ALL-WORD RESOLUTION: FROM $10 TO $290, MRVL WON THE ENTIRE AI ERA BY "NO GPU."

The Marvell stock price was innovative and the market focus shifted to its "real valuation logic"。

ORIGINAL TITLE: "MULTIWORD PARSING: FROM $10 TO $290, MRVL WON THE ENTIRE AI ERA BY "NO GPU"

Original by Mussolsol, Encryption Analyst

On June 3, 2026, Marvell Technology $MRVL stock price touched $290, a new high。

Over the past 12 months, it had risen by 254 per cent, less than $40 three years ago。

If we start with Matt Murphy's CEO in 2016 -- the stock price was less than $10, the market value was not even 2 billion, 30 times。

But the increase is not in itself something we'd like to talk about。

What this article really wants to understand is:What is the market offering Marvell? Behind this price, is this company still being understood with an outdated cognitive framework

There's a lot of people on the street who call Marvell Little Broadcom -- custom-made IA chip dicks, pick up hyperscaler after Broadcom and eat the rest. That's not all wrong, but there's a fatal blind spot:It defaults that Marvell is a shrinking version of Broadcom. And Marvell's real worth is exactly where it's nothing like Broadcom。

Marvell occupied a unique ecological position. The infrastructure of AI is moving from "stacking GPU" to "building systems," a position that will become more valuable。

This paper will try to make this clear。

Full text about 15,000 words, please read slowly

One, Marvell, what is it

If you want to see Marvell, the first step is to get rid of the chip company label. It doesn't do GPU, doesn't build CPU, doesn't sell memory。IT SELLS "CONNECTION" -- IT ALLOWS DATA TO FLOW AT THE SPEED OF LIGHT BETWEEN AI CHIPS, BETWEEN SERVERS, BETWEEN DATA CENTRES。

Let's see. Three pieces of business:

First: the light is connected — the moat

Marvell is the absolute boss of the high-speed light DSP. Global 400G above data centre light module, about 70% of DSP chips come from Marvell。

Every time you see "AI data centre light module" news, Marvell's in the back。

WHY IS 70% OF THE SHARES SO HARD TO SHAKE? HIGH-SPEED LIGHT DSP IS NOT A NORMAL CHIP. IT'S GOT TO FIX THE SIGNAL, DECOMPOSITION, CORRECTION, CLOCK RECOVERY, 800G, 1.6T AT THE SAME RATEThe physical layers of signal decay and noise management are appallingly complexI don't know。

After spending about $10 billion on the purchase of Inphi in 2021, Marvell has gained more than five years of production experience in this area, from 5 nm to 3 nm. Broadcom is chasing too, but this pre-emptive advantage can't be wiped out by smashing money。

In March 2026, Marvell pushed four 1.6 T DSP novels - Ara T, Ara X, Petra, Aquila M - from short to long range, Ethernet to Infiniband fully covered. Murphy told the truth at the FY2027 Q1 press conference: Light Interconnection Business FY2027 is expected to increase from 50% to 70%+。

It is not the market that has changed, but they themselves have underestimated the magnitude of the demand。

BLOCK 2: CUSTOM AI CHIP - GROWTH

It's the market's closest. The logic is simple: Amazon doesn't want every GPU to pay taxes to Young Waida, and he designed an AI training chip called Trainium. But Amazon doesn't make chips -- we need help with design and mass production. This man is Marvell。

For now, Marvell has it18 CUSTOM XPU DESIGN ITEMSIt covers three families - Amazon, Microsoft, Google. Livetime reach$75 billionI DON'T KNOW. FY2026 GENERATED ABOUT $1.5 BILLION IN REVENUE FROM CUSTOMIZED CHIPS THROUGHOUT THE YEAR, AND FY2028 IS EXPECTED TO MORE THAN DOUBLE。

But this business has one discomfort: the Māori rate is lower than the standard product. The non-GAAP Māori rate for FY2027 Q1 is 58.9 per cent and Broadcom is 77.5 per cent. It's very straightforward -- you're working for Amazon, not selling your own standard, researching heavy, client bargaining power。

