What's he betting on

The investment philosophy of Dian Ping always holds the "no vote without understanding." 。

Source: Fintech Blueprint

Compiled and collated: Bitpush News

Yesterday, the US SEC disclosed the latest 13F holdout report. The "China Buffet" account H&, silently managed and over $20 billion in family wealth and charity fund accounts, and H International Investment LLC, which built the first compliance stabilization currency giant, Circle (United States stock code: CRCL), held a market value of $19.08 million。

As a strong value investor, Duan Ping was famous for his war with Apple and Guizhou Shao, and his investment philosophy has always been one of "unreadable non-investment". This build-up, Circle, means not only the formal acceptance of traditional old capital for Web3 compliance assets. This paper will break down Q1 performance and the latest product layouts in depth, looking at whether the stabilization currency giant can make a shift from an "interest-driven" to an "infrastructure" business model through the re-engineering of the bottom structure。

Here is the text:

Circe spent a busy week。

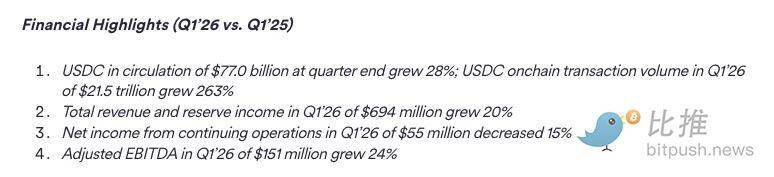

ALONG WITH THE RELEASE OF ITS PERFORMANCE IN THE FIRST QUARTER OF 2026 — TOTAL INCOME AND INTEREST INCOME ON RESERVES CLOSE TO $700 MILLION (20 PER CENT INCREASE OVER THE SAME PERIOD), USDC FLOWS REACHED $77 BILLION AND CHAIN TRANSACTIONS REACHED $21.5 TRILLION — IT ALSO DROPPED TWO MAJOR PRODUCT ANNOUNCEMENTS AND COMPLETED AN ADVANCE SALE OF $222 MILLION IN TOKENS。

Change the label for "interest rate vouchers"

For a long time, Circle has been labeled as the "interest-rate agent tool": 99 per cent of its 2024 revenues came from interest earned on USDC reserve assets。

