159 encryption protocols are known: with the exception of Hyperliquid, the coins with the repurchase mechanism are in loss

Repurchase and destroy? Take down Hyperliquid immediately. 。

This post is part of our special coverage Syria Protests 2011

Original language: Deep tide TechFlow

Introduction:This article tested six mechanisms to accumulate the value of tokens for 159 agreements and found that the scale of income was more important than the design of the mechanism - an average return of over $500,000 per day for agreements + 8 per cent and a minimum of 81 per cent. More critically, there are many mechanisms that look "win" and reverse immediately when one or two head items are removed, which is of direct reference value for investors to choose their tokens。

We've made a map of six mechanisms of value accumulation for 159 tokens, and we've tested the mechanisms that really translate into returns for currency holders。

Most of the narratives of the encryption industry on the accumulation of token value are wrong。

Research Settings

Two weeks ago, we released the report Investor Relations and Currency Transparency 2026. One finding was that 38 per cent of encryption agreements had an active value accumulated, and 62 per cent did not return any value to currency holders。

This article is a companion analysis. We got 159 protocol data sets, classified each token by cumulative mechanism, and pulled 1 year price performance from Artemis. The question is: What mechanisms are really translated into rewards

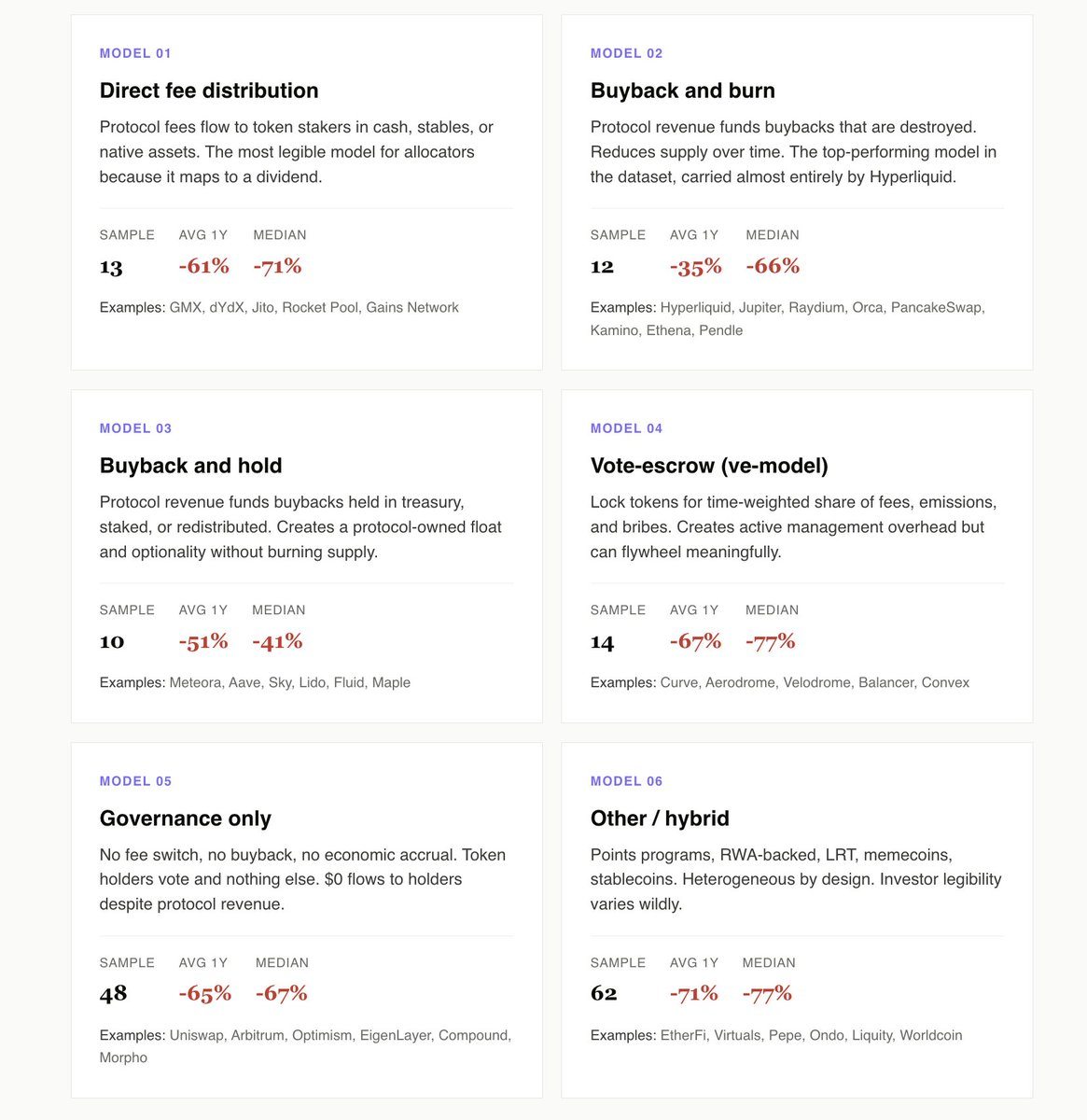

we identified six models: direct cost allocation, repurchase destruction, repurchase holding, voting hosting (v model), pure governance, and other/mixed models。

The following are our findings:

Active accumulation ahead of pure governance by 10 percentage points

direct costs, buy-back destruction, buy-back holdings and v models, 49 agreements, with an average return of -55 per cent over the past year. 48 pure governance agreements average - 65%。

The gap widens even further when it is limited to pure governance tokens that generate income, such as Uniswap, Arbitrum and Morpho. These agreements generate real income, but no money is given to the coin holders. The opportunity cost is the most visible part of the data concentration。

Pure governance is equivalent to an investor relations strategy whereby listed companies neither share the red nor buy back shares. The final configuration no longer pretends to be a going concern and begins to price it as a management awareness option。