We'll talk later。

Number three: Exchange chips and business storage - cash cattle

ETHERNET EXCHANGE OF CHIPS WF2027 IS EXPECTED TO EXCEED $600 MILLION (TWICE THE SAME RATIO), BENEFITING FROM THE RIGID DEMAND FOR HIGH-SPEED EXCHANGES WHEN THE AI CLUSTER EXPANDS FROM HUNDREDS TO OVER 100,000 GPUS. THE ENTERPRISE-LEVEL SSD AND HDD CONTROLLERS ARE THE OLD LINES, CONTRIBUTING TO A STABLE CASH FLOW, BUT THEIR SHARE SHRINKS YEAR AFTER YEAR UNDER PRESSURE FROM AI OPERATIONS。

Three pieces together, and the picture is clear: Marvell is not a chip company that does everything"AI DATA FLOW"The company that built the whole warehouse connection capability. From SerDes inside the chip, to PCIe/CXL swaps between the chip, to light DSPs between the racks, to a relevant light module between the data centres - each of which has a hand。

Understand that, it makes sense why Yin Weidar paid two billion for it. And I'm beginning to understand why Marvell called Little Broadcom was an error。

"CONNECT" BECAME THE LEADING ACTOR

THE SPOTLIGHT HAS BEEN ON THE GPU FOR THE LAST TWO YEARS。The force is muscle, the bigger the better。BUT WHEN THE AI CLUSTER EXPANDED FROM THOUSANDS OF GPUS TO 100,000, 500,000, A PHYSICAL LAW PROBLEM AROSE:The copper cable can only pass 3 meters, and beyond this distance, the signal declines to an inoperable level。

GPU CAN BE THE STRONGEST BRAIN IN THE WORLD, BUT THE TRANSMISSION OF SIGNALS BETWEEN NEURONS CAN'T KEEP UP AND THE IQ CAN'T WORK. IN 100,000 GPU CLUSTERS, EACH GPU SPENDS 30-50 PER CENT OF ITS TOTAL RUNNING TIME ON "SHOW DATA"。

THAT'S WHY LIGHT IS THE MAIN ACTOR. IT CAN PASS HUNDREDS OF METRES OR EVEN A FEW KILOMETRES WITH LITTLE DECLINE. THE LARGER THE CLUSTER, THE LARGER THE GPU, THE HIGHER THE PROPORTION OF LIGHT CONNECTIONS — NOT LINEAR GROWTH, ULTRALINEARITY。

Barclays calculates that in 2026 the output of light ports doubled, and in 2027 it doubled. Marvell Light Interconnection is expected to increase by about 90 percent a year in the next two years -- and so on -- and now it's up to 70 percent plus, but in terms of actual numbers, 90 percent may not be able to hit。

THE POINT IS THAT THIS TREND IS NOT A YEAR OR TWO. AS LONG AS AI MODEL PARAMETERS CONTINUE TO EXPAND, TRAINING AND REASONING CLUSTERS CONTINUE TO EXPAND, THE INTERCONNECTED DEMAND CURVE WILL NOT BE EVEN。

This is not a problem with the cycle of the atmosphere, but a long-term structural trend determined by the laws of physics。

For example, AI infrastructure is a city that's expanding wildly, GPU is building itself, Marvell sells pipes, wires and highways. Houses can be built by different architects, but after the infrastructure has been paved, it is much harder to change than building houses。

III. FROM $10 TO $290: AN UNDERVALUED CEO

In 2016, Marvell, a stock that was abandoned by the market。

The founders Seet Sutardja and Weili Dai were forced to step down for accounting investigations and governance crises, and the SEC intervened. Business stalls are well spread — mobile communications, printers, consumer electronics — but not one of the top three industries. The price of the stock is less than $10, and clients are starting to worry about whether the company will survive。

The radical hedge fund Starboard Value intervened that year, pushing for a reorganization of the management at the textbook level. Digged from Maxim Integrad when Matt Murphy was CEO。

But I personally think Murphy is worth a few more words: he worked at Maxim for 22 years, selling first-line to the executive vice president, running the company's product development, sales and losses. It's not the kind of semiconductor that's a "technology genius" CEO -- it's the kind of thing that's--Extremely pragmatic and focused businessmen。

I was impressed by what he said:"My father worked in the Apple's first sales team, and I understood from childhood that the best technology is zero."