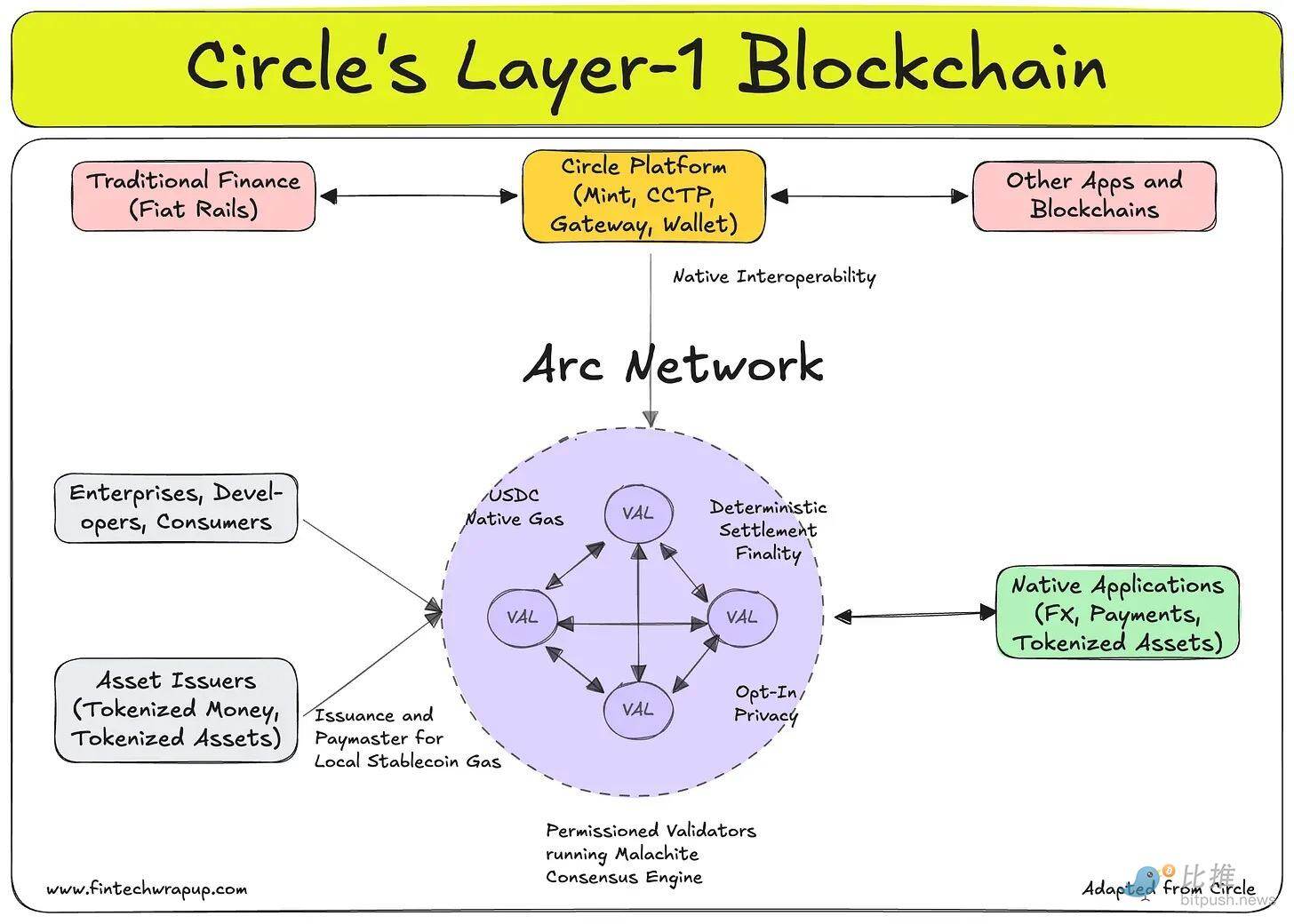

This makes the business extremely sensitive to the interest rate cycle and leaves equity investors with little basis for valuation pricing other than spread income and growth in the distribution of USDC. Arc (its Layer-1 block chain), Circle Agent Stack (intellectual technology warehouse) and Payments Network (Payments Network) are precisely a concentrated attempt by Circle to change the status quo – aimed at diversifying income and allowing the valuation logic of equities to be re-evaluated from a “receiving factor multiple” to a “lower structure multiple.”。

Perhaps the most unusual thing is that Circe, as a listed company with traditional equity structures, managed to raise $222 million through pre-sale of coins for its new Layer-1 block chain, which focuses on stable currency, and achieved a full-scale valuation of $3 billion (FDV)。

In the area of finance, some instruments will be included in the regular stockholders' roster (Cap Table), while others will be in the currency of a particular agreement. It is worth noting that Coinbase has not yet issued a token for the Taifung L2 network. The ability of a publicly listed company with a market value of billions of dollars to complete such a token financing means that currency assets have officially landed on Wall Street。

The current round of financing was led by Andréssen Horowitz (a16z), which committed $75 million, with the participation of BlackRock and Apollo. The advance sale consists of years of lock-outs; investors also have repayment rights if key milestones of the Arc network are not reached。

Circle holds 25 per cent of the 10 billion initial tokens available, 60 per cent for network participants and 15 per cent for long-term reserves. The Arc main network is expected to go online in the summer of 2026, and its testing network has processed 244 million transactions by early May。

At present, the practical function of ARC tokens (Utility) is still at the exploratory stage. This means that even without well-designed token economics, you can still get more than $200 million today. And, if we look closely, we'll find that the construction of a Layer-1 block chain does not actually require $200 million。

At the same time that Arc was launched, Circle published Circle Agent Stack... This is a tool kit for developers to build "AI Intelligences for USDC Transactions", which contains wallets, markets and a nanoscale payment layer (Nanopayments player) that can support transfers up to US$ 0.001000。

As a result, the company joined Stripe, Coinbase, Visa, Mastercard, Shopify, Fiserv and Brex in this rally called "Bank services for robots"。

Arc, it's a defensive war

Today, USDC runs in dozens of public chains and wallets like the Ether, Solana, etc. Circle could earn interest income from all these reserve assets. The problem, however, is how much it actually leaves in its pocket。

Under the Cooperation Agreement signed with Coinbase in 2023 (which was signed at the time of the dissolution of the Centre Alliance, when Coinbase had a huge bargaining chip as the largest distribution channel for Circle), the distribution of interest income from the reserve was divided into three steps:

- Circe first extracts a small issuer fee from the top floor。

- SUBSEQUENTLY, THE PARTIES EACH RECEIVED INTEREST INCOME FROM THE RESPECTIVE RESERVES BASED ON THE PROPORTION OF USDC HELD IN THE RESPECTIVE HOSTING PRODUCTS。

- As for the rest of the profits -- Coinbase takes 50% straight。

As a result, even if some USDC had no hosting relationship with Coinbase, Coinbase would have been able to take a portion of the interest income from the reserve。

In 2024, up to $908 million of the $1.68 billion in total income of Circle was given to Coinbase. The agreement is automatically renewed every three years, and Circle has no right of unilateral withdrawal. Thus, Arc is, to some extent, an effort by Circle to build a bottom-up structure that is fully owned and directly costed。

Once again, Coinbase has half of the revenue of Circle, which has no way out except to find a smart back door。

Arc’s winning logic is very direct: a Layer-1 block chain specifically designed to stabilize original currency finance. With USDC as the Gas (fuel) token, it has sub-second-level transaction finality, optional privacy protection, EVM compatibility, and a framework for resistance to quantum attacks. This is a new generation of settlement infrastructure and a substitute for the ACH, SWIFT and correspondent banking systems for institutions that themselves are engaged in resource allocation。