Hyperliquid is the type of buy-back destruction

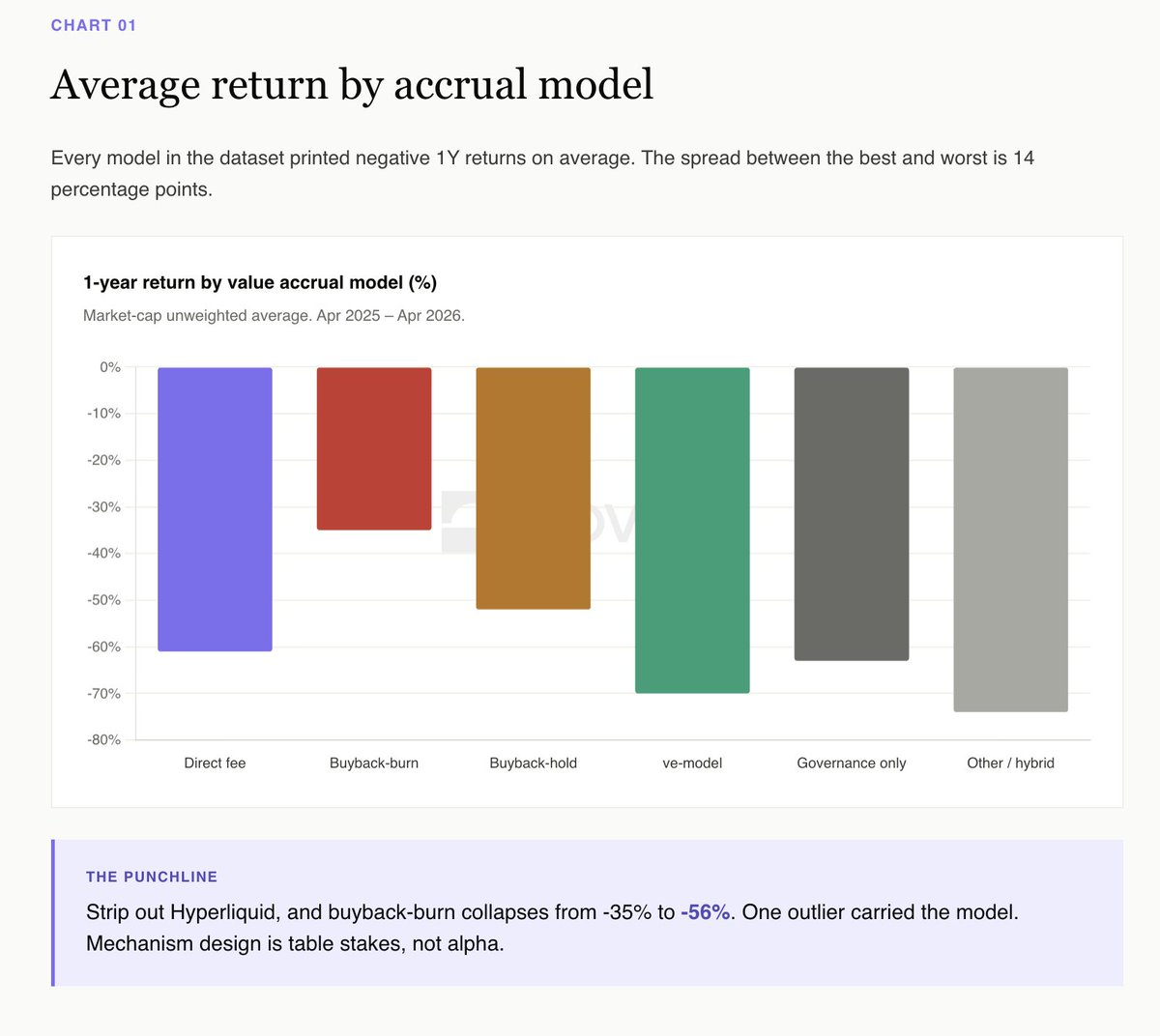

Based on surface data, the buy-back destruction won this year (average - 35 per cent) and the buy-back held second (52 per cent). It looks like the end of destruction。

But after removing Hyperliquid, the story reversed. Remove HYPE, buy back an average of -56%, buy back an average of -52%. A token determines the entire category。

Meteora is the cleanest case of repurchase possession. A $10 million buy-back scheme, Novora investor relationship rating 95/100, transparent treasury accumulation. This year it dropped by about 40 per cent, below the same median. The holding of repurchase tokens in the transparent treasury retains the right of option and creates visible, audited circulation. The destruction destroyed the right of choice in exchange for a marketing title。