Murphy did three things after taking office, looking at it simple, and it's extremely difficult to implement:

First, cut。

Mobile communication cut off. Printer chip cut off. Consumer electron cut off. Wi-Fi/Bluetooth business 17.60 billion sold to NXP (2019). Ethernet 2.5 billion is sold to Infinion (2025)。

All resources are concentrated in one direction: data centre infrastructure。

Second, buy。

In 2018, 6 billion won (i.e. ARM server CPU, DPU). In 2021, 10 billion in Indonesia, light DSP -- this changed Marvell's fate. By the end of 2025, 32.50 billion received Celestial AI (associated with silicon photons/photoweeds). Early 2026 540 million received XConn (PCIE/CXL exchange chip-related)。

FOUR ACQUISITIONS, EACH OF THEM A PIECE OF THE "AI CONNECTION" PUZZLE。

Third, tie。

Murphy's pursuit of something called "long-term vision" -- predictable income certainty for years. More than five years of agreement with AWS covering custom AI chips, light DSP, AEC DSP, PCIe retimer, DCI light modules and Ethernet exchange chips - not a single deal, a set of system-level collaborations。

IT IS DISCLOSED IN 10-K THAT CERTAIN CAPACITY RETENTION AGREEMENTS HAVE A DURATION OF 4 TO 10 YEARS。

THE RESULT? FY2016 REVENUE AT TAKEOVER APPROXIMATELY$2.65 billion(2.32 BILLION DOLLARS IN 2017), LOW PROFIT. FY2026 INCOME82 billion(+42% YoY), non-GAAP EPSUSD 2.84(+81% YoY)。

TEN YEARS AGO, A SECOND-LINE CHIP PLANT THAT CRAWLED OUT OF THE GOVERNANCE CRISIS BECAME A CORE PROVIDER OF AI INFRASTRUCTURE。

There is a pattern that I have tested over and over again:THE WHOLE CHAIN OF "CEO-STRATEGIC FOCUS ON LARGE MERGERS AND ACQUISITIONS AND BLANKETING OF LARGE CLIENTS" RUNS THROUGH, AND EVERY STEP OF THE WAY CAN SEE EVIDENCE IN FINANCIAL FIGURES -- A COMPANY LIKE THIS DESERVES SERIOUS TIME。

iv. $2 billion from Inverda: endorsement or compilation

On 31 March 2026, Inverda announced a $2 billion strategic equity, Marvell - subscription of 2 million convertible priority shares, with an initial conversion price of approximately $9184, corresponding to approximately 2.4 per cent equity after full conversion。

Message the same day Marvell went up 13%. But the excitement of the market was different from what I had been thinking。

What the market sees is: "This guy is my approved partner." "The logic is correct. Two billion dollars is not public relations, but strategic investment. In 2026, a series of light-connected companies — Coherent (2 billion), Lumentum (2 billion), Marvell (2 billion) — crashed into the same track, a signal that sounded more powerful than any analyst's report。

But we should focus more on the cooperation framework -NVLink Fusion.

NVLink Fusion is a semi-customed AI infrastructure platform pushed by Young Weidar. Third-party manufacturers (e.g. Marvell) can provide customized XPU accelerators with direct access to the high-speed interconnectivity network in England. Young Weidar himself provides Vera CPU, ConnectX web cards, Bluefield DPU, NVLink Interconnection and Spectrum-X Switches。

It's translated into white:"You Hyperscaler want to replace GPU with your own customized chip? No problem, I used NVLink Fusion to feed your chips into my ecology. The chips are for you to make, but the interface is still mine."

I can only say very brilliant. Turning the "enemy" into "client" -- the more heperscaller wants to get rid of the GPU, the more he needs his network. And Marvell, the one who made the customized chip for the hyperscaler and the one who built the interfacing ecology for the British。

It's a good fight。

The Next Web has an analytical title that is harsh but precise: "The $2 billion investment of Ingweida to Marvell is not an investment, it is a toll

Through this investment, Yvette has set up cards at every entrance to the ecology. But a different angle -- Marvell is part of the toll station. The left hand makes chips for the cloud factory and the right hand builds networks for Young Wei Da。

They can't leave it, they're sending it money。

Of course, it also means a constant tension:YVDA IS BOTH A PARTNER AND A RIVAL。It makes its own web chips and is also set up with silicon, and the boundaries of cooperation and competition have been blurred。

But my personal judgment is that at the stage of the "building of systems" of AI infrastructure, we need Marvell, more than Marvell. Because the customized chip demand for hyperscaler is structural and irreversible, the refusal of Yvette to cooperate is tantamount to giving the cake to Broadcom。

