF) BECAME FULLY EFFECTIVE IN 2027, THE SCALE OF SUCH OFFSHORE TRANSACTIONS WAS REFLECTED IN THE DATA. ULTIMATELY, INVESTORS BEAR THE RISK OF SPECULATION IN ANY CASE, WHILE LOSING DOMESTIC REGULATORY SAFEGUARDS, WHILE THE KOREAN EXCHANGE LOSES THE REVENUE THAT THOSE TRANSACTIONS WOULD HAVE GENERATED。

This structure has also made the Korea Exchange itself vulnerable, with single products, almost all of their revenues, derived from transaction fees and exposed entirely to fluctuations in the trading cycle. Coinbase spreads its revenues across such operations as trusteeship, currency stabilization, tokenization stocks and derivatives to buffer the down-market cycle, while the Korean exchange must rely on a single product to sustain the same cycle. As this gap accumulates over the season, it eventually evolves into a difference in investment capacity and product competitiveness, and this difference will again manifest itself, as does the convenient gap felt by domestic users。

OF COURSE, THE KOREAN GOVERNMENT IS ALSO PUSHING FOR ENCRYPTED CURRENCY REGULATION. THE GOVERNMENT'S COMMITMENT IS FULLY DEMONSTRATED BY THE FACT THAT THE SECOND PHASE OF THE ORGANIC LAW ON DIGITAL ASSETS, THE INSTITUTIONALIZATION OF THE SECURITIES-TYPE CURRENCY ISSUE (STO), THE APPROVAL OF COMPANY TRANSACTIONS, THE ISSUANCE OF THE KOREAN WON STABILIZATION CURRENCY AND THE ETF IN CASH WILL BE LAUNCHED SIMULTANEOUSLY IN 2026. HOWEVER, EVEN IF THESE NEW RULES WERE EVENTUALLY INTRODUCED, THEY MIGHT NOT BE OPERATED BY EXISTING ENCRYPTED EXCHANGES, BUT WOULD BE HANDED OVER TO HOLDERS SUCH AS SECURITIES FIRMS, ELECTRONIC REGISTRIES, ETC。

Thus, the convergence that is taking place is not the transformation of an encrypted exchange into a securities firm, but the acquisition of shares in an encrypted exchange by securities firms and banks and their integration into the same system. In 2026, Hanhua Investment Securities increased its shareholding in Dunamu to 9.84 per cent, making it the third-largest shareholder; Hanya Financial Group 6.55 per cent; Samsung Securities, Samsung Credit Card and Samsung SDS 4 per cent. Korbit was acquired by the Future Assets Group; Korea ' s investment securities signed a strategic equity investment agreement that acquired 20 per cent of Coinone ' s shares and became its third largest shareholder. Such alliances are growing rapidly as financial regulators are cautious about financial and encrypted currency segmentation and tend to ease restrictions。

Would Korea allow an encrypted exchange to evolve into a “everything exchange”, as it does abroad? This possibility is minimal。

But instead of advocating immediate deregulation, the article proposes a protective framework designed for an era, which, as markets move rapidly towards asset integration today, creates more hidden outcomes. Korea’s encrypted exchange, operating in such a harsh environment, in a bear-market like the current one, will shift these costs to users, and will eventually lead to the emergence, as today, of “dogs” with short-lived trading needs, resulting in more victims。