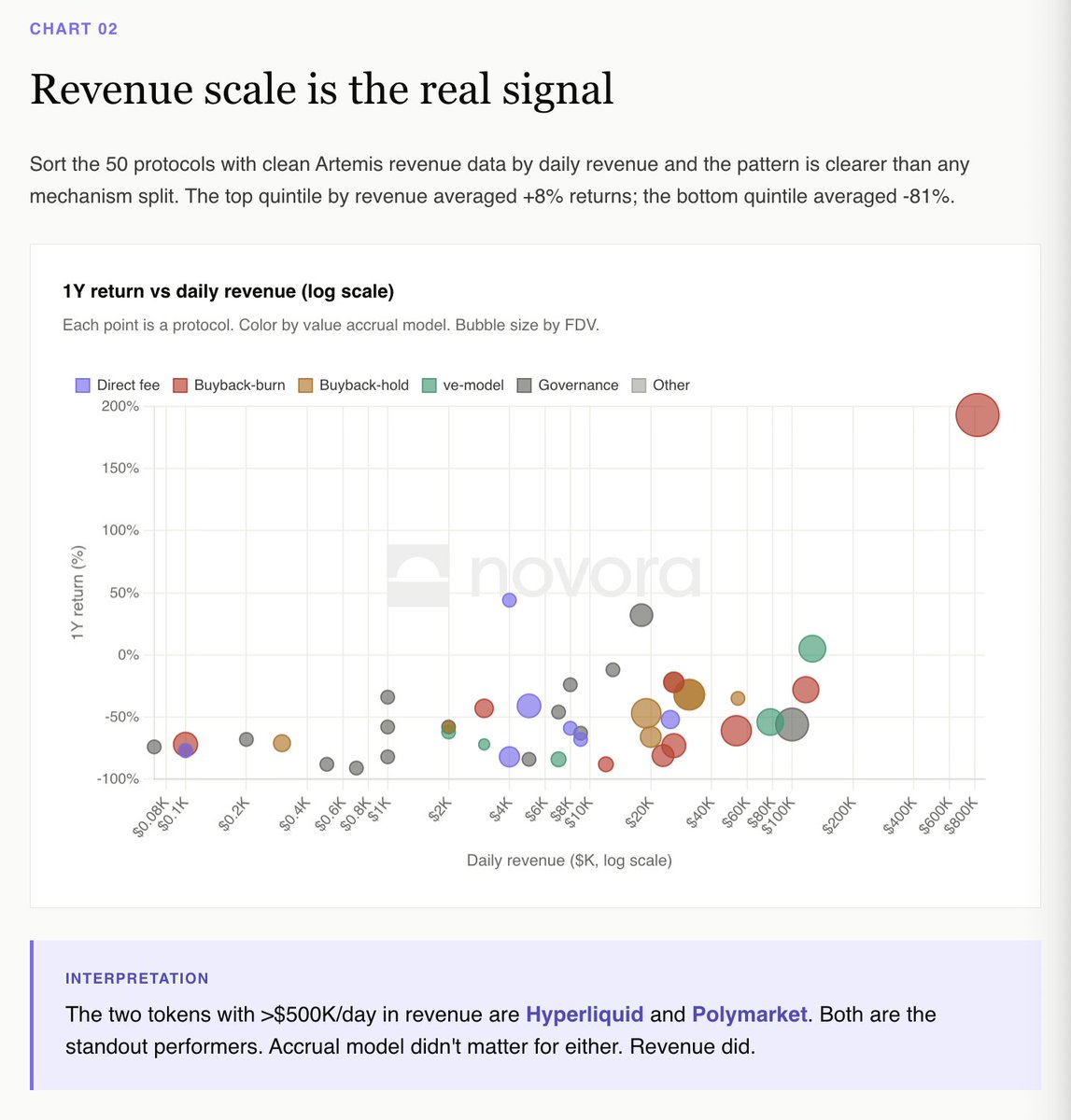

The income scale is the real signal

Fifty agreements with clear Artemis income data are ranked on a daily basis and the pattern is clearer than any mechanism。

The average rate of return for agreements with the highest income quintile was + 8 per cent. The lowest fifth average - 81%。

Two agreements with a daily income exceeding $500,000 are Hyperliquid and Polymarket. Both featured prominently in the data sets. Their cumulative models differ, but the income trajectory is the same。

dYdX paradox vs Hyperliquid

Direct cost allocation is the most readable model of the agency ' s configuration, as it clearly maps the dividends. dYdX run textbook version: 100 per cent of the transaction fee is paid to the pledge, 75 per cent of net income is repurchased, and the best investor relationship infrastructure。

dYdX dropped 82% in the last 12 months. The mechanism is fully committed, but not operational。

Hyperliquid is the opposite. Zero traditional investor relationship infrastructure, annual + 193 per cent。

If you're the configurationr, it's the clearest interpretation of the data collection: you buy a part of the agreed income, and if it falls, the coin falls. Mechanisms are the basic requirement and the revenue trajectory is everything。

ve, the model needs a permanent bribe to run

Aerodrome is the only ve model token with a positive (+5%) return of 1 year of data concentration. The mechanism relies on the Base ecosystem to flow to sustain the bribe market。

Velodrome, Curve, Balancer and every smaller ve fork fell - 54% to -84%. ve The wheel is valid, but it requires new capital on a continuous basis. When capital flows stop, the whole structure collapses。