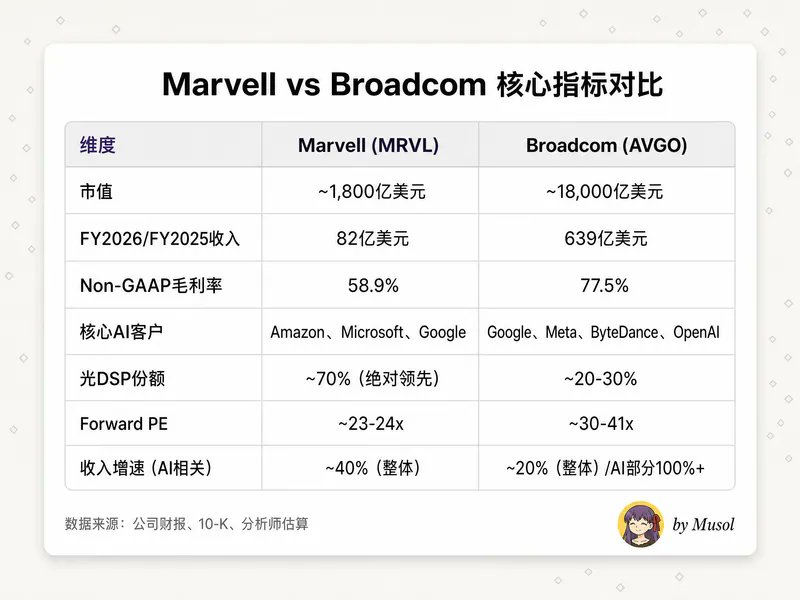

What's the difference with Broadcom

Many people will quickly conclude after reading this form:"Broadcom is better -- ten times larger, 20 points taller than Māori, and not too expensive to value."

There can be no mistake, but two of the most crucial things are missing。

First, there are structural reasons for the Māori gap, not "Marvell won't make money."。

77.5 per cent of Broadcom is not a pure semiconductor: including VMware ' s software income, EBITDA ' s profit margin of 67 per cent, significantly higher than the combined Maori ratio。

Look at the semiconductor alone, about 60-65 percent. The 58.9% of Marvell is really low, but the gap is not as exaggerated as it appears. Furthermore, with the expansion of Custom ASIC and the low cost of R & D, the Māori rate has clearly improved the path - the company's medium-term target, the non-GAAP operating profit margin is 38 per cent。

Second, Marvell in the light DSP is not the dick, it's the boss。

Seventy percent of the market share, and Broadcom is the one that's chasing it. The DSP is precisely the most beneficial link in the transition of AI infrastructure from "training-led" to "debris-based" — the reasoning cluster is much more distributed than the training cluster, and the demand for light interconnection is much more intense。

Duan Ping has a classification framework that I've always found very useful: "B type business" is better for you than anyone else, but others are doing it; "A category business" is something that you can't do, or you can't do it. Marvell's light DSP is closer to class A; custom ASIC is closer to class B, but client binding depth and switching cost is extremely high, and category B is actually not less colourful。

The market looks at Marvell in the "Small Broadcom" framework and naturally calculates "not worth $180 billion." But instead of the three-dimensional framework of "the light-connected head + custom chip dick + the Eco-Partnership of England," the valuation logic is different。

Numbers don't lie

Financial data is the only test of all narratives

FY2027Q1 KEY NUMBERS:

• Quarterly income of 24.18 billion, +28 per cent, ring +9 per cent and record high. Super-guide median value 18 million。

:: Data centre income of 18.33 billion, representing 76 per cent, +27 per cent and +11 per cent。

• Non-GAAP EPS 0.80, which meets expectations. Operating cash flows of 639 million — a record high。

• Q2 DIRECTION: INCOME OF APPROXIMATELY 2.7 BILLION (MEDIAN), +12% RING/ +35%。The data centre is expected to grow by a medium to high double-digit ring。

Several trends are noteworthy:

Growth is accelerating。

FY2026 +42%, FY2027 GUIDELINES +40%, FY2028 TARGET +45%. THE 8 BILLION BASE FIGURE CAN ALSO ACCELERATE, INDICATING THAT THIS IS NOT A REPLENISHMENT OR A PERIODIC REBOUND -It's structural demand on the slope。