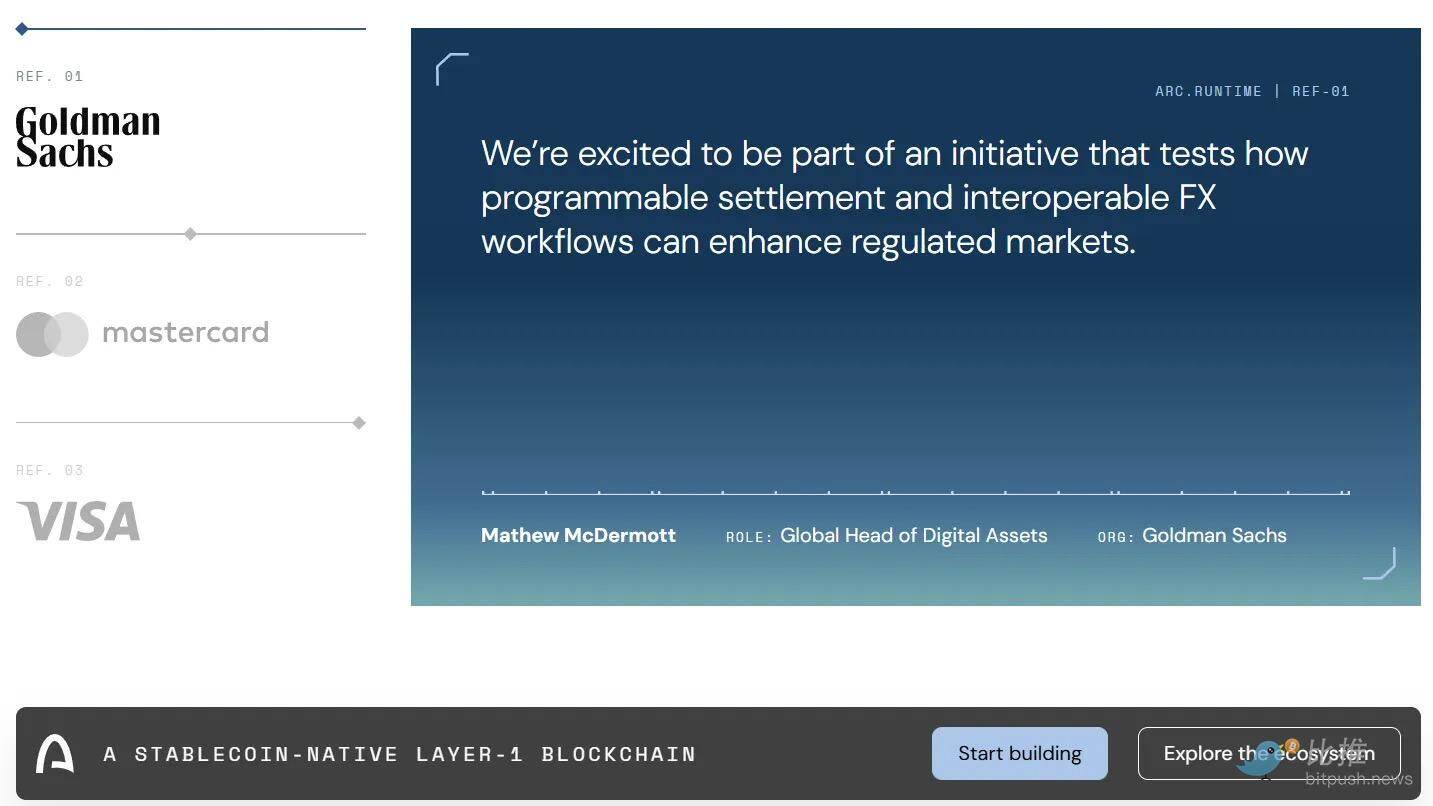

Launched in October 2025, the network has attracted over 100 institutional participants, including BlackRock, Goldman Sachs, Visa and State Street Bank, and processed 244 million transactions。

But to be sure, similar institutions have joined Tempo and the various AI payment and intelligence protocols that we have reported in the past. This shows that the industry is diversifying in the process of restructuring the payment track。

By contrast, the $3 billion in pre-sale pegs to a full-scale valuation (FDV) appears somewhat confusing. Because the ARC token function is still being explored. The investor's current bet is actually the future value of the "stabilized currency settlement mother chain" - thus closing the entire vertical ecology and closing the current gap in the disclosure of value to third parties. And whether this option is worth $3 billion depends on the volume of future transactions. Specifically, it depends on whether the Circle can move a sufficient share of the current $77 billion in circulation to Arc to generate revenue sufficient to support the service charges for the valuation。

At the same time, the regulatory context has increased this urgency。

The GENIUS Act, signed in July 2025, clearly opens the way for banks to issue their own payment stabilization notes through subsidiaries and is subject to supervision by their existing federal regulatory bodies. JP Morgan and Bank of New York are already piloting tokenization deposits. Once the regulated bank is in dollar currency size, the market's demand for third-party stabilizers, such as Circle, shrinks。

Arc does not address this directly, but having an autonomous chain infrastructure can create network effects and conversion costs. It's a line of defense against the risk of profit-splitting or vertical integration from all of Canton to Ripple, and then to Morgan Chase Kinexys。

Circle Agent Stack was an attack. War

Agent Stack is a developers toolkit for building AI smarts that can be traded using USDC. It consists of a wallet, a market and a nano-paid layer capable of achieving a low transfer of up to US$ 0.001 000. The core logic is that, as AI intelligents take over more and more operational and financial work, the scale and precision of the transactions they need will be those that are not supported by existing payments (e.g., bank card networks, ACH, SWIFT, etc.) because fixed costs are too high (the existing network leads to transactions that are not economically viable). A USDC primary chain that supports minimally programmable payments does not exist. There is currently no perfect solution in the market for an AI smart body that has to pay for the API call times, in seconds or in data queries。

Ramp launched Argentina Cards in March 2026. In short, it allows enterprises to issue virtual cards for the expenditure of autonomous intelligent bodies. And Stripe, after buying Bridge at the end of 2024, had his answer: issuing smart-body cards through Bridge, providing wallet infrastructure through Privy, and supporting stable currency payments in 32 markets。

- Ramp 'Agent Cards: Created specifically for enterprise cost control。

- : For USDC primary micropayments in the Arc chain。

- Stripe: Position yourself into a whole stack (with statutory currency, stable currency and bottom structure of wallets under an API)。

Circle versus Stripe

The structural advantage of Circle lies in the assets themselves。

The USDC is the dominant compliance and stabilization currency and has become the unit of account for a significant part of the chain of activity. While Bridge, under the banner of Stripe, issues its own stabilization currency through Open Issuance. USDH, one of Bridge's flagship issues, was declared closed this week because of its inability to counterbalance $5 billion USDC on Hyperliquid, and Coinbase stepped in to become the official USDC Treasury Deployment. Building the bottom structure of the smarts above the USDC means that the smarts can inherit the current mobility and network depth from day one. This asset advantage has proved to be far more difficult to replicate than it appears to be。

As mentioned earlier, Stripe also hatched Tempo, a Layer-1 block chain tailored to pay. However, Tempo is positioned to support any common payment settlement of a stable currency, while Arc is built entirely around USDC. Both companies are betting that the future of payments will be clear on customised exclusive chains, rather than on generic chains such as the Etherport。