this is not a criticism of the model. it's a recognition that ve tokens are a bet on the inflow of ecosystems, not necessarily on the purely protocol fundamentals。

Mixed category average - 71%

Credit plan, RWA, LRT, memecoin, stabilization currency. 62 agreements. The most exotic categories of data concentration. Average 1 annual return: 71 per cent。

This is the home of most of the projects published in 2024-2025: Esther Fi, Renzo, Puffer, Usual, Virtuals, AI16Z, the entire LRT queue, memecoin queue. These tokens rely on narrative and TGE air-drop transactions, not cash flow mechanisms. Once the drop lock is complete, there's nothing to support the price。

Investor readability is fundamental. The configuration cannot cover a cumulative mechanism that relies on future narratives。

Panorama

Average 1 annual return by cumulative model:

Repurchase destruction: -35% (extracted by Hyperliquid; remove HYPE for -56%)

Repurchase holdings: 52 per cent

Direct cost allocation: -55 per cent

Pure governance: - 65 per cent

voting hosting model: 67%

Other/mixed: 71%

Of 135 agreements for which empirical data are available, 5 have been corrected in the past year. Medium return: 66 per cent。

What does that mean

The market would not design a premium for a good mechanism, but would penalize a token that was completely unmechanized。

The clearest empirical interpretation in 2025 was that value accumulation did not generate excess returns and income was generated. But 48 pure governance agreements show the cost of no mechanism. When the market chooses between paying your tokens and non-payment tokens, it chooses the one that pays。