Business leverage released。

EPS growth (81 per cent) is much faster than income growth (42 per cent). Customize the size effect of the chip, increase the positive rate of light DSP production, and Murphy's strict control over costs。

The custom chip has a hidden gold mine - attach. In 2025, the company disclosed an easily ignored data: by 2028, the TAM of Custom XPU was about $40.8 billion, and the TAM of TAM around XPU was about 14.6 billion — the latter compounding at 90 per cent. A lot of people are staring at "who designed the most expensive AI chip," but the real profits are hidden in the corner。

PEG Crude: Forward PE approximately 23-24 times, income growth about 40%, PEG about 0.6。

By contrast, Broadcom Forward PE is about 30-41 times more, income growth is about 20%, PEG is about 1.5-2.0. With this simple lens of PEG, Marvell's pricing is not expensive. Of course, the PEG is just a rough starting point — whether the rate of increase will be sustained, whether the Māori rate will be improved, whether the competition pattern will deteriorate, is the real variable。

VII. Story of Light: Celestial AI and Next

Light DSP is Marvell's now, Celestial AI is its future。

In December 2025, Marvell announced a $3.25 billion acquisition of Celestial AI, a start-up company for photoweed technology. Thirty-five billion is a down payment, and if Celestial AI accumulated a profit of two billion before FY2029, the total value would be 5.5 billion。

It's not cheap. Murphy, why would you pay

Because Celestial AI solves the next physical bottleneck of the AI chip interconnection:The copper cable is at the end。

The current AI server is connected with NVLink between GPUs, fast but short distances. An accelerator 8 GPU, a shelf 4 and a cluster of hundreds of hangs - the physical limits of the copper cable became a bottleneck for the system as a whole。

The Phhotonic Fabric of Celestial AI replaces electricity with light to achieve direct light interconnection of the chips to the chips — the bandwidth of the Chiplet 16 Tbps per chip, reducing power consumption by half, with a delay of nanoseconds。

Words are:Light DSP is the extension of the freeway inside the data centre from two lanes to eight lanes, and Celestial AI is a direct portal between each building。

There is also a detail of the acquisition: Amazon supported the deal。

Marvell even issued an equity certificate to Amazon allowing Amazon to purchase up to $9 million in Marvell shares based on the purchase of Phhotonic Fabric products. Amazon would not simply endorse the supplier's acquisition - it was endorsed because it really needed the technology。

Marvell expects Celestial AI to start contributing meaningful income in the second half of FY2028, with Q4 FY2028 annualized income of 500 million and Q4 FY2029 annualized by 1 billion。IF THE ROAD MAP IS FULFILLED, THE INTERCONNECTION BUSINESS ALONE WILL MOVE FROM "FIRST BUSINESS" TO "SUPER BUSINESS" — AN ALL-WIELDY PLATFORM ACROSS THE DSP, SILICON PHOTONS AND PHOTOWEEDS。

Plus, early in 2026, 540 million XConn, Marvell now has a complete "Electron + Light" interlocking puzzle: PCI/CXL interconnection between the SerDes inside the chip and the PCI/CXL interconnection between the light and the DSP & data centre。

NO SECOND COMPANY HAS AN EQUALLY COMPLETE LAYOUT ON THIS TRACK。

Eight, 25, 4%. After that, of course, there are risks

the most important thing about investment in research is not "why it rises" — there are reasons everywhere in the cattle market. it's important to find out what's going to make it fall, and then to judge whether you're willing to take it or not, and i think the concept of risk control in @aleabitoreddit is worth everyone's attention。

Risk one: Trainium three lost, client concentration more than you think. High

Marvell recently lost the main design of the next generation of Amazon Trainium3 -- taken by Alchip of Taiwan, China. The company stressed that Trainium 2.5 continues to be done by Marvell, "without income faults"。

But the market sees the other side: the largest custom chip customer does not choose an old partner for the next generation. That's not a good signal。

FY2026, THE TOP 10 CLIENTS CONTRIBUTED 82 PER CENT OF THEIR INCOME AND TWO OVER 10 PER CENT. THE 10-K IS VERY HONEST: "AI'S CURRENT LEVEL OF CAPITAL SPENDING ON INFRASTRUCTURE IS NOT NECESSARILY SUSTAINABLE IN THE LONG TERM."