Differences in capital structure are also noteworthy. Circe raised $222 million ($3 billion FDV) for Arc through pre-sale. Stripe is a privately owned, continuously profitable company with a recent estimate of $70 billion – it can finance the expansion of Tempo and Bridge entirely from its balance sheet, without diluting equity through tokens。

The manner in which the two companies have access to ammunition differs substantially in absorbing and subsidizing the costs of a new chain ecosystem。

In the final analysis, the ability and preferences of "paying processors (e.g. Stripe)" and "distributors of cash equivalents (e.g. Circle)" are quite different. The former are well-distributed and the ecology is home to numerous businesses and customers, while the latter have a seat in every exchange and encrypted wallet. We believe that blind vertical integration and the introduction of an expensive arms race would be a mistake。

The algorithm of the books of income

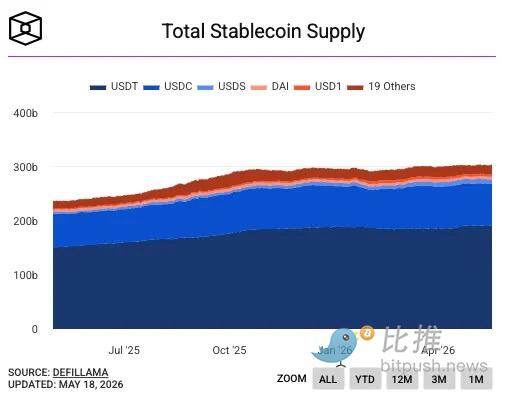

Circle's business model today is simple: $77 billion USDC is in circulation and earns about 4.1 per cent of the return on reserve assets, much of which goes to Coinbase under distribution agreements. Its total annual income in 2025 was $2.75 billion。

Analysts forecast revenues of approximately $3.2 billion in 2026, which means about 15 per cent growth. Compared to last year's growth rate of 64%, this figure appears to be quite moderate, reflecting two realities:

- The decline in interest rates reduced the return on reserve assets

- The GENIUS Act limits the sharing of reserve income with distribution partners, leaving the cooperation agreement with Coinbase under regulatory review。

New products must be understood in this context. Circle estimated non-reserve income in 2026 to be between $150 million and $170 million, which, although higher than $110 million in 2025, still represents less than 6 per cent of total income. Arc's transaction costs, the developer's income from Agent Stack and the costs of CPN (Circle's payment network) are at an extremely early stage. To achieve a revaluation of the valuation from the "interest rate proxy tool" to the "bottom architecture platform", these lines of business need to be increased not only in absolute terms, but also in terms of income. From the current trajectories, the Circe story goes faster than the financial figures。

Stock movements also reflect such chainsaws. In June 2025, at an IPO price of $31, the CRCL briefly jumped to close to $300, before falling back and stabilizing at around $114. After the release of the first quarter, Morgan Chase increased the price target to $155, Needham to $150 and Deutsche Bank to $101. The market consensus is expected to stay between $125 and $130, which means that the upper space is very cautious compared to current levels。

See more and more

Multi-logicism requires three conditions at the same time:

- MERCHANDISE GROWTH IN USDC IS FAST ENOUGH TO OFFSET THE IMPACT OF DECLINING RESERVE YIELDS

- Arc could generate significant cost income and partially replace or break out of the cooperation agreement with Coinbase

- Agent Stack is able to take the lead in establishing a bottom-up structure in the area of smart pay before Stripe relies on volume to crush。

If these three points are fully achieved, Circle will successfully transform into a paying infrastructure company whose valuation multiplier will be driven by volume of transactions and network effects rather than by the Fed ' s interest rate cycle。

It's easier to look at empty logic:

Interest rates are falling faster than they are in circulation; the agreement with Coinbase has reduced distribution channels during the reorganization process, but has failed to effectively cover the volume of transactions; Arc has been unable to move a sufficiently large USDC to its own chain; and Stripe or Ramp has introduced a better intelligent infrastructure at a lower cost, completing the siege on Circle。

Circle's announcements are certainly the right step in the strategic direction. But now, they are just chips and bets and have not yet turned into real business. Circle is asking investors to pay for these three simultaneously realized options, while its core business model is facing a solid structural reversal. That requirement could not be said to be unreasonable — it seemed somewhat expensive at the current valuation level。