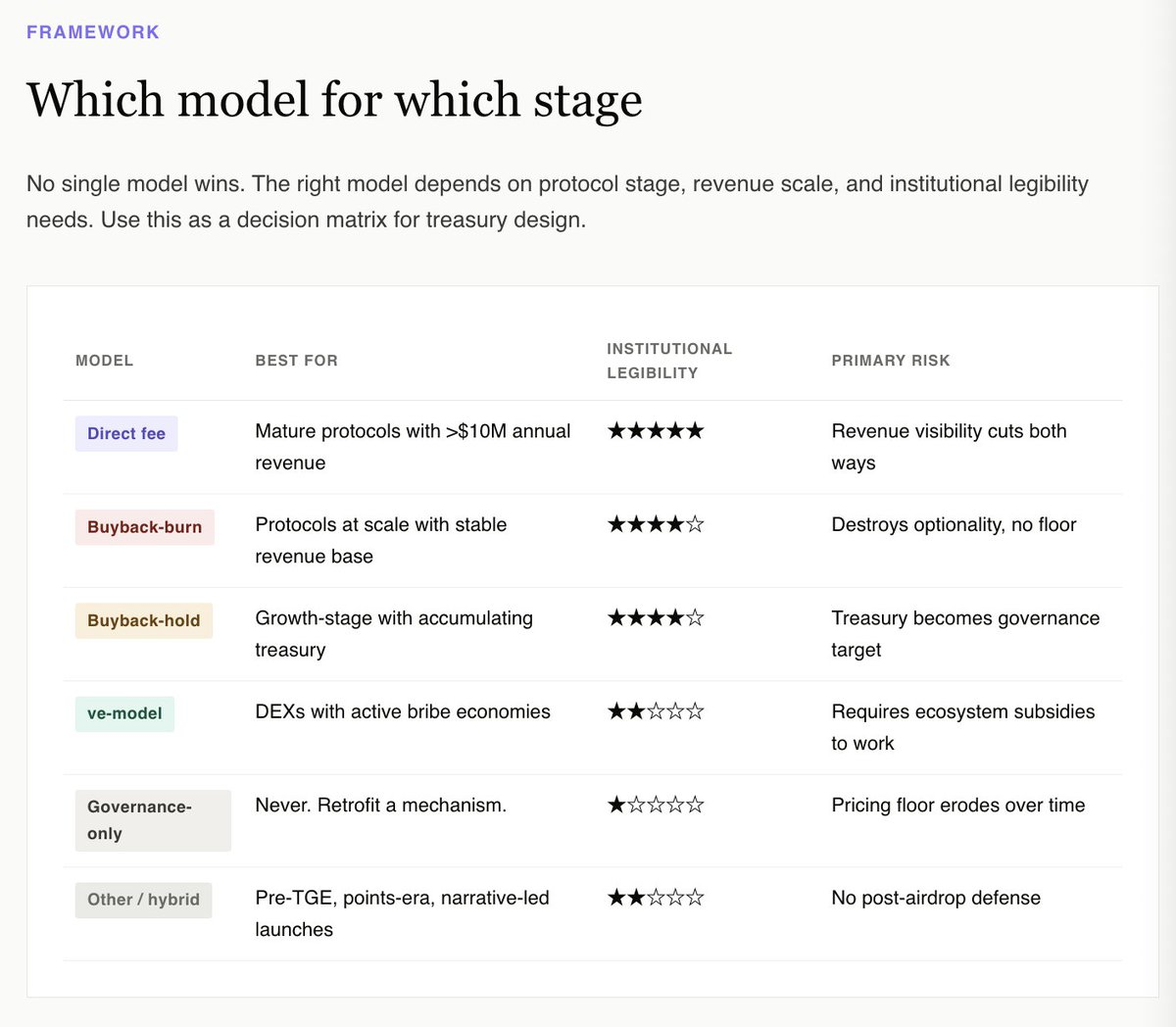

For the treasury, the right question is not what mechanism maximizes the upper space. The data indicate that none can be reliably achieved. The right question is what mechanism would make the token look investable from the basic perspective of the agency ' s configuration。

This perspective immediately excludes pure governance and hybrid categories. It prefers repurchase holdings with transparent treasury disclosure, repurchase destruction of scale agreements (Hyperliquid), distribution of direct costs of mature income generation agreements, and, for narrow DEX original coins, binding of the ve model for active bribery markets。

The honest answer to all other tokens, including most of those issued in the last 24 months, is to modify a mechanism before the next lock is unlocked. Do it while you have a choice。

Full interactive reports containing all 159 protocols and filterable data sets are online:

https://www.novora.co/research/value-accrual-2026.html

This paper is intended for information purposes only and does not constitute a financial, investment or legal recommendation. All data are validated from open sources in April 2026. Nova may have an advisory relationship with the agreement mentioned in this report. Prior to making investment decisions, you are requested to conduct your own research and consult with qualified financial consultants at all times。