If Amazon or Microsoft were to reduce any custom chip plan, Marvell's income would go straight to the punch。

Risk II: Māori rate ceiling

Non-GAAP Māori rate 58.9 per cent, nearly 20 percentage points lower than Broadcom. It's not temporary, it's structural. Customization of ASIC is essentially a service business -- designing exclusive chips for clients, with end-products, with natural limits on your bargaining space。

The scale effect can be improved, but cannot be fundamentally addressed。

IF FUTURE INCOME GROWTH IS DRIVEN MAINLY BY CUSTOM ASCIC (LOW MĀORI RATE) RATHER THAN LIGHT DSP (HIGH MĀORI RATE), THERE WILL BE A DIFFERENCE BETWEEN INCOME GROWTH AND INCREASED PROFITABILITY. MARKET-BASED VALUATION MULTIPLIERS MAY NOT BE AS GENEROUS AS MANY EXPECTATIONS。

Risk Three: The "call station" in Weida could turn into a "call station + competitor"

Young Weida has invested 2 billion, but is building his own network chip team. Spectrum-X switch, Bluefield DPU, NVLink interconnection - direct or potential competition with Marvell's exchange chip, custom ASIC. 2.4 The holding of shares is not controlled, but ecologically bound。

In the future, if Yvette decides to internalize more value links of NVLink Fusion — like more light-connected chips — Marvell's location becomes delicate。

Risk four: insiders sell

Since 2026, CEO Murphy has accumulated a decrease of approximately $5.3 million (sold three times at prices ranging from 98.70 to 177.26), CFO Willem Meintjes a reduction of about 4.7 million, COO Chris Koopmans a reduction of about 2.73 million and CDO Sandeep Bharathi a reduction of about 13.14 million。

No internal increase。

The absolute amount is not very large in terms of shareholding (Murphy, although still holding approximately $131 million stock), and is implemented through the 10b5-1 preset。

But the signal is clear: stock prices have risen to the highest point in history, with a group of people who know the company selling, and no one buying。

At least you should ask yourself:I bought this stock because I understood its value or because I saw it go up 254%

Risk five: Supply chain

10-K DISCLOSURE REQUIRES LOCKING IN CAPACITY 26-52 WEEKS IN ADVANCE, WITH SOME AGREEMENTS LASTING 4-10 YEARS。

The 5nm/3nm capacity and GPU manufacturers (e.g., Weidar, AMD) have been fiercely competing, and the light DSP delivery cycle has grown to six months。

Marvell judge needs differently - promises that too much capacity results in a fall in demand, or that demand is over-anticipated but not enough -The punishment goes straight to the reportI don't know。

AI, THIS SUPERCYCLE OF CAPITAL, REWARDS NOT ONLY THE RIGHT PEOPLE, BUT ALSO THE RIGHT PEOPLE"The supply chain doesn't fall off the chain."。

After all the risks, what was my conclusion

These risks are real。

The loss of Trinium 3 is no small matter, the structural problems of the Māori rate are not solved overnight, and the insiders sell it with vigilance. But I'm not on Marvell's side for three reasons:

First, the bad news of the drop of Trainium 3 has been covered by a doubling of the revenue of the FY2028 customized chip。

The next generation that lost its biggest client could also provide double guidance to other customers (Microsoft Maia, Google Axion and the "new undisclosed hyperscaler") who are stronger than the market wants。

Secondly, light connects this moat with reality and is widening。

70% DSP share + Celestial AI Silicon Photons + XConnn's PCIe/CXL exchange = a set of total inn capabilities that others cannot replicate in the short term。

Competing people can take one or two customized chip orders, but no one can catch up with Marvell in three or five years on the light interconnection。

THIRD, PEG 0.6 GIVES A CERTAIN MARGIN OF SAFETY。

40% of the increase in income corresponds to 23 times the forward PE - this price is not "the market has made it the next Broadcom to fire" but "the market is still hesitant that it is worth less than Broadcom."。

IX. Some reflections about the times

Peter Tyre, in From 0 to 1, put forward an argument that made many entrepreneurs uncomfortable:Competition is for losers to create monopolies for real good firms。

"All failed firms are the same -- they have not escaped competition."

In investment, this framework forces you to ask a sharp question:Is this company that you're studying struggling in a competitive market, or is it in a market that it defines as a monopoly

The interesting thing about Marvell is it's doing two things at the same time。

Customize the AI chip field, which is Broadcom's chaser - the "participator"。

IN THE FIELD OF LIGHT INTERCONNECTION AND HIGH-SPEED DSP, IT IS AN ABSOLUTE MARKET LEADER, THE "MONOPOLY"。

The $2 billion investment in Inverda essentially confirms Marvell's monopolistic value on the dimension of Connect。

Tiel says one of the characteristics of monopolies is that markets are smaller than they look -“Monopoly enterprises often hide their monopoly position so as not to attract regulatory attention.”

Marvell, on the contrary:Its monopolistic position is ignored by the market because everyone's staring at the gap between it and Broadcom on custom chips。

Do a thought experiment: Marvell now has a market value of about 250 billion, corresponding to EY2027 about 11.5 billion in income, about21.7 Multimarket rate。But the 11.5 billion-mile data centre part is about 9.2 billion, growing at 50% plus。

The value of the block alone was 2300-2760 billion, valued separately on the basis of the Broadcom valuation multiplier (about 25-30 times market rate)。

The market gives $250 billion, equivalent to discounts on data centre operations and other business deliveries。

Of courseDivision valuation is too rough– The data centre operation in Marvell does not really get a multiple of Broadcom, with different Māori ratios, higher customer concentration and a weaker position for custom chips than Broadcom。

But it provides at least a starting point for thinking:Market pricing for Marvell is likely to remain the new reality of the old narrative, "This is the company that lost Trainium3," rather than "This is the only company in the world with a scalable income on the three battlefields of light DSP, silicon photons and custom-made AI chips."。

My judgment may be wrong. The competition for customized chips may be more intense than I thought, the growth in optical interconnection demand may be less optimistic than the model’s prediction, and Celestial AI’s 1 billion-year income target may not be met。

But now I'm willing to bet on "AI Connect." Not because Marvell was the best company, but because it was in the right place。

X. End of story: Light and civilization

Here, I want to skip the investment framework and say something bigger。

Every leap in human civilization, looking back, is not due to a single breakthrough, but to an escalation of "connection"。

Words allow ideas to pass through time, print works allow knowledge to flow across classes, telegrams allow information to reach across the oceans, and the Internet connects the brains of all human beings for the first time。

Each time, what really changes the world is not the content itself, but the speed and breadth of content flows。

THE AI ERA IS REPEATING THE SAME STORY。

We've focused too much on the brain -- bigger models, better calculations, smarter reasoning. But the brain never exists in isolation。

A MAN'S WISDOM, IF HE CANNOT COMMUNICATE WITH OTHERS, IS ONLY AN ISLAND. THE SAME HOLDS TRUE FOR THE 100,000 GPU CLUSTERS - IF DATA CANNOT MOVE FREELY BETWEEN THEM, THE STRENGTH OF THE CALCULATIONS IS JUST A SILENT SILICON。

Light is the messenger of this time。

From a physical point of view, light is the speed limit for the transmission of information in the universe。IT TOOK US THOUSANDS OF YEARS TO LEARN HOW TO HANDLE IT -- FROM THE PLASTER TO THE FIBER OPTICS, FROM MORSE CODE TO THE DSP SIGNAL PROCESSING OF 1.6T. NOW, WHEN HUMANS FIRST TRIED TO BUILD A REAL "SILICA BRAIN", WE WENT BACK TO THE SAME OLD PROBLEM: HOW CAN IDEAS, WHETHER CARBON- OR SILICON-BASED, FLOW AT THE SPEED OF LIGHT

Marvell's story, apparently, is a chip company that's been fighting for 10 years. But deep down, it touches on a more fundamental proposition: in any complex system, the value of "connection" will eventually outweigh the value of "node."。

In the Internet age, the total value of routers and fibre-optics ultimately exceeded that of any server。

In the age of social networking, the platform is worth more than any content creator。

IN THE AI ERA, THE SAME LOGIC IS HAPPENING AGAIN — WHEN EVERYONE FIGHTS FOR THE CROWN OF THE STRONGEST BRAIN, THE REAL WINNER IS PROBABLY THE MAN WHO WOVEN THE NEURAL NETWORK。

We are standing at a magical and delicate historical node. For the first time, human beings are capable of building something smarter than themselves, and whether this thing is really "smart" depends on whether we can solve a seemingly ordinary engineering problem: free travel between the chips。

The thing itself is a poem。

Original Link